Emission3 Blog

Stay ahead of the compliance curve with insights on CBAM, SB 253, CSRD, and the future of carbon accountability.

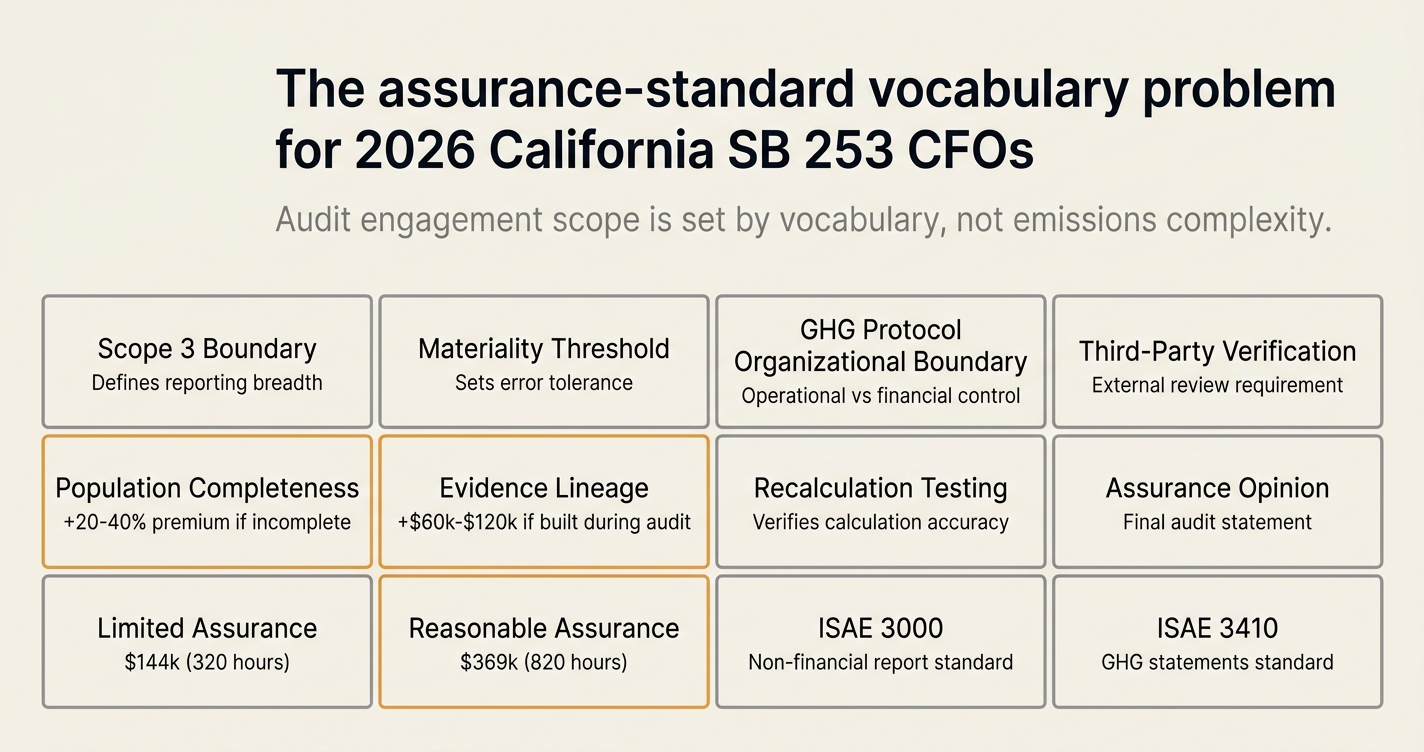

The assurance-standard vocabulary problem for 2026 California SB 253 CFOs

SB 253 CFO compliance consists of emissions totals and assurance vocabulary. Finance teams budget for the first—but audit engagement scope is set by the second.

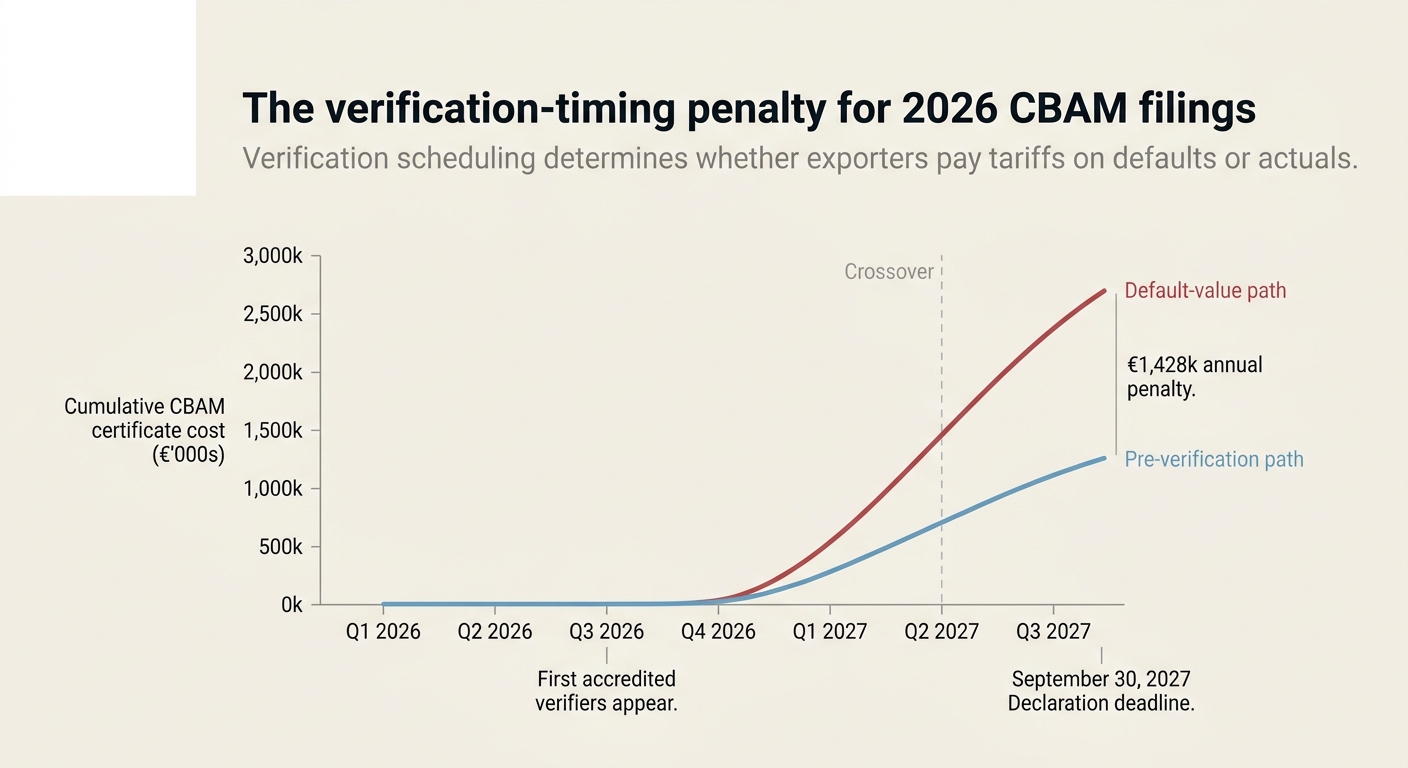

The verification-timing penalty for 2026 CBAM filings

CBAM filings consist of declared emissions and verification scheduling. Exporters focus on the first—but the tariff cost is set by the second.

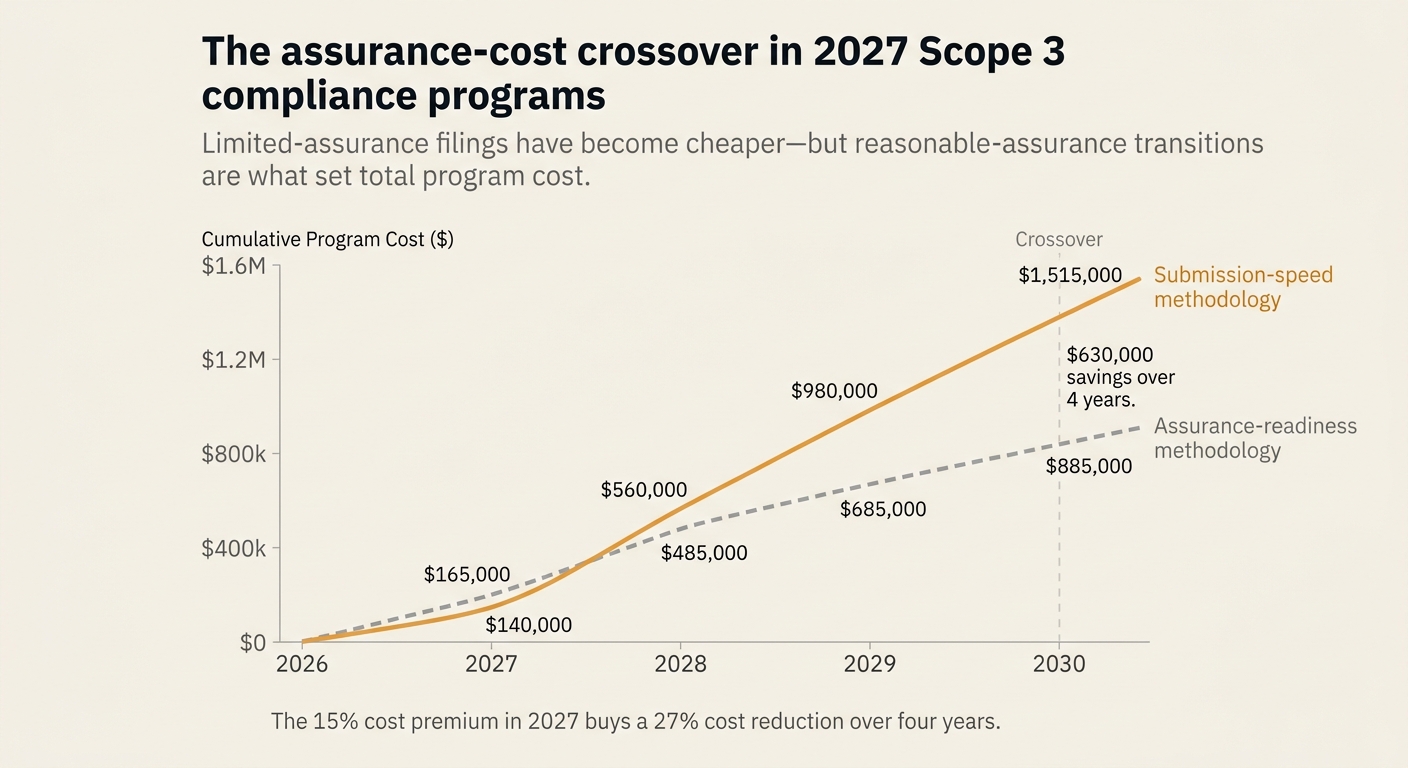

The assurance-cost crossover in 2027 Scope 3 compliance programs

Scope 3 compliance consists of limited-assurance filings and reasonable-assurance transitions. CFOs budget for the first—but 2027 audit fees are set by the second.

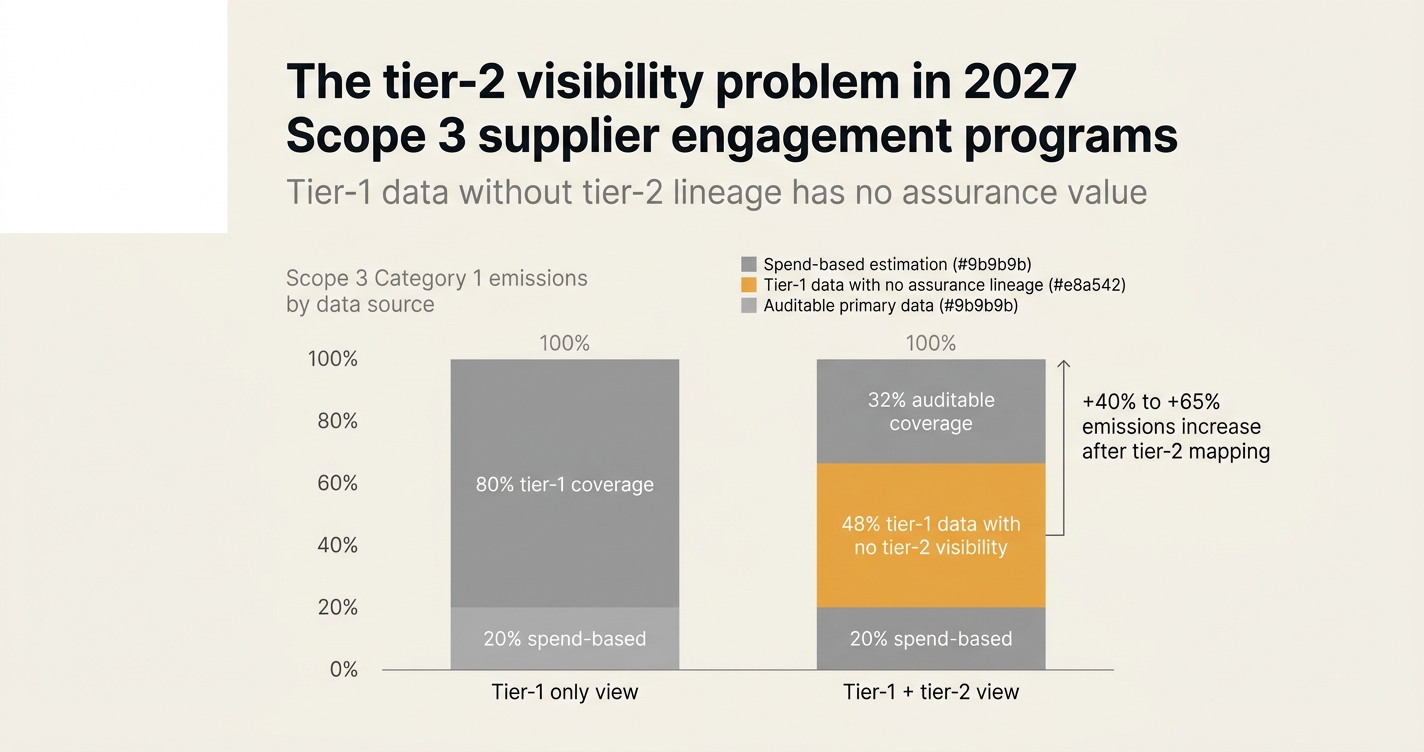

The tier-2 visibility problem in 2027 Scope 3 supplier engagement programs

Scope 3 engagement consists of two things: tier-1 supplier data and tier-2 visibility. Procurement teams optimize for the first—but 60% of emissions live in the second.

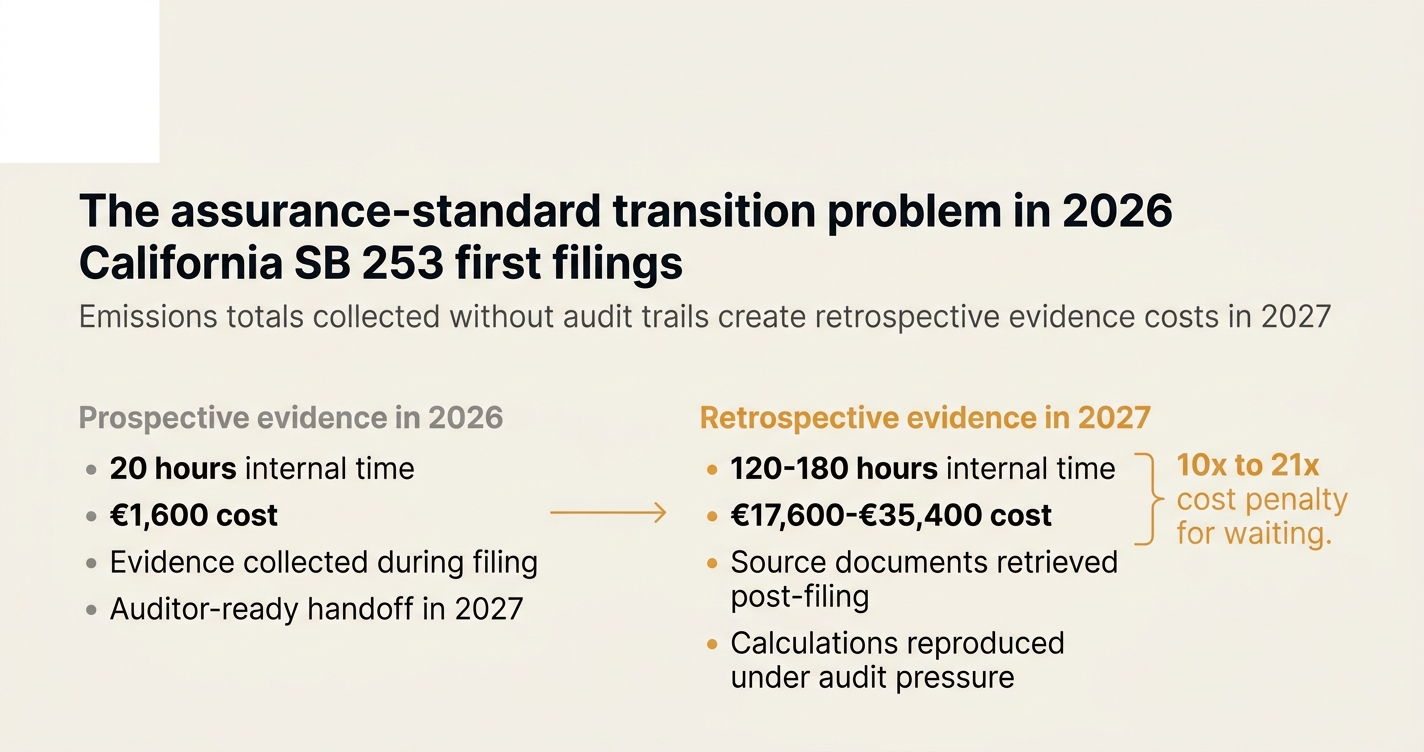

The assurance-standard transition problem in 2026 California SB 253 first filings

SB 253 filings consist of two things: emissions totals and assurance methodology. CFOs budget for the first—but 2027 audit fees are set by the second.

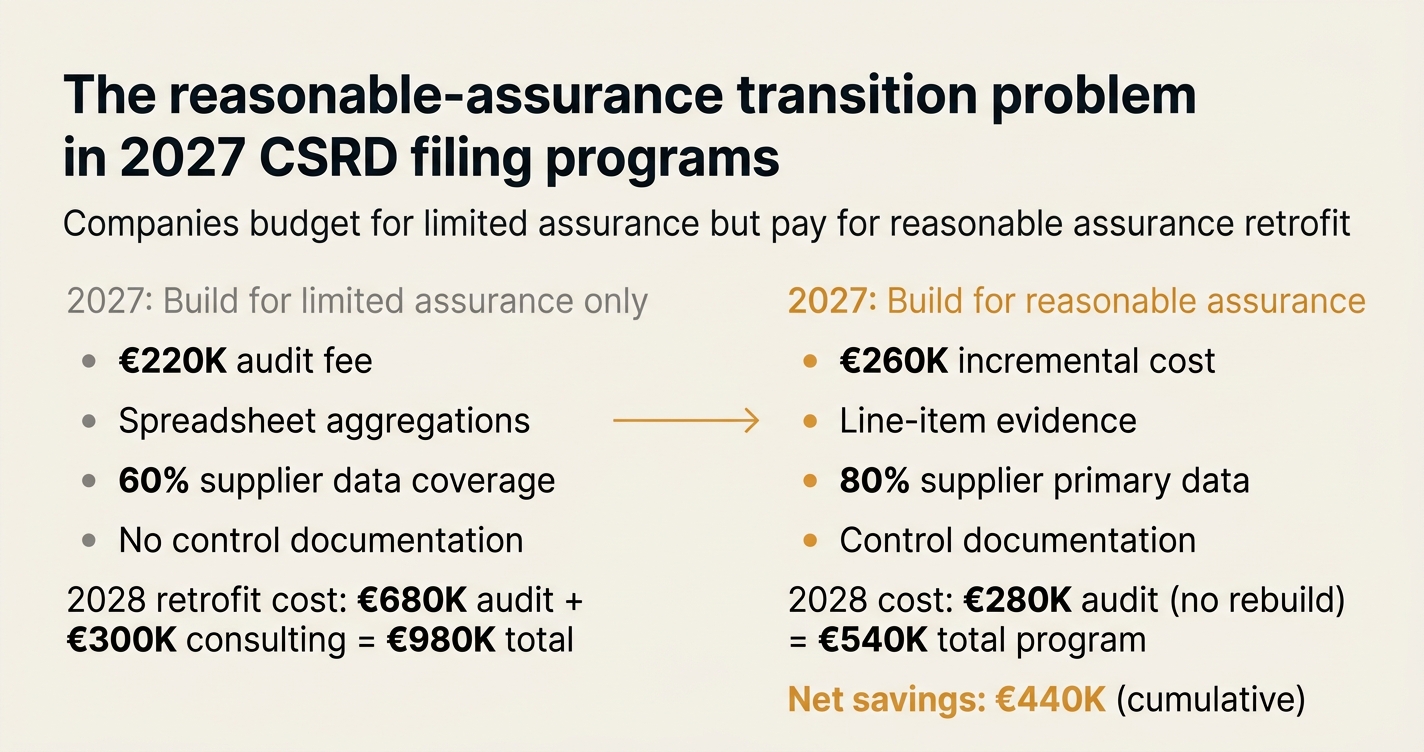

The reasonable-assurance transition problem in 2027 CSRD filing programs

CSRD filings consist of two things: sustainability data and assurance methodology. Companies budget for limited assurance—but 2028 reasonable assurance is what sets total program cost.

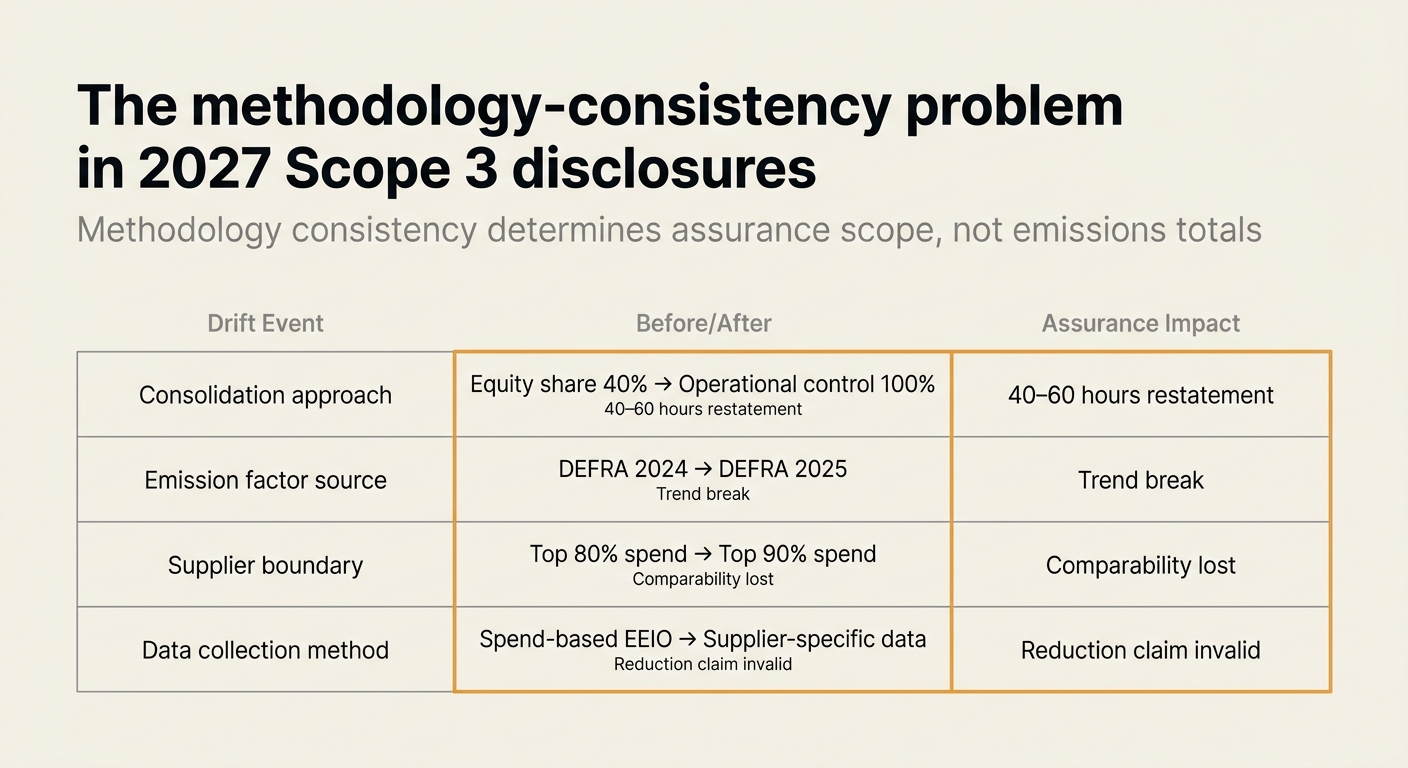

The methodology-consistency problem in 2027 Scope 3 disclosures

Scope 3 disclosure consists of two things: emissions totals and methodology consistency across reporting years. Teams focus on the first—but assurance scope is set by the second.

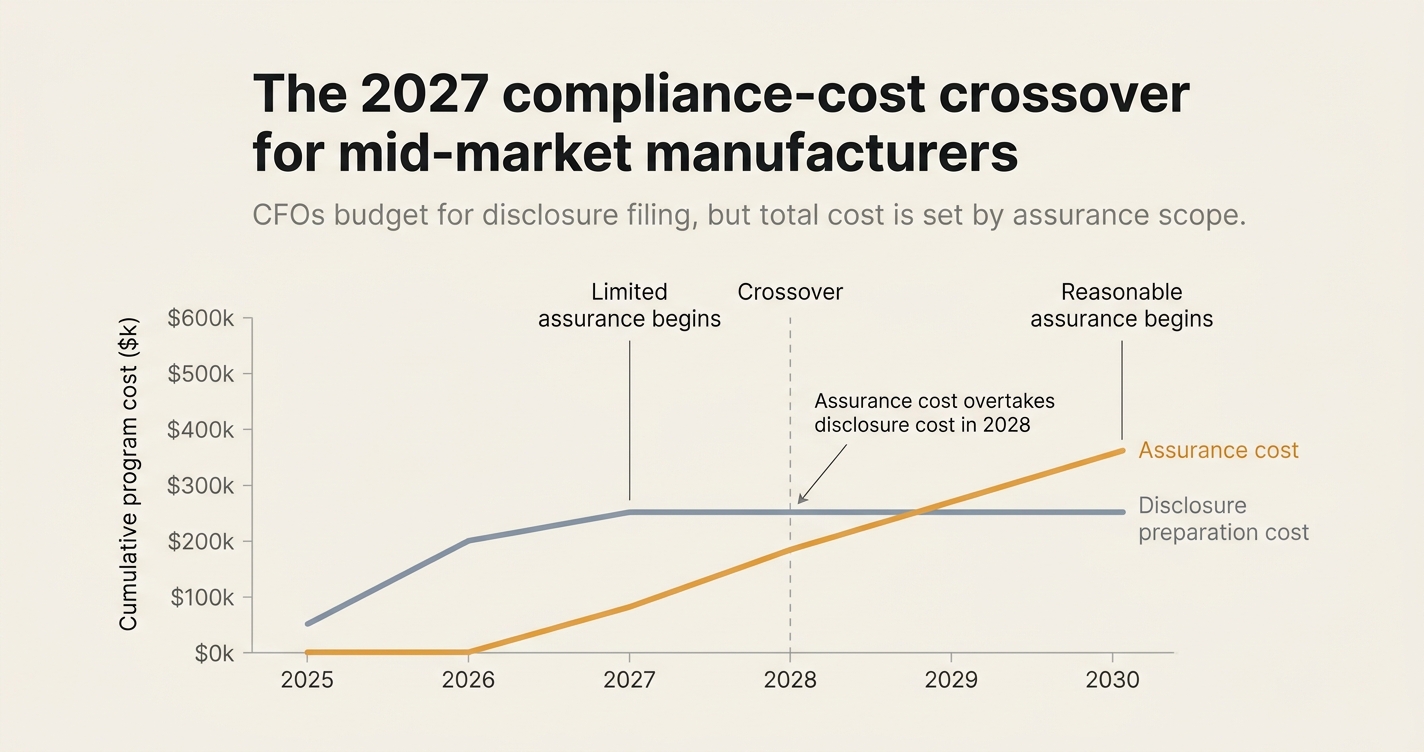

The 2027 compliance-cost crossover for mid-market manufacturers

2027 compliance consists of two things: disclosure filing and assurance cost. CFOs budget for the first—but total program cost is set by the second.

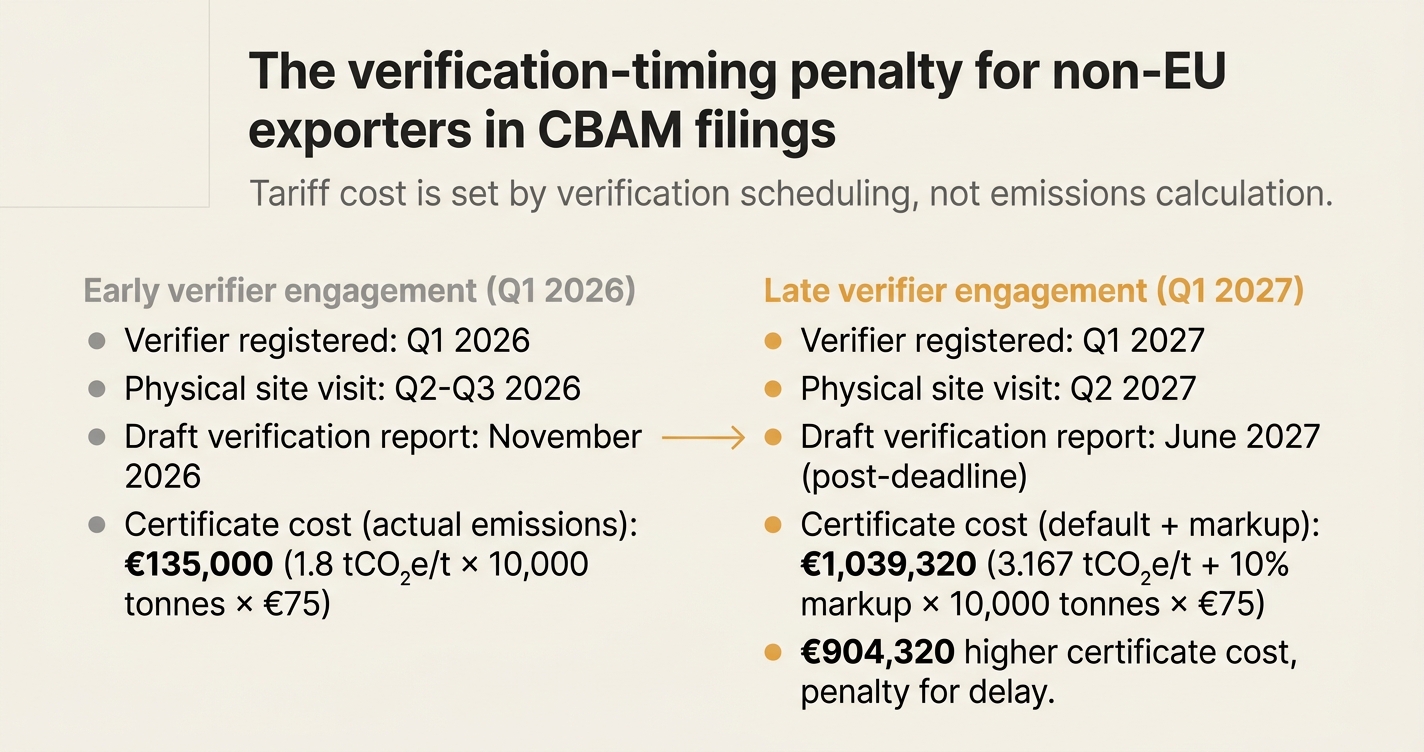

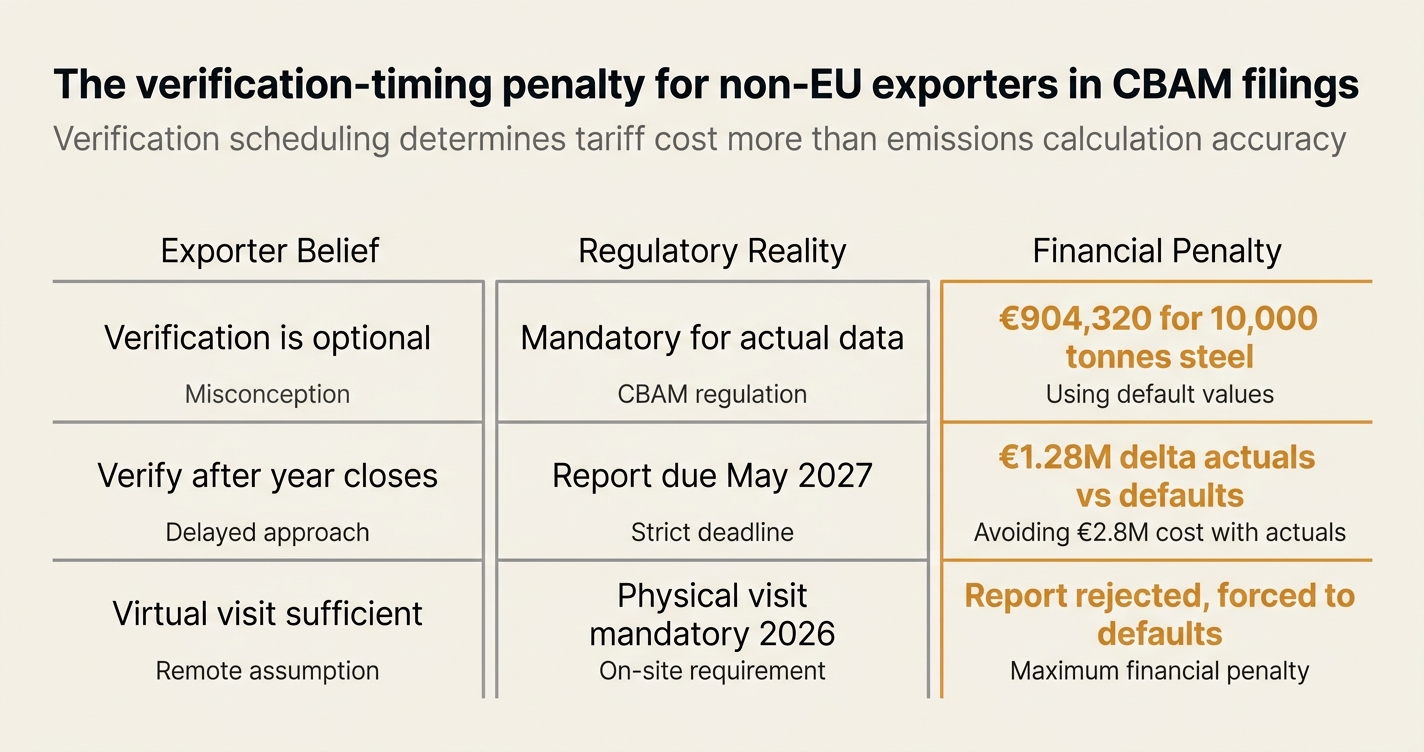

The verification-timing penalty for non-EU exporters in CBAM filings

CBAM filings consist of two things: embedded emissions totals and verification scheduling. Exporters focus on the first—but the tariff cost is set by the second.

