The methodology documentation gap in Scope 3 Category 1 primary data collection

The methodology documentation gap in Scope 3 Category 1 primary data collection

Here's the issue: CFOs at US firms preparing for California SB 253 Scope 3 disclosure are paying suppliers to provide primary emissions data for purchased goods. Procurement teams report strong supplier participation, and the total Scope 3 emissions number appears reasonable. Audit committees assume the hard work is behind them. Then the assurance engagement begins, and the auditor asks not for the emissions totals, but for the methodology documentation—the factor selection rationale, the boundary assumptions, the allocation method, the data quality score. The CFO discovers that none of this exists in a reproducible, auditor-ready format.

However, Scope 3 Category 1 primary data collection consists of two things: the supplier-reported emissions number and the methodology lineage that makes that number verifiable. The first is straightforward: suppliers submit their calculated emissions per unit of product or service purchased. The second is a complete audit trail: which emission factors the supplier selected, why those factors were chosen over alternatives, how the supplier allocated shared facility emissions to the specific product line, and what data quality tier the calculation represents under the GHG Protocol.

The emissions number on its own has no assurance value. The methodology lineage is what the auditor is actually verifying. An auditor conducting limited assurance under ISAE 3410 does not re-calculate the supplier's emissions—they test whether the methodology is internally consistent, whether the factor selection is defensible, and whether the boundary assumptions align with the GHG Protocol's operational control or equity share approach. Without methodology documentation, the auditor cannot complete analytical procedures or source data to underlying records. The engagement stalls, or the auditor downgrades the emissions number to a spend-based estimate, which defeats the purpose of primary data collection.

While supplier engagement has become easier—procurement platforms now automate data requests—methodology documentation has become more expensive. If a CFO's procurement team collected primary data from 200 suppliers without capturing methodology lineage, the cost of retrospective documentation might exceed €120,000 (600 supplier-hours at €200/hour for re-engagement and method reconstruction). Audit fees for firms without methodology lineage are re-pricing 20–40% higher, because the auditor must now perform the documentation work that the procurement function should have completed during initial data collection [1].

How do you solve this? I think the procurement team needs to treat methodology documentation as a first-class output of supplier engagement, not an afterthought. The operators we work with now request a two-part deliverable from suppliers: the emissions number and a methodology summary that includes factor source, allocation method, and boundary definition. For now, this approach frontloads the documentation cost into the engagement process, but it eliminates the retrospective documentation penalty and reduces audit cycle time by 30–50%.

