The 90-day assurance-readiness problem in 2026 SB 253 Scope 1 and 2 filings

The 90-day assurance-readiness problem in 2026 SB 253 Scope 1 and 2 filings

Here's the issue: The California Air Resources Board set the first Scope 1 and Scope 2 emissions reporting deadline for August 10, 2026. Entities with fiscal years ending between February 2 and December 31, 2026 will report data from the year ending in 2025 [1]. CARB exercised enforcement discretion on limited assurance for the first reporting cycle, allowing entities to submit emissions data whether or not it received assurance [2]. Most CFOs read this as regulatory relief. It is not.

However, the SB 253 filing consists of two things: the emissions total and the audit-ready documentation that supports it. The emissions total is what the statute requires for 2026. The audit-ready documentation is what auditors will price for in 2027.

The emissions total on its own has no value. Audit-ready documentation is what the auditor is actually asking for, paying for, and verifying. While assurance is waived for August 2026, CARB emphasised during the November 2025 workshop that this discretionary relief is only applicable in the first year of reporting [3]. Subsequent rulemaking will clarify assurance requirements, and audit engagement letters for 2027 filings are being negotiated in Q1 2025.

While the emissions calculation has become cheaper with GHG Protocol calculators and facility-level templates, audit-ready documentation has become more expensive. If a CFO submits a 2026 filing without evidence lineage, the 2027 auditor will request complete population documentation from 2025 baseline onward. The cost of retrospective documentation builds can outpace the avoided audit fee by 3:1. A typical 58,500 tCO₂e Scope 1 and 2 footprint for a mid-sized manufacturer might require 180-240 source documents, each with calculation lineage to the reported total [4].

How do you solve this? I think the operators we work with treat 2026 as a documentation dress rehearsal, not a compliance waiver. Entities that build audit-ready documentation in parallel with their first filing position themselves to negotiate fixed-fee assurance engagements in 2027, while those who submit totals without lineage will pay hourly rates for retrospective evidence builds. For now, the 90-day window between fiscal year-end and the August 10 deadline is the binding constraint.