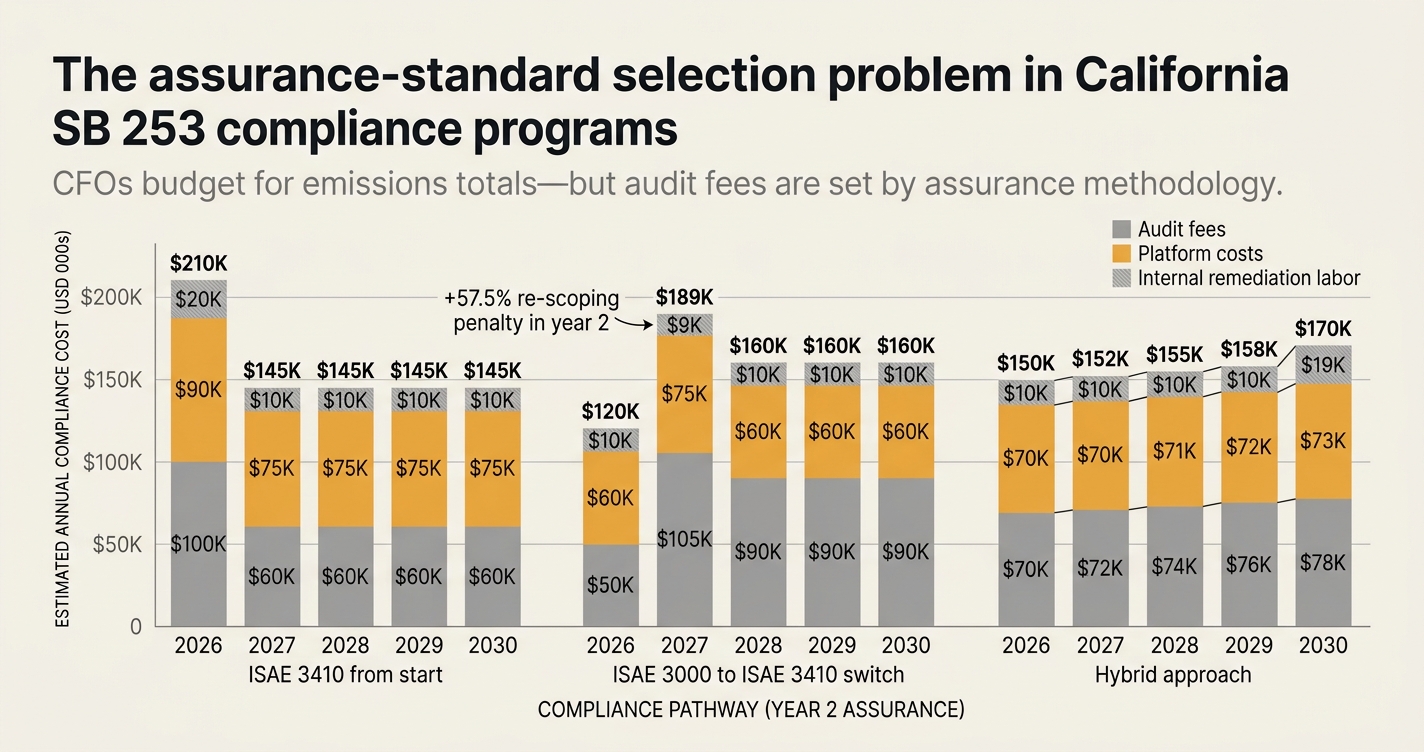

The assurance-standard selection problem in California SB 253 compliance programs

SB 253 filings consist of two things: emissions totals and assurance methodology. CFOs budget for the first—but audit fees are set by the second.

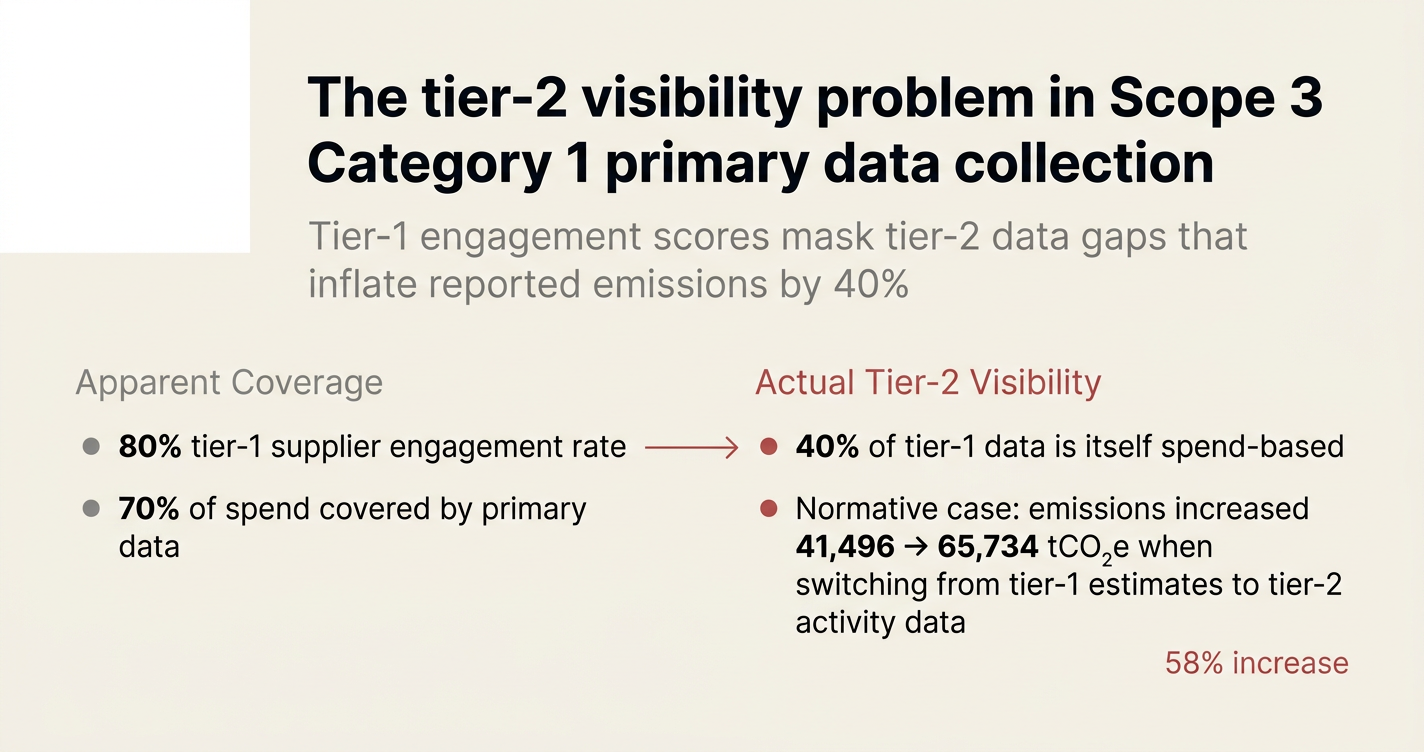

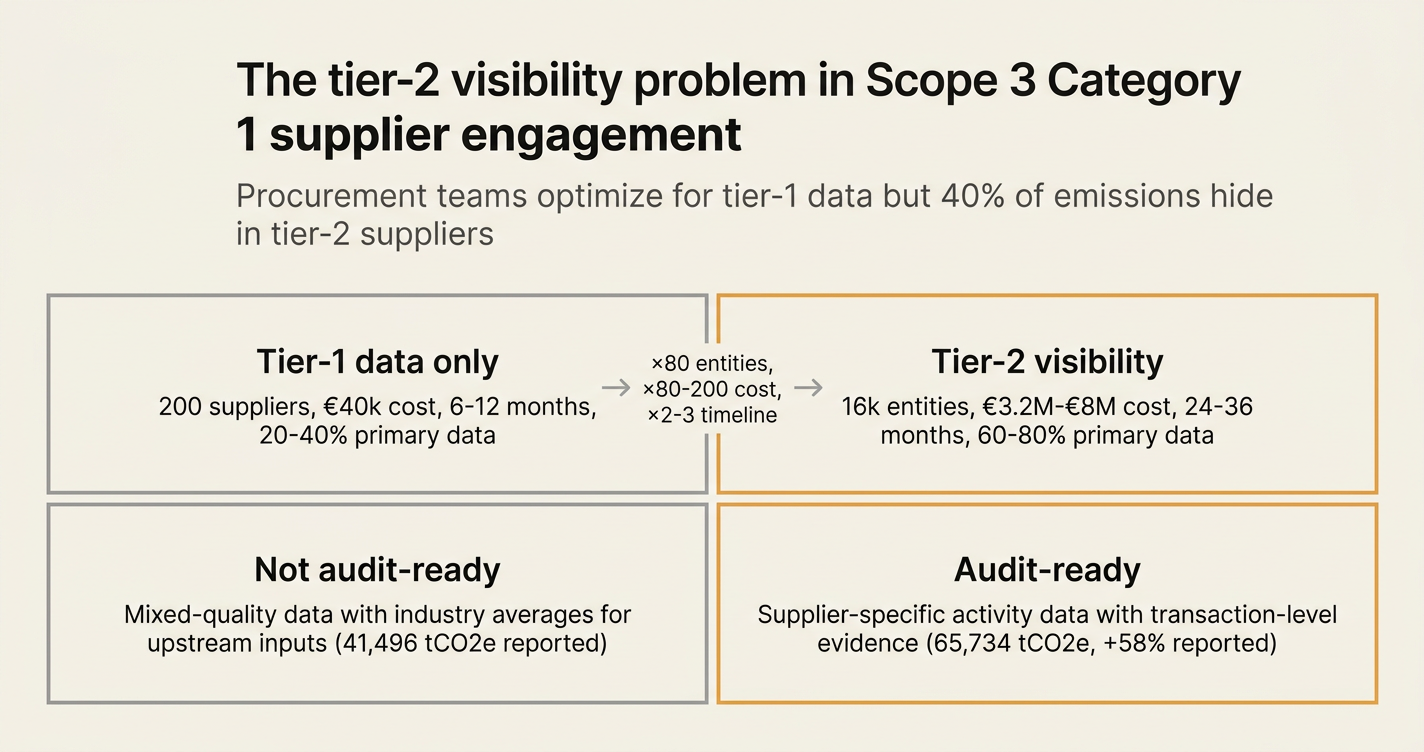

The tier-2 visibility problem in Scope 3 Category 1 primary data collection

Scope 3 Category 1 consists of two things: tier-1 supplier engagement and tier-2 data availability. Procurement teams optimize for the first—but 60% of emissions live in the second.

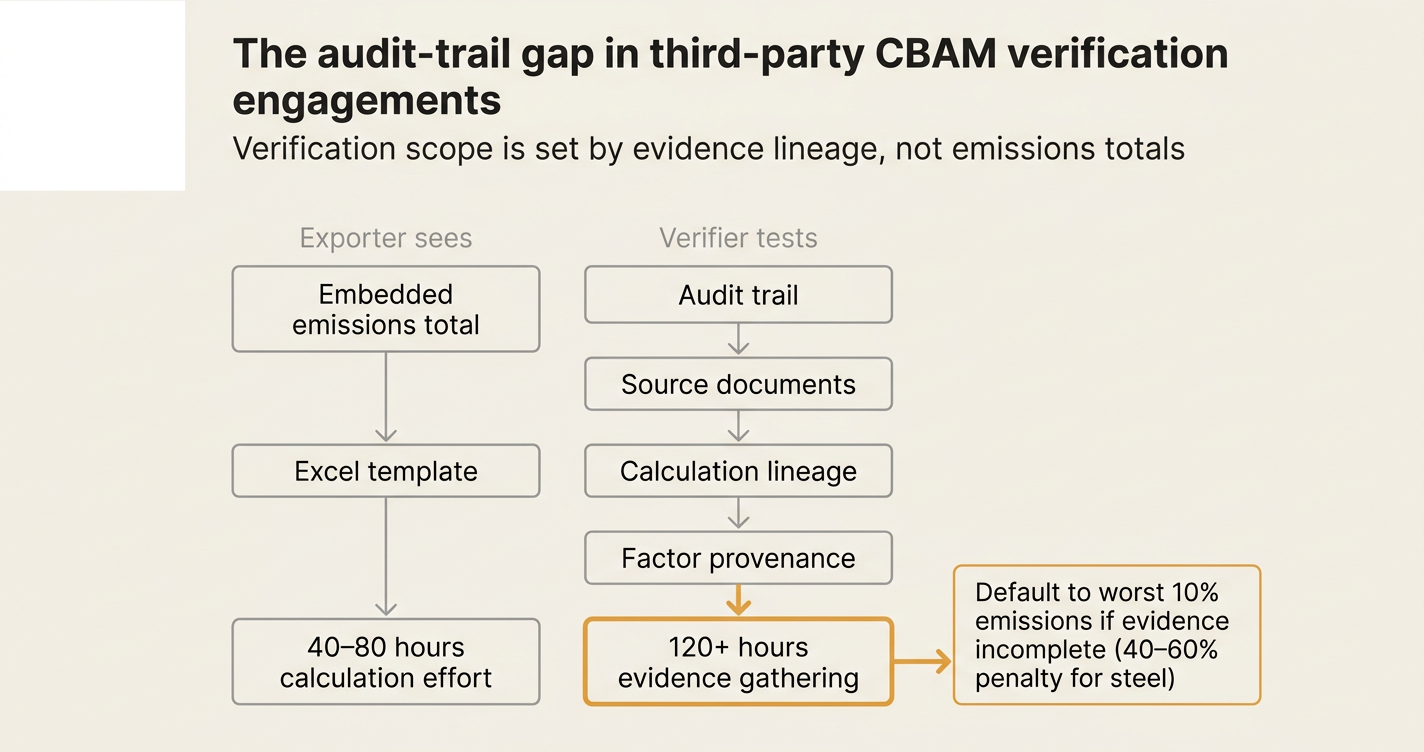

The audit-trail gap in third-party CBAM verification engagements

CBAM verification consists of two things: embedded emissions totals and evidence lineage. Exporters budget for the first—but auditor scope is set by the second.

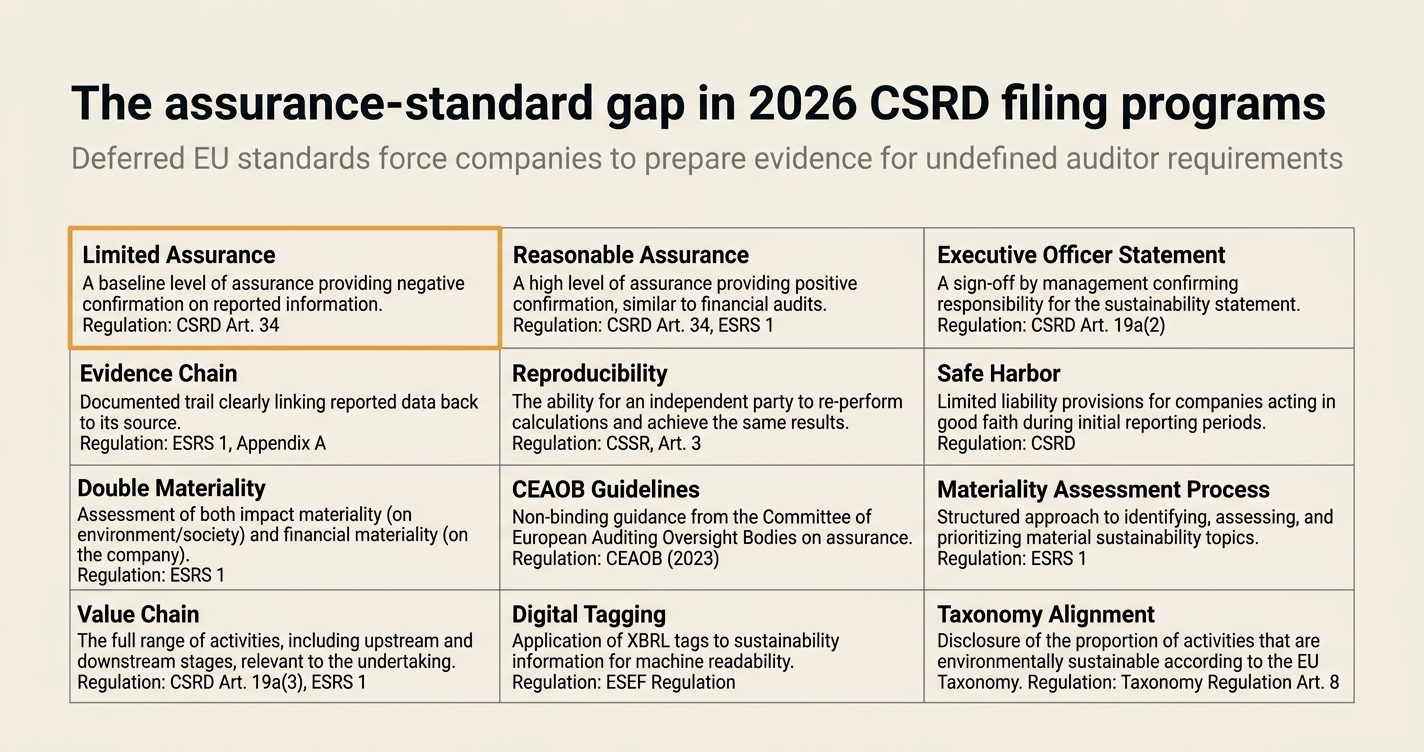

The assurance-standard gap in 2026 CSRD filing programs

CSRD filings consist of two things: sustainability data and assurance methodology. Companies budget for the first—but auditor scope is set by the second.

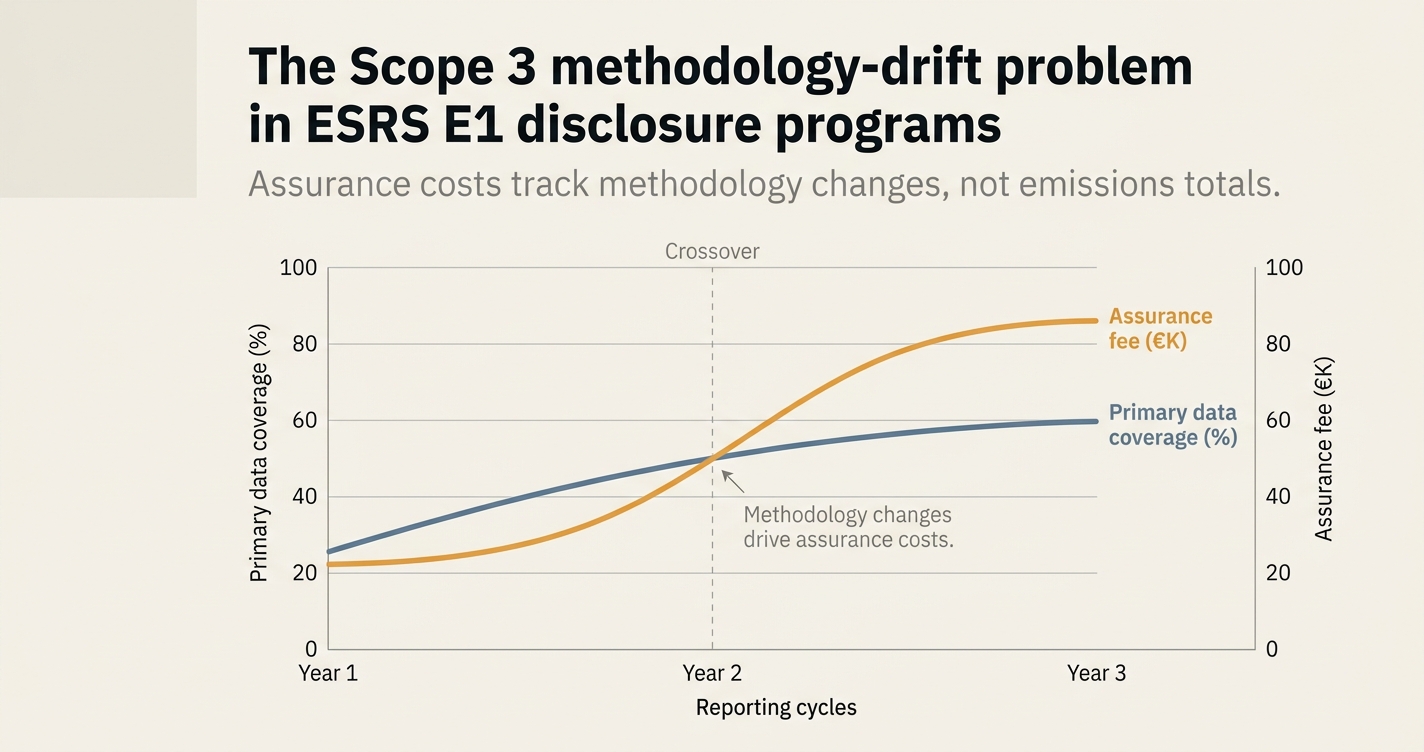

The Scope 3 methodology-drift problem in ESRS E1 disclosure programs

ESRS E1 disclosure consists of two things: emissions totals and methodology consistency across reporting years. Teams focus on the first—but assurance scope is set by the second.

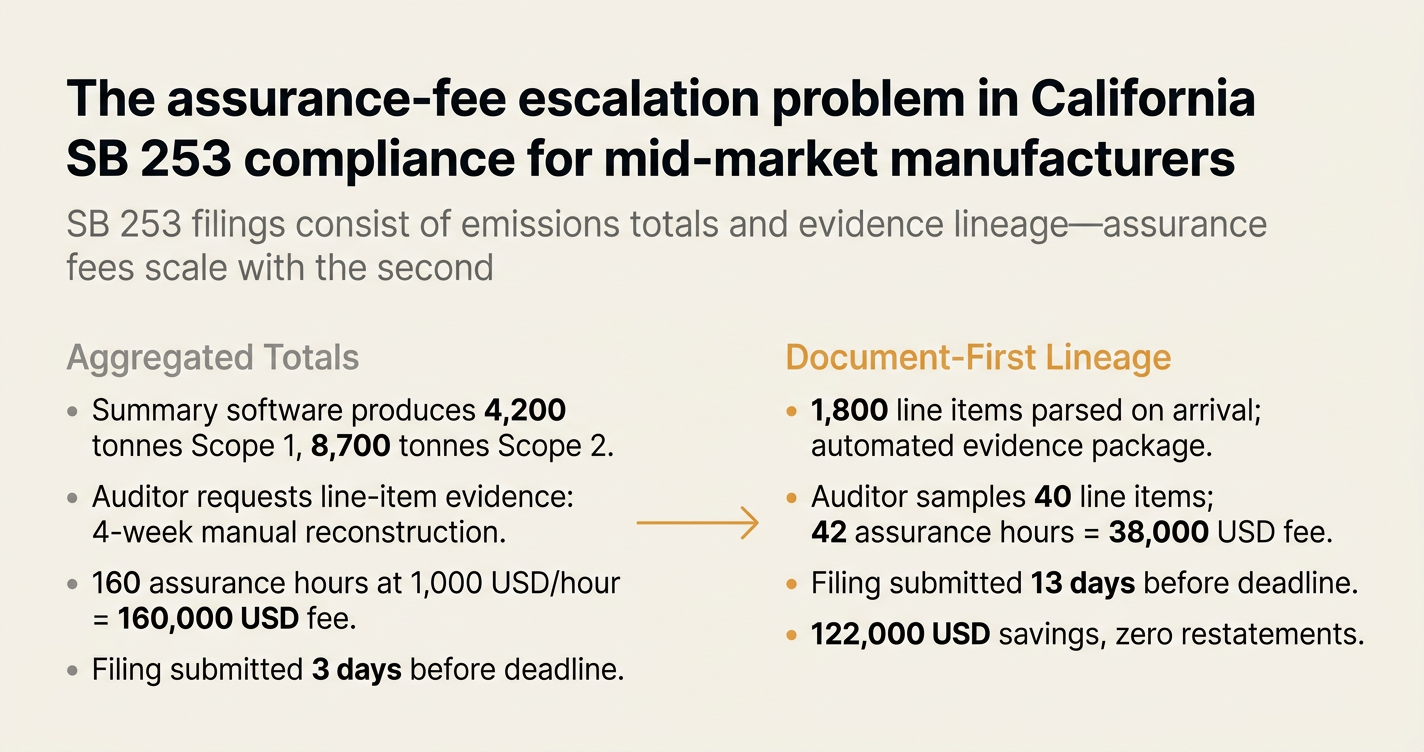

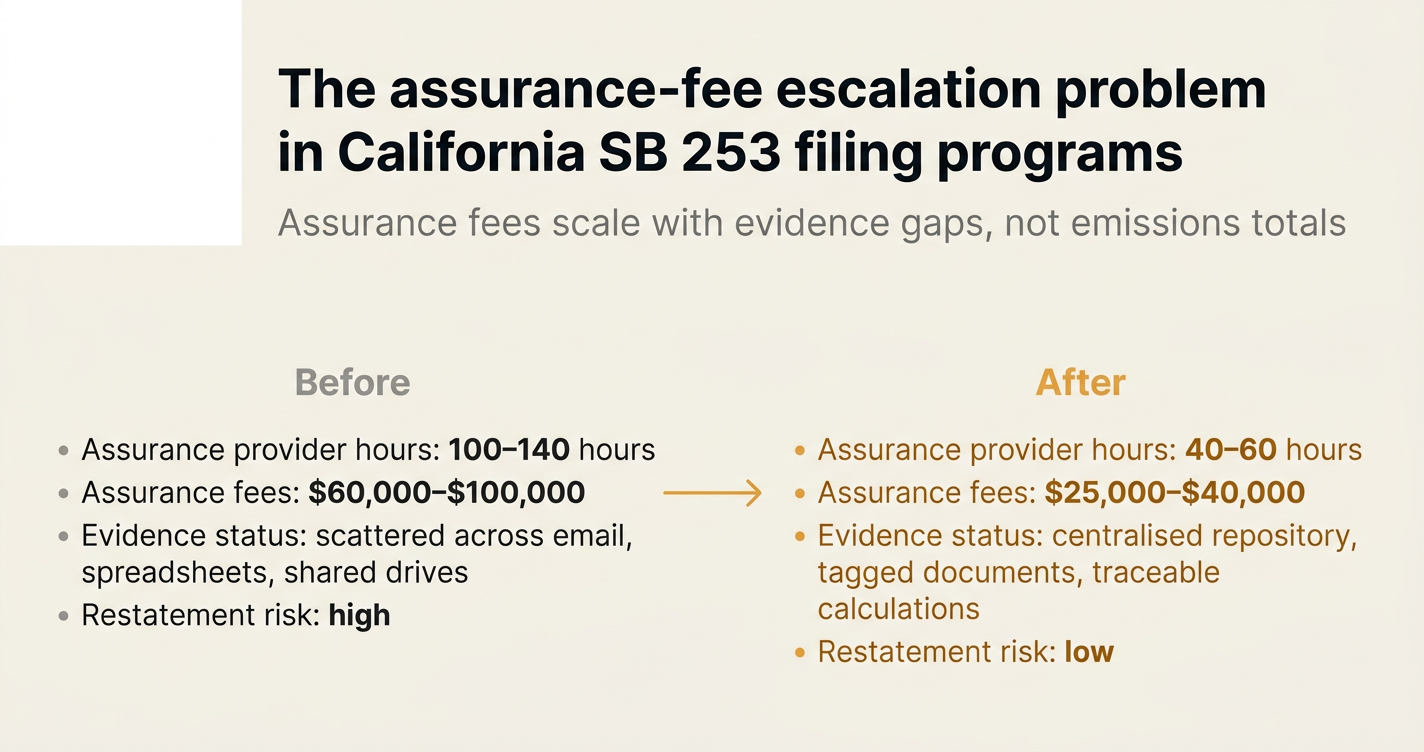

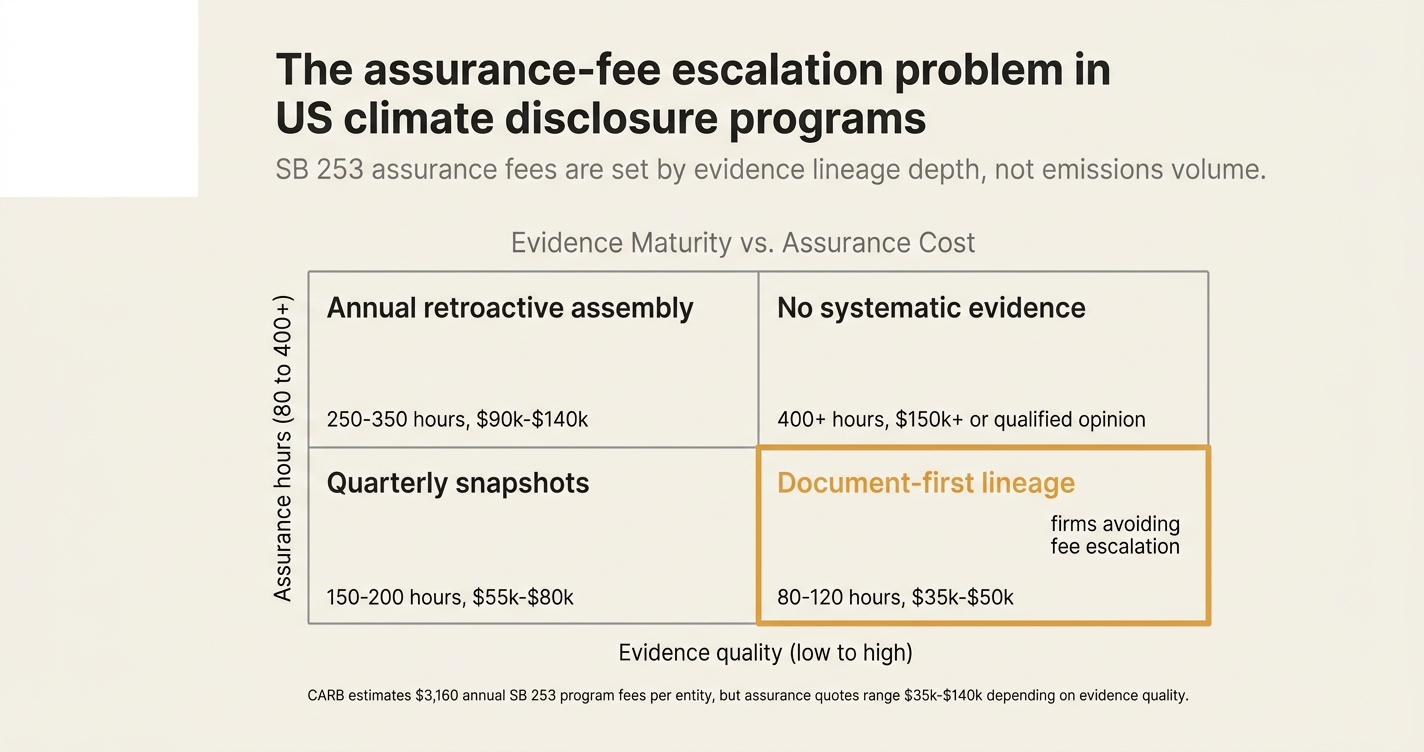

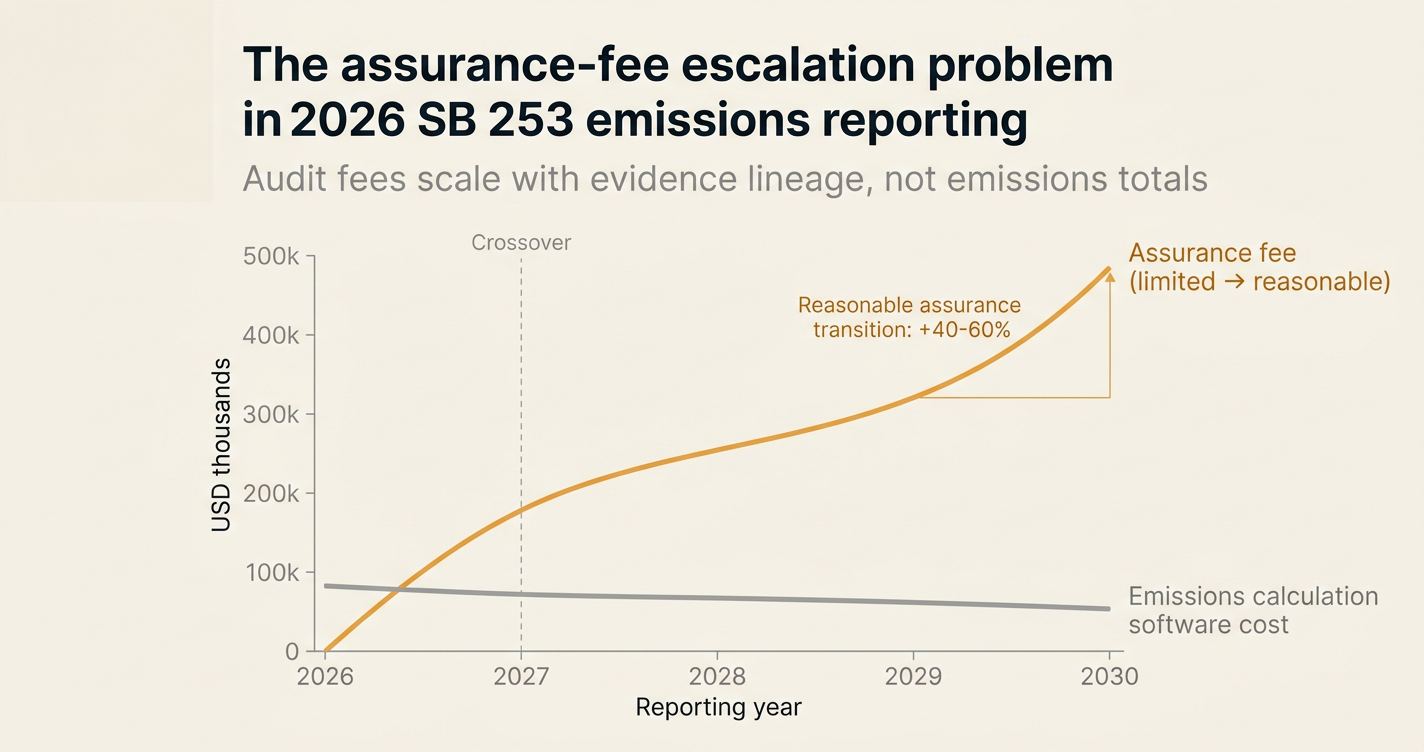

The assurance-fee escalation problem in California SB 253 compliance for mid-market manufacturers

SB 253 filings consist of two things: emissions totals and evidence lineage. CFOs budget for the first—but assurance fees are set by the second.

The verification-timing penalty for non-EU exporters in CBAM filings

CBAM filings consist of two things: embedded emissions totals and verification scheduling. Exporters focus on the first—but the tariff cost is set by the second.

The assurance-fee escalation problem in California SB 253 filing programs

SB 253 filings consist of two things: emissions totals and evidence lineage. CFOs budget for the first—but assurance fees are set by the second.