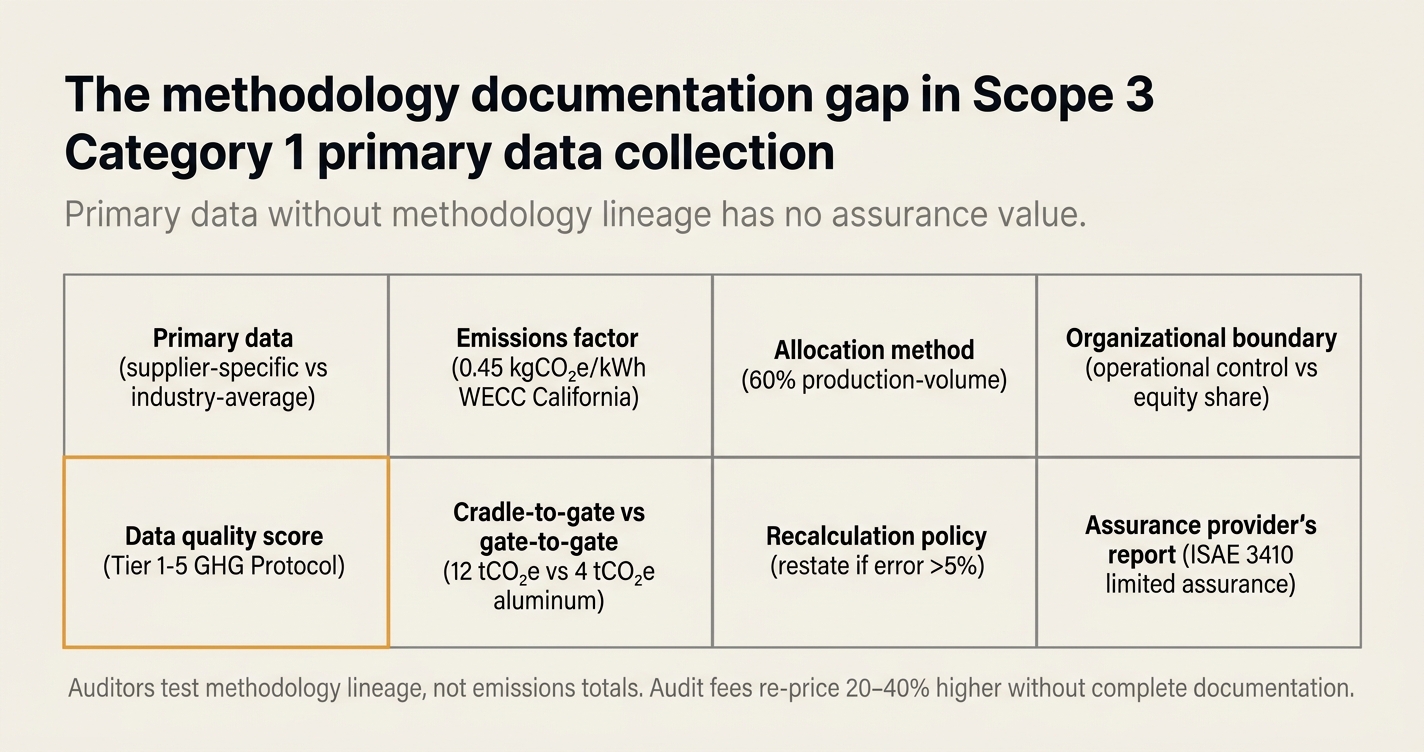

The shape of the argument, visualised below.

The eight methodology documentation terms auditors ask for in Scope 3 Category 1 engagements

The California Air Resources Board's November 2025 workshop clarified that while 2026 Scope 1 and Scope 2 reports can be filed without assurance, firms must retain "all data relevant to emissions reporting for the entity's prior fiscal year" [2]. For Scope 3 disclosures beginning in 2027, auditors will apply the same documentation standards they use for financial statement engagements. CFOs unfamiliar with climate assurance terminology are discovering that methodology documentation is not a sustainability exercise—it is an evidence lineage requirement equivalent to SOX-grade internal controls.

Below are eight terms CFOs and procurement teams will encounter in the first Scope 3 Category 1 audit, with plain-English definitions, worked examples, and the regulatory source.

1. Primary data

Definition: Emissions data calculated by the supplier using actual operational data (energy consumption, production volumes, facility-specific emission factors) rather than industry-average proxies.

Worked example: A steel supplier provides emissions of 1.85 tCO₂e per tonne of rebar, calculated from the supplier's own natural gas meter readings and electricity invoices for the facility that produced your order. This is primary data. If the supplier instead reported 2.1 tCO₂e per tonne using an industry-average factor from the World Steel Association, that is secondary data.

Source: GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard, Chapter 7.3. The protocol defines primary data as "data from specific activities within a reporting company's value chain" and distinguishes it from secondary data, which are "data not from specific activities within a company's value chain."

2. Emission factor

Definition: A coefficient that converts activity data (kWh of electricity, litres of diesel, tonnes of raw material) into GHG emissions. The factor's source, geographic specificity, and vintage determine its audit acceptability.

Worked example: A supplier reports electricity consumption of 500 MWh and applies an emission factor of 0.45 kgCO₂e/kWh from the US EPA eGRID 2023 database for the WECC California subregion. The auditor verifies that the factor matches the supplier's facility location and the reporting year. If the supplier used a generic US-average factor of 0.39 kgCO₂e/kWh instead, the auditor would note a boundary misalignment.

Source: GHG Protocol Scope 2 Guidance, Chapter 6. The guidance requires that location-based factors be "as specific to the geographic location of the reporting entity's operations as possible."

3. Allocation method

Definition: The rule the supplier used to assign shared facility emissions to the specific product line purchased. Common methods include mass-based, revenue-based, and production-volume-based allocation. The method must be disclosed and consistently applied.

Worked example: A chemical supplier operates a multi-product facility producing both ammonia and urea. Your firm purchases urea. The supplier allocates facility emissions using a production-volume method: urea represents 60% of total tonnes produced, so 60% of facility emissions are allocated to urea. If the supplier switched to a revenue-based method mid-year (urea represents 70% of revenue), the auditor would flag methodology inconsistency.