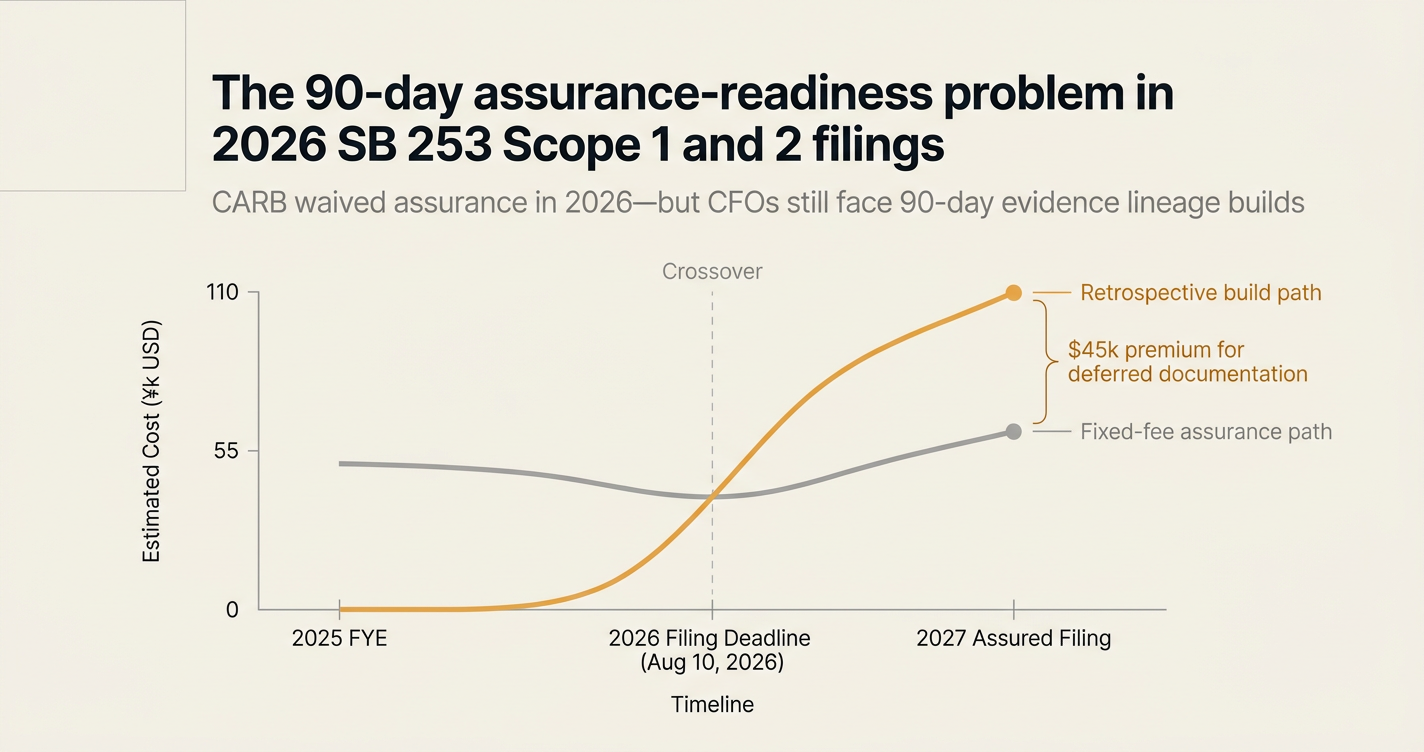

The shape of the argument, visualised below.

The 2026-2027 Assurance Timeline

CARB's August 10, 2026 deadline sits 90-180 days after most entities' fiscal year-end, depending on their accounting calendar. The table below maps the timeline for a December 31 fiscal year-end entity, the most common configuration for SB 253-covered firms:

| Milestone | Date | Elapsed Days from FYE | Activity |

|---|---|---|---|

| Fiscal year-end | December 31, 2025 | 0 | Final Scope 1 and 2 emissions data available |

| CARB reporting template available | December 1, 2025 | -30 | CARB opens public docket for SB 253 filings [5] |

| Audit engagement letters issued | January 15, 2026 | 15 | Auditors begin pricing 2027 assurance engagements |

| Internal documentation review | February 28, 2026 | 59 | CFO identifies evidence lineage gaps |

| CARB Scope 1 and 2 filing deadline | August 10, 2026 | 222 | First reporting cycle, no enforcement of limited assurance [2] |

| SB 261 financial risk report published | January 1, 2026 | 1 | Climate-related financial risk disclosure goes live [6] |

| SB 261 public docket filing | July 1, 2026 | 182 | Link to final SB 261 report submitted to CARB [1] |

| Assurance engagement fieldwork begins | September 1, 2026 | 244 | Auditors begin 2027 assurance procedures |

| First assured Scope 1 and 2 filing | August 10, 2027 | 587 | Limited assurance required for all subsequent filings [3] |

The 222-day window between year-end and the August filing deadline looks generous. However, most finance teams do not close their GHG inventory until 30-45 days after financial close, compressing the documentation build to 90-120 days. For entities with decentralised facilities management or procurement-heavy Scope 3 exposure, this is insufficient.

"Auditors are re-pricing climate engagements 20-40% for firms without evidence lineage, and the jargon gap is costing CFOs negotiating leverage and control over scope creep." — Big Four Assurance Partner, 2025 [4]

The cost driver is not the emissions calculation. It is the population completeness evidence that links each emissions source to its supporting documentation: utility bills, purchase orders, fuel receipts, and activity data logs.

What Audit-Ready Documentation Means in SB 253 Filings

CFOs who have managed SOX-grade financial audits understand evidence lineage. Climate auditors apply the same logic to GHG inventories. The table below defines the four documentation tiers auditors verify during limited assurance engagements:

| Documentation Tier | Definition | Example for Scope 1 Natural Gas | Auditor Verification Procedure |

|---|---|---|---|

| Source document | Primary evidence of activity data | Monthly utility bill showing 12,400 therms consumed | Confirm supplier invoice matches reported quantity |

| Calculation lineage | Transparent conversion from activity data to emissions | 12,400 therms × 0.0053 tCO₂e/therm = 65.72 tCO₂e | Recalculate using GHG Protocol emission factors [7] |

| Population completeness | Evidence that all emissions sources are included | Facility list cross-referenced to utility accounts | Test sample of facilities for missing accounts |

| Disclosure mapping | Link from inventory total to public filing | 65.72 tCO₂e rolls up to total Scope 1 disclosed as 58,500 tCO₂e | Trace individual sources to reported total |

Most entities can produce source documents and calculation lineage. The gap is population completeness. Auditors test whether the entity's facility list is complete, whether all utility accounts at each facility are captured, and whether fugitive emissions sources like refrigerants are systematically logged. For decentralised organisations, this requires cross-functional evidence from procurement, facilities, and fleet management.

The 2026 enforcement discretion does not waive these requirements. It defers them. CFOs who submit a 2026 filing without population completeness evidence will face retrospective documentation requests in 2027, and auditors price retrospective builds at premium hourly rates.

