The default-value penalty for non-EU steel exporters in CBAM filings

The default-value penalty for non-EU steel exporters in CBAM filings

Here's the issue: You ship steel to the EU, your importer files the CBAM declaration, and the tariff cost per tonne comes back 40% higher than the competitor quoting from the plant next door. Your emissions are comparable, your production route is the same, but the certificate charge is wildly different. The gap is not in the carbon intensity of your steel—it is in whether you documented it.

However, CBAM filings consist of two things: embedded emissions totals and installation-level data.

Embedded emissions totals on their own have no value. Installation-level data is what the EU importer is actually paying for—and what determines the certificate cost.

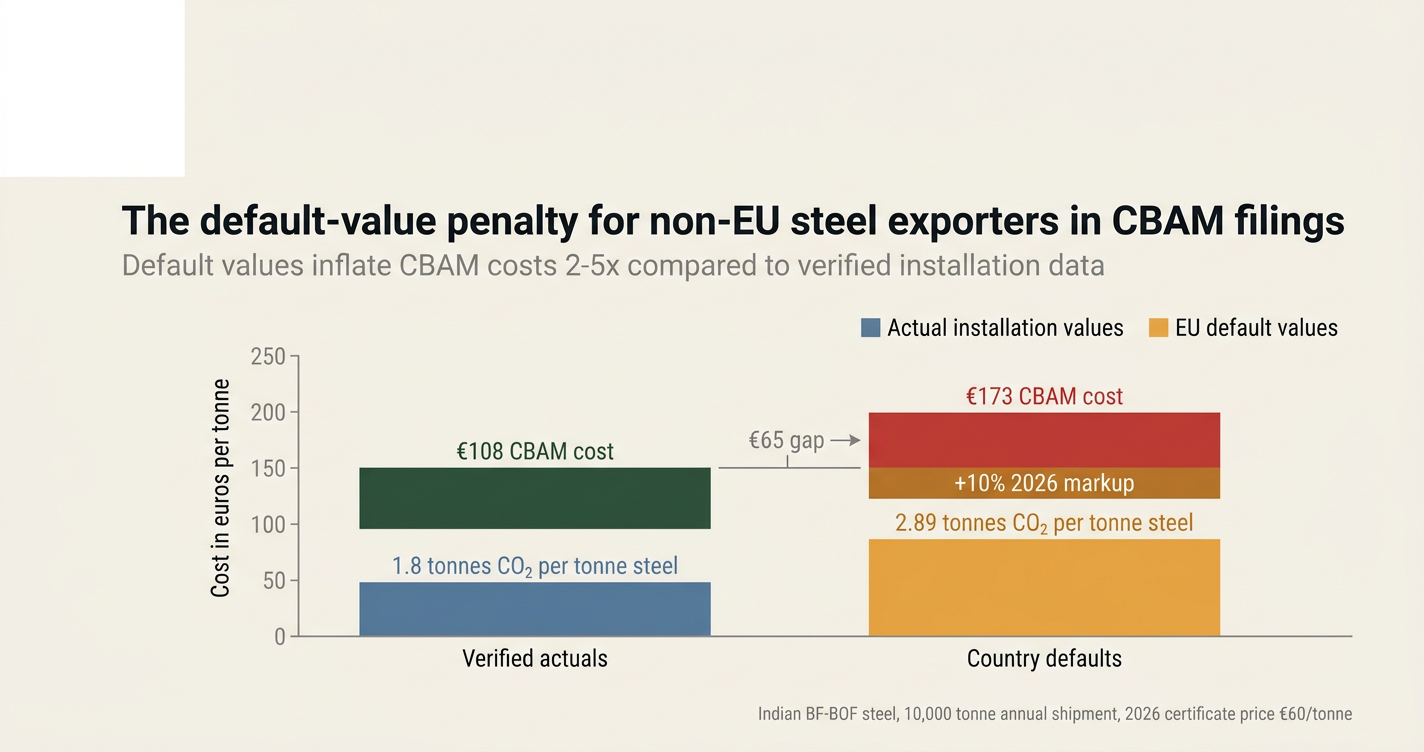

While calculating emissions totals has become cheaper (every consultant offers a carbon footprint), building installation-level data has become more expensive. If you rely on defaults instead of verified actuals, the cost of the default markup might outpace the savings of not documenting. For basic oxygen furnace steel from India, the default value is 2.89 tonnes CO₂ per tonne of steel, deliberately inflated to discourage use. If your actual installation emits 1.8 tonnes, the difference is a 61% tariff premium you are paying for documentation you did not build.

How do you solve this? I think the operators we work with who cut CBAM costs are the ones who stopped treating documentation as an admin task and started treating it as a tariff-reduction input. For now, the penalty for skipping installation-level data is a punitive default value—and the only way to avoid it is to document actual emissions with third-party verification before the 2027 declaration cycle.

The shape of the argument, visualised below.

