The methodology documentation gap in ESRS E1 Scope 3 disclosures

The methodology documentation gap in ESRS E1 Scope 3 disclosures

Here's the issue: ESRS E1 requires comprehensive Scope 3 emissions disclosure for all material categories, but the standard's emphasis on GHG Protocol alignment creates a verification problem that most sustainability teams have not yet encountered. The gap costs 40-60 hours per category during the assurance transition from limited to reasonable, as auditors demand full lineage for every emission factor, calculation method, and data source decision. What looks like a straightforward emissions total becomes a documentation archaeology exercise when the verifier asks, "Why this factor and not that one?"

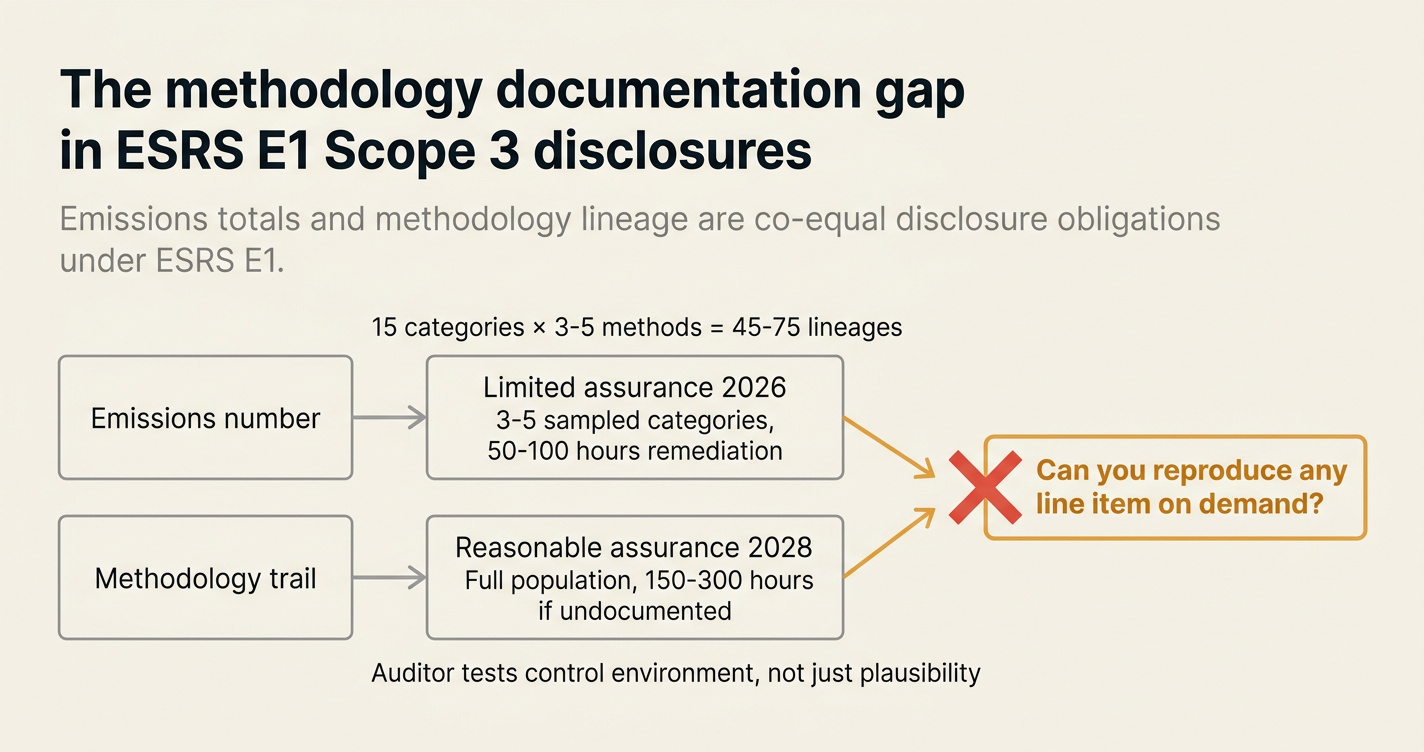

However, ESRS E1 Scope 3 disclosure consists of two things: the emissions number itself and the methodology trail that produced it.