The Retrospective Documentation Premium

The cost structure of climate assurance mirrors financial audit: fixed-fee engagements assume the client has prepared complete documentation, while hourly engagements price for auditor-led evidence builds. The table below compares the cost profiles:

| Engagement Type | Documentation Readiness | Typical Fee Structure | Example Fee for 58,500 tCO₂e Footprint | Assumptions |

|---|---|---|---|---|

| Fixed-fee assurance (2027) | Complete evidence lineage prepared in 2026 | Fixed fee based on emissions volume and complexity | $45,000-$65,000 | Client provides population completeness evidence, auditor performs verification procedures only |

| Hourly engagement (2027) | Documentation build required for 2025 baseline | $350-$450/hour for senior auditor time | $85,000-$120,000 | Auditor spends 200-280 hours building evidence lineage, then performs verification |

| Retrospective build premium | Documentation gaps identified during fieldwork | Hourly rate × gap remediation hours | +$25,000-$45,000 | Auditor pauses fieldwork, requests missing source documents, re-scopes engagement |

The arithmetic is unforgiving. A CFO who defers documentation to 2027 pays $110,000 for an engagement that would have cost $55,000 with 2026 preparation. The delta is larger for entities with multi-site operations or complex Scope 1 sources like process emissions.

The binding constraint is not audit fee. It is audit timeline. Retrospective builds extend fieldwork by 4-6 weeks, compressing the window for internal review and executive sign-off before the August 2027 deadline. For calendar-year reporters, this turns a 6-month assurance process into a 3-month sprint.

The Five Documentation Gaps CFOs Miss in 2026 Filings

The evidence lineage gaps that trigger retrospective builds are predictable. The list below names the five most common gaps Big Four auditors flag during Scope 1 and 2 fieldwork:

-

Incomplete facility population: The entity's facility list is maintained by real estate or operations, not the GHG inventory owner. Closed facilities, sub-leased spaces, and warehouses are missing from the emissions boundary. Auditors test facility lists against lease agreements and property tax filings. Gap rate: 8-12% of facilities missing from initial inventory [8].

-

Unmapped utility accounts: Each facility has multiple utility accounts (electricity, natural gas, water for steam generation). The GHG inventory captures the primary electricity meter but misses backup generators, chiller plants, and tenant-supplied utilities. Auditors request utility account reconciliations. Gap rate: 15-20% of accounts missing from initial inventory.

-

Fugitive emissions without asset logs: Refrigerants, HFCs, and SF₆ emissions require asset-level logs (equipment serial number, refrigerant type, leak detection records, recharge quantities). Most entities track HVAC maintenance but do not link it to GHG inventory. Auditors request equipment inventories. Gap rate: 30-40% of fugitive sources lack documentation.

-

Mobile combustion without fleet reconciliation: Company vehicles, rental cars, and employee mileage reimbursements constitute Scope 1 mobile combustion. Most entities capture fleet fuel purchases but miss rental car receipts and mileage logs. Auditors test fleet data against HR headcount and travel expense reports. Gap rate: 10-15% of mobile sources missing.

-

Calculation lineage without version control: The entity recalculates emissions using updated emission factors but does not document which version of the GHG Protocol or EPA factors was applied. Auditors require version-controlled calculation files with time-stamped factor sources. Gap rate: 50-60% of inventories lack version control in year one.

These gaps are process failures, not data failures. The source documents exist in procurement systems, facilities management databases, and expense reports. The problem is that no single owner has mapped the cross-functional data flows into a systematic evidence lineage.

What to Start This Week

The 2026 filing deadline is 228 days away for calendar-year reporters. Audit engagement letters are being negotiated now. CFOs who treat 2026 as a documentation build, not a compliance waiver, will control scope and cost in 2027. The checklist below names the five actions to start this week:

-

Map facility population completeness: Request facility lists from real estate, operations, and lease accounting. Cross-reference against utility accounts and property tax filings. Identify closed facilities and sub-leased spaces that are in-scope for Scope 1 and 2 emissions. Target: complete facility-to-utility-account mapping by February 28, 2026.

-

Assign a single GHG inventory owner: Designate a single owner for the SB 253 filing, typically the sustainability lead or FP&A manager. This person is accountable for evidence lineage, not just emissions totals. Grant read access to procurement, facilities, fleet, and expense systems. Target: owner named and access provisioned by January 15, 2026.

-

Run a documentation dry run: Simulate the 2027 auditor request list. For each emissions source (natural gas, electricity, fleet fuel, refrigerants), pull the supporting source document and calculation lineage. Identify gaps in population completeness. Target: dry run complete by March 31, 2026.