The default-value vs actual-value decision

You have two options for CBAM declarations starting January 2026: submit verified installation-level data (actual values) or accept EU-assigned default values. The table below scores each option against five explicit criteria that determine your certificate cost, audit exposure, and long-term competitiveness in EU markets.

| Criterion | Actual installation values | EU default values |

|---|---|---|

| Certificate cost per tonne | Matches your real emissions (e.g. 1.8 t CO₂/t steel) | Country average + 10% markup in 2026, + 20% in 2027, + 30% from 2028[1] |

| Verification requirement | Mandatory third-party verification with on-site audit in 2026[2] | No verification needed, but no cost reduction either |

| Importer preference | EU buyers prefer suppliers with verified actuals to lower their CBAM liability[3] | Importers may push the default-value tariff cost back onto you |

| Data preparation timeline | 6-9 months to build monitoring plan, collect meter data, and schedule verifier site visit | Zero preparation, but zero cost control |

| Competitive positioning | Demonstrates operational efficiency and decarbonization readiness | Signals inability or unwillingness to document emissions |

| Regulatory trajectory | Default values rise annually; actual values lock in your real footprint | Penalty grows 10% annually, making defaults increasingly punitive[4] |

| Audit trail depth | Full lineage from meter readings to declared figures, registry-ready | No audit trail, no evidence, no rebuttal if disputed |

| Scope coverage | Direct + indirect emissions (electricity) from 2026[5] | Defaults cover direct only; indirect emissions revert to worst-case assumptions |

The five criteria that determine the verdict

1. Certificate cost per tonne shipped

This is the only number your CFO cares about. If your installation emits 1.8 tonnes CO₂ per tonne of steel, and the Indian default is 2.89 tonnes, you are paying for an extra 1.09 tonnes of emissions you did not produce. At €60 per CBAM certificate (2026 estimate), that is a €65 penalty per tonne of steel. On a 10,000-tonne annual shipment, you are leaving €650,000 on the table by not documenting actual data[1].

The default values published in December 2025 are deliberately conservative. For Turkish electric arc furnace steel, the default is 1.02 tonnes CO₂ per tonne of product—but efficient installations in the same country emit as low as 0.6 tonnes. The 42% gap is not production variance, it is the documentation penalty[6].

2. Importer pressure and cost pass-through

EU importers can file CBAM declarations with either actuals or defaults, but they cannot absorb the cost difference indefinitely. The importers we work with are already writing supplier terms that shift the default-value penalty back onto the exporter. If you ship 5,000 tonnes of aluminium to Germany and rely on defaults, the importer may reduce the purchase price by the differential between your default and a competitor's verified actual. This is not hypothetical—it is already happening in Turkish and Indian steel contracts for 2026 deliveries[7].

From the importer's perspective, paying for your defaults is paying for your decision not to document. They will pass that decision back to you in the form of a price cut or a supplier switch.

3. Verification timeline and infrastructure readiness

Verification is mandatory for actual values. The first official verification cycle covers the full 2026 calendar year, with on-site audits required at every installation[2]. This is not a desktop review—the verifier will inspect meter calibration certificates, production records, fuel delivery documentation, and energy purchase invoices. If your CMMS or ERP does not track this data at installation level, you cannot pass verification[5].

The verification bottleneck is not emissions calculation—it is evidence availability. Verifiers need a clear audit trail from raw measurement (gas meter, electricity invoice) to reported figure (tonnes CO₂ per tonne of product). If that trail does not exist, you default. If it exists but is incomplete, you default. The only way to avoid defaulting is to build the trail in 2026, before the 2027 declaration window opens[8].

4. The annual markup escalation on defaults

Default values rise by 10% in 2026, 20% in 2027, and 30% from 2028 onwards[4]. This is not inflation adjustment—it is a punitive escalator designed to make defaults economically unviable. If your baseline default is 2.5 tonnes CO₂ per tonne of cement in 2026, it becomes 2.75 in 2027 and 3.25 in 2028. Your actual emissions did not change, but your CBAM cost increased 30% because you did not document.

The escalator is asymmetric: actual values are locked to your real footprint and can only improve if you decarbonize. Defaults are locked to a penalty schedule and can only get worse. The longer you wait to document, the wider the gap.

5. Competitive signal to EU buyers

EU importers view verified actual values as a signal of operational maturity. If you can produce a verification report for 2026, you are demonstrating that your installation has metering infrastructure, data systems, and process controls robust enough to pass third-party audit. That signal matters when EU buyers are comparing two suppliers at similar price and quality—one with verified actuals, one relying on defaults.

The operators we work with who maintained EU contracts through 2026 are the ones who treated CBAM documentation as a sales input, not a compliance burden. The ones who lost volume to European producers are the ones who assumed defaults were "good enough."[3]

The verdict: actual values if you can build the audit trail in 2026

If you have 6-9 months to build a monitoring plan, install or calibrate meters, and coordinate a verifier site visit, actual values will cut your CBAM cost by 30-60% compared to defaults. If you cannot build that infrastructure by Q4 2026, you will default for the 2027 declaration cycle—and the penalty will grow 10% annually from there.