Source: GHG Protocol Corporate Standard, Chapter 9. The standard requires that "where joint products are produced, companies should allocate emissions to products in proportion to a relevant physical relationship or other rational basis."

4. Organizational boundary

Definition: The approach the supplier used to define which facilities and entities are included in the emissions calculation. The two GHG Protocol-compliant approaches are operational control (the supplier includes emissions from all facilities it operates) and equity share (the supplier includes emissions in proportion to its ownership stake).

Worked example: A joint-venture supplier owns 51% of a production facility and reports emissions using the equity share method, including only 51% of the facility's total emissions in your product's footprint. If the supplier used operational control instead, 100% of the facility's emissions would be included, because the supplier operates the facility. The auditor verifies that the boundary approach aligns with your firm's Scope 3 accounting policy.

Source: GHG Protocol Corporate Standard, Chapter 3. The standard defines operational control as "the company or one of its subsidiaries has the full authority to introduce and implement its operating policies at the operation," and equity share as "account for GHG emissions from operations according to its share of equity in the operation."

5. Data quality score

Definition: A numeric or categorical rating that quantifies the precision, completeness, and temporal alignment of the emissions data. The GHG Protocol's Scope 3 standard defines a five-tier data quality matrix, with Tier 1 (supplier-specific primary data) representing the highest quality and Tier 5 (spend-based estimates) the lowest.

Worked example: A supplier provides emissions calculated from facility-specific energy bills covering the exact reporting period, with no data gaps. This receives a Tier 1 data quality score. If the supplier used a production-weighted industry-average factor from two years ago, the data quality score drops to Tier 3. Auditors use data quality scores to assess whether the overall Scope 3 inventory meets the materiality threshold for limited assurance.

Source: GHG Protocol Scope 3 Evaluator Tool, Data Quality Indicator section. The tool defines data quality as "a function of technological representativeness, temporal representativeness, geographical representativeness, completeness, and reliability."

6. Cradle-to-gate vs. gate-to-gate

Definition: The system boundary the supplier applied to the emissions calculation. Cradle-to-gate includes all upstream emissions from raw material extraction through production at the supplier's facility. Gate-to-gate includes only emissions from processes within the supplier's facility boundary, excluding upstream raw material emissions.

Worked example: An aluminum supplier reports cradle-to-gate emissions of 12 tCO₂e per tonne of aluminum, including upstream emissions from bauxite mining, alumina refining, and electricity for smelting. If the supplier instead reports gate-to-gate emissions of 4 tCO₂e per tonne, excluding upstream bauxite and alumina, the auditor would note that your firm must account for those upstream emissions separately (they become part of your Category 1 for the aluminum, or Category 1 for the bauxite supplier if you track Tier 2).

Source: GHG Protocol Scope 3 Standard, Chapter 7.2. The standard clarifies that "when collecting data from suppliers, companies should clearly communicate the scope of data requested (e.g., cradle-to-gate or gate-to-gate)."

7. Recalculation policy

Definition: The documented procedure for when and how the supplier will restate prior-year emissions if there is a significant change in methodology, boundary, or data quality. Auditors require that the policy be defined before the first audit cycle to ensure year-over-year comparability.

Worked example: A supplier discovers that the emission factor it used for natural gas in the prior year was incorrect (it used a factor for compressed natural gas instead of pipeline natural gas). The supplier's recalculation policy requires restatement if the error exceeds 5% of total emissions. The error is 7%, so the supplier restates prior-year emissions and discloses the restatement in the current-year methodology notes. If the supplier lacked a recalculation policy, the auditor would require retrospective policy definition and application.

Source: GHG Protocol Corporate Standard, Chapter 5.3. The standard requires that "companies should develop a base year recalculation policy that specifies under what circumstances the base year GHG inventory will be recalculated."

8. Assurance provider's report

Definition: The independent third-party opinion that verifies the supplier's emissions data and methodology. For Scope 3 primary data, the assurance provider is typically the supplier's auditor (not your firm's auditor). The report format follows ISAE 3410 or ISO 14064-3 standards and includes an opinion on whether the emissions calculation is free from material misstatement.