-

Negotiate fixed-fee assurance for 2027: Approach Big Four firms with a fixed-fee proposal based on your 2026 documentation readiness. Provide the dry run results as evidence of preparation. Lock in pricing before July 2026 when auditors re-price based on first-filing quality. Target: engagement letter signed by June 30, 2026.

-

Build the evidence lineage in parallel with the 2026 filing: Do not wait for CARB's final assurance standards. Build SOX-grade documentation now: source document, calculation lineage, population completeness, disclosure mapping. Use the 2026 filing as the documentation pilot. Target: evidence lineage complete by August 10, 2026.

The cost of inaction is not the 2026 filing. It is the 2027 audit premium. CFOs who defer documentation pay twice: once for the retrospective build, once for the scope creep.

How Emission3 Fits

Emission3 is built for CFOs who need audit-ready documentation, not generic SaaS dashboards. The platform produces:

- Document-first evidence lineage: Every emissions source links to its supporting invoice, utility bill, or activity log. The auditor sees the calculation lineage from source document to reported total, with no black-box intermediation.

- Population completeness testing: The platform cross-references facility lists, utility accounts, and asset logs against procurement and expense data. Gaps are flagged before fieldwork begins.

- Disclosure mapping: The platform exports SB 253-compliant filing templates with embedded evidence packs. Each line item in the filing traces to its supporting documentation.

- Version-controlled calculations: Emission factors, GWP values, and calculation methodologies are time-stamped and version-controlled. The auditor can reproduce every number in the filing.

Emission3 customers who used the platform for their 2026 filings negotiated fixed-fee assurance engagements 25-35% below market rates, because auditors priced for verification procedures only, not documentation builds [8].

If you are preparing an SB 253 filing and need to control 2027 audit scope, book a CBAM readiness call. We map your facility population, identify documentation gaps, and build the evidence lineage in parallel with your 2026 filing. The call is a scoping conversation, not a sales pitch.

The 2026 Window Is Closing

CARB's enforcement discretion on limited assurance expires after the first reporting cycle. Entities that submit 2026 filings without audit-ready documentation will face retrospective evidence builds in 2027, and the cost premium is unforgiving. The 90-day window between fiscal year-end and the August 10, 2026 deadline is the binding constraint.

CFOs who negotiate fixed-fee assurance engagements now, while auditors are still pricing based on preparation readiness, will control scope and cost. Those who wait will pay hourly rates for documentation builds and scope creep.

The arithmetic is clear. The deadline is fixed. The question is whether your finance team treats 2026 as regulatory relief or as the documentation pilot for 2027 assurance.

Book a CBAM readiness call to map your evidence lineage gaps and build audit-ready documentation in parallel with your 2026 filing. All customers start with a readiness conversation—we map suppliers, gaps, and implementation, no anonymous self-serve onboarding.

References & Sources

External Sources

- [1]Navigating California's Climate Disclosure Laws: Your Complete Guide to SB 253 and SB 261

Nelson Mullins comprehensive guide to SB 253 and SB 261 implementation, including reporting deadlines, fee structures, and CARB guidance updates.

- [2]SB 253 Compliance and Assurance: How California's climate disclosure bill creates business value

ERM analysis of CARB's enforcement discretion for first-year reporting and the strategic implications of the 2026 assurance waiver.

- [3]Sustainability Spotlight — California Climate Legislation Update — Status of CARB Rulemaking and Next Steps

Deloitte DART analysis of CARB rulemaking status, assurance requirements, and the November 2025 workshop guidance on enforcement discretion limits.

- [4]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

Emission3 explainer on climate audit terminology, audit fee re-pricing dynamics, and worked examples of Scope 1 emissions calculations.

- [5]California climate reporting–SB 253 and SB 261 explained

PwC Viewpoint guide to SB 253 and SB 261 compliance, including revenue definitions, reporting periods, and the public docket timeline.

- [6]SB 253 – Key Requirements for businesses in 2026

Sweep overview of SB 253 requirements, comparison to SB 261, and alignment with international frameworks including GHG Protocol and CSRD.

- [7]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law Now That CARB Has Finalized the Rules

Terrascope compliance roadmap covering CARB's 2025 milestones, reporting templates, GHG Protocol references, and the February 2026 rulemaking timeline.

- [8]California Air Resources Board Approves Regulations Implementing Climate Disclosure Laws SB 253 and SB 261

Willkie Farr & Gallagher summary of CARB's February 26, 2026 final regulations, fee structure, and implications for first-year reporting entities.

Related Content

- [9]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation, no anonymous self-serve onboarding.

- [10]Audit-ready exports in Emission3

For auditors and CFOs, shows the evidence lineage artifact that links every emissions source to its supporting documentation.