The emissions number on its own has no regulatory value. The methodology trail is what the auditor is actually verifying—and what reasonable assurance from 2028 will explicitly price for. Without full documentation of factor selection rationale, boundary decisions, and data quality tiering, the inventory cannot survive a scenario analysis or a year-on-year consistency check. The number is a summary; the trail is the asset.

While emissions calculation has become cheaper through software, methodology documentation has become more expensive. If a multinational reports 15 Scope 3 categories under ESRS E1, and each category relies on 3-5 distinct calculation approaches, the documentation burden might reach 45-75 discrete methodology lineages. At 2-3 hours per lineage during the first assurance cycle, the undocumented inventory costs 90-225 hours of remediation before the auditor can even begin substantive testing. The emissions number was always the output; the methodology trail was always the work.

How do you solve this? I think the operators we work with who successfully transition from limited to reasonable assurance share one practice: they treat every factor selection as a documented decision point, not a calculation shortcut. For now, that means capturing why a GLEC Framework emission factor was chosen over an IEA factor, or why a spend-based estimate was used when supplier primary data was requested but not received. The documentation does not need to be elegant, but it does need to be contemporaneous and complete.

Visualised:

What ESRS E1 actually requires for Scope 3 methodology

ESRS E1, paragraph 46 states that undertakings must "refer to ESRS 1 paragraphs from 62 to 67" and "include the GHG emissions in accordance with the extent of the undertaking's operational control over them."[1] Paragraph 50 further requires disaggregation of scope 1 and 2 emissions, while Appendix A paragraph AR 46 explicitly directs companies to "consider the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (Version 2011)" and to "screen its total scope 3 GHG emissions based on the 15 scope 3 categories."[2]

The standard does not merely ask for the total. It requires:

- Emission factors and their sources: ESRS E1 mandates disclosure of "the methodologies, emission factors, and data sources used."[3] This is not optional metadata; it is a primary disclosure requirement.

- Category-by-category breakdown: The GHG Protocol Scope 3 Standard requires reporting by category, and ESRS E1 adopts this structure without modification.[4]

- Justification for exclusions: While ESRS E1 allows materiality-based exclusions (unlike the GHG Protocol, which requires all categories with disclosed justification), auditors still expect documentation of the materiality assessment itself.[2]

- Consistency over time: ESRS 1 requires methodology consistency across reporting periods. Any change in calculation approach, boundary, or factor set must be disclosed and explained.[1]

The regulatory text is unambiguous: the number and the methodology are co-equal disclosure obligations.

The three gaps auditors surface during ESRS E1 Scope 3 verification

| Gap | What it looks like | Why it fails assurance | Remediation cost |

|---|---|---|---|

| Factor selection rationale | Spreadsheet uses DEFRA factors for freight, GLEC factors for fuel, and supplier-specific factors for purchased goods—no documented reason why each was chosen. | Auditor cannot verify whether factors are fit-for-purpose or consistently applied. No way to reproduce the calculation in a future period. | 15-25 hours per category to reconstruct decision logic from emails, reconstruct factor libraries, and draft retrospective methodology notes. |

| Data quality tiering | Inventory combines primary supplier data, industry averages, and spend-based estimates in a single category total—no record of which line items used which approach. | Auditor cannot assess whether the mix of data sources is reasonable or whether high-quality data was prioritised. No way to trend data quality improvement over time. | 20-30 hours per category to re-map each line item to its source, assign quality tiers, and document substitution rules for missing data. |

| Boundary and completeness | Scope 3 Category 1 (Purchased Goods and Services) excludes office supplies and IT services because "they're immaterial"—no quantified threshold or screening analysis on file. | Auditor cannot verify that the boundary is consistent with ESRS 1 materiality guidance or that excluded items were actually tested for significance. | 10-15 hours per category to perform retrospective screening, document the materiality threshold, and recalculate any material categories that were excluded. |

These gaps do not indicate bad faith. They indicate a workflow that was designed for calculation, not verification. The sustainability team produced the number; the auditor is asking for the architecture.

"The majority of logistics-related Scope 3 GHG emissions in the GHG Protocol categories Upstream Transportation and Distribution... rely almost exclusively on primary data captured via our financial reporting system to calculate both Scope 1 and Scope 2 GHG emissions as well as Scope 3 emissions in the category Fuel and Energy-Related Activities."[5]

DHL's 2025 ESRS E1 disclosure illustrates the standard: every emission source is tied to a named data system, every category is tied to a named calculation approach (GLEC Framework 3.1, IEA emission factors 2024). The disclosure does not stop at the number. It documents the trail.