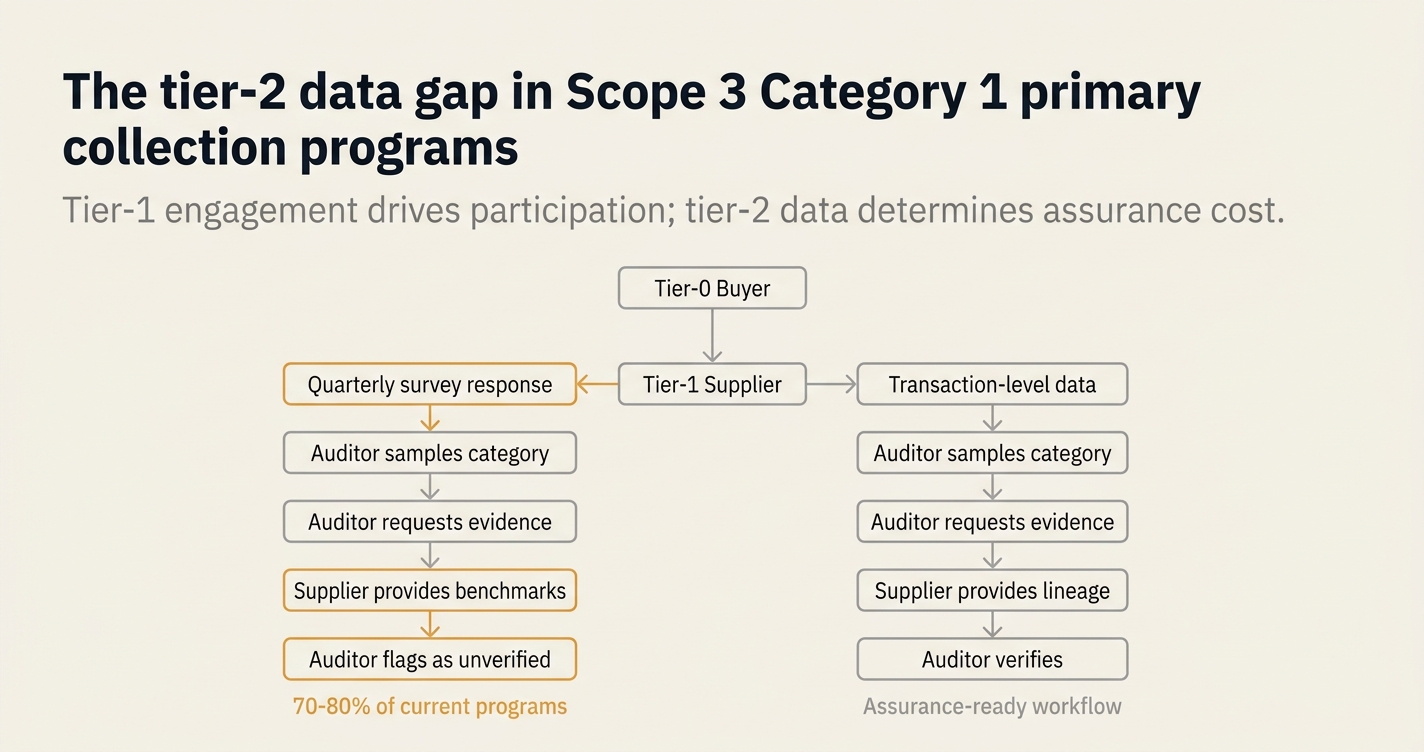

The tier-2 data gap in Scope 3 Category 1 primary collection programs

Scope 3 Category 1 consists of two things: tier-1 supplier engagement and tier-2 data availability. Procurement teams optimize for the first—but 60% of actual emissions live in the second.

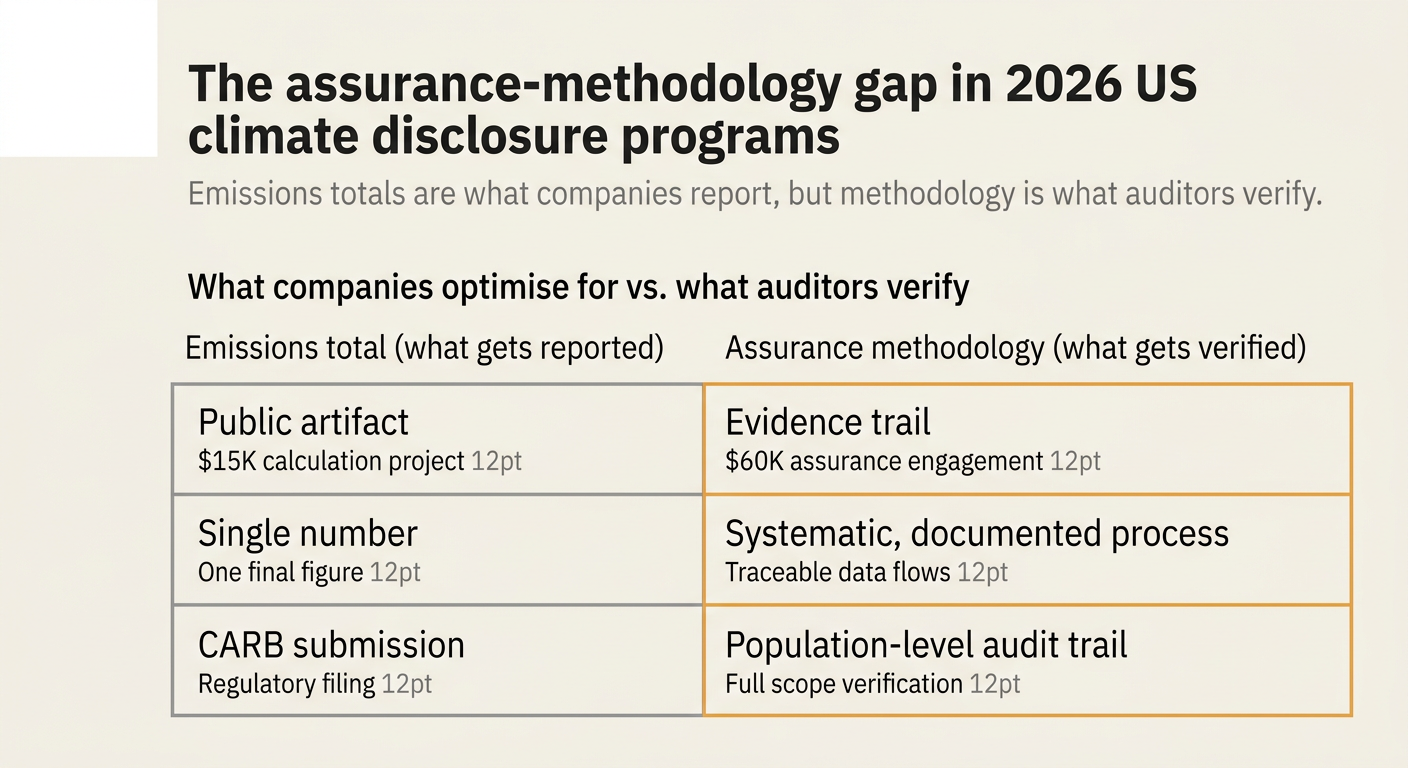

The assurance-methodology gap in 2026 US climate disclosure programs

US climate disclosure consists of two things: emissions totals and assurance methodology. Companies budget for the first—but auditor scope is set by the second.

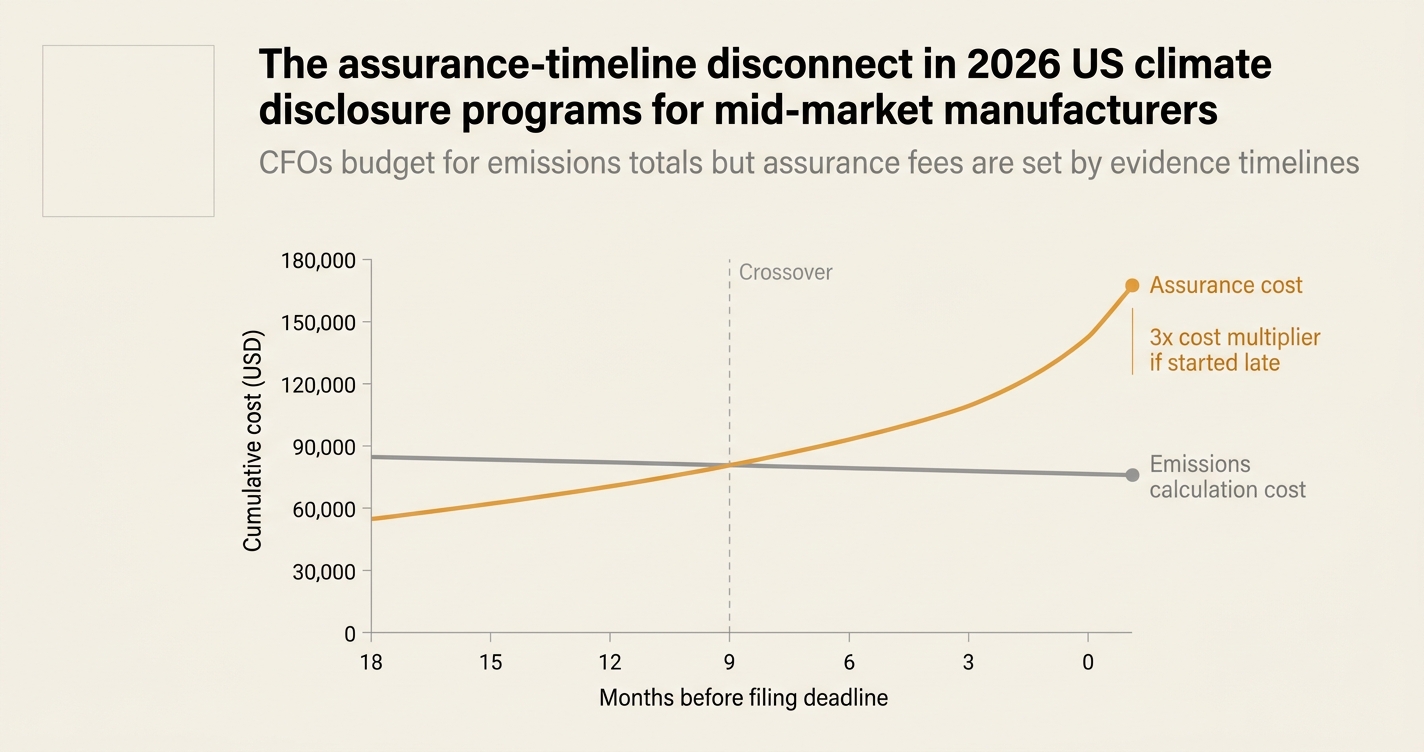

The assurance-timeline disconnect in 2026 US climate disclosure programs for mid-market manufacturers

US climate disclosure consists of two things: emissions totals and evidence-gathering timelines. CFOs budget for the first—but assurance fees are set by the second.

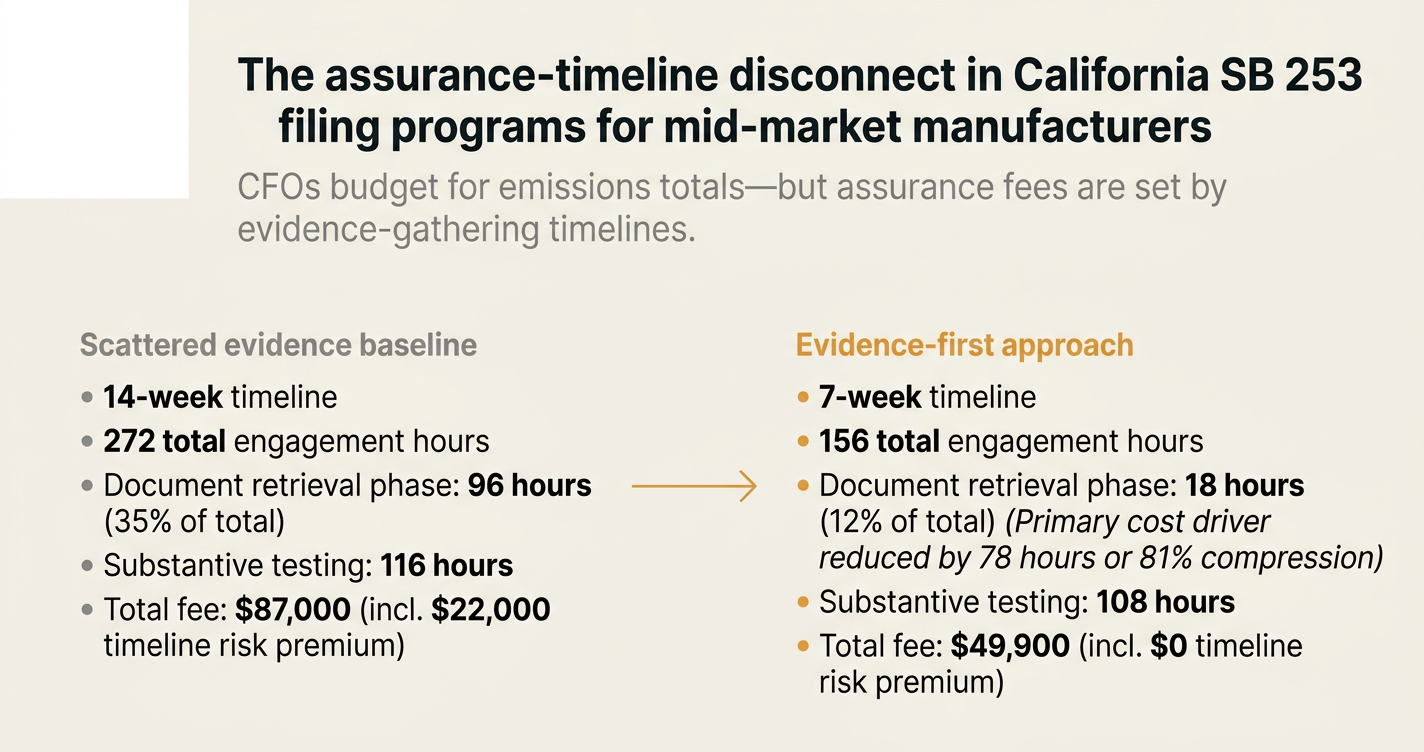

The assurance-timeline disconnect in California SB 253 filing programs for mid-market manufacturers

California SB 253 filings consist of two things: emissions totals and evidence-gathering timelines. CFOs budget for the first—but assurance fees are set by the second.

The assurance-fee escalation problem in US climate disclosure programs

SB 253 compliance consists of two things: emissions totals and evidence lineage. CFOs budget for the first—but assurance fees are set by the second.

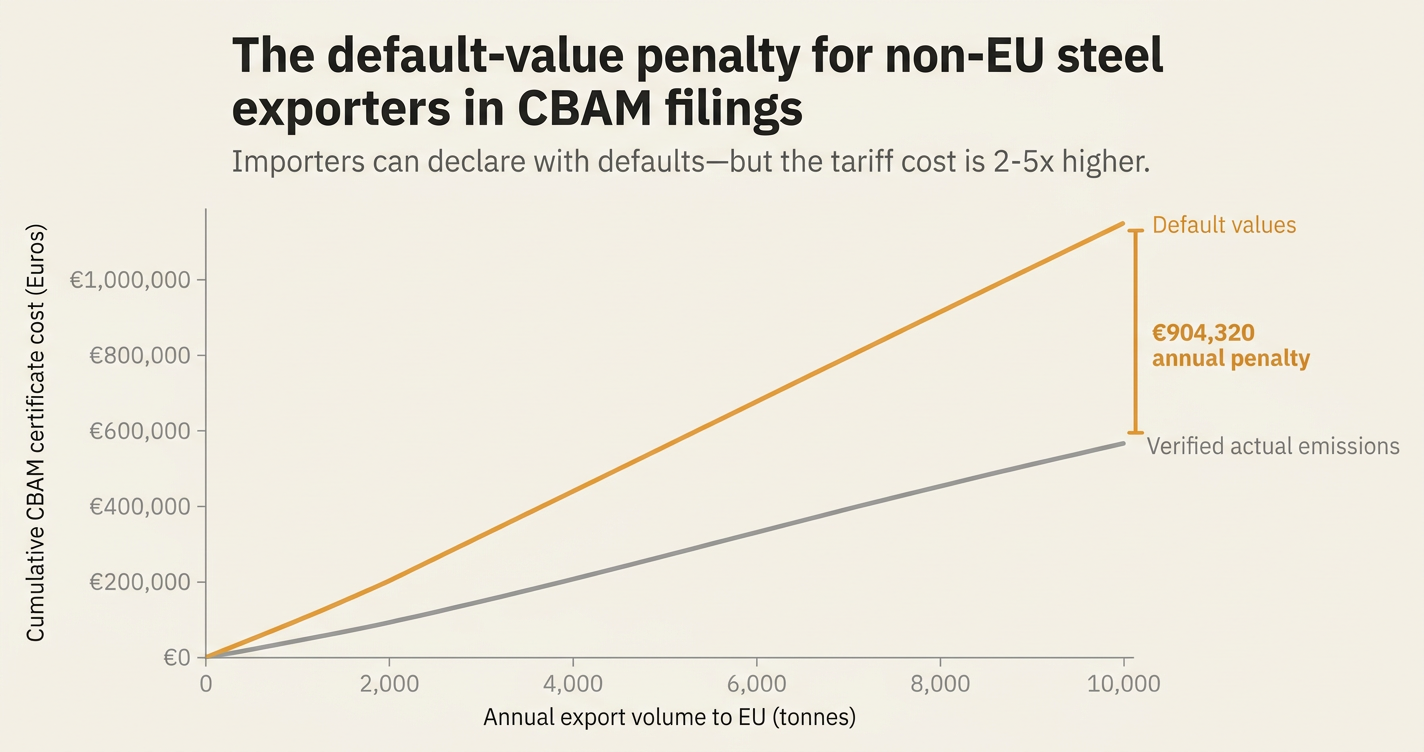

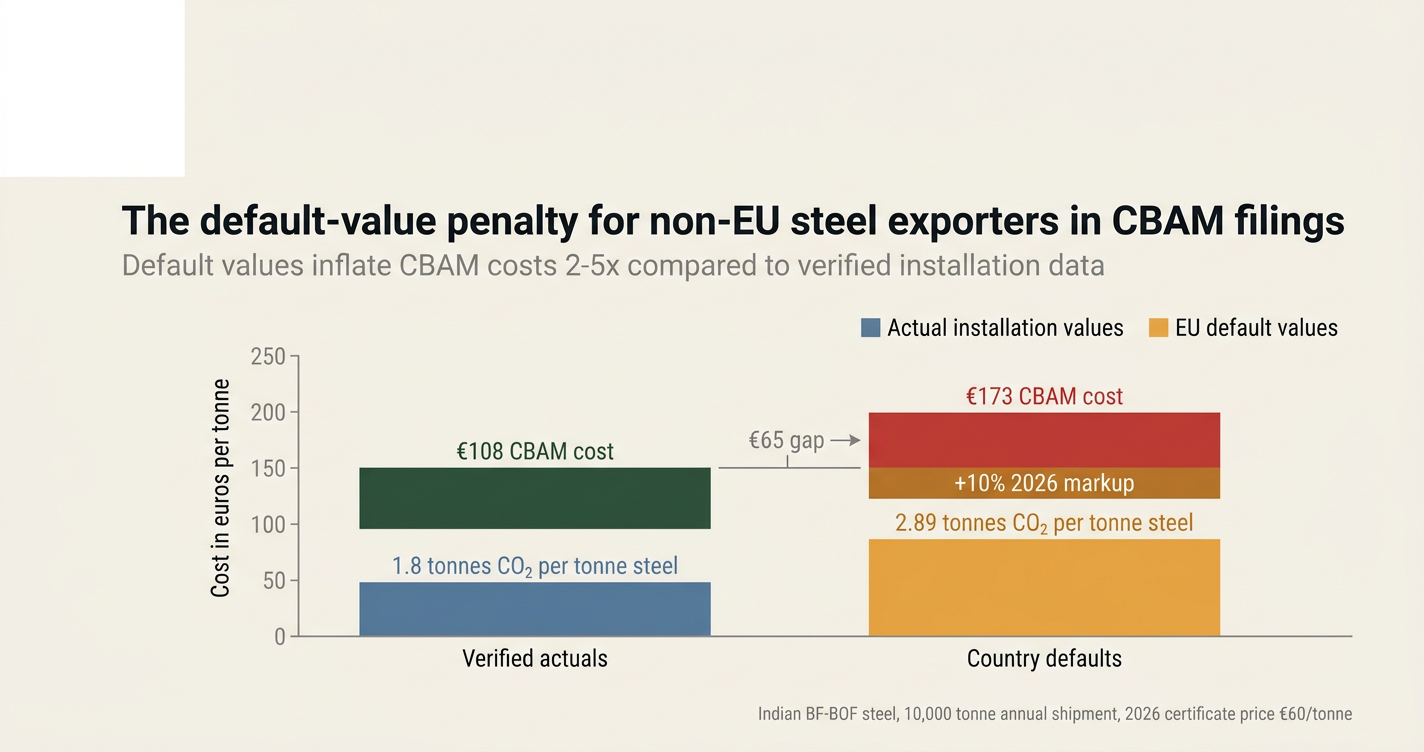

The default-value penalty for non-EU steel exporters in CBAM filings

CBAM filings consist of two things: embedded emissions totals and installation-level data. Importers can declare with defaults—but the tariff cost is 2-5x higher.

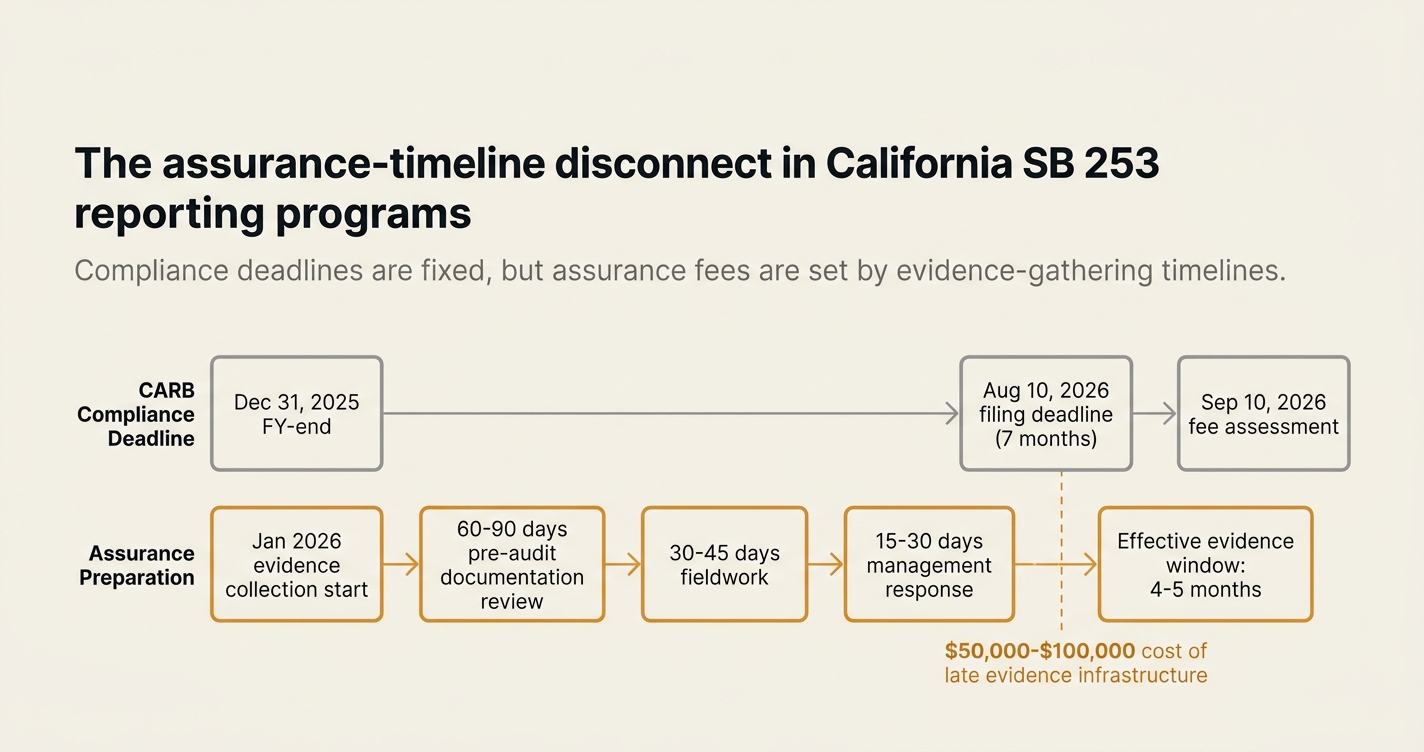

The assurance-timeline disconnect in California SB 253 reporting programs

SB 253 reporting consists of two things: emissions totals and evidence-gathering timelines. Companies budget for the first—but assurance fees are set by the second.

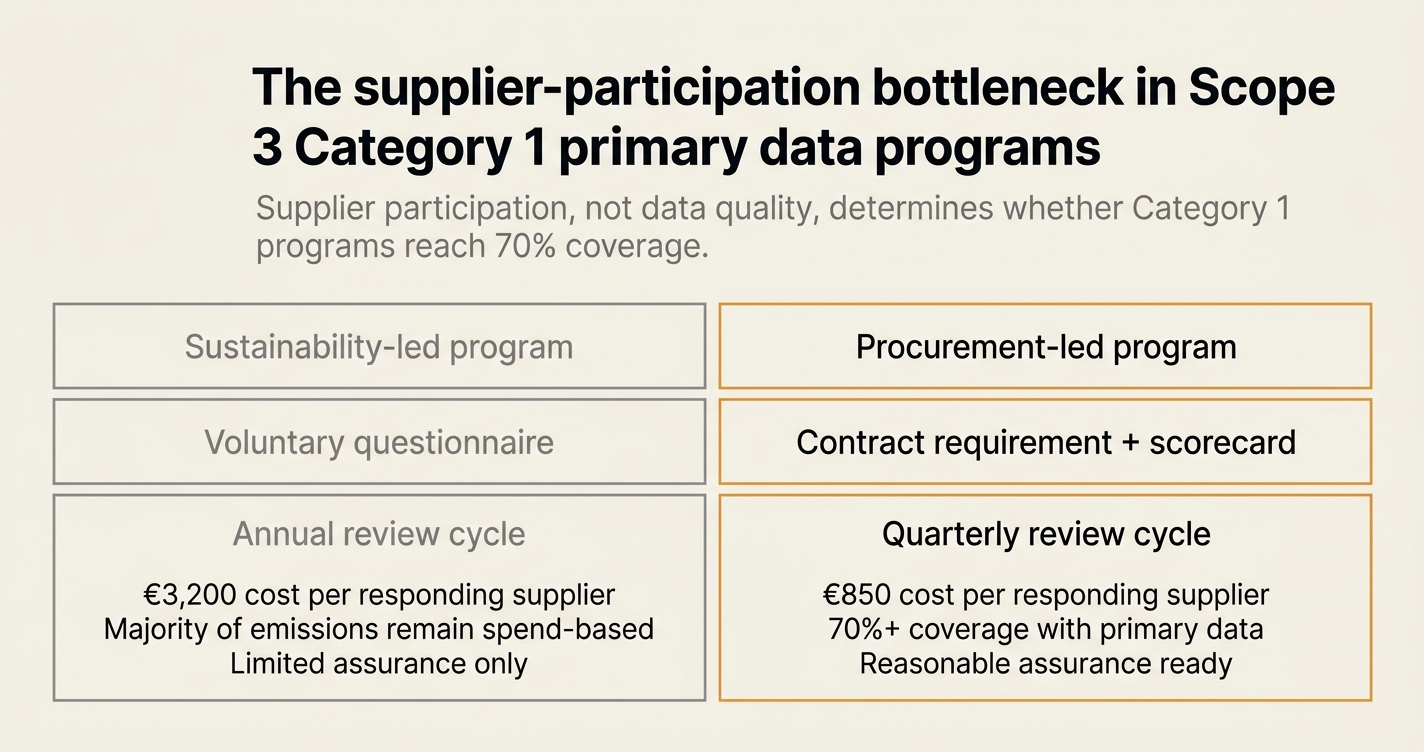

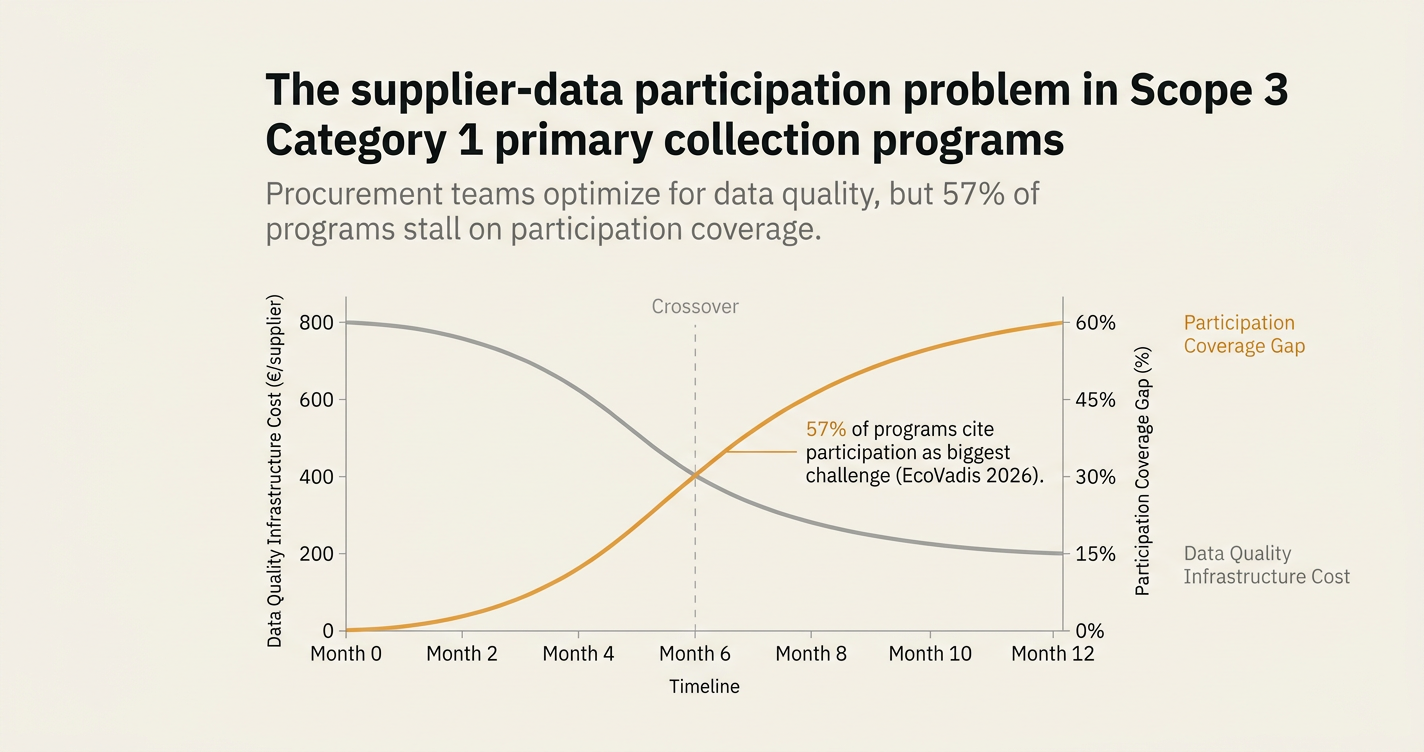

The supplier-participation bottleneck in Scope 3 Category 1 primary data programs

Scope 3 Category 1 primary collection consists of two things: supplier participation and data quality. Procurement teams optimize for the second—but 57% of programs stall on the first.

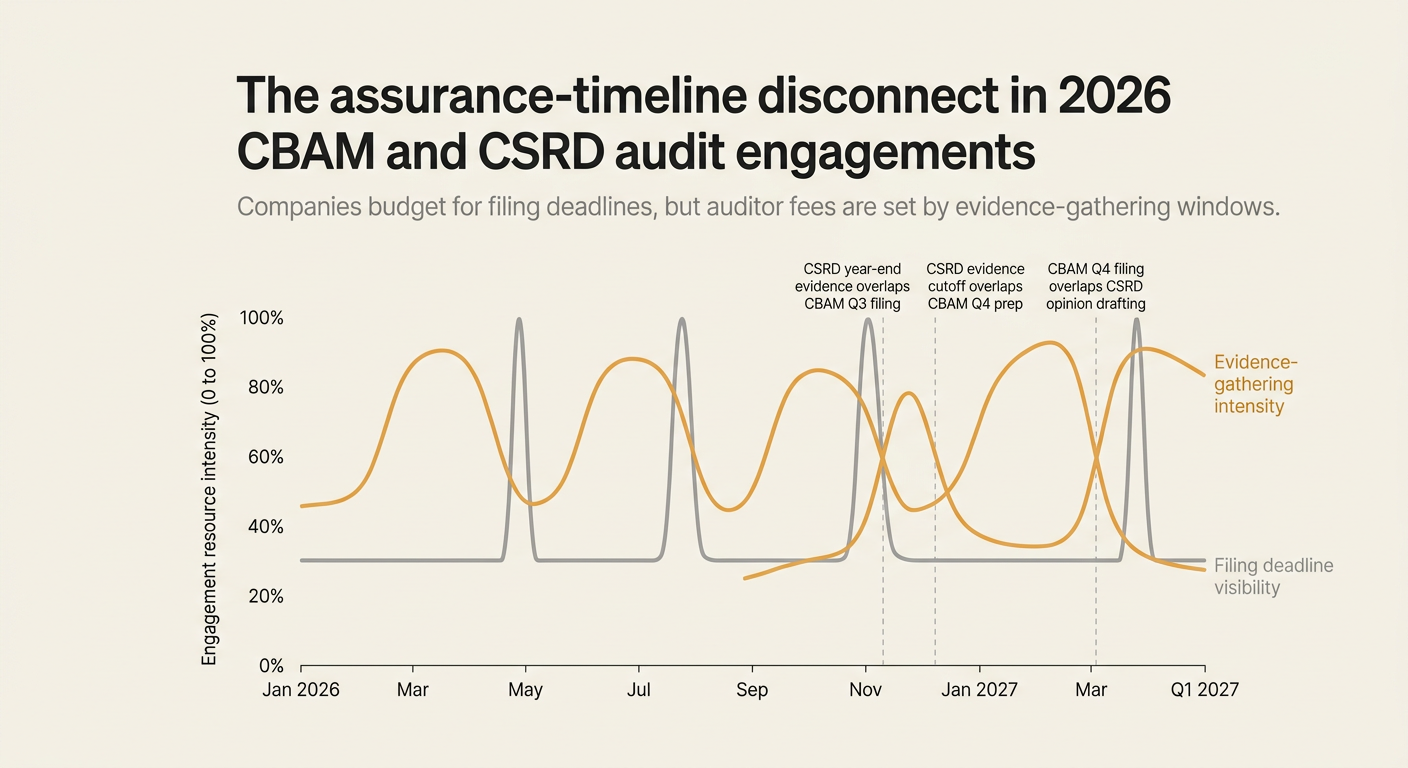

The assurance-timeline disconnect in 2026 CBAM and CSRD audit engagements

CBAM and CSRD assurance consists of two things: compliance deadlines and evidence-gathering timelines. Companies budget for the first—but auditor fees are set by the second.