The decision is not whether to document emissions. The decision is whether to document them before the first verification cycle closes, or accept a permanent tariff premium that compounds every year.

"To use actual values, EU importers depend entirely on data from non-EU installation operators. For imports in 2026, the full calendar year of 2026 needs to be covered. These producers must collect data according to a monitoring plan, report this data to accredited verifiers and obtain a compliant verification report."[2]

The importers who absorb the default-value penalty in 2026 will not absorb it in 2027. They will switch suppliers, renegotiate contracts, or pass the cost back to you. The choice is not between documenting and not documenting—it is between documenting now and losing margin later.

How Emission3 fits

Emission3 is positioned as productized CBAM implementation backed by compliance infrastructure. We do not sell carbon accounting software. We build the installation-level audit trail that verifiers require, using the documents you already have: utility bills, fuel delivery records, production logs, and invoices.

The installation-level data flow works like this:

- Document ingestion: You upload utility bills, meter readings, and production records. Our system extracts line-item evidence (kWh consumed, gas delivered, tonnage produced) and links each data point to a source document.

- Deterministic calculation: We calculate embedded emissions using the CBAM methodology specified in Implementing Regulation 2025/2547. Every number is reproducible, with full lineage from source document to declared figure.

- Verification-ready output: We generate the evidence pack that verifiers need: meter calibration certificates, production allocation tables, and a full calculation audit trail. The output is formatted for the electronic template the Commission will release in Q1 2027[2].

The difference between Emission3 and a generic carbon platform is that we do not ask you to manually enter data into forms. We extract it from documents you already produce, build the calculation lineage, and hand verifiers a complete audit trail. The verification bottleneck is not emissions math—it is evidence availability. We solve for evidence[5].

If your installation ships more than 2,000 tonnes of steel, aluminium, or cement to the EU annually, and you want to avoid the default-value penalty, the work starts in Q1 2026. Book a CBAM readiness call to map your supplier data gaps, meter infrastructure, and verification timeline[8].

Next steps: build the audit trail before Q4 2026

The 2027 CBAM declaration cycle opens in Q1 2027. Verification reports for 2026 can be issued starting January 2027, but the site visit and data collection must happen during 2026[2]. If you wait until Q4 2026 to start building the audit trail, you will not have time to schedule the verifier, collect 12 months of meter data, or produce the monitoring plan. You will default.

The operators we work with who cut CBAM costs are the ones who started documentation in Q1 2026, not Q4. They treated the verification site visit as a fixed deadline and worked backward. If you are shipping to the EU in 2027, the default-value penalty is optional. The audit trail is not.

Book a CBAM readiness call to map your installation-level data gaps, meter infrastructure, and verification timeline. We will walk through your current documentation, identify what verifiers will ask for, and build the implementation plan that gets you to verified actuals before the 2027 declaration window opens. No anonymous self-serve onboarding—every customer starts with a readiness conversation[8].

References & Sources

External Sources

- [1]CBAM reporting requirements & Compliance Guide for 2026

The Commission has published provisional default values for all major countries that export to the EU, deliberately kept very high to encourage importers and exporters to use actual emission values.

- [2]EU CBAM Emissions Data: Monitoring, Reporting & Verification

For imports in 2026, the full calendar year of 2026 needs to be covered. Producers must collect data according to a monitoring plan, report this data to accredited verifiers and obtain a compliant verification report. Verification reports for 2026 can be issued in an electronic EU template from January 2027 via the CBAM Registry.

- [3]CBAM | Your Guide to the EU Carbon Border Adjustment Mechanism

From 2026, relying on defaults instead of verified actuals will significantly increase your CBAM cost exposure. The Commission revised default benchmarks downward in late 2025, which actually raises CBAM exposure for most products.

- [4]EU CBAM enters compliance phase and outlines path ahead

Most of the newly established default values will rise by 10% in 2026, 20% in 2027, and 30% from 2028 onwards. This top-up is intended to discourage reliance on default values and incentivize importers to report with actual emission values.

- [5]EU CBAM for Steel Exports: Track Embedded Carbon & Ensure Compliance

From January 2026, embedded carbon data submitted for CBAM must be third-party verified by an EU-accredited verifier. Verifiers require meter calibration certificates, production records, fuel delivery documentation, and a clear audit trail from raw measurement to reported figure.

- [6]A Guide to the EU CBAM

A physical site visit of the non-EU installation is mandatory starting in 2026. Aligning internal data systems with CBAM methodologies and coordinating third-party verification can reduce the risk of disruption and avoid reliance on punitive default values.

- [7]CBAM Verification: Carbon Border Adjustment Mechanism

The default values are intentionally conservative and can significantly increase CBAM costs. If your production processes are less carbon-intensive, using verified actual emissions data can substantially lower EU importers CBAM liability.

Related Content

- [8]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation. No anonymous self-serve onboarding.

- [9]How Emission3 handles CBAM

Specific to CBAM exporters, shows the installation-data flow from document ingestion to verification-ready output.