The cost structure of undocumented methodology under reasonable assurance

The CSRD assurance timeline is fixed: limited assurance in 2026, reasonable assurance from 2028. Most in-scope companies are entering their first limited assurance cycle now. The problem is that limited assurance tests the plausibility of the disclosure, not the completeness of the underlying control environment. Reasonable assurance tests the control environment—and without methodology documentation, there is no control environment to test.

The cost differential is quantifiable:

- Limited assurance (2026-2027): Auditor samples 3-5 high-value Scope 3 categories, requests source documents for the sampled items, and issues a limited assurance opinion. If the documentation gap surfaces, the auditor notes it as a deficiency but does not necessarily block the opinion. Remediation cost: 50-100 hours across all categories, mostly deferred.

- Reasonable assurance (2028 onward): Auditor tests the entire population, requests full methodology lineage for every category, and verifies that the inventory control environment can reproduce the disclosure in future periods. If the documentation gap persists, the auditor cannot issue a reasonable assurance opinion without qualification. Remediation cost: 150-300 hours across all categories, non-deferrable, plus potential restatement of prior-year comparatives if the methodology is found to be inconsistent.

The gap does not shrink over time. It compounds, because each year's undocumented inventory becomes a liability for the next year's consistency verification.

What methodology documentation actually looks like in practice

For Category 1 (Purchased Goods and Services), a documented methodology lineage includes:

- Data source hierarchy: "We requested primary data from all suppliers with >€500k annual spend. For suppliers who provided data, we used reported emissions. For suppliers who did not respond, we used EXIOBASE industry-average factors matched to the supplier's sector code. For residual spend, we used spend-based factors from DEFRA 2024."

- Factor selection rationale: "We chose EXIOBASE over EEIO factors because our procurement system captures supplier country of origin, and EXIOBASE provides country-specific sectoral factors. EEIO is US-only and would require all non-US suppliers to be mapped to US equivalents, introducing error."

- Boundary documentation: "Category 1 includes all goods and services procured through the central ERP system (98.4% of total procurement spend by value). Excluded: employee reimbursements for business expenses (captured in Category 6, Business Travel) and capital goods (captured in Category 2). Materiality threshold: 1% of total procurement spend, tested annually."

- Quality tier assignment: "Of the €420m total Category 1 spend, €180m (42.9%) was calculated using supplier primary data, €160m (38.1%) using industry-average factors, and €80m (19.0%) using spend-based factors. Target for 2026: increase primary data coverage to 60%."

This is not a paragraph in the ESRS E1 disclosure. It is a methodology note in the internal control file that the disclosure references. The auditor verifies the note, not the disclosure.

Why the gap persists even in well-resourced sustainability teams

The methodology documentation gap is not a resource problem. It is a workflow problem. Most sustainability teams build their Scope 3 inventory in spreadsheets, using a calculation-first workflow:

- Collect data (supplier responses, invoices, spend reports).

- Apply emission factors (from a library, a database, or a consultant's model).

- Sum the results by category.

- Export the totals to the disclosure template.

The methodology decisions happen in step 2, but they are not recorded in step 2. The factor library is maintained separately (often by a consultant or a software vendor). The rationale for choosing one factor over another is implicit ("it was the default in the tool") or undocumented ("we discussed it on a call"). The boundary and quality tier decisions happen in step 1, but they are not formalised until the auditor asks for them in step 4.

The workflow was designed for reporting, not verification. The gap opens the moment the auditor asks, "Can you show me how this number was calculated?" and the team realises the answer is distributed across six people's email inboxes and three generations of spreadsheet versions.

The infrastructure ESRS E1 reasonable assurance actually requires

Reasonable assurance assumes an inventory control environment that can:

- Reproduce any line item on demand: If the auditor samples a €50k supplier emission entry, the system must be able to surface the source data (invoice, supplier response), the calculation method (factor, formula), and the decision rationale (why this factor, why this boundary) in a single audit trail.

- Document factor version and provenance: If the inventory uses DEFRA 2024 factors in year 1 and DEFRA 2025 factors in year 2, the system must record the version change and flag any line items where the factor changed materially.

- Track data quality over time: If the target is to increase primary data coverage from 40% to 60%, the system must be able to report current coverage by category, by supplier, and by spend tier, not just as a one-time snapshot.