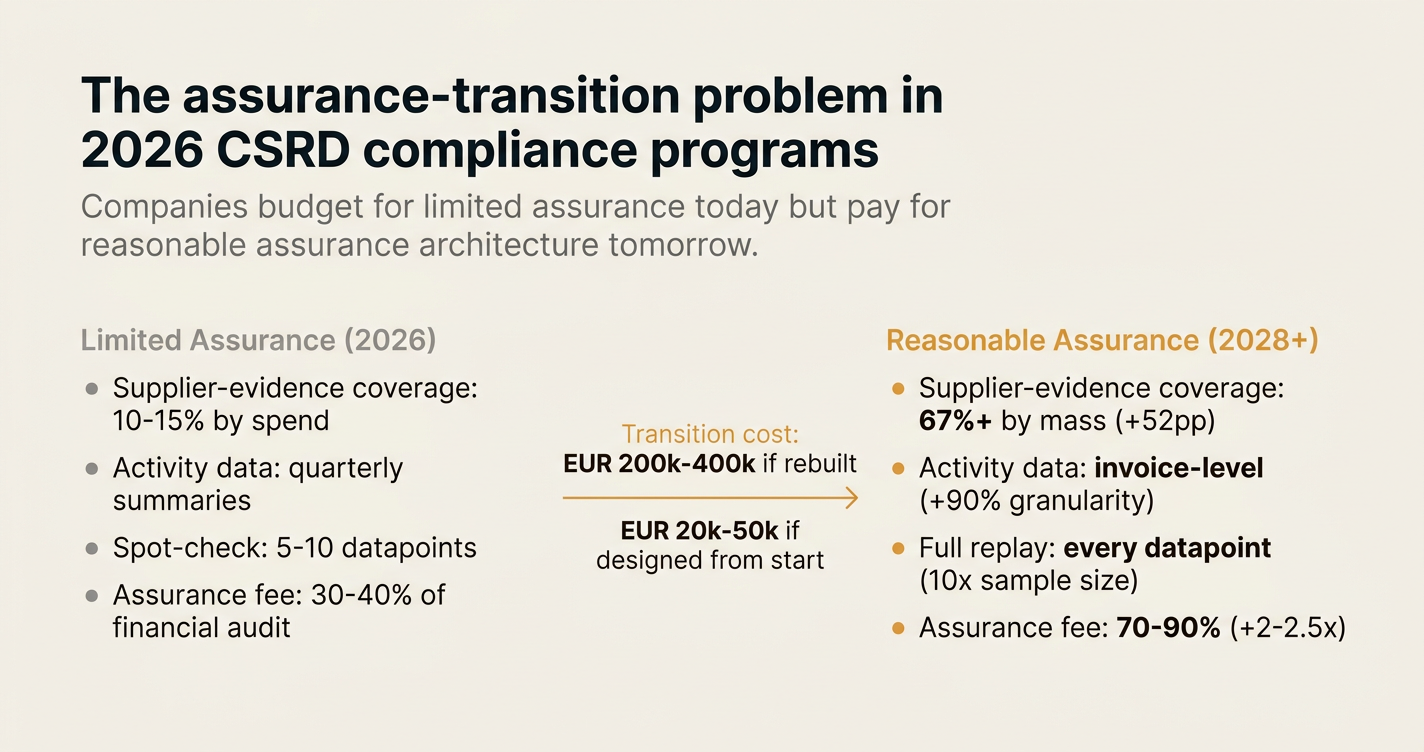

The assurance-transition problem in 2026 CSRD compliance programs

CSRD assurance consists of two things: limited assurance in 2026 and reasonable assurance from 2028. Companies budget for the first—but auditor fees are set by the second.

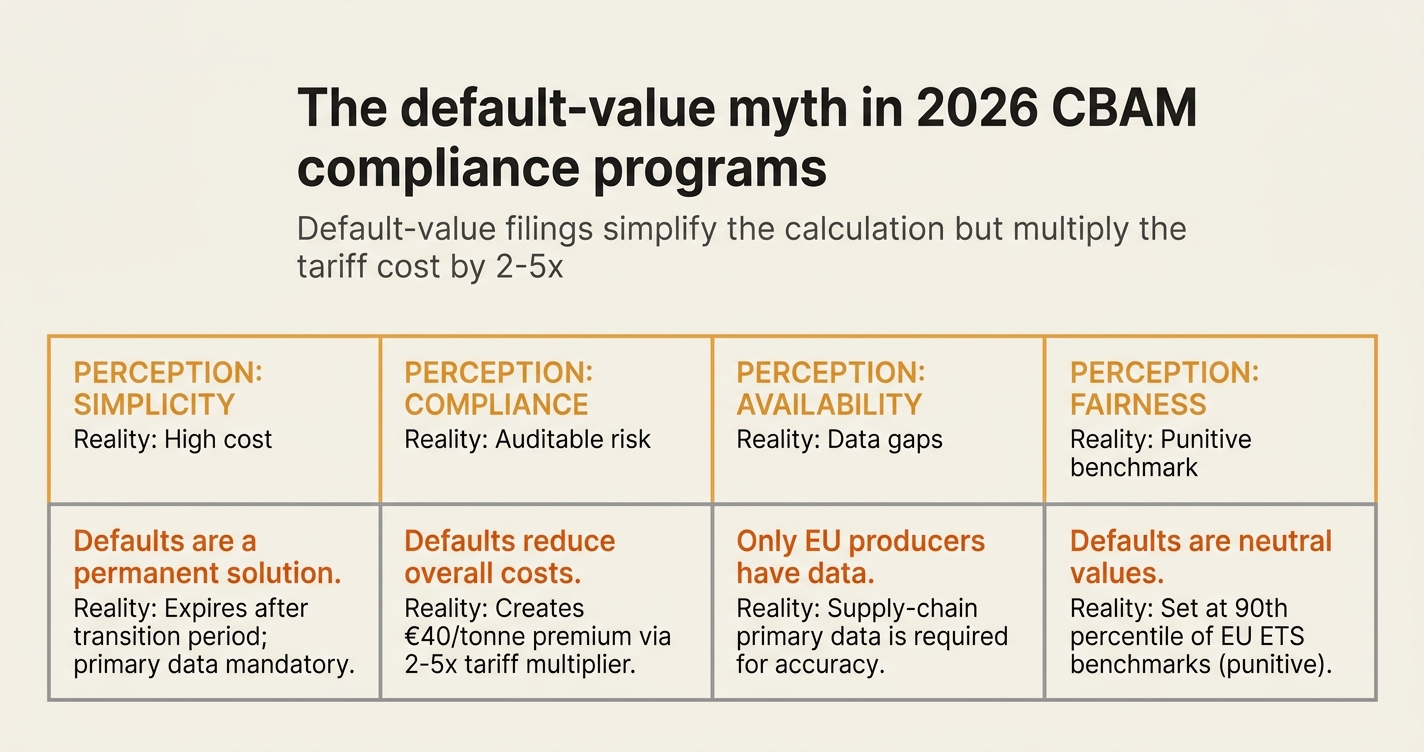

The default-value myth in 2026 CBAM compliance programs

CBAM filings consist of two things: embedded emissions totals and installation-level data. Importers can use defaults—but the certificate cost is 2-5x higher.

The assurance-fee escalation problem in 2026 SB 253 emissions reporting

SB 253 reporting consists of two things: emissions totals and evidence lineage. CFOs budget for the first—but assurance fees are set by the second.

The default-value penalty for non-EU steel exporters in CBAM filings

CBAM filings consist of two things: embedded emissions totals and installation-level data. Importers can declare with defaults—but the tariff cost is 2-5x higher.

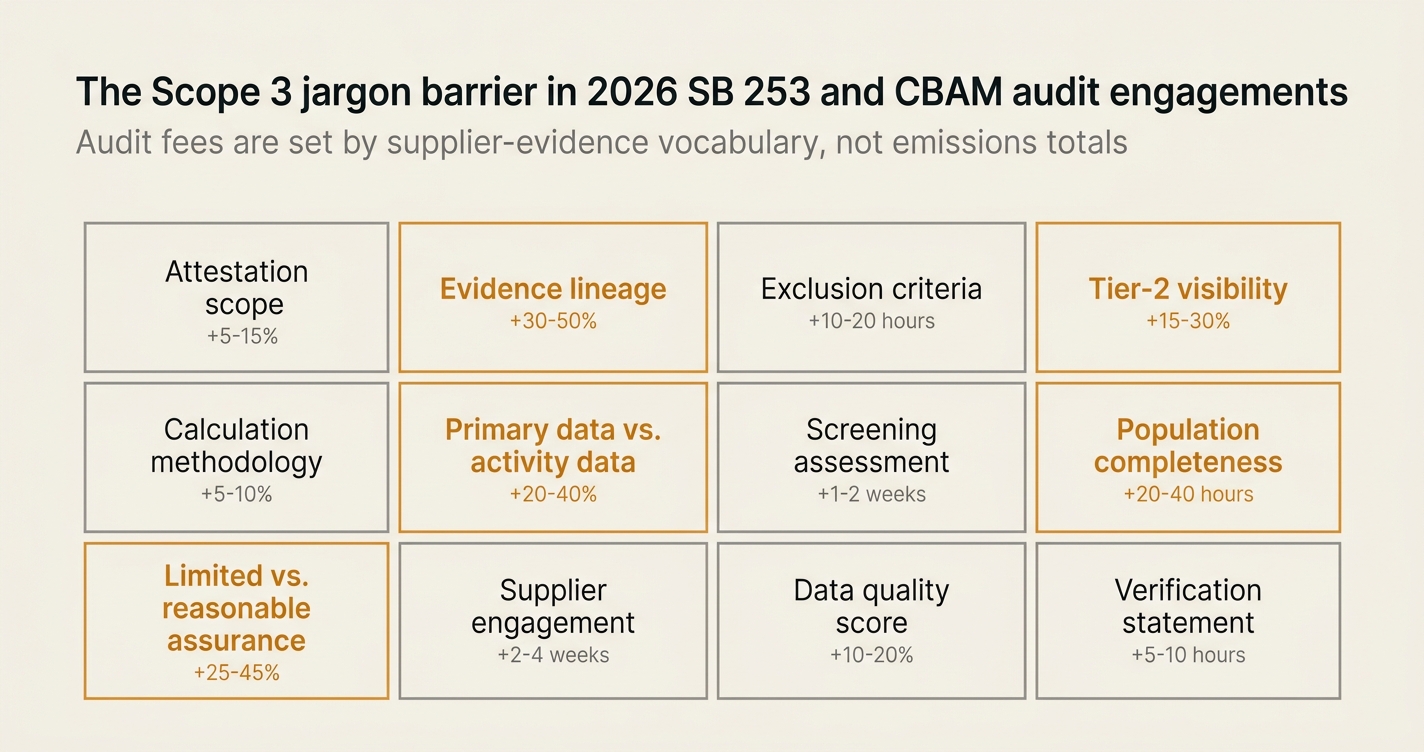

The Scope 3 jargon barrier in 2026 SB 253 and CBAM audit engagements

Scope 3 audits consist of two things: emissions totals and supplier-evidence vocabulary. CFOs negotiate the first—but audit fees are set by the second.

The supplier-data participation problem in Scope 3 Category 1 primary collection programs

Scope 3 primary collection consists of two things: supplier participation and data quality. Procurement teams optimize for the second—but 57% of programs stall on the first.

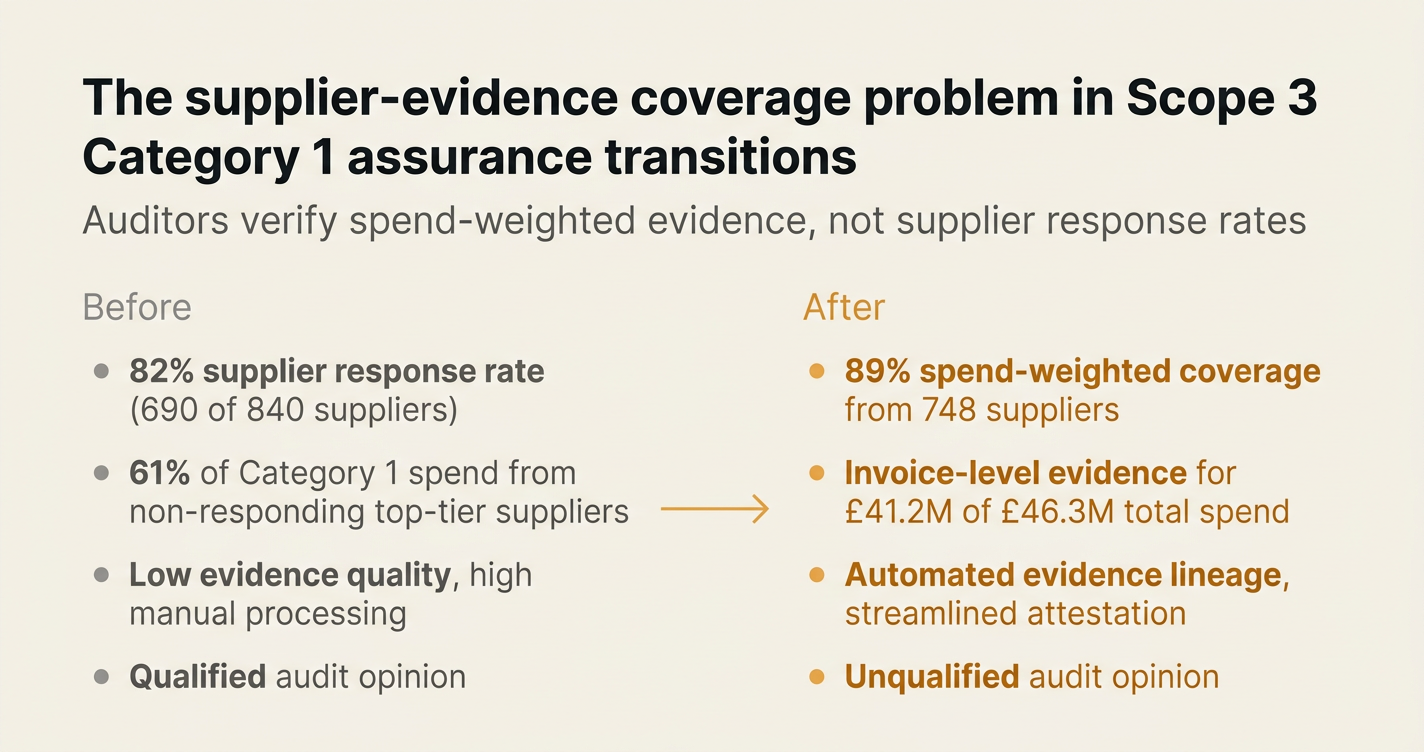

The supplier-evidence coverage problem in Scope 3 Category 1 assurance transitions

Scope 3 assurance consists of two things: emissions totals and supplier-evidence coverage. Auditors verify the second—and most transition plans lack it.

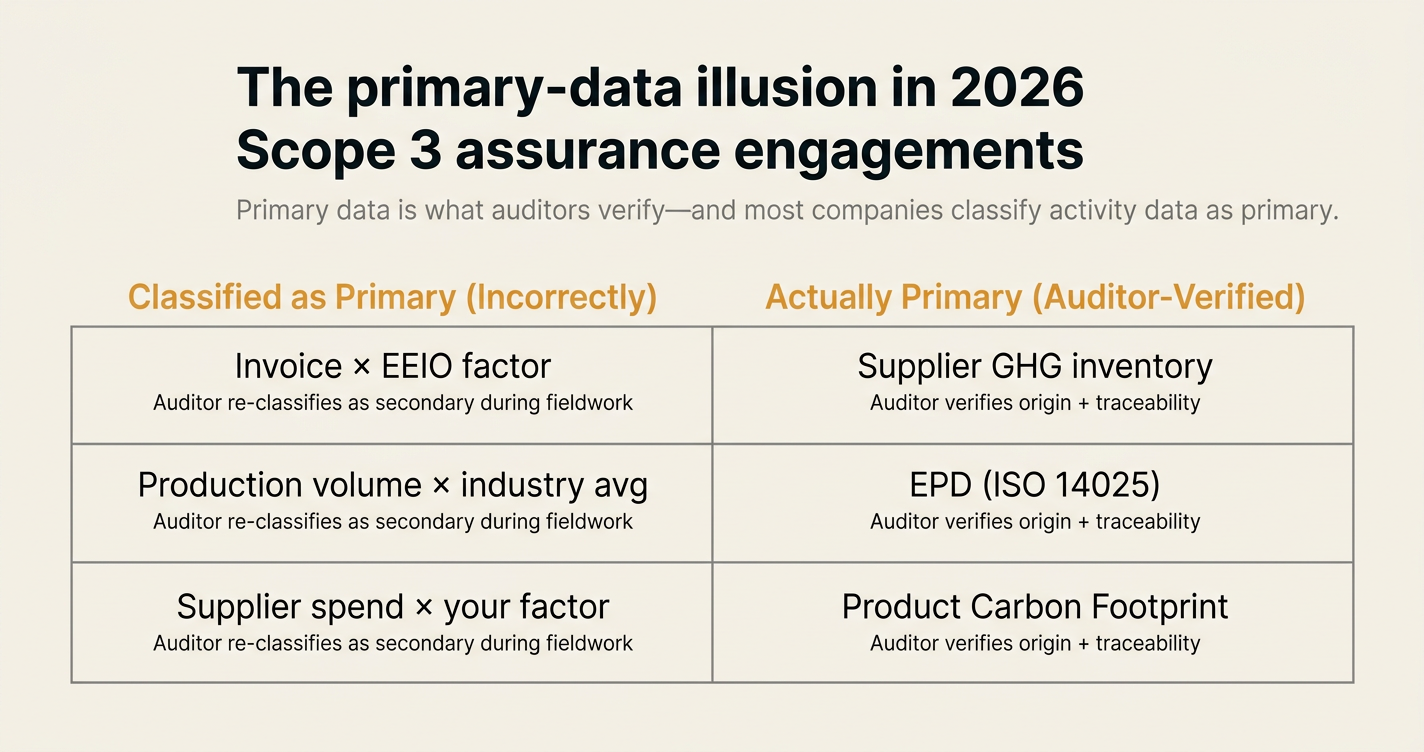

The primary-data illusion in 2026 Scope 3 assurance engagements

Scope 3 assurance consists of two things: primary data and activity data. Auditors verify the first—and most companies classify the second as primary.

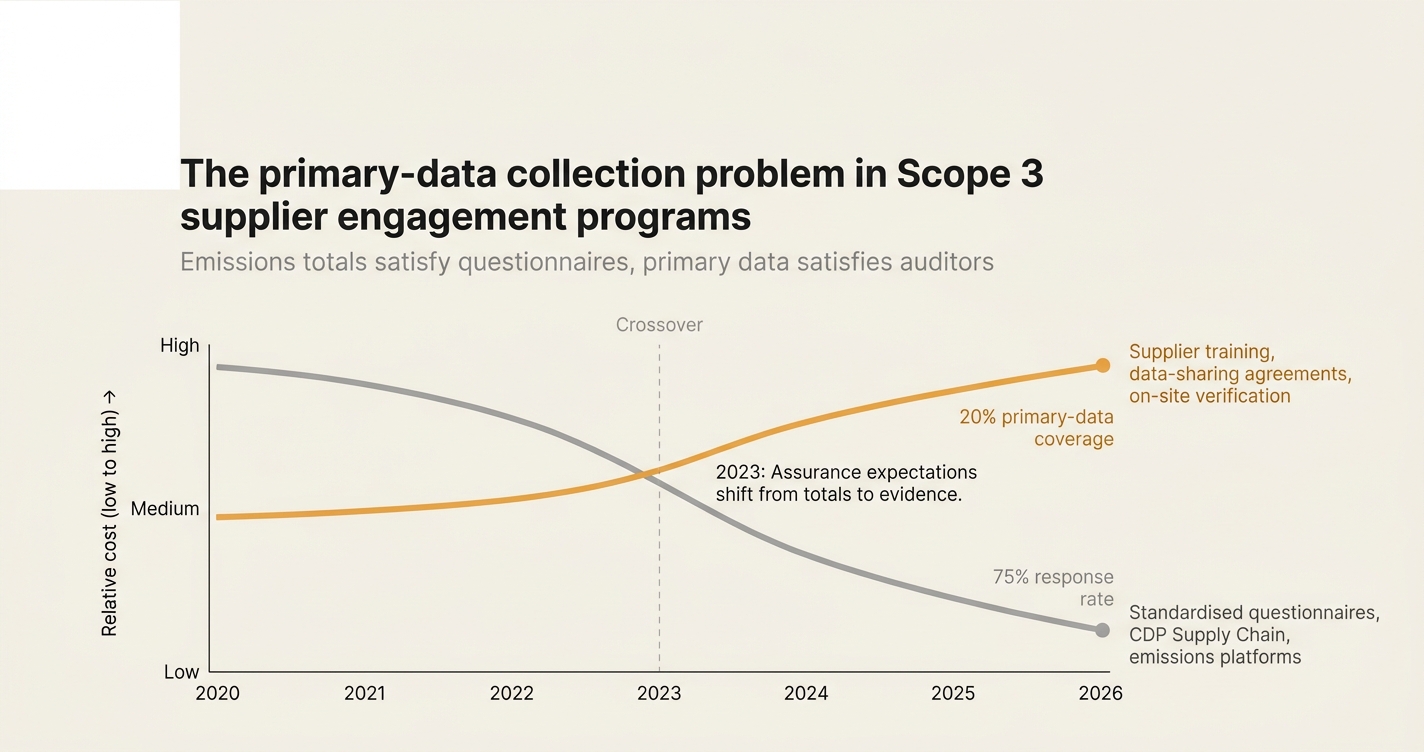

The primary-data collection problem in Scope 3 supplier engagement programs

Supplier engagement consists of two things: emissions totals and primary data. Auditors verify the second—and most procurement systems lack it.

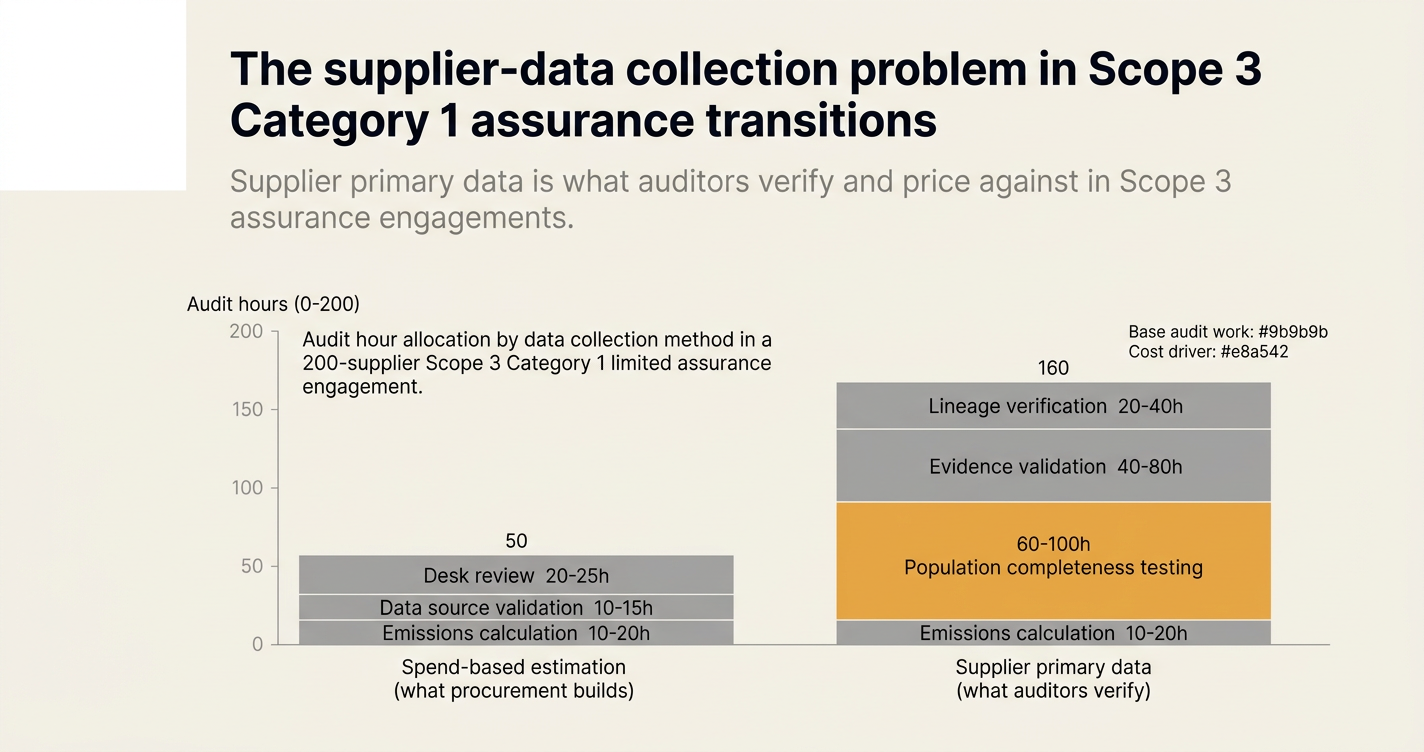

The supplier-data collection problem in Scope 3 Category 1 assurance transitions

Scope 3 assurance consists of two things: emissions totals and supplier primary data. Auditors verify the second—and most procurement systems lack it.

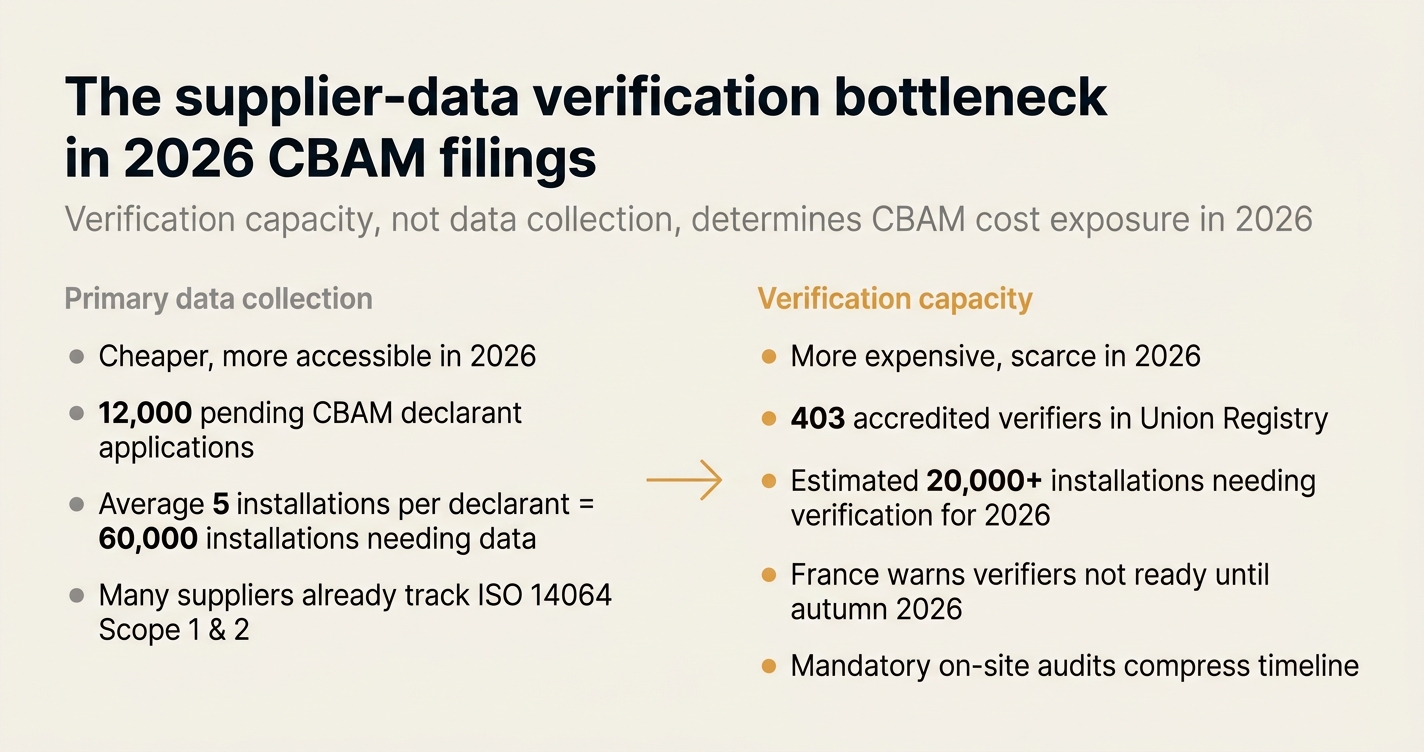

The supplier-data verification bottleneck in 2026 CBAM filings

CBAM filings consist of two things: embedded emissions totals and verified supplier data. Importers can declare in Q1 2027—but verifiers may not be available.

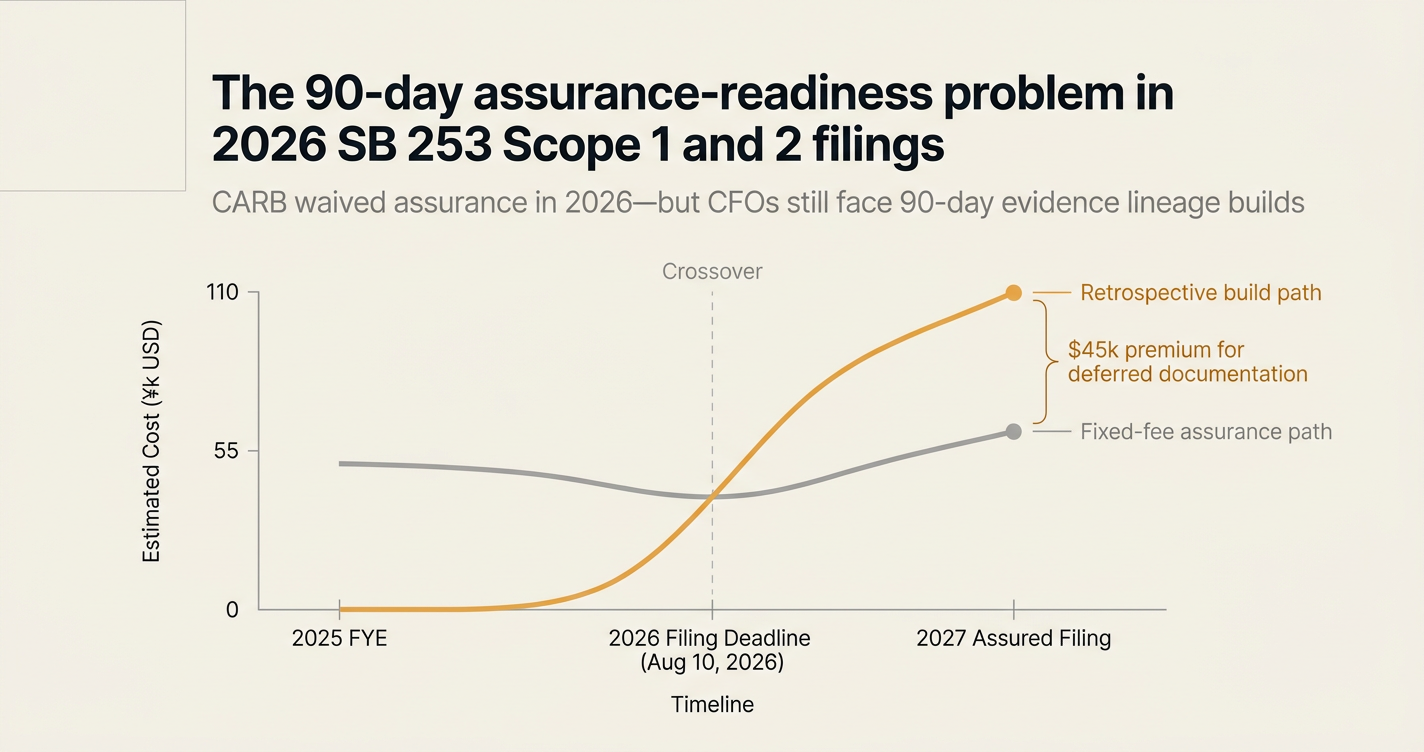

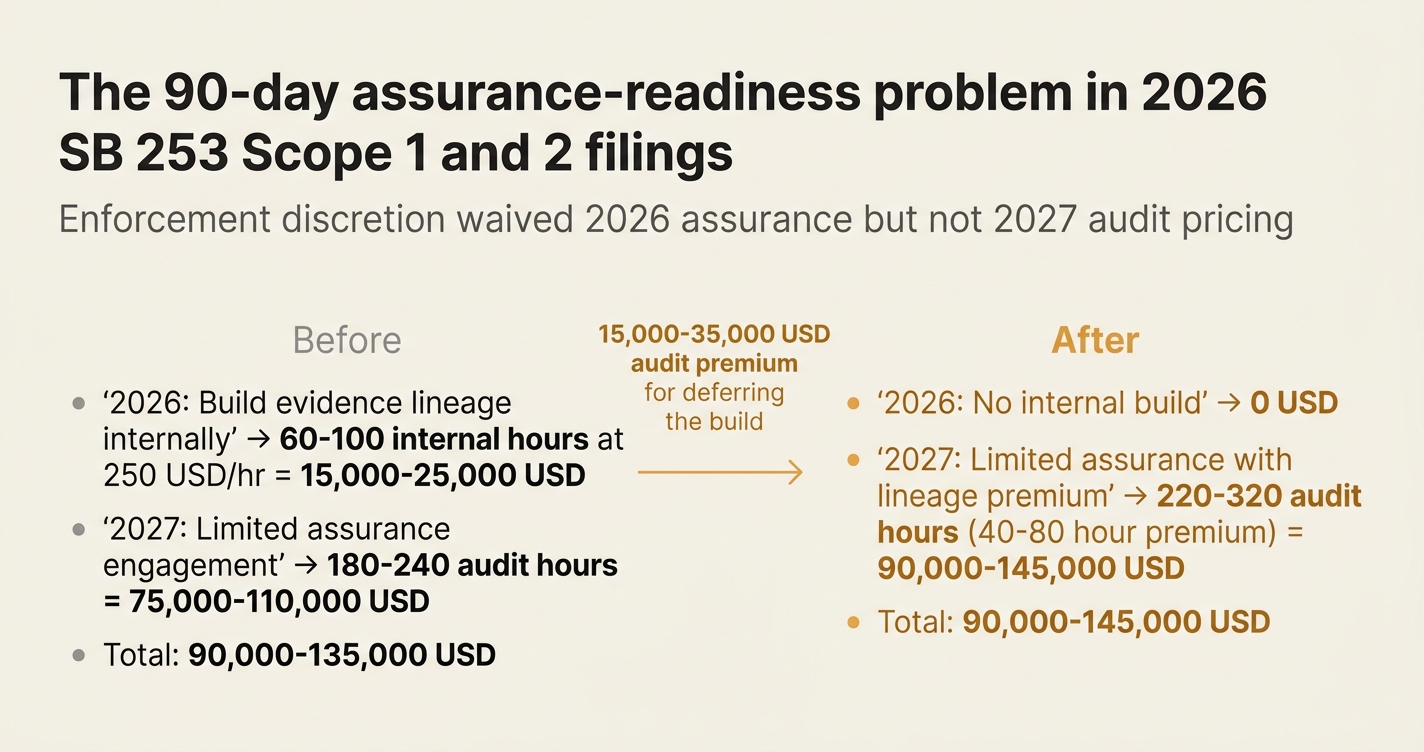

The 90-day assurance-readiness problem in 2026 SB 253 Scope 1 and 2 filings

SB 253 filings consist of two things: emissions totals and audit-ready documentation. CARB waived assurance in 2026—but CFOs still face 90-day evidence lineage builds.

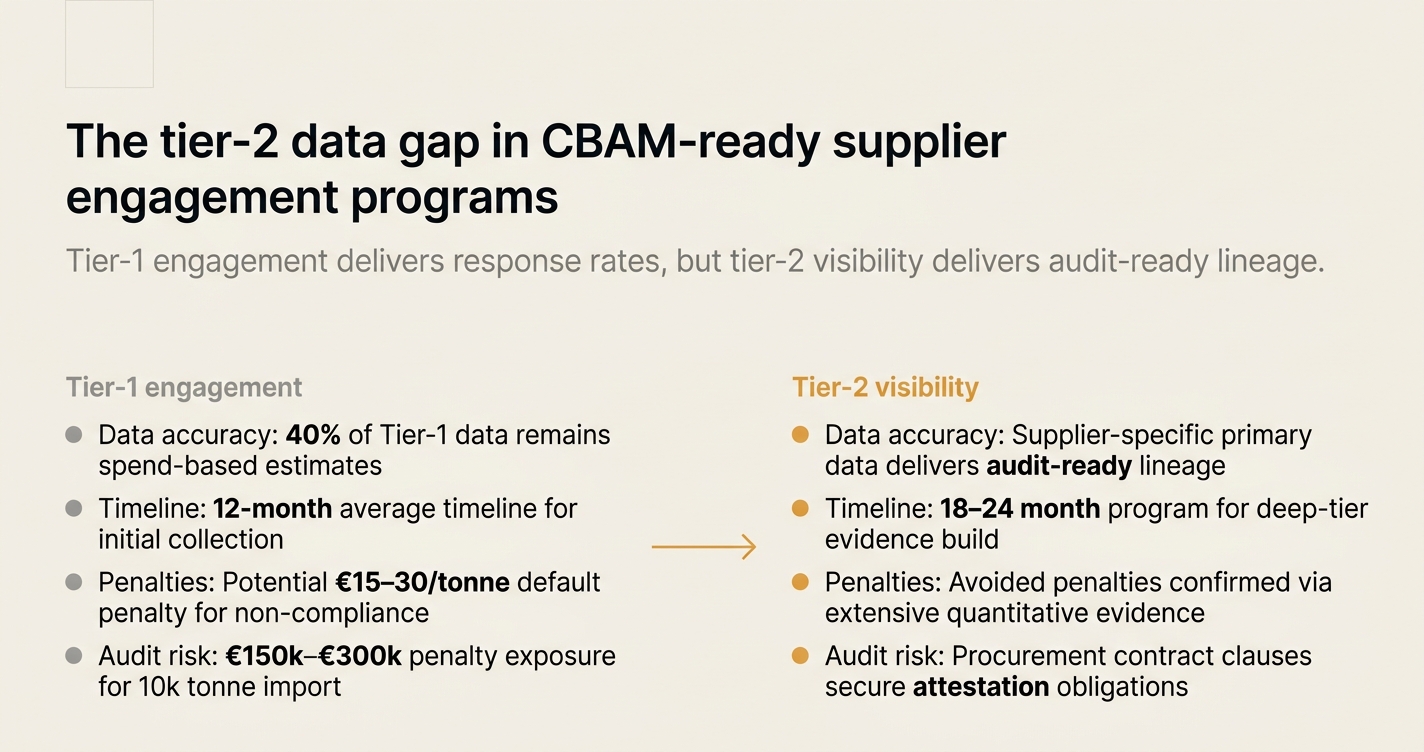

The tier-2 data gap in CBAM-ready supplier engagement programs

Supplier engagement consists of two things: tier-1 data collection and tier-2 visibility. Procurement teams optimize for the first—but 40% of embedded emissions hide in the second.

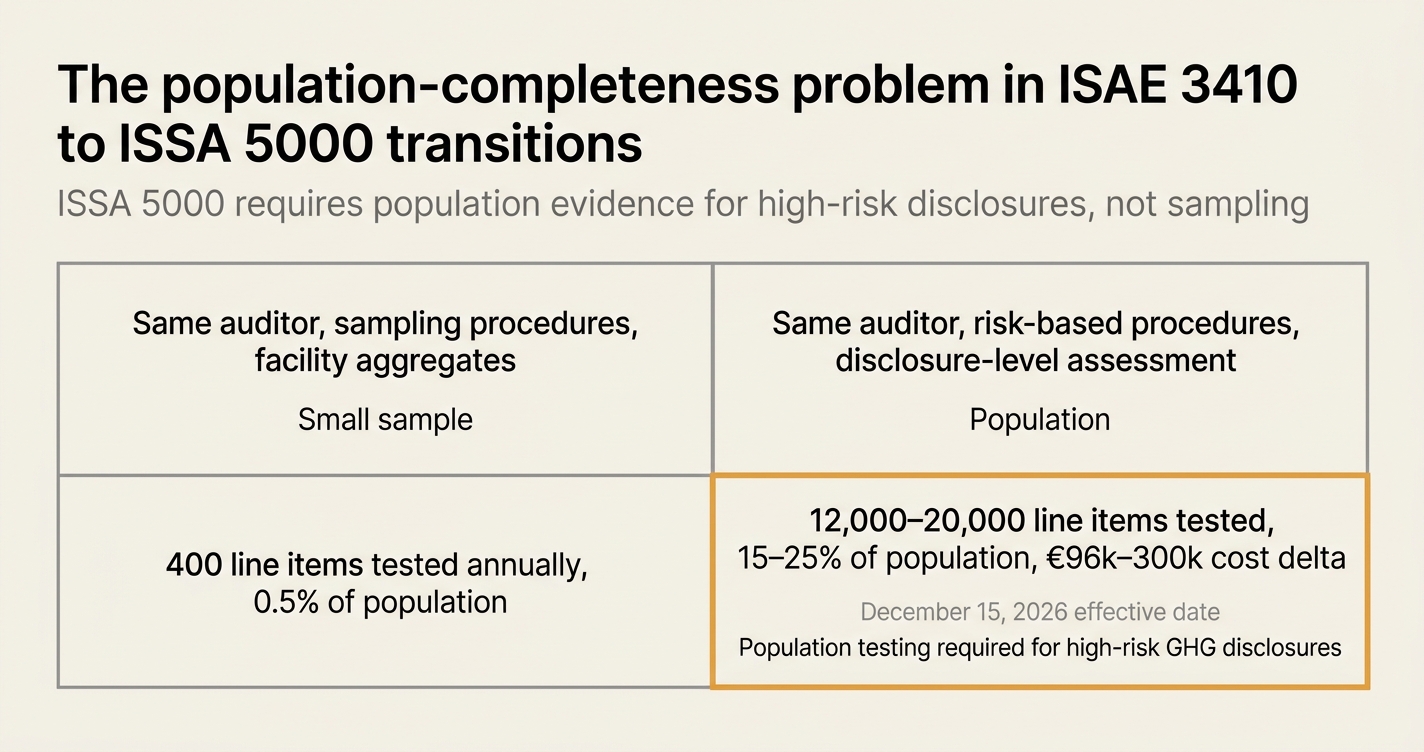

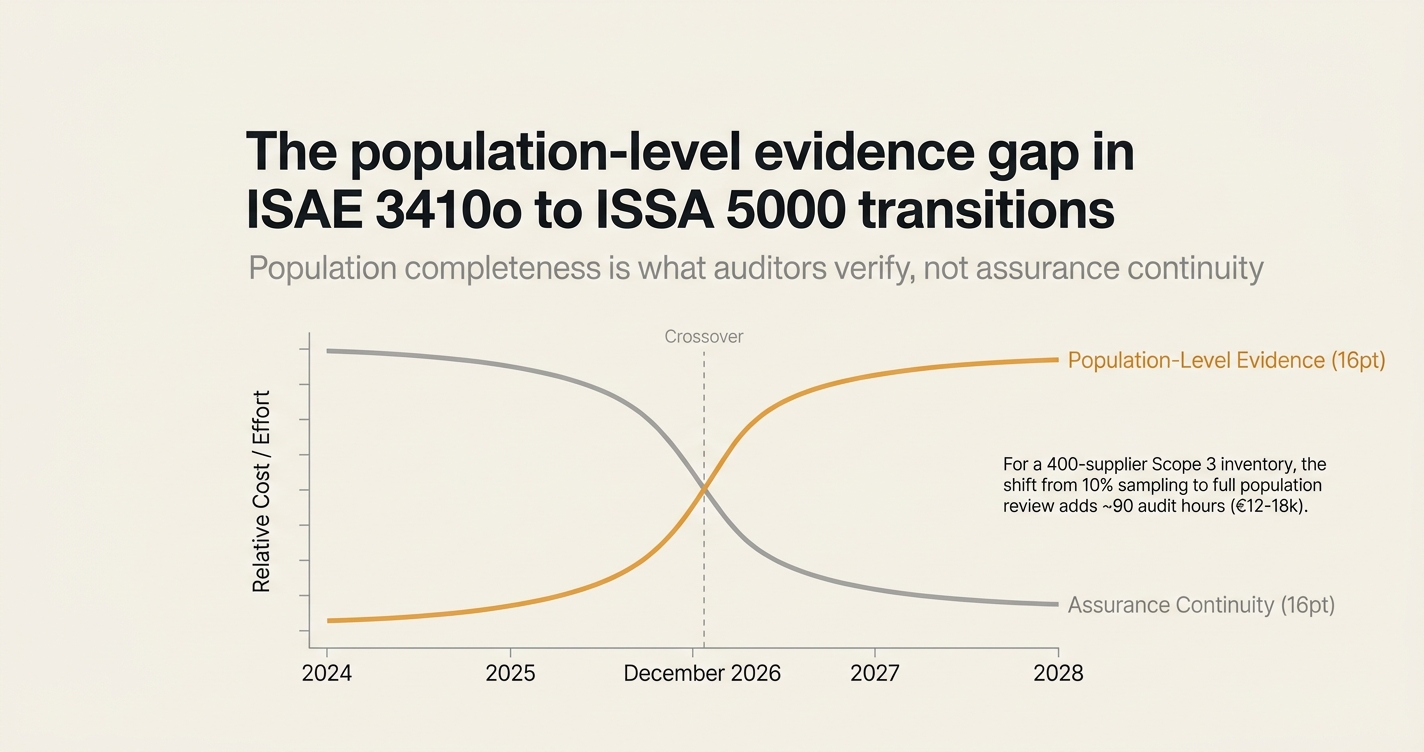

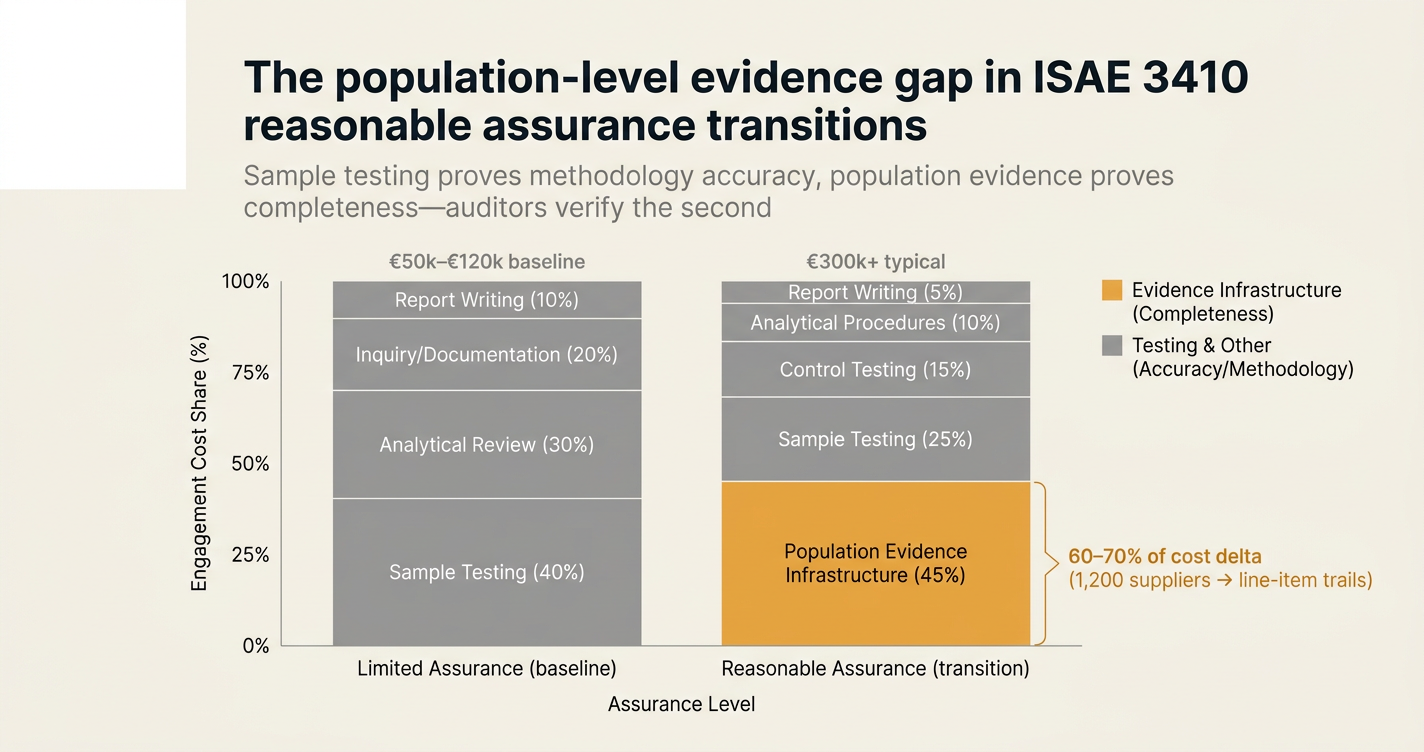

The population-completeness problem in ISAE 3410 to ISSA 5000 transitions

ISAE 3410 transitions consist of two things: assurance continuity and population-completeness evidence. Auditors verify the second—and most transition plans lack it.

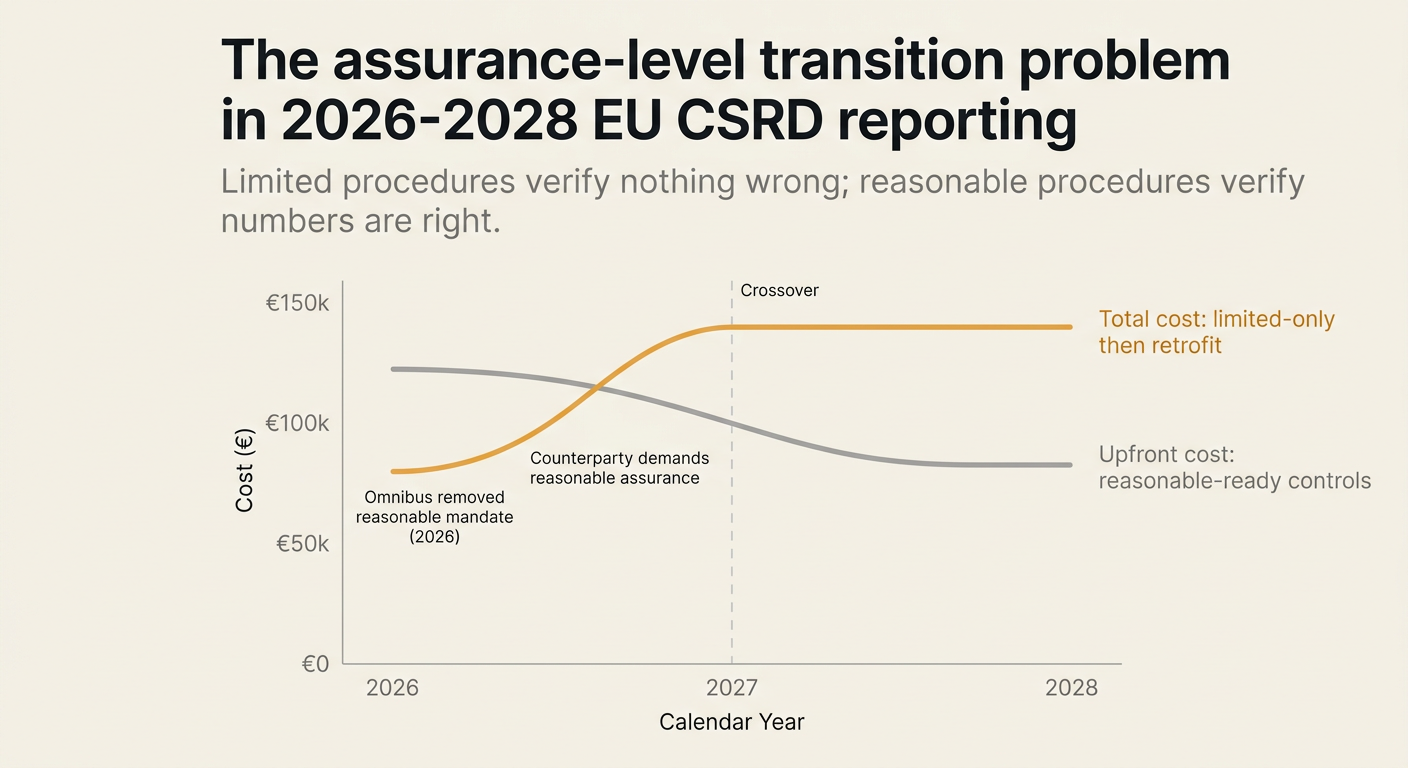

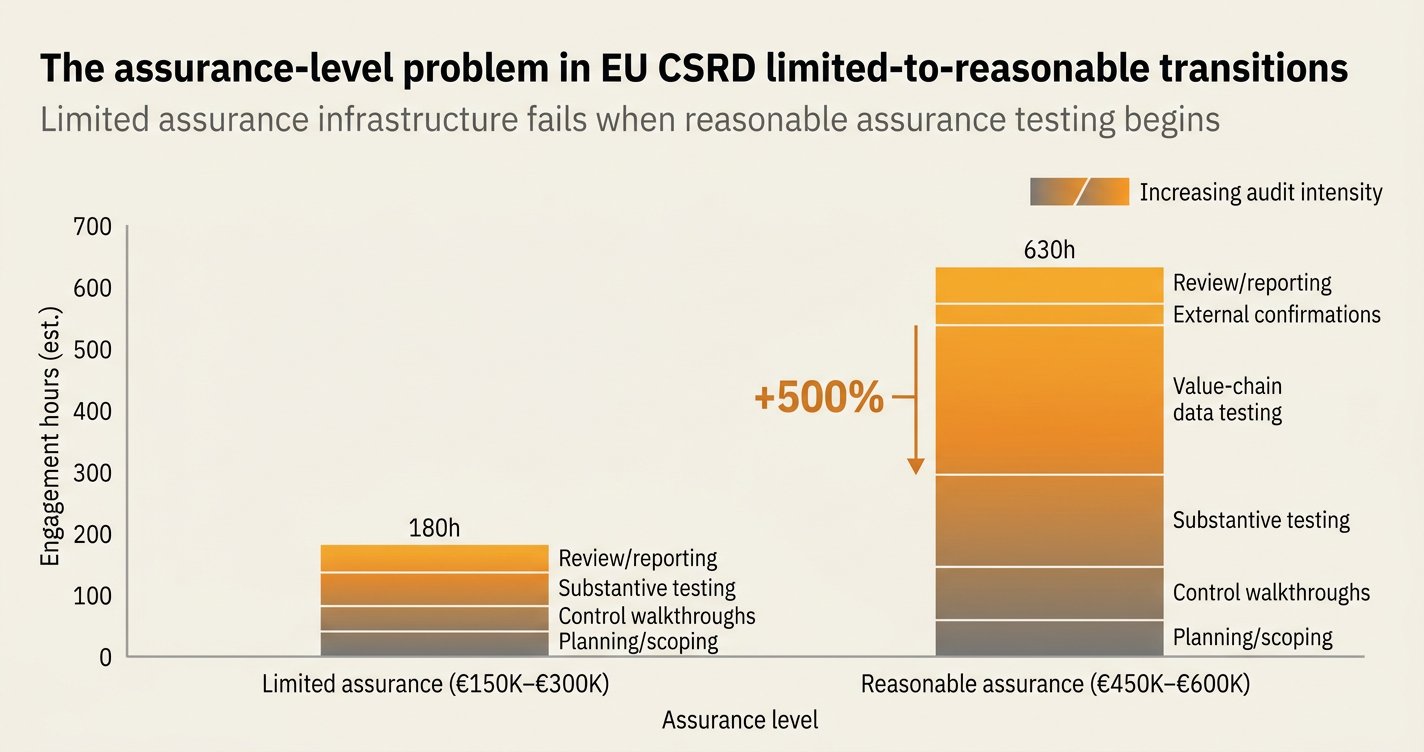

The assurance-level transition problem in 2026-2028 EU CSRD reporting

CSRD assurance consists of two things: limited procedures and reasonable procedures. The Omnibus removed the reasonable transition—but auditors still price for it.

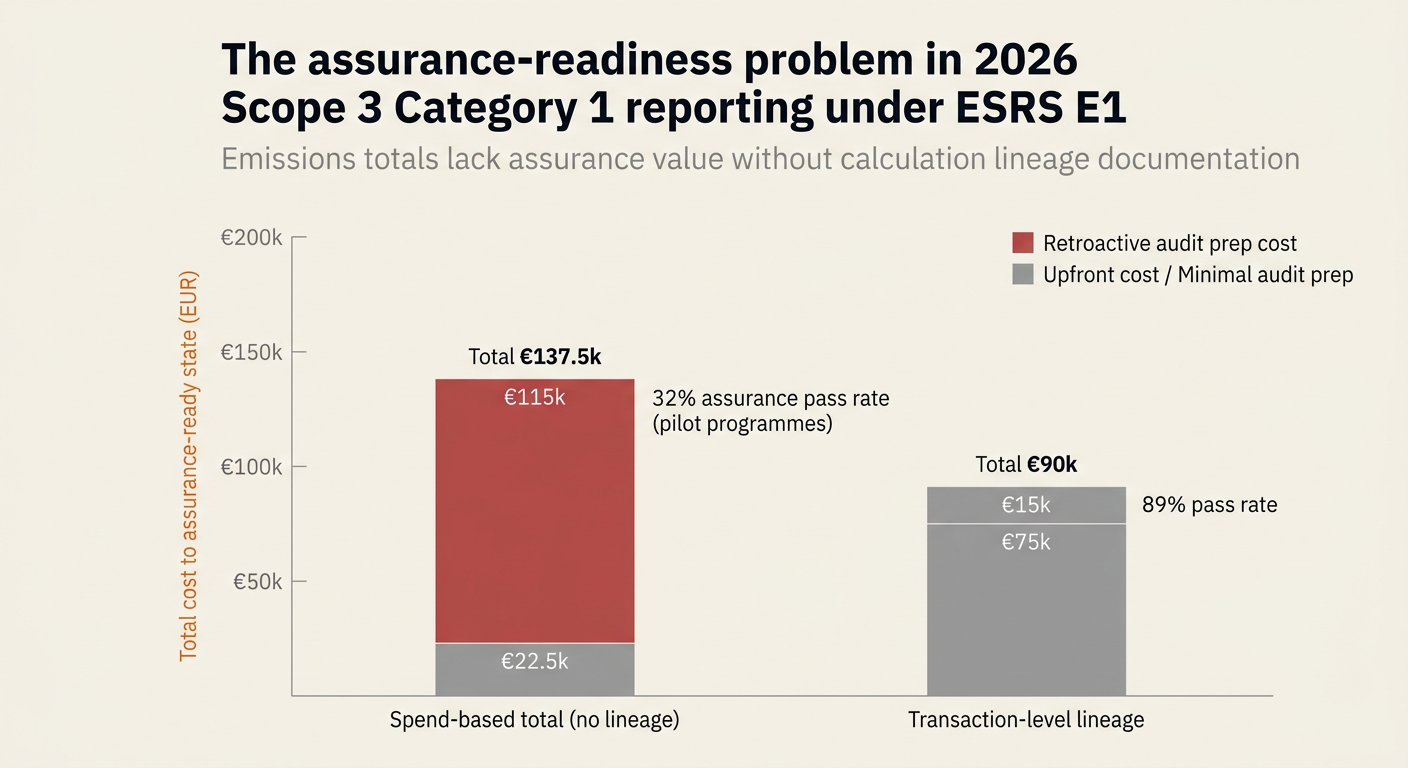

The assurance-readiness problem in 2026 Scope 3 Category 1 reporting under ESRS E1

Scope 3 Category 1 reporting consists of two things: emissions totals and calculation lineage. Auditors verify the second—and most procurement teams lack it.

The 90-day assurance-readiness problem in 2026 SB 253 Scope 1 and 2 filings

SB 253 filings consist of two things: emissions totals and audit-ready documentation. CARB waived assurance in 2026—but CFOs still face 90-day evidence lineage builds.

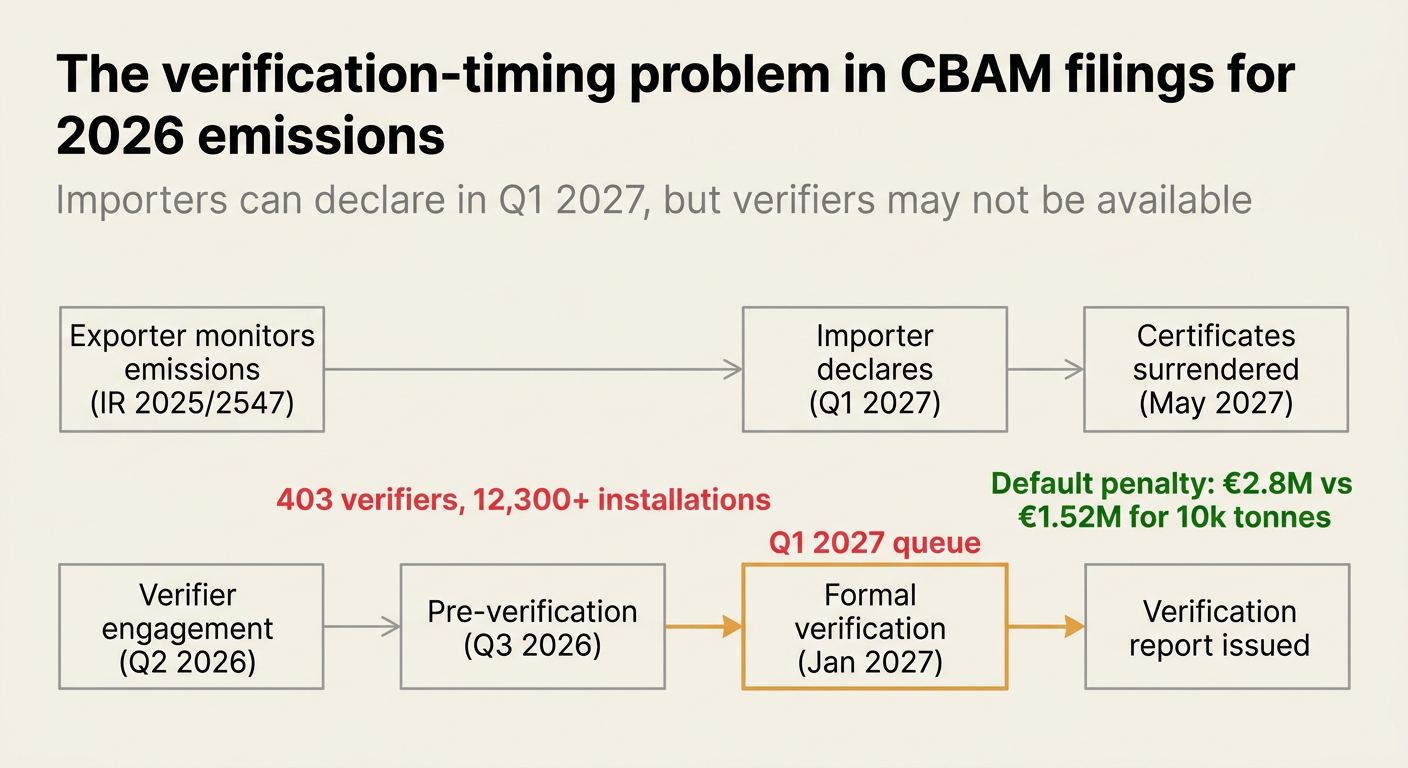

The verification-timing problem in CBAM filings for 2026 emissions

CBAM filings consist of two things: embedded emissions totals and third-party verification. Importers can declare in Q1 2027—but verifiers may not be available.

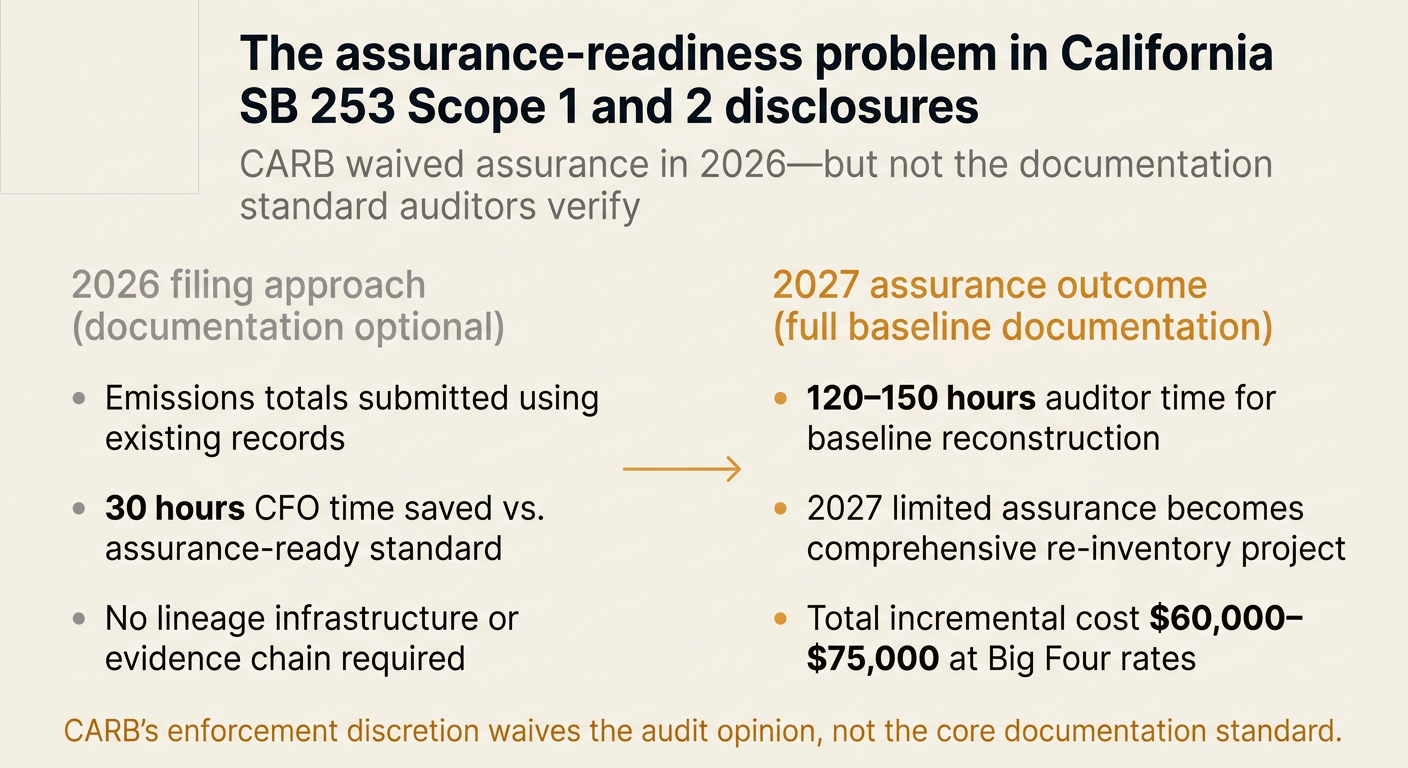

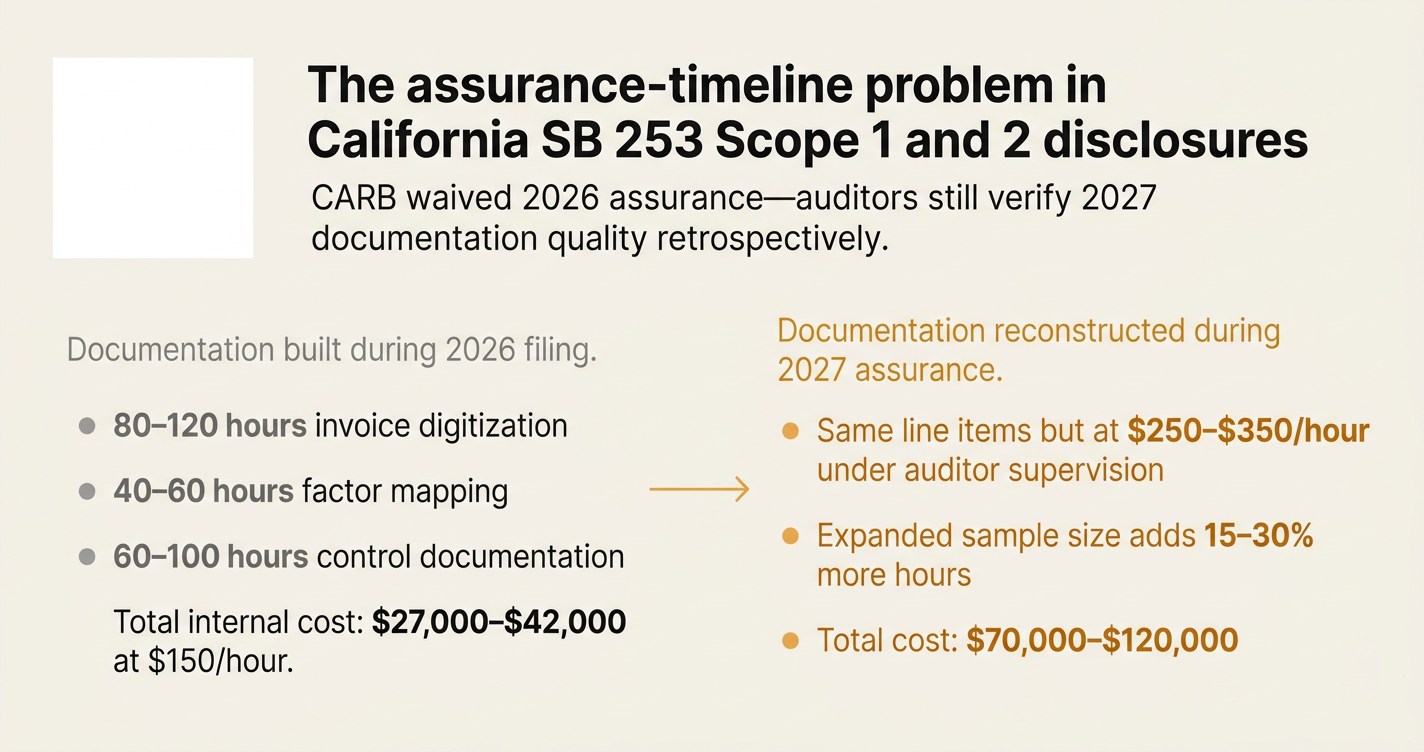

The assurance-readiness problem in California SB 253 Scope 1 and 2 disclosures

SB 253 disclosure consists of two things: emissions totals and assurance-ready documentation. CARB waived limited assurance in 2026—but auditors still verify documentation quality.