- Support scenario analysis: If the company models a decarbonisation pathway that assumes 30% supplier engagement by 2026, the system must be able to rerun the inventory under the assumption that 30% of spend-based factors are replaced by primary data, and show the impact on the total.

This is not a spreadsheet. It is a data lineage and control system. The gap is the distance between a calculation tool and a verification-ready control environment.

How Emission3 fits

Emission3 is built for the ESRS E1 reasonable assurance transition. Every Scope 3 line item is calculated with full lineage: the source document (invoice, BoM, supplier response), the emission factor and its version, the quality tier, and the decision rationale. The system exports evidence packs for auditors, not just summary totals for disclosure templates.

For Category 1 (Purchased Goods and Services):

- Primary data collection: Supplier engagement workflows track request status, parse responses, validate incoming data against GHG Protocol Scope 3 calculation rules, and flag outliers for review. The system does not assume all suppliers will respond; it documents who responded, who did not, and what fallback method was used for non-respondents.

- Factor selection audit trail: If the system applies an EXIOBASE factor to a supplier, the lineage includes the factor version, the sector mapping logic, and the decision rule that selected EXIOBASE over DEFRA or EEIO. The auditor does not need to ask why; the trail is already attached to the line item.

- Data quality tiering: Every line item is tagged as primary, secondary, or tertiary data. The disclosure includes a quality breakdown by spend value, by category, and by supplier. The system tracks the trend over time and flags any categories where data quality is declining.

The methodology documentation is not a retrospective remediation task. It is built into the calculation workflow. The gap closes because the tool was designed for reasonable assurance from the start.

What to do now

If you are entering your first ESRS E1 limited assurance cycle in 2026, and your Scope 3 inventory is calculated in spreadsheets, the methodology documentation gap will surface during the audit. The remediation cost is 50-100 hours now, or 150-300 hours in 2028 when reasonable assurance begins.

Start by documenting your factor selection rationale for your three highest-spend Scope 3 categories. Write a one-page methodology note for each category that answers:

- What data sources did you use? (Primary, secondary, spend-based?)

- What emission factors did you use, and why those factors? (Version, provenance, selection logic?)

- What is your boundary, and how did you test for completeness? (Materiality threshold, screening analysis?)

- What is your data quality by spend tier? (% primary, % secondary, % tertiary?)

If you cannot answer these questions from memory, you cannot reproduce the calculation under audit. The gap is not the number. The gap is the trail.

Book a CBAM readiness call with Emission3. We will map your current Scope 3 inventory, identify the methodology gaps that will surface under reasonable assurance, and show you what a verification-ready control environment looks like. All customers start with a readiness call—we do not offer anonymous self-serve onboarding because the workflow starts with understanding your current state, not selling you a tool.[6]

References & Sources

External Sources

- [1]ESRS E1 - Climate Change (Draft November 2025)

EFRAG's draft ESRS E1 standard, detailing disclosure requirements for Scope 1, 2, and 3 emissions, methodology consistency under ESRS 1, and GHG Protocol alignment.

- [2]Overview of GHG Protocol Integration in Mandatory Climate Disclosure

GHG Protocol's official comparison of how ESRS E1 integrates the Scope 3 Standard, including category-by-category reporting and exclusion disclosure requirements.

- [3]The GHG Protocol Explained: A Complete Guide to Corporate Emissions Reporting

Comprehensive guide to GHG Protocol methodology under CSRD, including ESRS E1 disclosure requirements for emission factors, data sources, and methodologies.

- [4]Greenhouse Gas Protocol

World Resources Institute's official Greenhouse Gas Protocol page, explaining the Corporate Value Chain (Scope 3) Standard and its 15 category structure.

- [5]Environment (ESRS E1) | Q4 2025 - DHL Reporting Hub

DHL's 2025 ESRS E1 disclosure, demonstrating full methodology documentation for Scope 1, 2, and 3 emissions, including factor sources and data system lineage.

Related Content

- [6]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, gaps, and implementation. No anonymous self-serve onboarding.

- [7]Scope 3 with primary data

Emission3's Scope 3 solution for supply-chain leaders and sustainability managers, with full methodology lineage and evidence packs for auditors.

- [8]The methodology documentation gap in Scope 3 Category 1 primary data collection

Primary data collection consists of two things: supplier emissions and methodology lineage. Auditors verify the second—and most procurement teams lack it.