The tier-2 visibility problem in Scope 3 Category 1 supplier engagement

Scope 3 supplier engagement consists of two things: tier-1 data and tier-2 visibility. Procurement teams optimize for the first—but 40% of embedded emissions hide in the second.

The population-level evidence gap in ISAE 3410 to ISSA 5000 transitions

ISAE 3410 transitions consist of two things: assurance continuity and population completeness evidence. Auditors verify the second—and most transition plans lack it.

The assurance-level problem in EU CSRD limited-to-reasonable transitions

CSRD assurance consists of two things: limited procedures and reasonable procedures. Auditors charge for the second—and most first-wave reporters lack the controls.

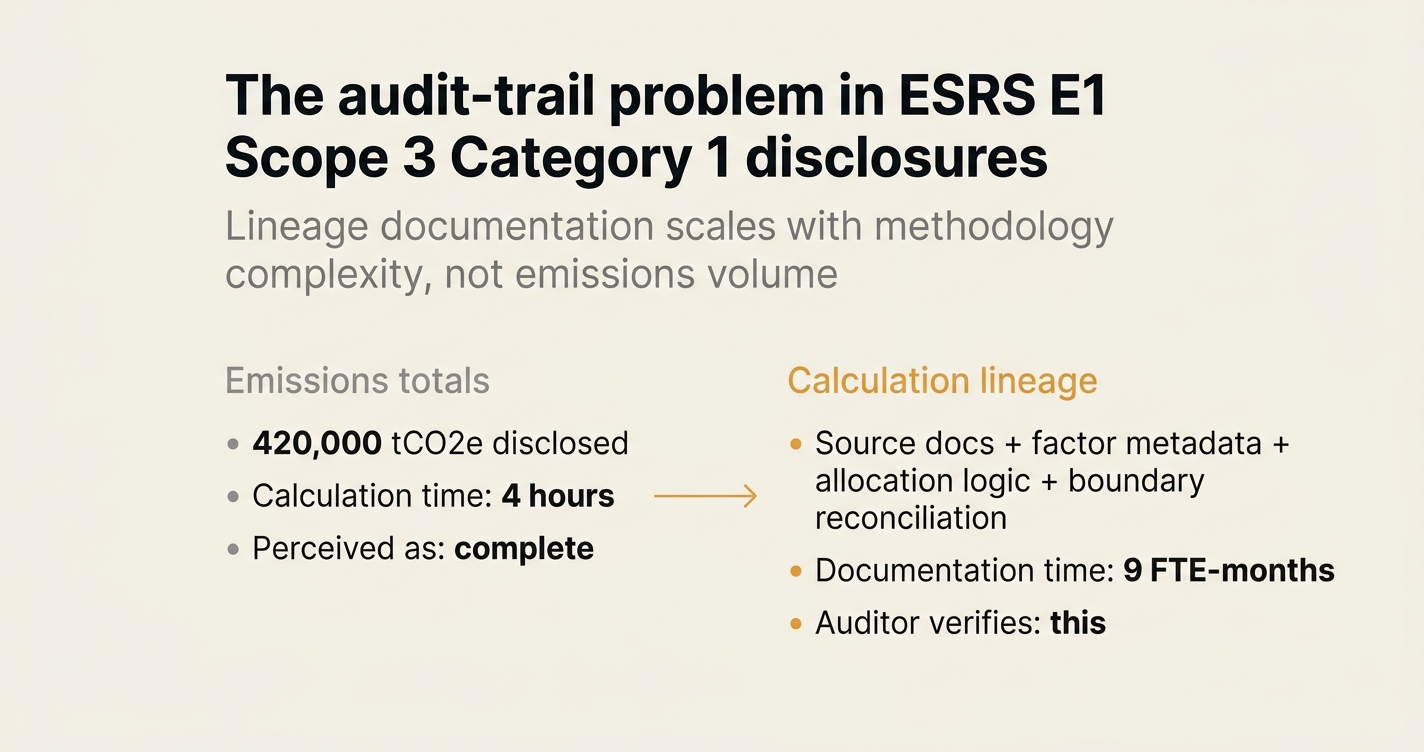

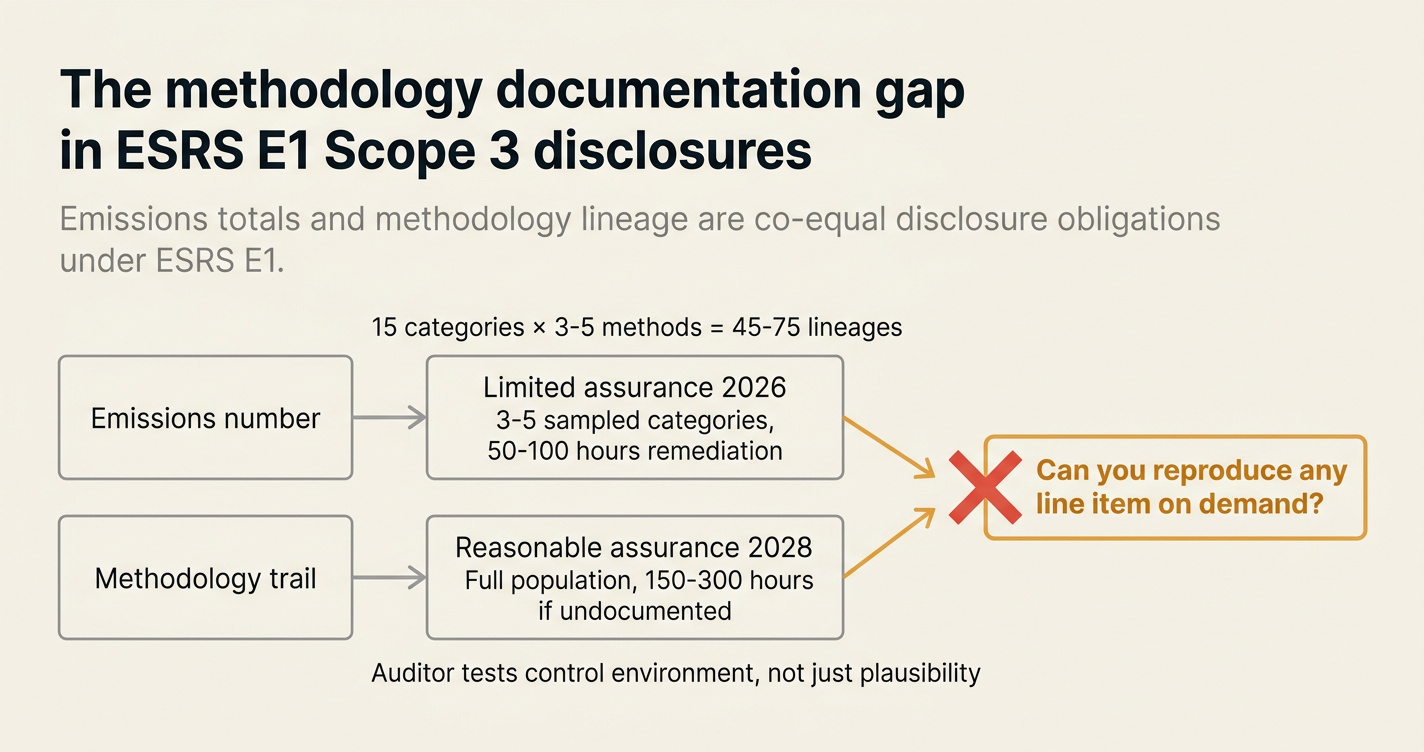

The audit-trail problem in ESRS E1 Scope 3 Category 1 disclosures

Scope 3 Category 1 disclosure consists of two things: emissions totals and calculation lineage. Auditors verify the second—and most procurement teams lack it.

The assurance-timeline problem in California SB 253 Scope 1 and 2 disclosures

SB 253 disclosure consists of two things: emissions totals and audit-ready documentation. CARB waived assurance in 2026—but auditors still verify documentation quality.

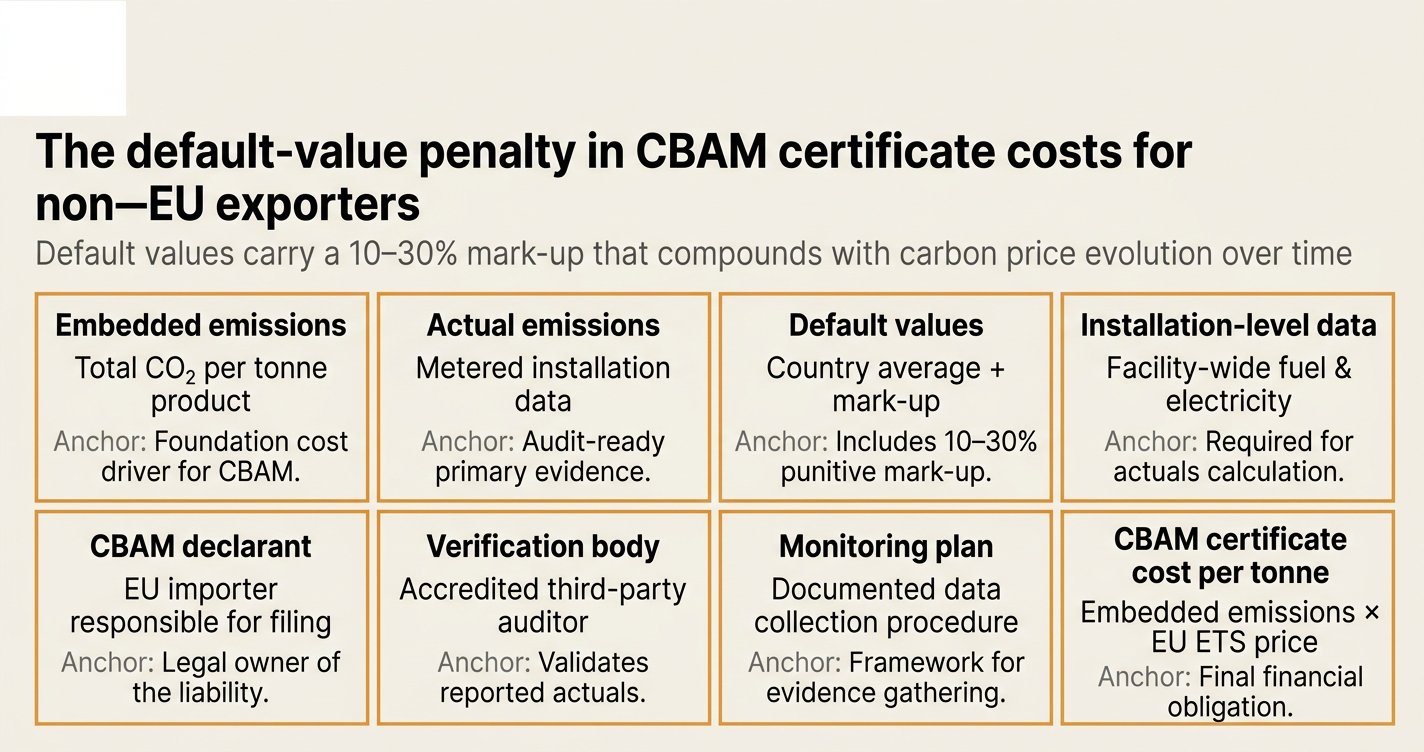

The default-value penalty in CBAM certificate costs for non-EU exporters

CBAM filings consist of two things: embedded emissions and actual installation data. Importers pay for the first—but the regulator charges a 10–30% penalty on the second.

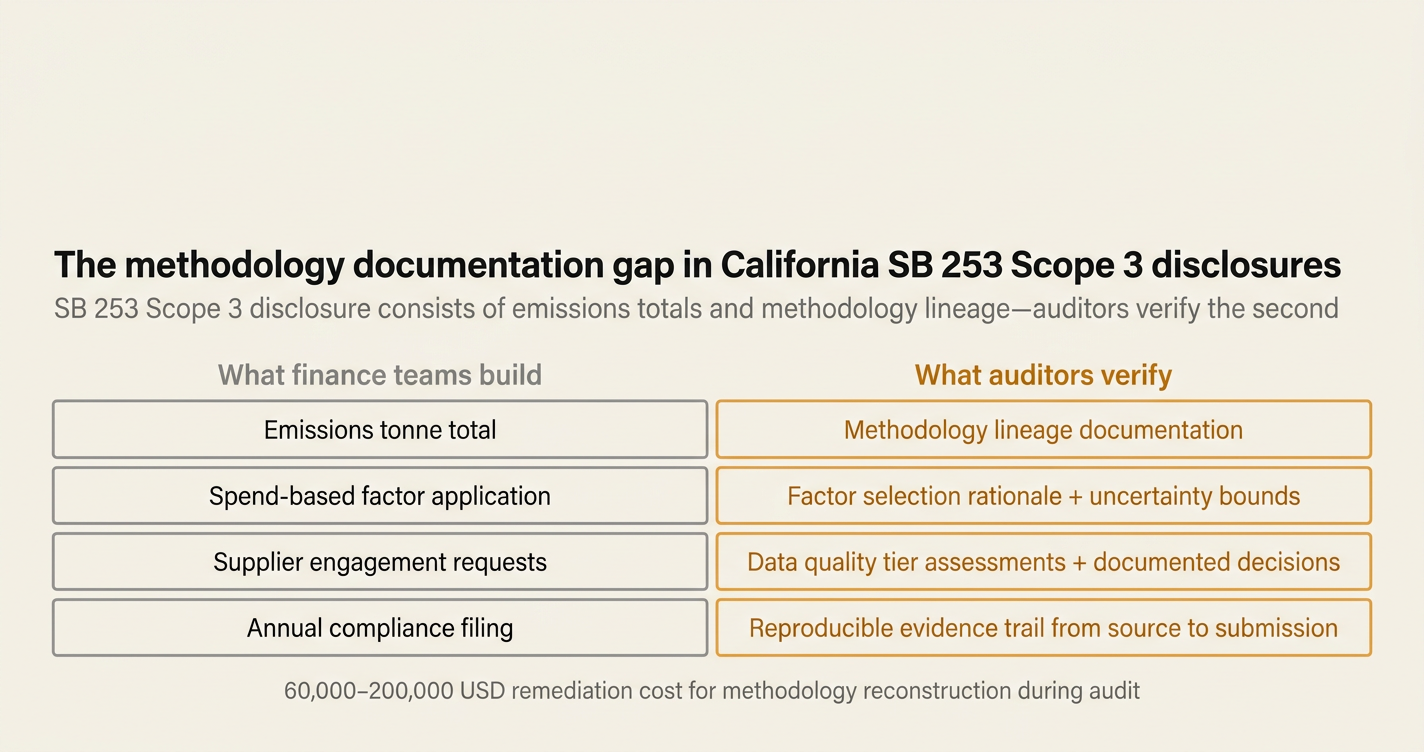

The methodology documentation gap in California SB 253 Scope 3 disclosures

SB 253 Scope 3 disclosure consists of two things: emissions totals and methodology lineage. Auditors verify the second—and most CFOs lack it.

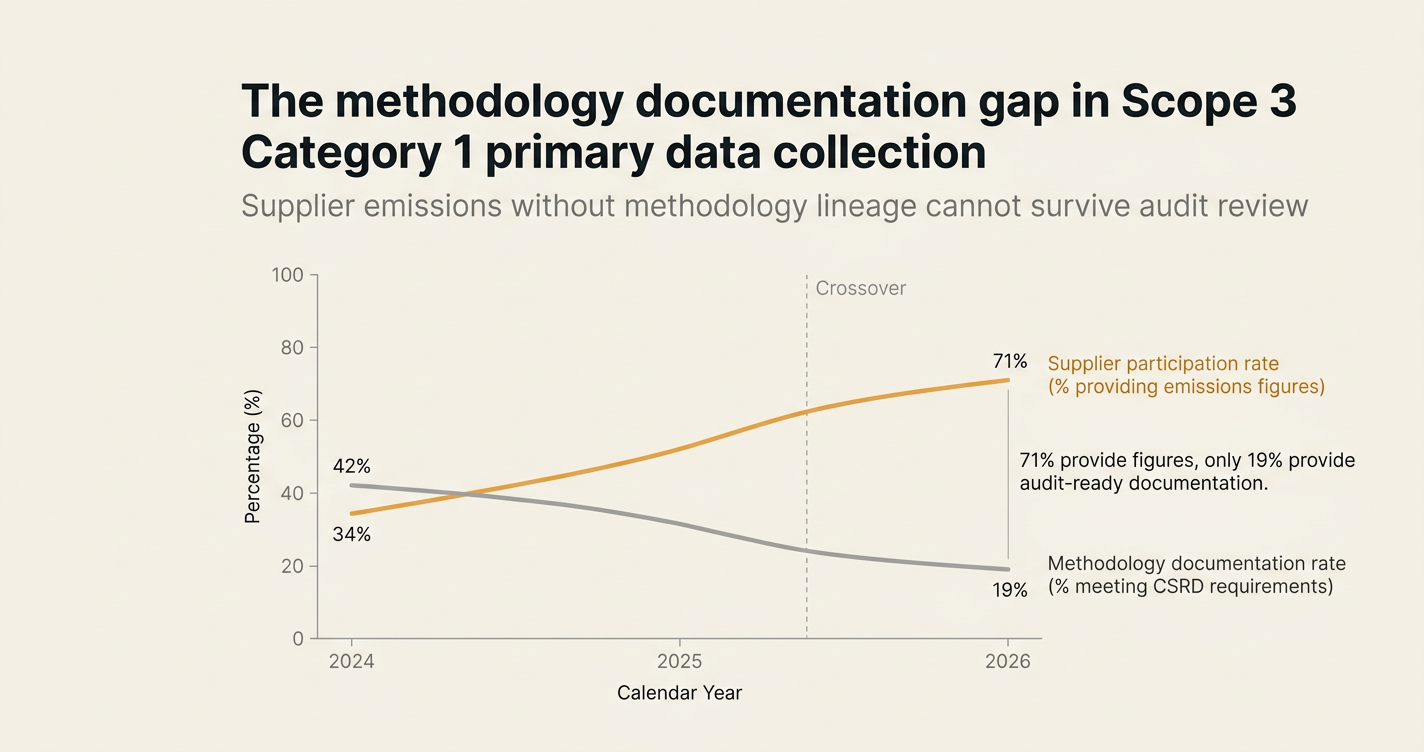

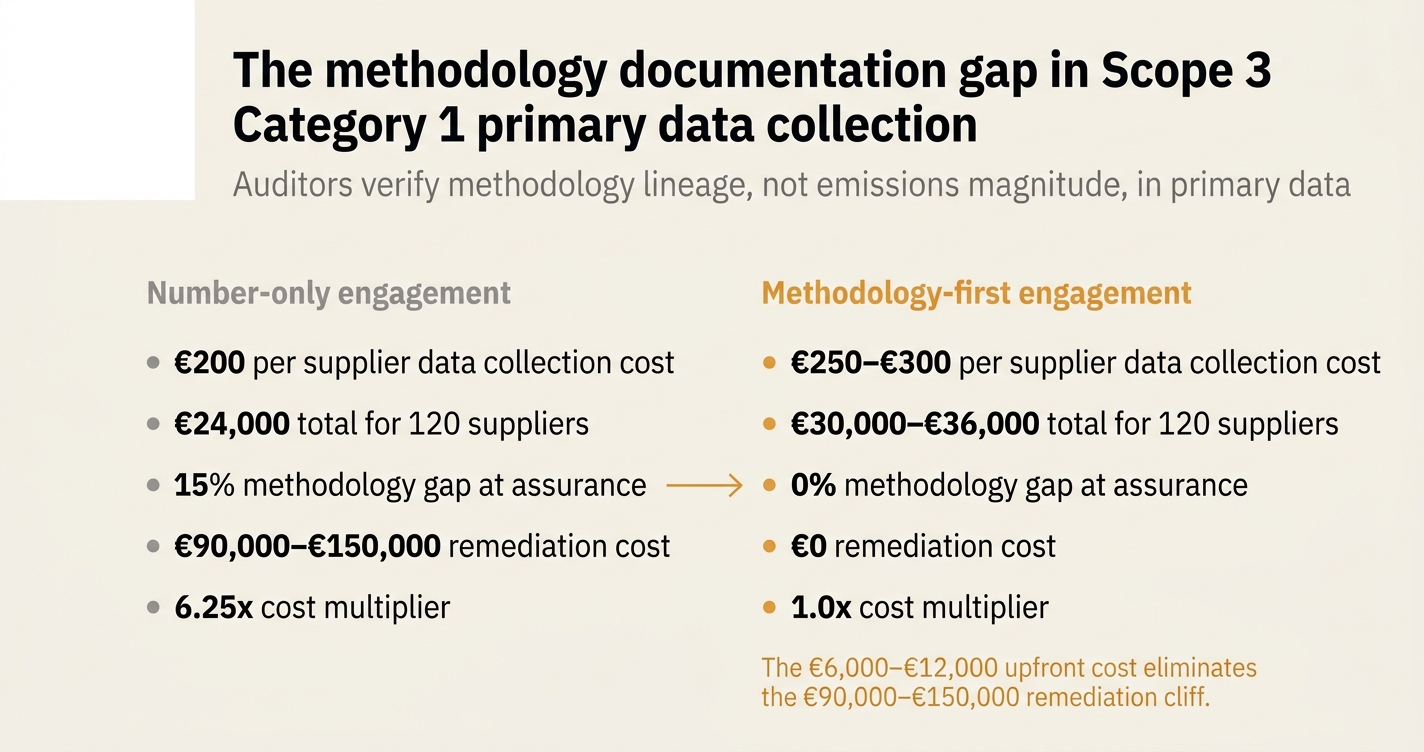

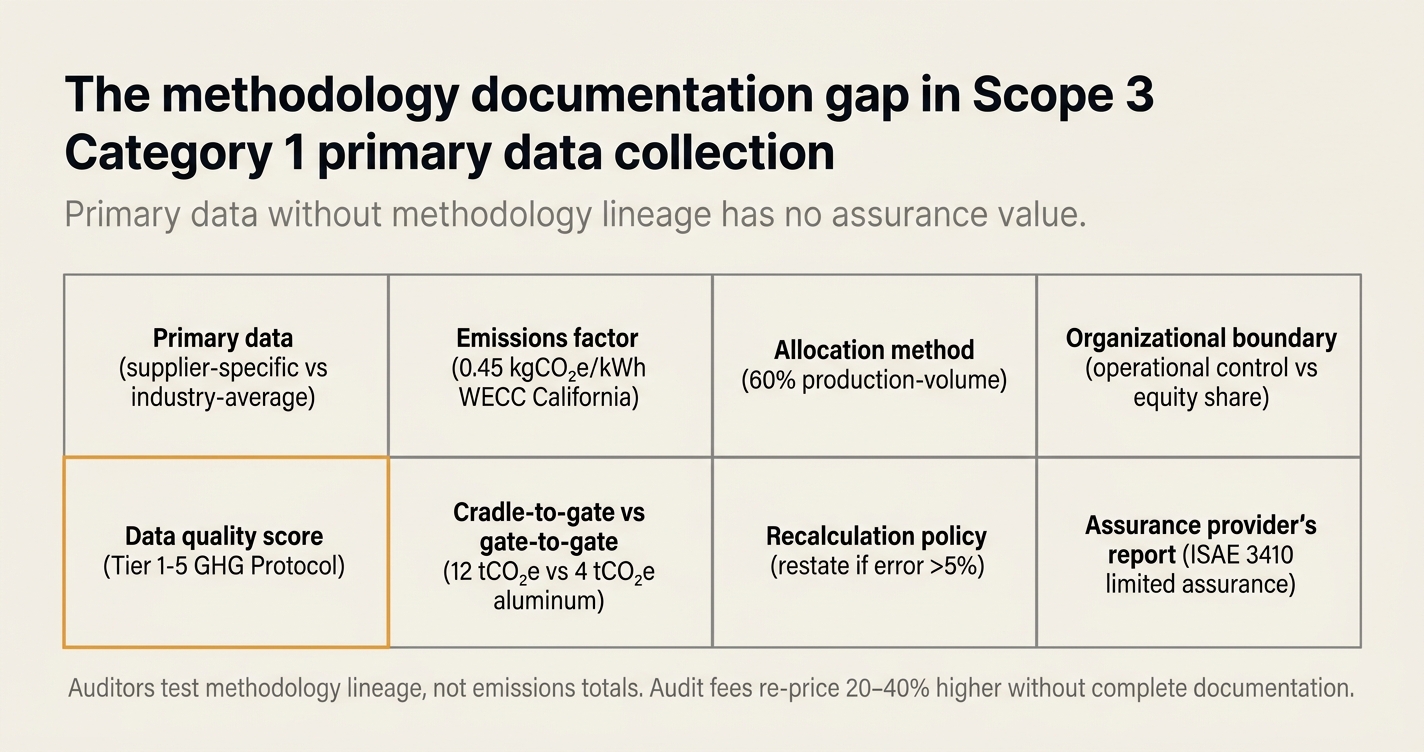

The methodology documentation gap in Scope 3 Category 1 primary data collection

Primary data collection consists of two things: supplier emissions and methodology lineage. Auditors verify the second—and most procurement teams lack it.

The population-level evidence gap in ISAE 3410 reasonable assurance transitions

ISAE 3410 reasonable assurance consists of two things: sample testing and population completeness. Auditors verify the second—and most Scope 3 inventories cannot prove it.

The methodology documentation gap in Scope 3 Category 1 primary data collection

Primary data collection consists of two things: supplier emissions and methodology lineage. Auditors verify the second—and most procurement teams lack it.

The methodology documentation gap in ESRS E1 Scope 3 disclosures

ESRS E1 disclosure consists of two things: emissions totals and methodology lineage. Auditors verify the second—and most sustainability teams lack it.

The methodology documentation gap in Scope 3 Category 1 primary data collection

Primary data collection consists of two things: supplier emissions and methodology lineage. Auditors verify the second—and most procurement teams lack it.

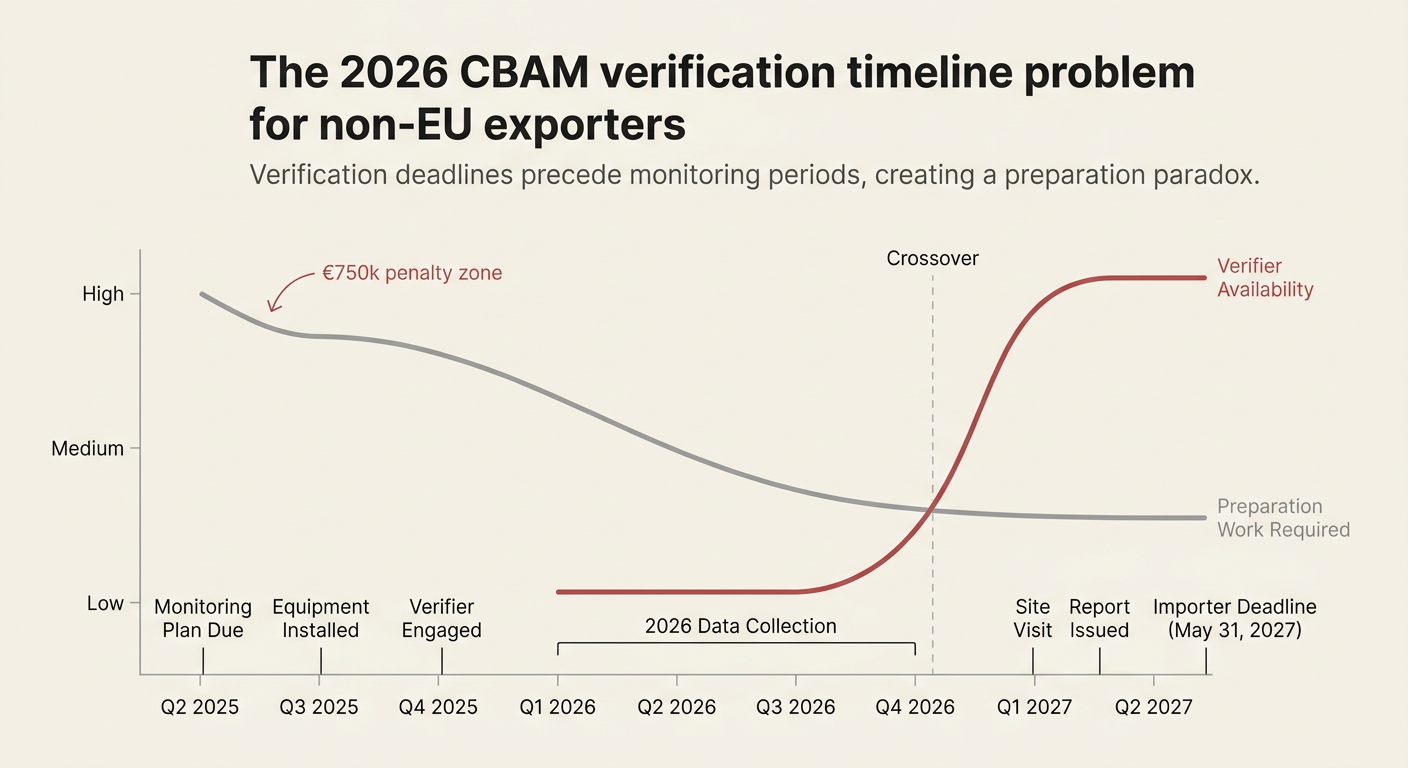

The 2026 CBAM verification timeline problem for non-EU exporters

CBAM verification consists of two things: the emissions declaration and the verifier's site visit. Importers pay for the second—and most exporters have missed the preparation window.

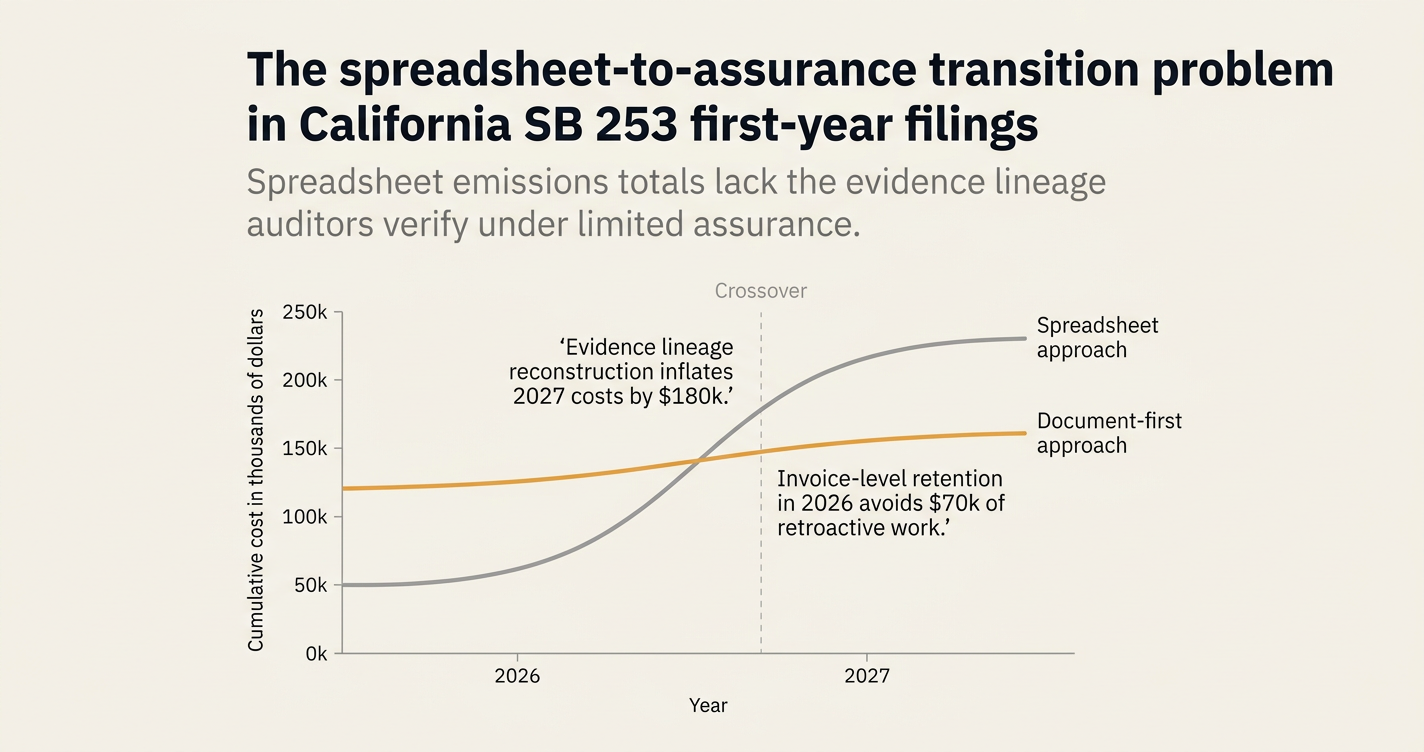

The spreadsheet-to-assurance transition problem in California SB 253 first-year filings

SB 253 filings consist of two things: the emissions number and the evidence lineage. Auditors verify the second—and most CFOs lack it.

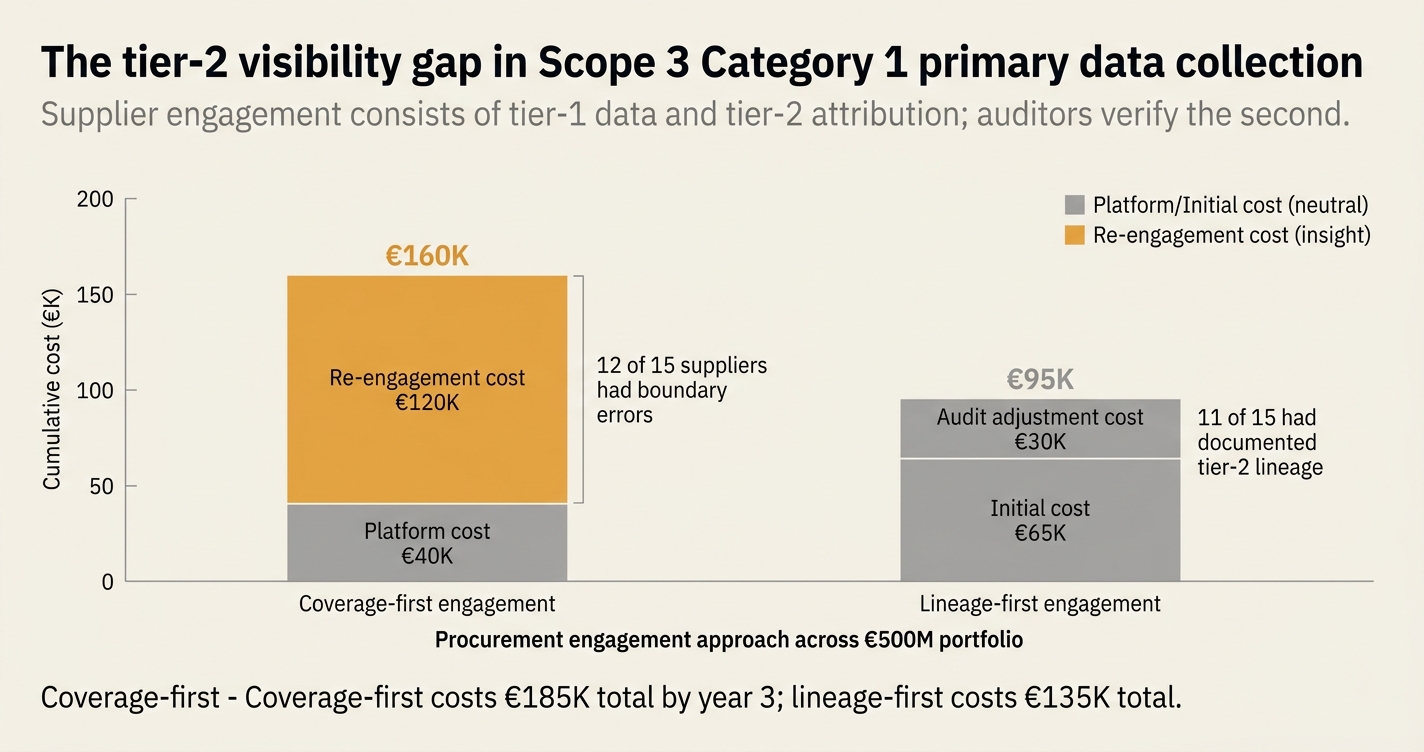

The tier-2 visibility gap in Scope 3 Category 1 primary data collection

Supplier engagement consists of two things: tier-1 data collection and tier-2 emission attribution. Auditors verify the second—and most procurement teams lack it.

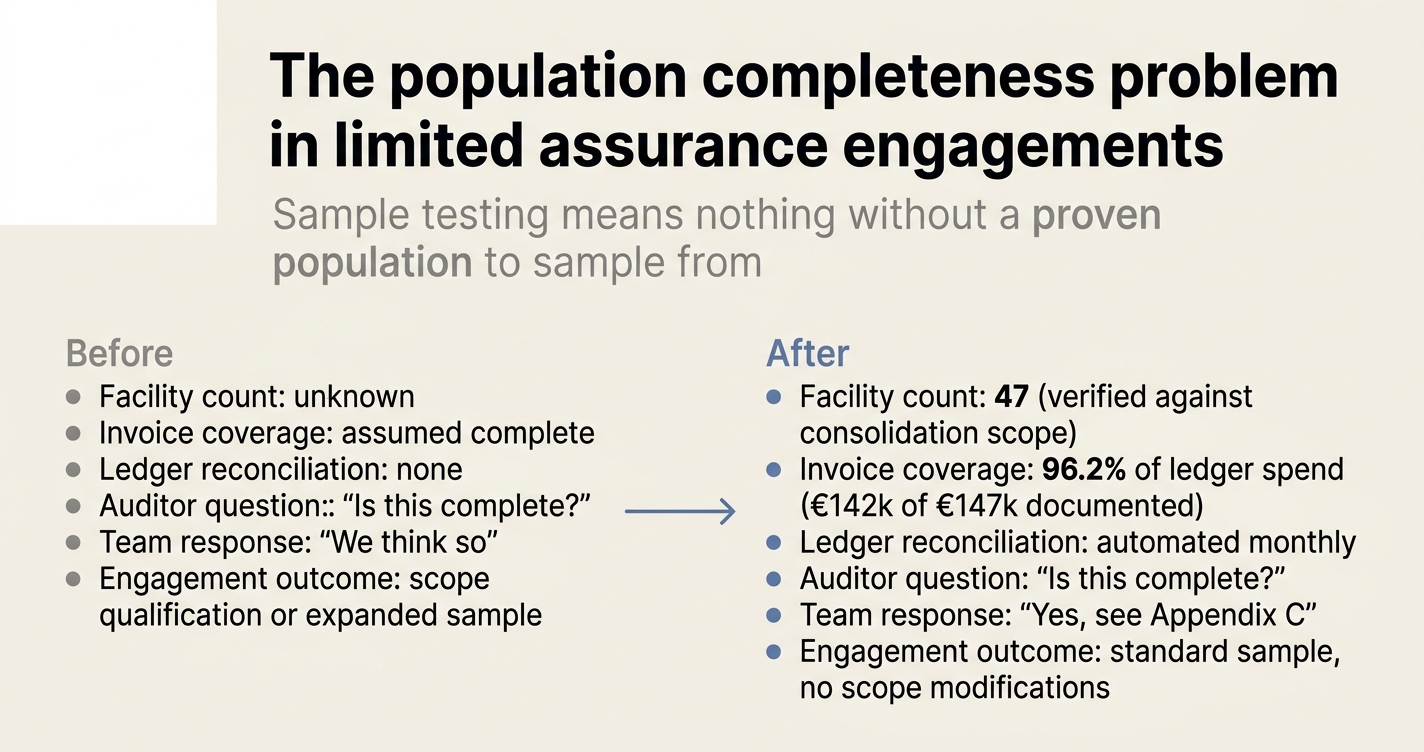

The population completeness problem in limited assurance engagements

Limited assurance consists of two things: sample testing and population inference. Auditors verify the second—and most climate inventories cannot prove it.

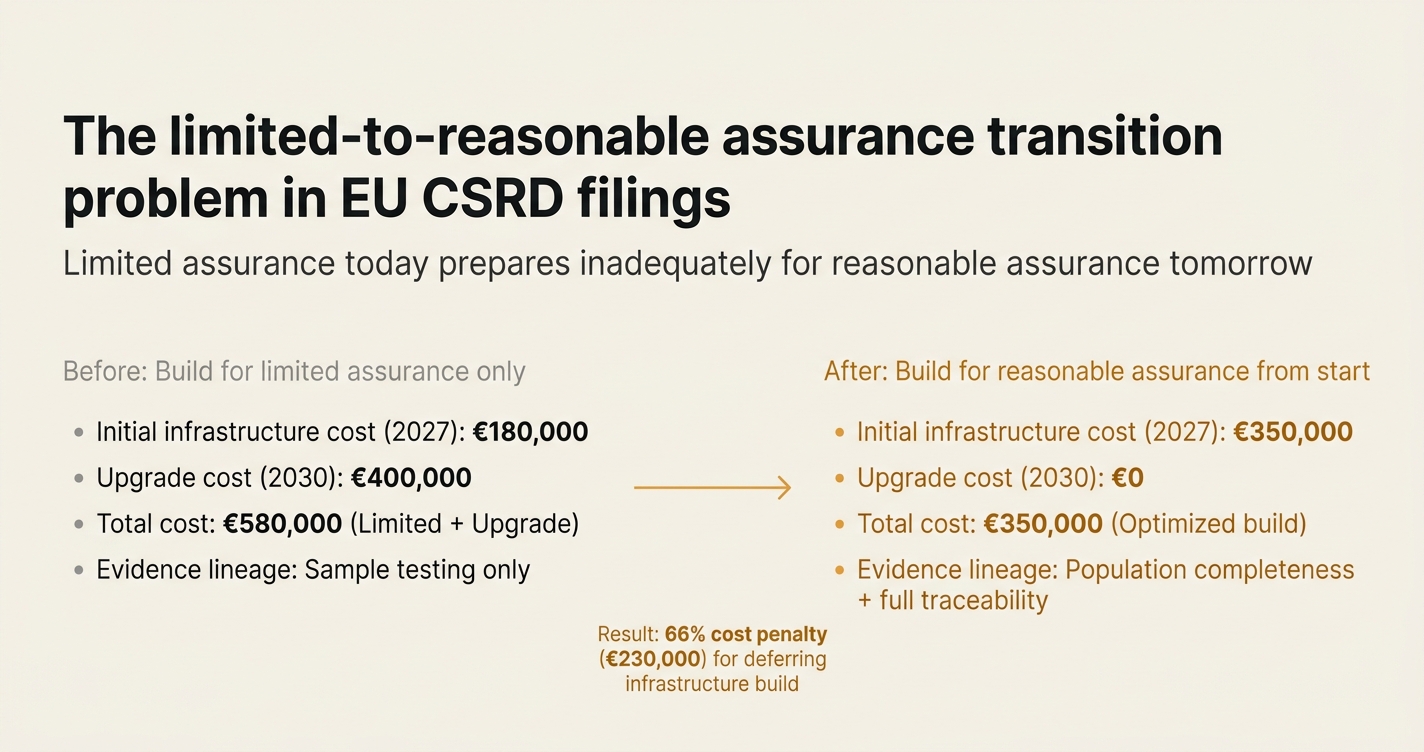

The limited-to-reasonable assurance transition problem in EU CSRD filings

CSRD assurance consists of two things: limited assurance today and reasonable assurance tomorrow. Auditors price for the second—and most filers lack the infrastructure.

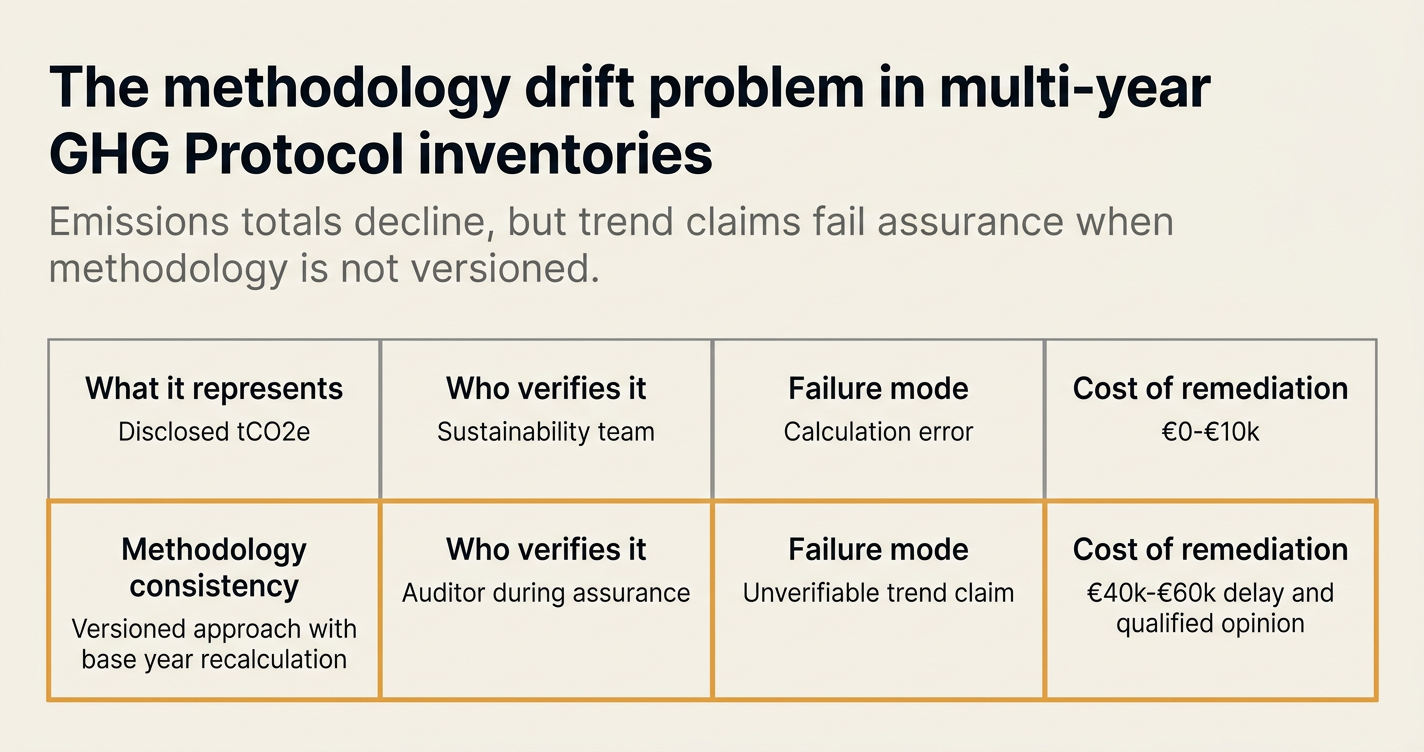

The methodology drift problem in multi-year GHG Protocol inventories

GHG inventories consist of two things: emissions totals and methodology consistency. Auditors verify the second—and most sustainability teams lack it.

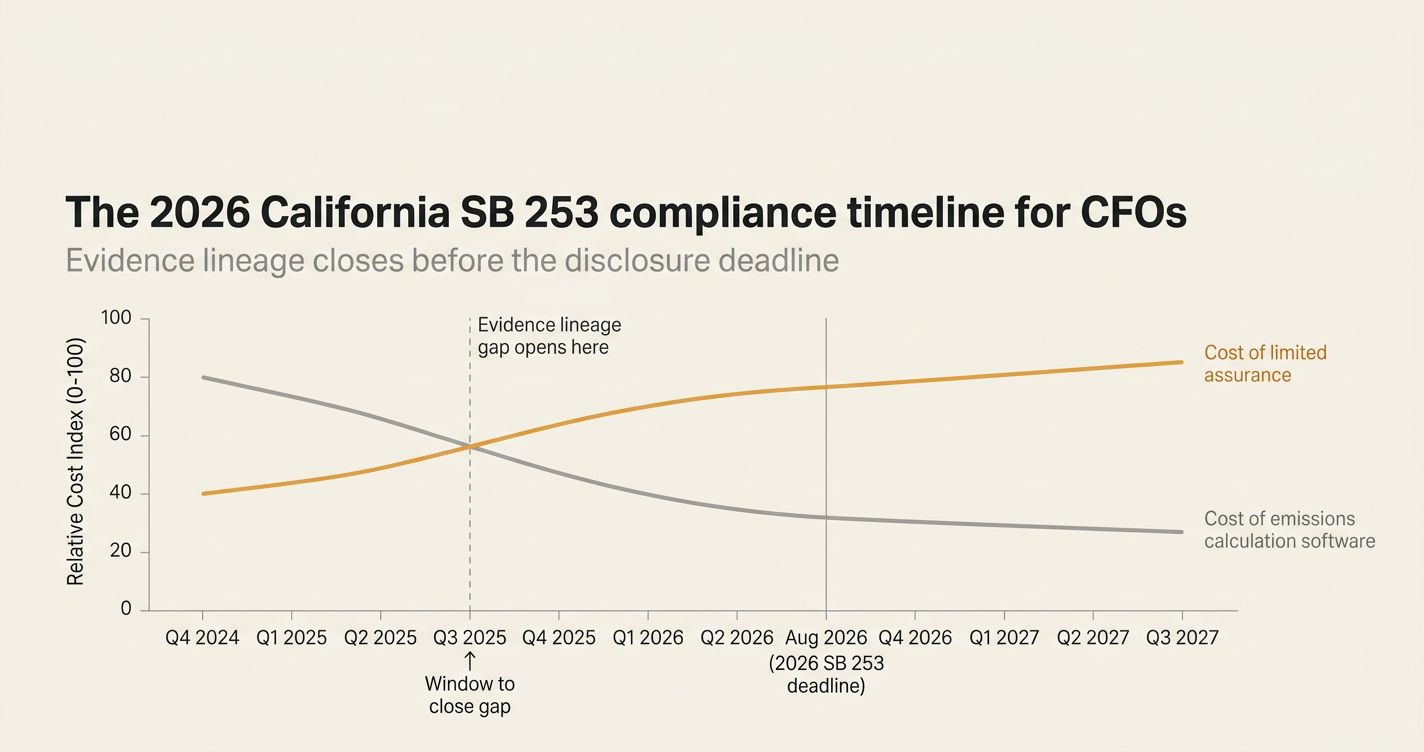

The 2026 California SB 253 compliance timeline for CFOs

SB 253 filings consist of two things: the emissions disclosure and the evidence lineage. Auditors verify the second—and most CFOs are 6-9 months behind schedule.

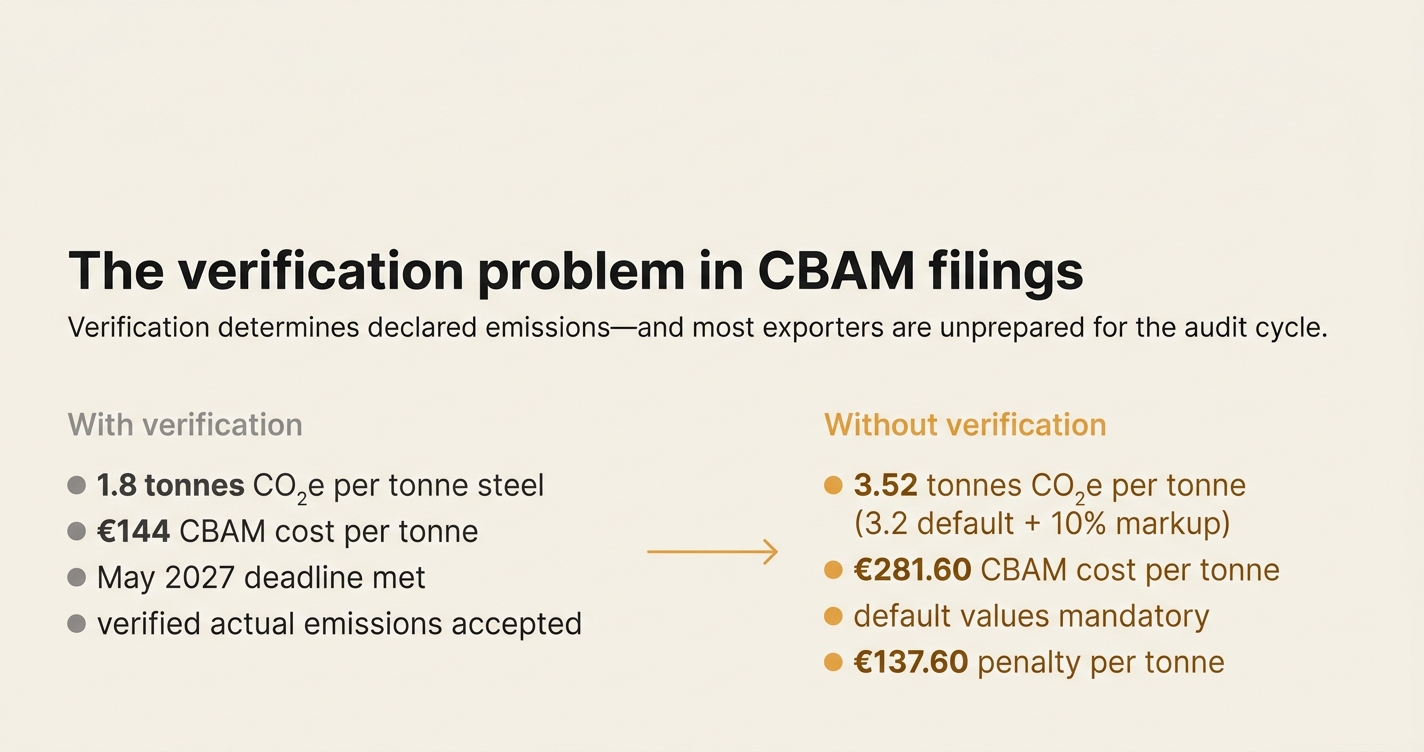

The verification problem in CBAM filings

CBAM filings consist of two things: declared emissions and tariff cost. Verification determines the first—and most exporters are unprepared for the audit cycle.

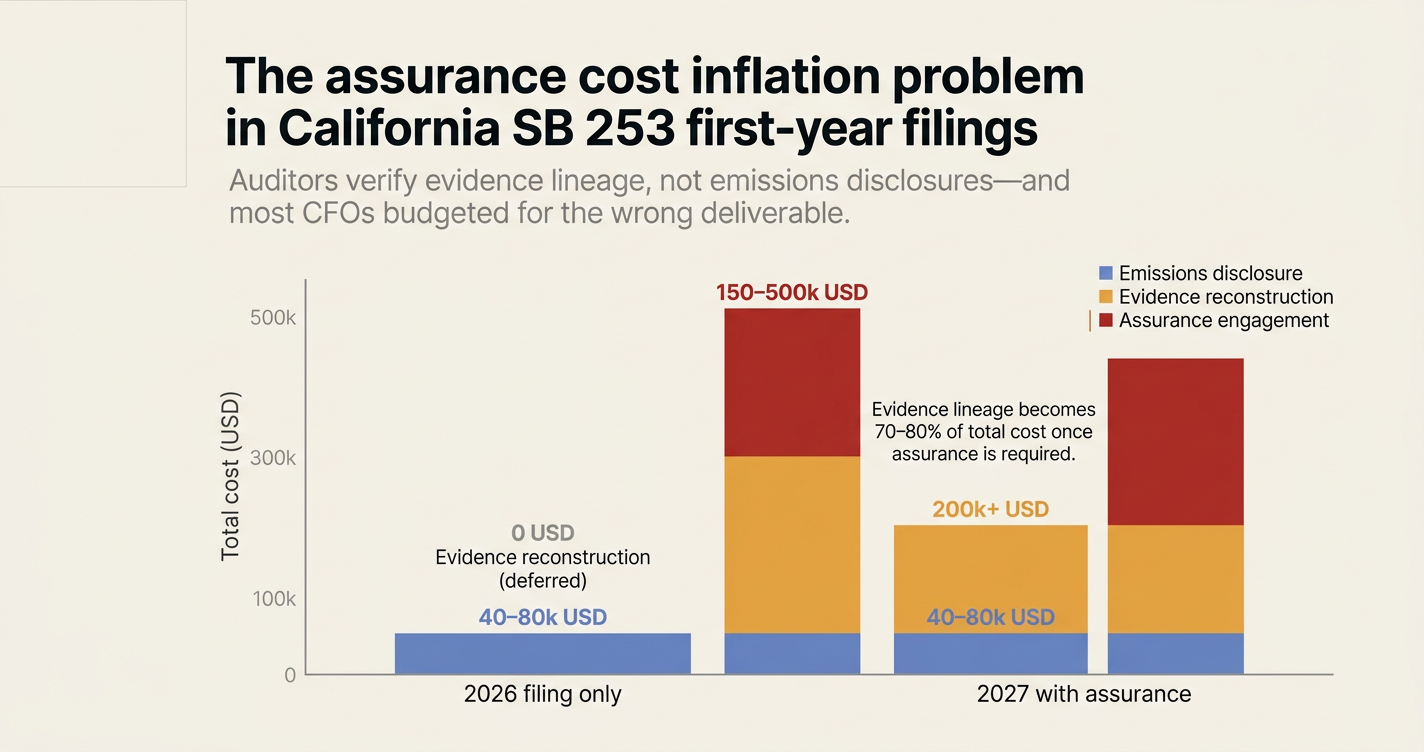

The assurance cost inflation problem in California SB 253 first-year filings

SB 253 filings consist of two things: the emissions disclosure and the evidence lineage. Auditors verify the second—and most CFOs budgeted for the first.

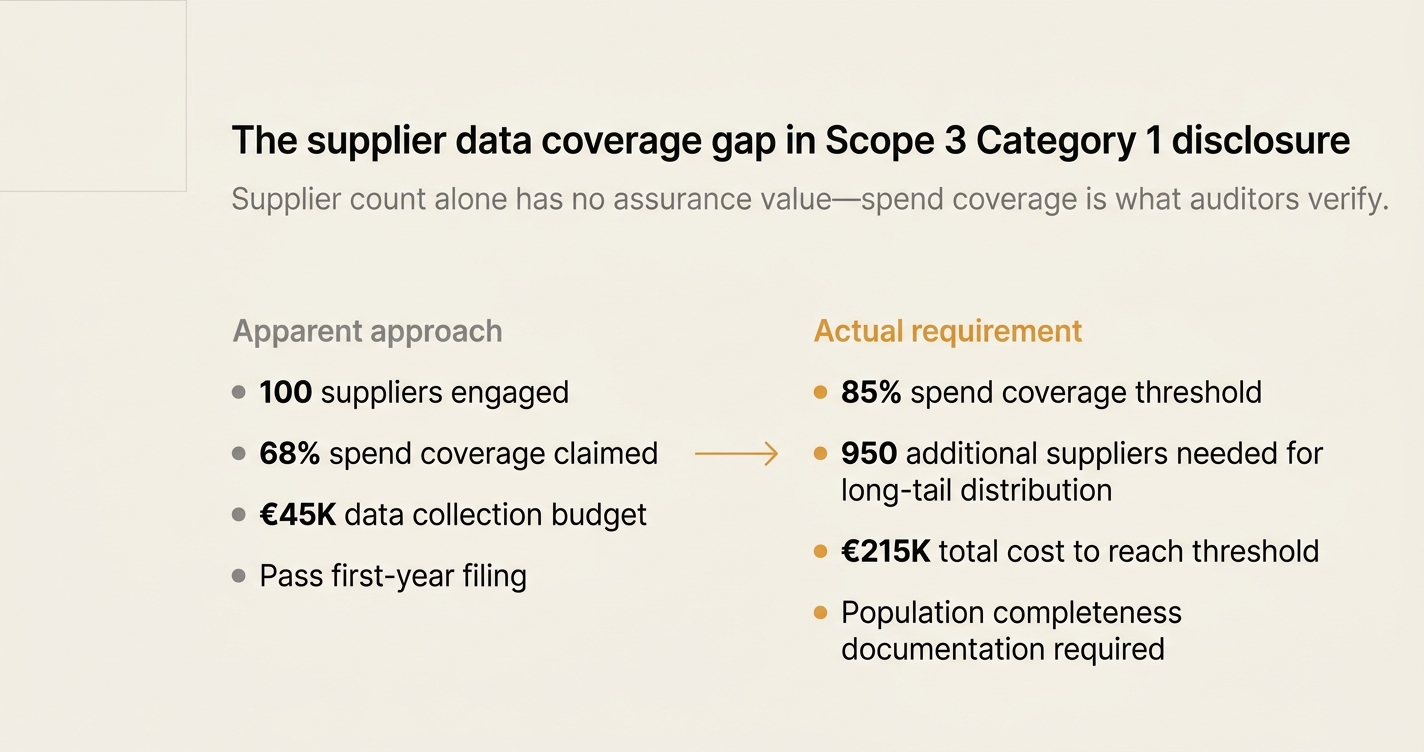

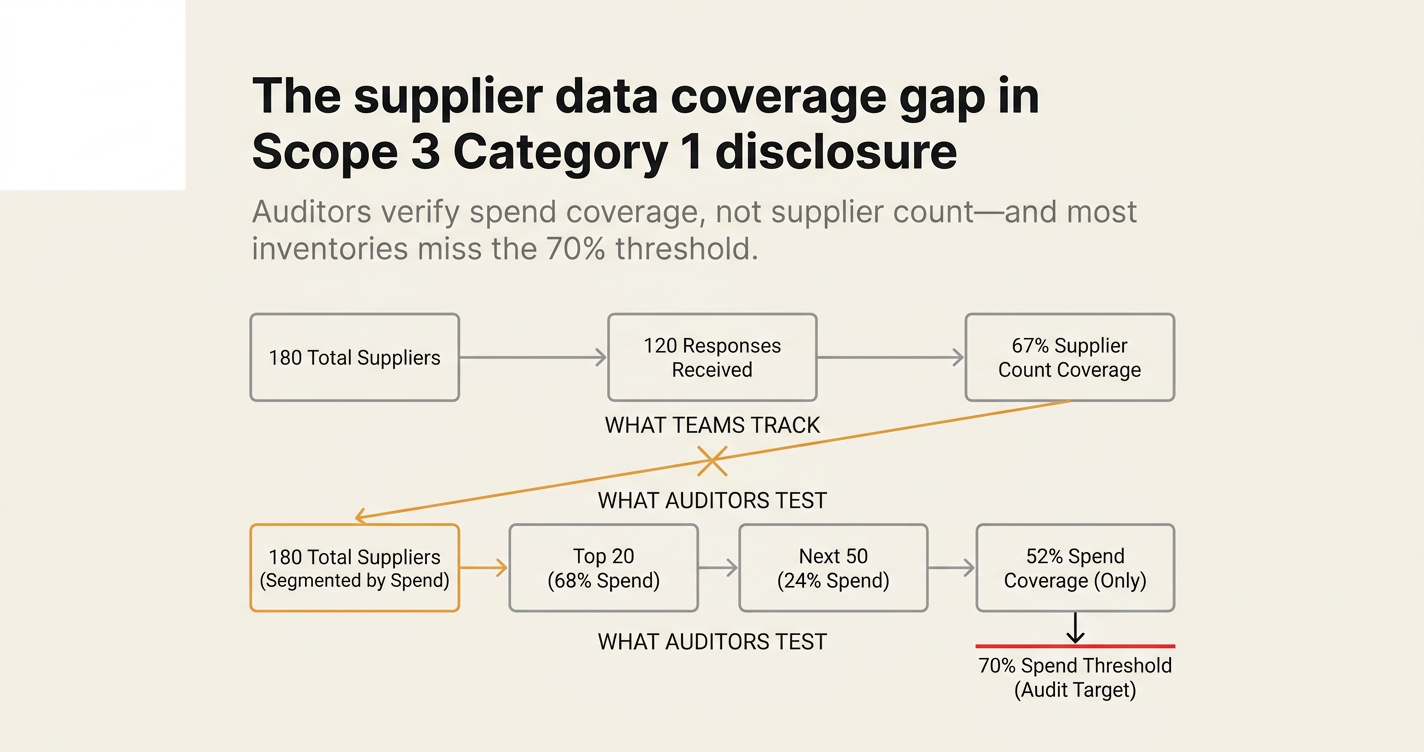

The supplier data coverage gap in Scope 3 Category 1 disclosure

Scope 3 Category 1 disclosure consists of two things: supplier count and spend coverage. Auditors verify the second—and most procurement teams miss it.

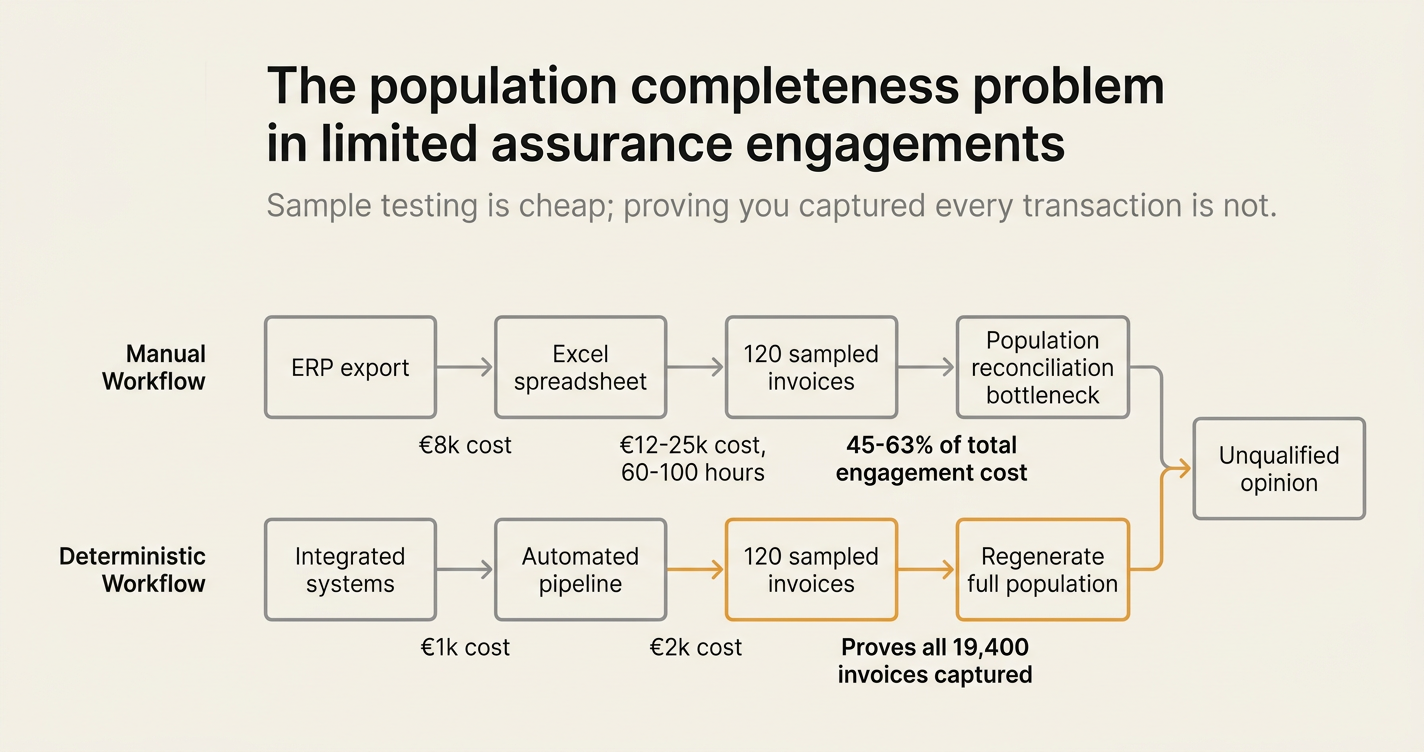

The population completeness problem in limited assurance engagements

Limited assurance consists of two things: sample testing and population inference. Auditors verify the second—and most climate inventories cannot prove it.

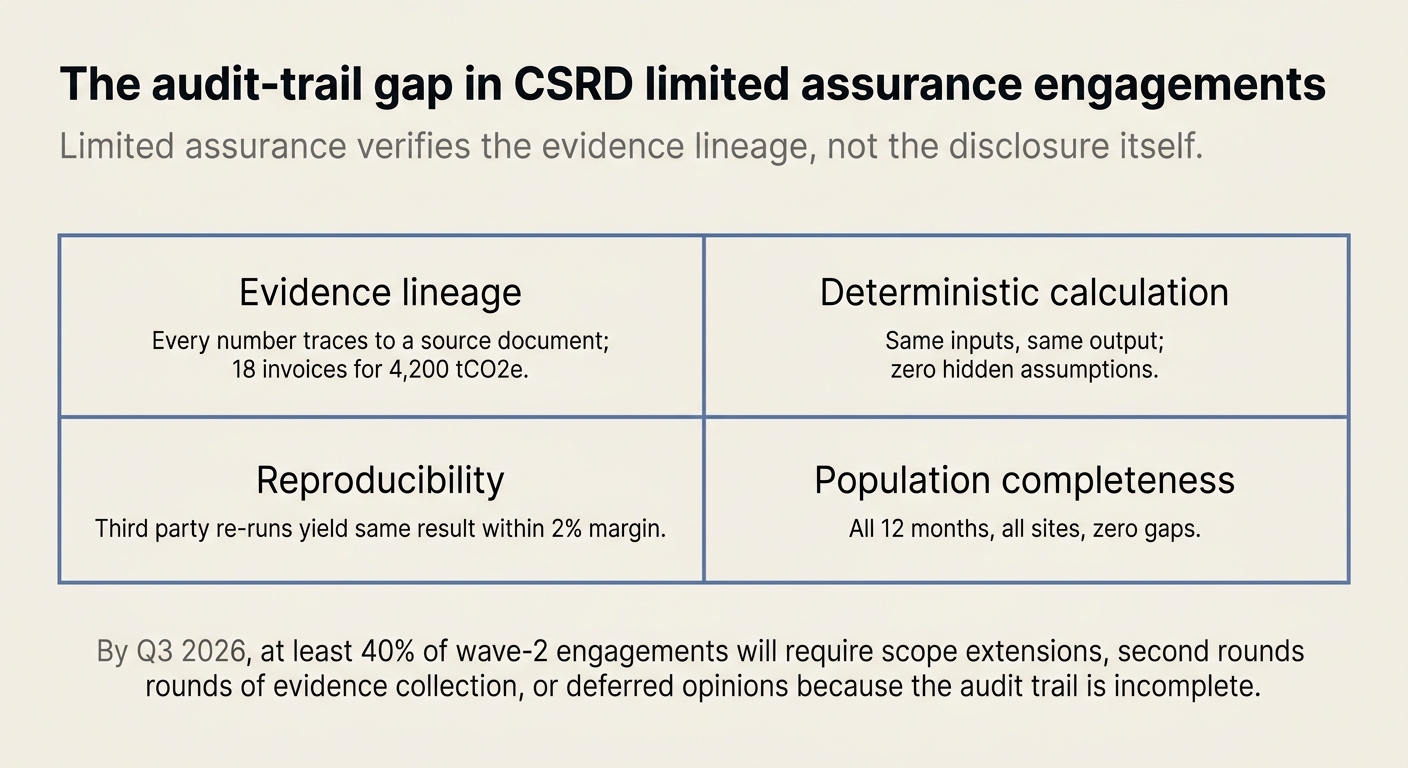

The audit-trail gap in CSRD limited assurance engagements

CSRD limited assurance consists of two things: the sustainability disclosure and the evidence lineage. Auditors verify the second—and most filers lack it.

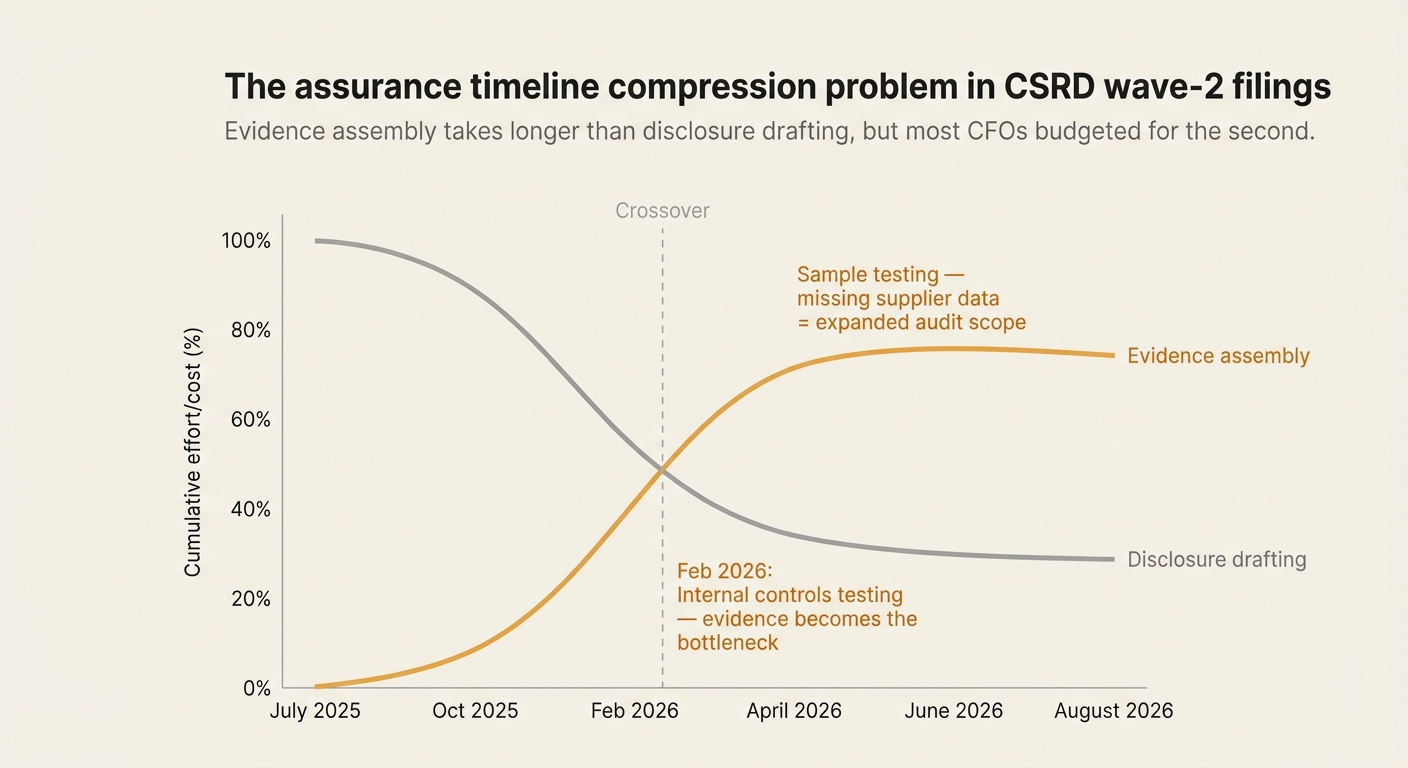

The assurance timeline compression problem in CSRD wave-2 filings

CSRD filings consist of two things: the disclosure itself and the evidence lineage. Auditors verify the second—and most companies are 6-9 months behind schedule.

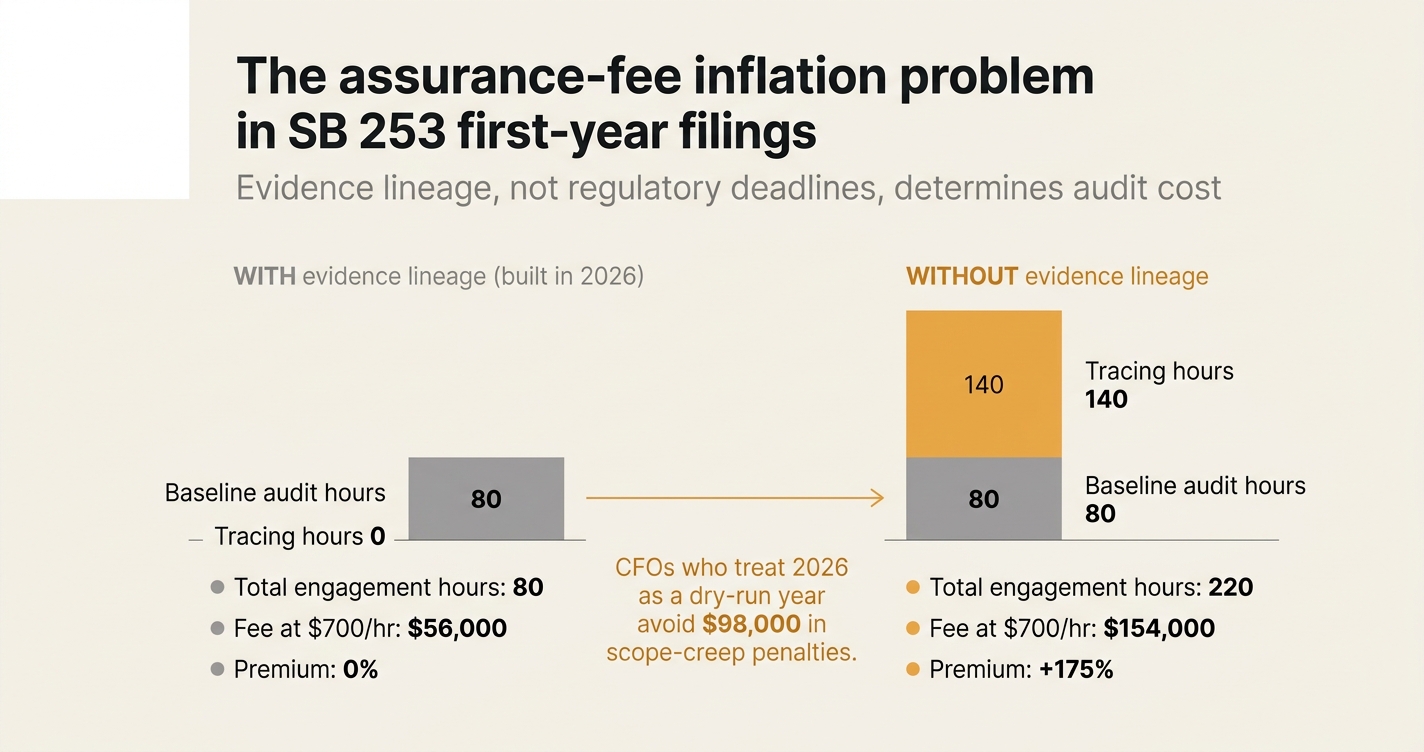

The assurance-fee inflation problem in SB 253 first-year filings

SB 253 filings consist of two things: the emissions number and the evidence lineage. Auditors verify the second—and most CFOs budgeted for the first.

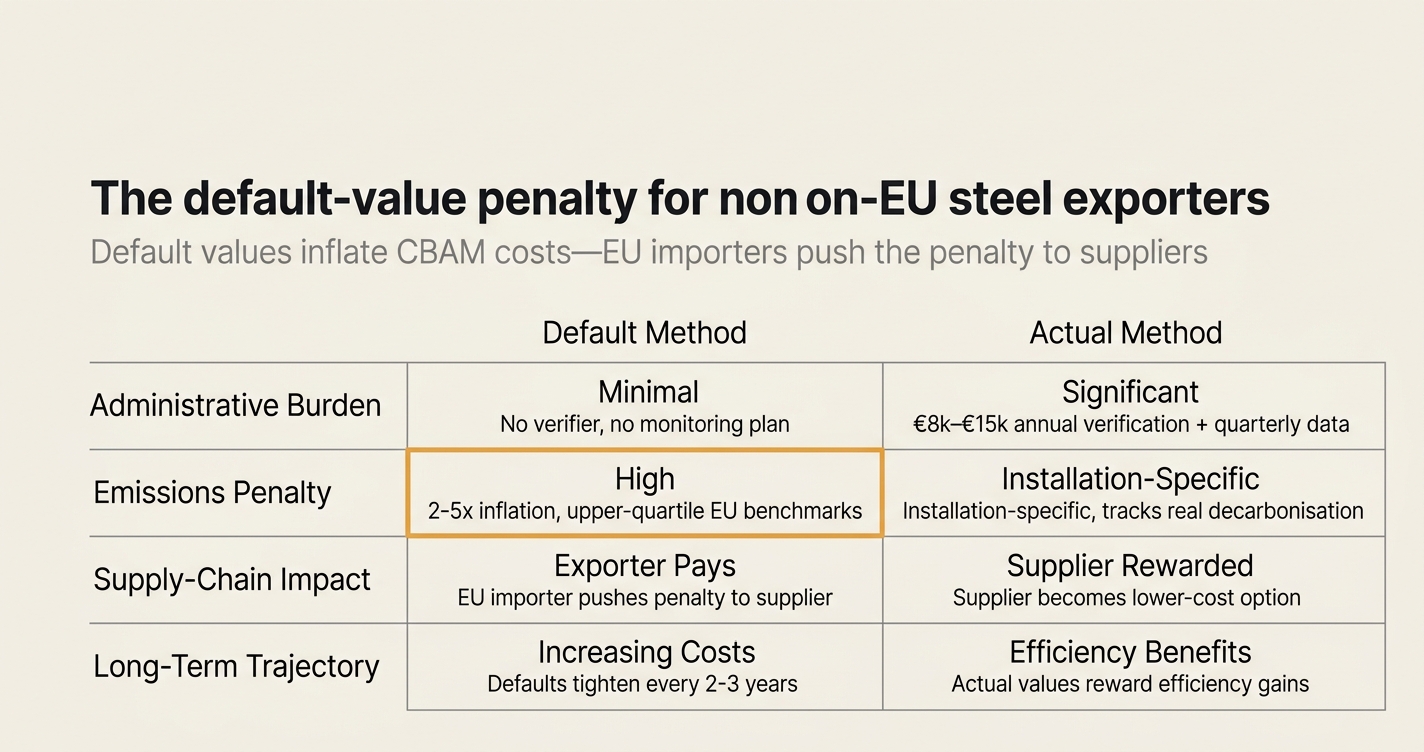

The default-value penalty for non-EU steel exporters

CBAM filings consist of two things: declared emissions and tariff cost. Default values inflate the first—and EU importers will push the second back on the supplier.

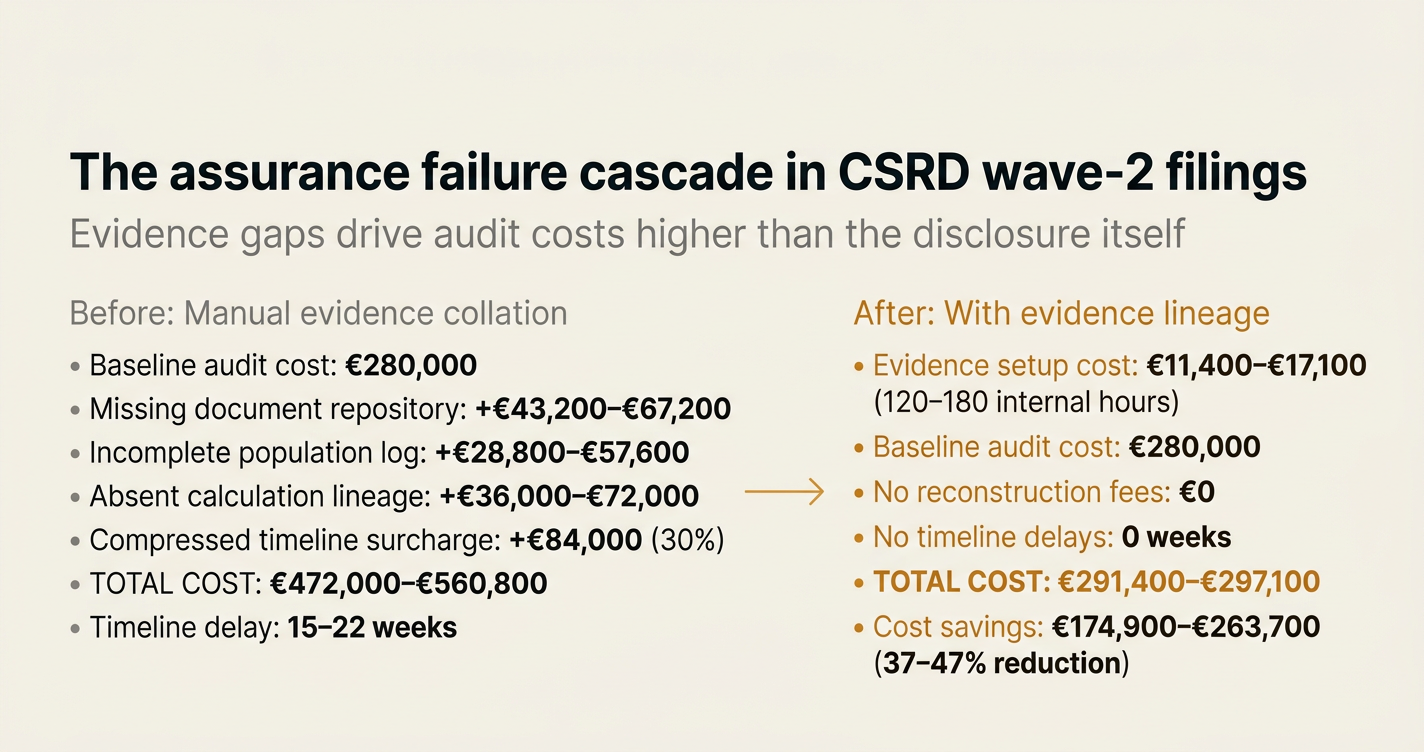

The assurance failure cascade in CSRD wave-2 filings

CSRD wave-2 filings consist of two things: the disclosure itself and the evidence lineage. Auditors verify the second—and most filers are unprepared.

The supplier data coverage gap in Scope 3 Category 1 disclosure

Scope 3 Category 1 disclosure consists of two things: supplier count and spend coverage. Auditors verify the second—and most procurement teams miss it.

Climate Assurance Glossary: 12 Terms Third-Party Auditors Will Use in Your 2026 CSRD Filing

CSRD wave-2 filers face limited assurance in 2026. Here are 12 terms your auditor will use—and what they mean for your evidence requirements.

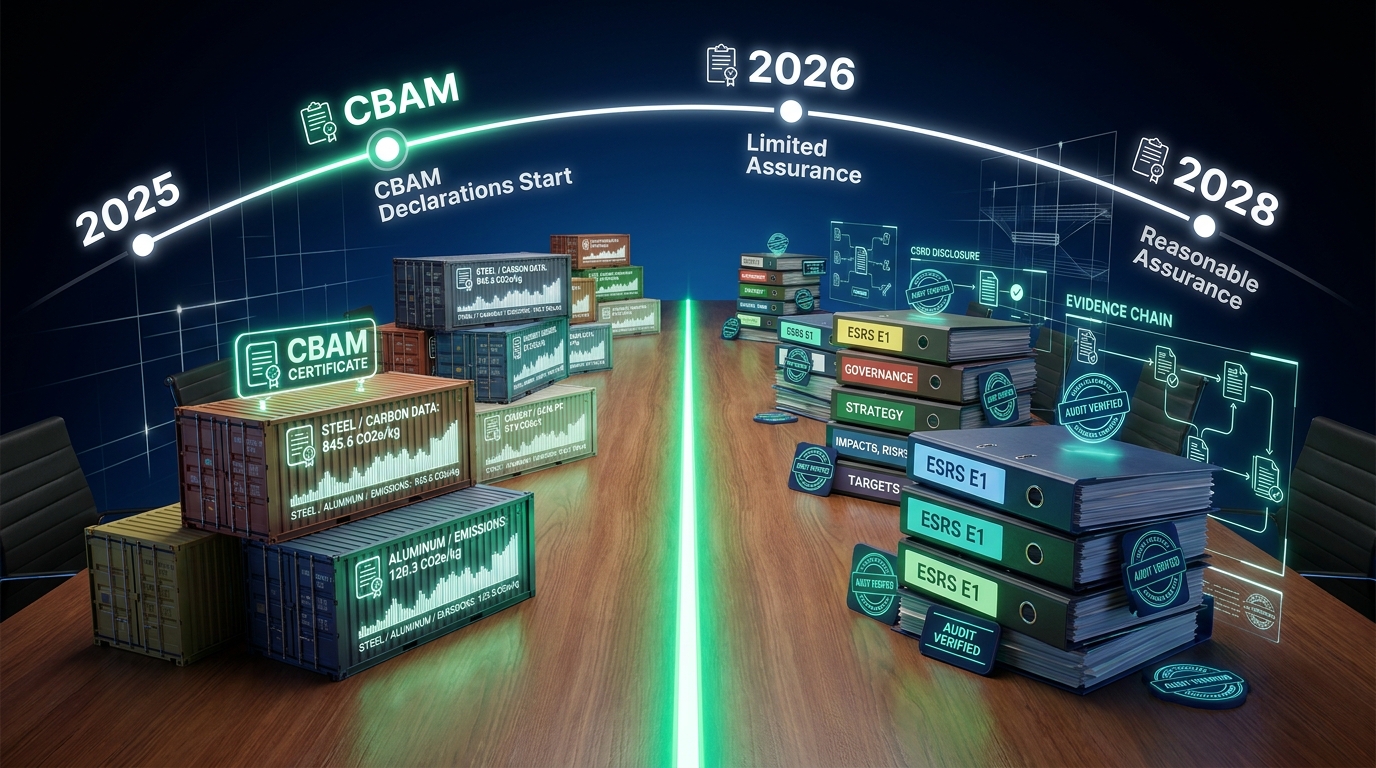

CSRD Wave-2 Limited Assurance: 14 Dates from 2026 to 2028 Most Filers Will Miss

CSRD wave-2 filers report ESRS E1 under limited assurance in 2026, escalating to reasonable assurance by 2028. Most inventories are already behind on 14 critical milestones.

A Mid-Cap CSRD Filer Lost €2.7M in Assurance Failure Costs—Here's the Line-Item Breakdown

A European manufacturer failed ESRS E1 limited assurance in 2026. Restatement, audit fee inflation, and executive liability exposure totalled €2.7M—more than 4x their original budget.

7 Myths About Climate Assurance Costs That Will Fail Your 2026 Filing

Most CFOs underestimate the true cost of failed climate assurance. Restatements, executive liability, and audit fee inflation will exceed €2.4M for mid-cap filers.

CBAM 2026: Why Default Emissions Data Will Cost Non-EU Exporters €14.8B in Preventable Tariffs

Non-EU exporters using default emissions values face 2-5x inflated CBAM costs. Installation-level data cuts certificate expenses—but only 18% of Asian exporters are ready.

CSRD ESRS E1: The 3 Limited Assurance Clauses That Will Fail 68% of Wave-2 Filers in 2026

CSRD wave-2 companies file ESRS E1 under limited assurance in 2026. Three statutory clauses—Scope 3 lineage, credit documentation, transition plan linkage—will fail most inventories.

CSRD & ESRS E1: 12 Terms Supply Chain Leaders Must Know Before 2026 Limited Assurance

CSRD wave-2 filers report ESRS E1 climate data in 2026 under limited assurance. Here are 12 terms supply chain and procurement leaders will hear from auditors.

CSRD & ESRS E1 Timeline: 14 Critical Dates from 2026 Limited to 2028 Reasonable Assurance

CSRD wave-2 filers report ESRS E1 climate data under limited assurance in 2026, escalating to reasonable assurance by 2028. Most inventories miss these milestones.

CSRD Wave-2 Filer Cuts ESRS E1 Audit Prep by 840 Hours Using Document-First Evidence

A European manufacturing group passed ESRS E1 limited assurance in 2026 by building evidence lineage from 19,400 invoices. Here's how they avoided scope 3 sampling failure.

7 Myths About ESRS E1 Climate Disclosure That Will Fail Limited Assurance in 2026

CSRD wave-2 filers face ESRS E1 limited assurance in 2026. Most existing GHG inventories lack the lineage, Scope 3 evidence, and methodology rigor auditors require.

CSRD Wave-2 Filers Face ESRS E1 Limited Assurance in 2026—Most Inventories Will Not Pass

CSRD wave-2 companies report ESRS E1 climate data in 2026 under limited assurance. Most existing GHG inventories lack the granular lineage, Scope 3 evidence, and credit documentation auditors now require.

CSRD vs CBAM: Which Compliance Path Hits Your 2026 Budget Harder?

CSRD wave-2 filers face ESRS E1 limited assurance in 2026. Non-EU exporters face CBAM default premiums. Both require audit-grade data—but the cost structures differ.

The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

California SB 253 Scope 1+2 reports debut in 2026. Here are 12 terms CFOs will hear from auditors—and what they mean for executive liability and assurance fees.

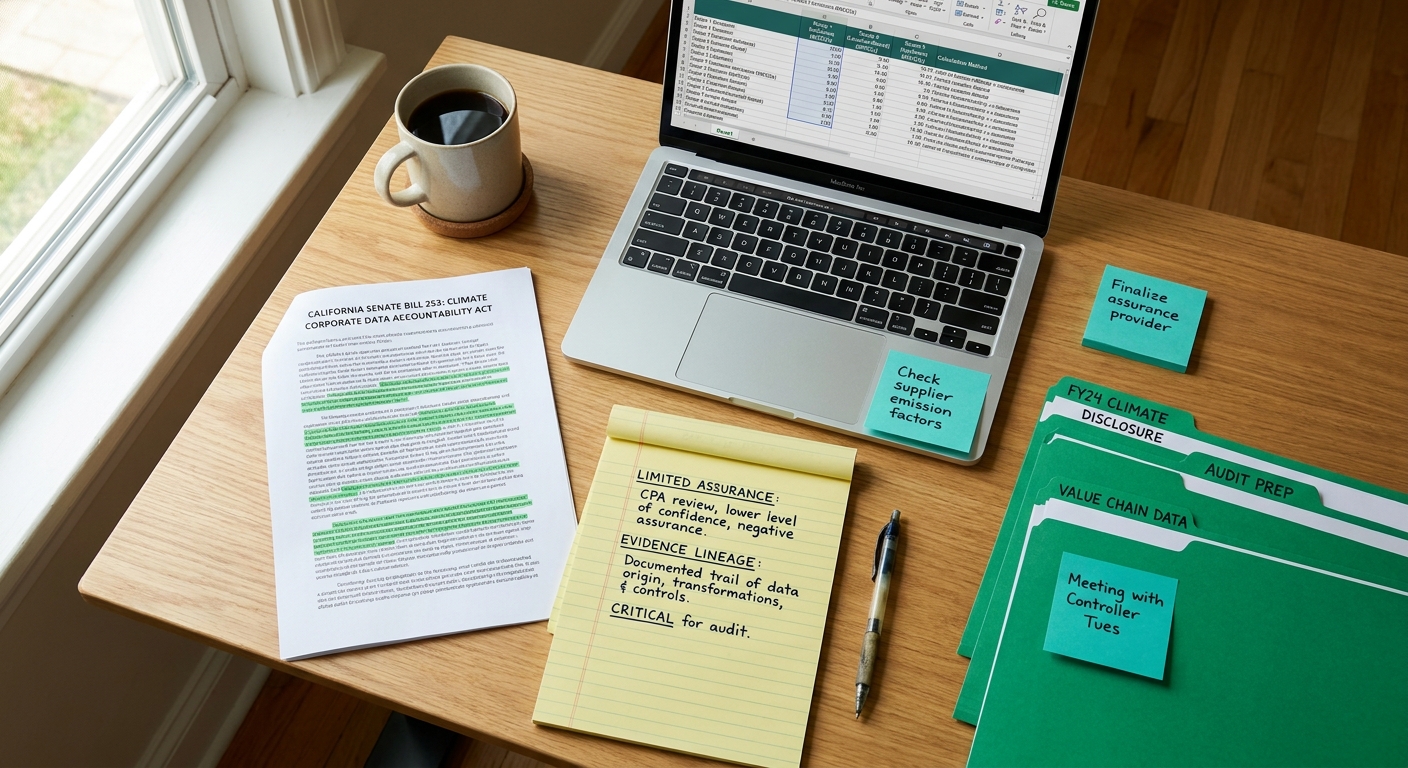

382 Days to First SB 253 Reports: The 2026 Procurement Data Timeline You're Already Behind On

California SB 253 Scope 1+2 reports are due in 2026. Procurement teams need primary supplier data covering 70%+ of spend—and most are starting 18 months late.

How a Big Four Firm Cut 740 Audit Hours on a $2.8B Revenue Client — 2026 SB 253 Case Study

A Big Four assurance team reduced climate audit hours by 62% for a California-headquartered client using document-first evidence. Here's how they avoided sampling failure.

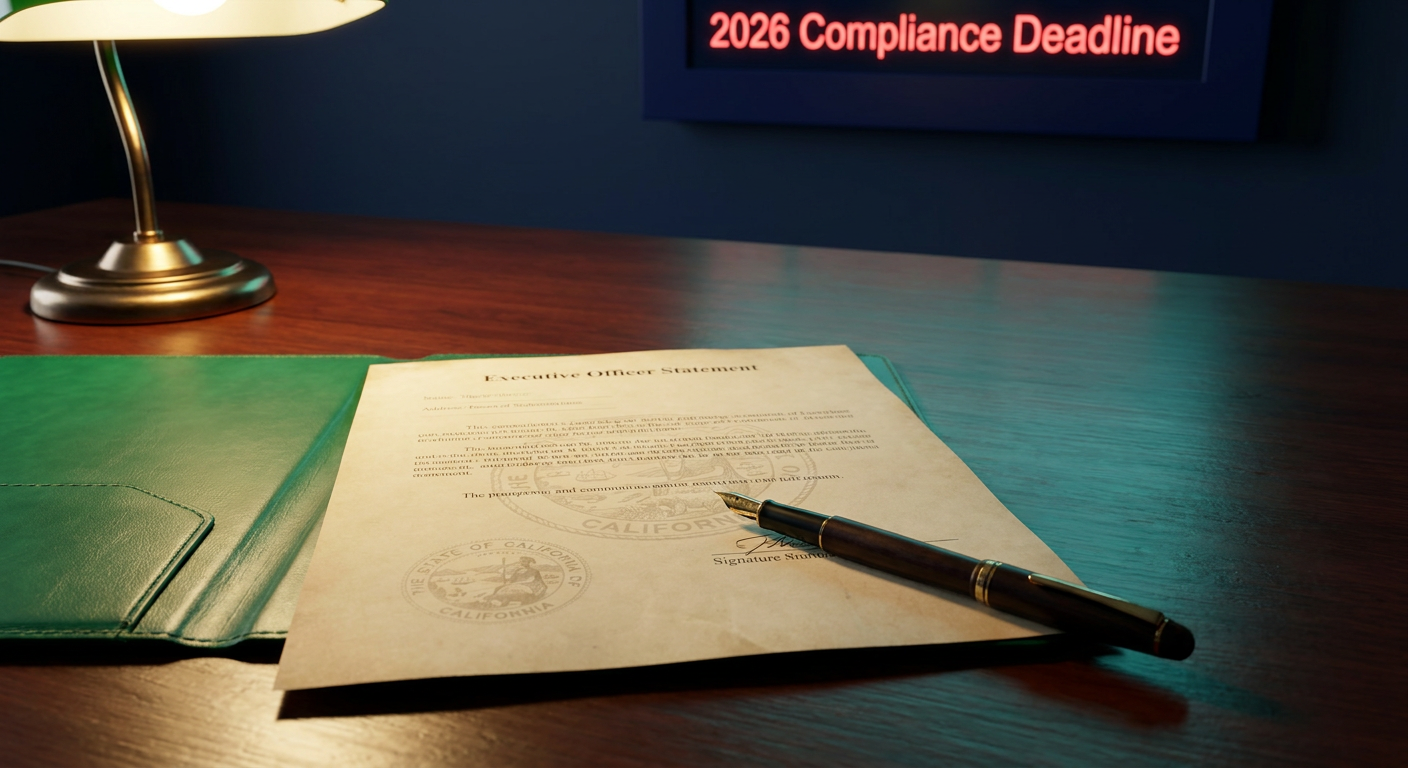

7 Myths About California SB 253 That Could Trigger Executive Officer Liability in 2026

California SB 253 mandates Scope 1+2 disclosure by 2026, with executive officer statements carrying personal liability. These seven myths could expose your officers to enforcement.

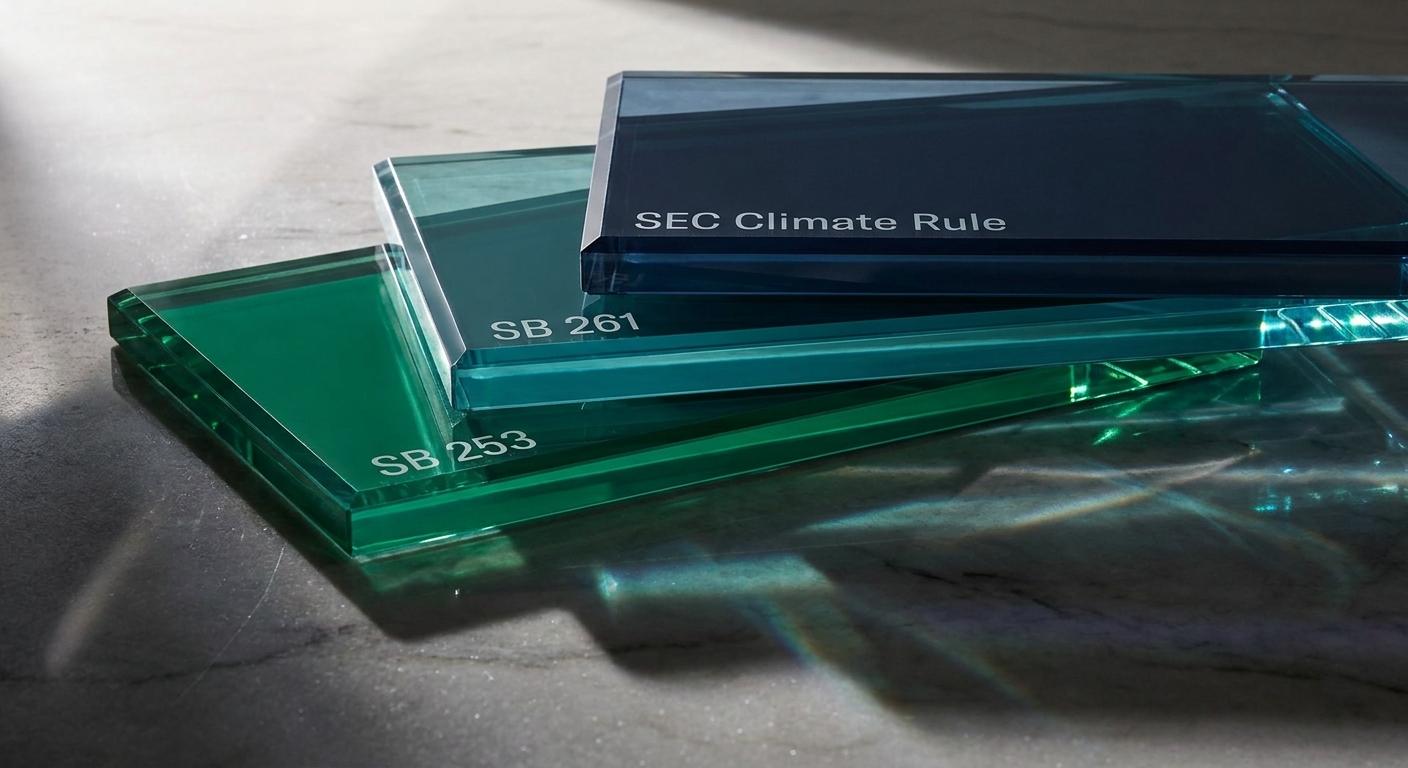

The US Climate Disclosure Stack: SB 253, SB 261, and the 2026 CFO Reckoning

California SB 253 mandates Scope 1+2 disclosure by 2026. SB 261 adds climate risk reporting. The SEC climate rule reshapes materiality. CFOs face a three-layer compliance stack.

Audit Fees for Climate Disclosure: 20-40% Re-Pricing Without Evidence Lineage

Climate disclosure audit fees are re-pricing 20-40% for firms without evidence lineage. Here's what CFOs pay for assurance—and how to avoid premium pricing.

15-Step CBAM Readiness Checklist for Non-EU Exporters: Avoid 2026 Default Premiums

The CBAM transitional period ends December 31, 2025. Non-EU exporters without installation-level data face sectoral defaults 2-5x actual emissions.

382 Days Until CBAM Declarations Become Mandatory: Your 2026 Compliance Timeline

The CBAM transitional period ends December 31, 2025. Non-EU exporters have 382 days to secure installation-level data or face sectoral defaults 2-5x real emissions.

How a €12M Procurement Team Avoided €2.1M in CBAM Default Premiums — A 2026 Case Study

A European manufacturer transformed tier-2 supplier data capture in 11 months — avoiding €2.1M in CBAM default penalties by securing primary emissions data for 73% of spend.

7 CBAM Myths Third-Party Auditors Believed — Until the 2026 Cliff

The CBAM transitional period ends December 31, 2025. Here are the seven myths auditors believed—and the reality of population-level evidence requirements.

CBAM 2026: Why 47% of EU Importers Will Pay Default Premiums — And How to Avoid It

The CBAM transitional period ends December 31, 2025. Nearly half of EU importers lack installation-level data—triggering sectoral defaults 2-5x real emissions.

CBAM Compliance 2026: Default Method vs Actual Emissions — Which Route Will Cost You More?

The CBAM transitional period ends December 31, 2025. Non-EU exporters face a stark choice: submit actual installation data or pay sectoral defaults—often 2-5x real emissions.

15-Step CFO Checklist: Survive the 2026 CBAM Cliff Without Paying Default Premiums

The CBAM transitional period ends December 31, 2025. Non-EU exporters without installation-level data will pay sectoral defaults—2-5x their actual footprint.

SB 253's $500K Penalty Hammer: California's New Climate Law Decoded

California's groundbreaking SB 253 mandates emissions reporting for $1B+ revenue companies. Learn the deadlines, penalties, and compliance requirements for 2026-2027.

Stay Updated

Planning CBAM reporting or supplier data collection? Book a CBAM readiness call after you subscribe; we’ll align on timeline and scope.