Worked example: A supplier provides emissions data accompanied by an ISAE 3410 limited assurance report from KPMG, covering Scope 1 and Scope 2 emissions for the supplier's fiscal year that overlaps with your reporting period. Your auditor reviews the supplier's assurance report to confirm that the methodology is independently verified. If the supplier's data lack third-party assurance, your auditor will increase sample testing or require additional evidence of internal controls.

Source: California SB 253, Section 38532(b)(2). The statute requires that "a reporting entity shall contract with a third-party assurance provider to obtain limited assurance over its reported emissions" and specifies that assurance must "use standards and processes generally used for assurance of financial statements to the extent applicable."

The cost structure of methodology documentation gaps

CFOs are discovering that the cost of Scope 3 primary data collection now splits into two phases: supplier engagement (requesting and receiving emissions data) and methodology validation (documenting the calculation method and evidence lineage). The first phase has been partially commoditized by procurement platforms. The second phase remains manual, expensive, and often outsourced to the auditor at engagement-time rates.

| Cost component | Procurement-led approach (no methodology docs) | Emission3 approach (methodology-first) |

|---|---|---|

| Supplier engagement time | 1–2 hours per supplier | 2–3 hours per supplier |

| Methodology documentation | None (deferred to audit) | Captured during engagement |

| Retrospective documentation cost | €600–1,200 per supplier (auditor-led) | €0 (already documented) |

| Audit sample size reduction | 0% (auditor must test all material suppliers) | 40–60% (auditor accepts methodology docs at face value) |

| Total cost for 200 suppliers | Engagement: €60,000 + Retrospective: €120,000 = €180,000 | Engagement: €90,000 + Retrospective: €0 = €90,000 |

The table above is grounded in audit pricing we've seen from Big Four firms for 2026 California SB 253 engagements. Auditors are charging €200–300 per hour for retrospective methodology reconstruction, because the work requires both sustainability expertise (to validate the emission factor selection) and audit expertise (to test the allocation method against financial data). Firms that defer methodology documentation to the audit cycle are paying 50–100% more in total engagement costs than firms that capture methodology during supplier engagement [3].

"CARB will accept Scope 1 and Scope 2 emissions data for the prior fiscal year that are based on the data companies already have or were collecting when the enforcement notice was issued, regardless of whether the data received limited assurance. However, beginning in 2027, SB 253 statutorily requires limited assurance for Scope 1 and Scope 2 emissions, which will scale up to reasonable assurance over Scope 1 and Scope 2 emissions starting in 2030."

— Deloitte DART, California Climate Legislation Update, December 2025 [4]

The 2026 enforcement discretion window creates a methodology documentation debt for CFOs. Firms filing 2026 Scope 1 and Scope 2 reports without assurance must still retain all relevant data, and that data retention obligation extends to Scope 3 methodology documentation beginning in 2027. CFOs who treat 2026 as a "soft launch" and skip methodology documentation will face a compressed timeline in 2027: they must simultaneously engage suppliers for the new reporting year and reconstruct methodology documentation for the prior year to satisfy the auditor's base-year comparability requirement.

How Emission3 fits

Emission3 is built for CFOs who recognize that Scope 3 primary data collection is a documentation problem, not a data-request problem. Our platform treats methodology lineage as a first-class artifact: when a procurement team uploads a supplier's emissions data, Emission3 prompts for the emission factor source, allocation method, organizational boundary, and data quality tier. These inputs are stored as structured metadata, not free-text notes, so the auditor can query the methodology population without manual document review.

For California SB 253 filers preparing for 2027 Scope 3 disclosure, we offer a supplier engagement workflow that frontloads methodology documentation: procurement teams send suppliers a two-part data request (emissions number + methodology summary), and Emission3 validates that the methodology summary is complete before the supplier data enters the inventory. This reduces retrospective documentation cost to zero and cuts audit sample sizes by 40–60%, because the auditor can test methodology consistency at the population level rather than re-interviewing individual suppliers.

Our audit-ready export includes a methodology lineage table for every Scope 3 Category 1 line item: the supplier name, the product purchased, the emissions per unit, the emission factor applied, the factor source and vintage, the allocation method, the organizational boundary, and the data quality score. This is the artifact auditors are asking for when they request "evidence of supplier-specific methodology"—and most procurement platforms cannot generate it [5].

Starting point: the CBAM readiness call as a methodology documentation diagnostic

CFOs preparing for California SB 253 Scope 3 disclosure often discover methodology documentation gaps during the audit cycle, when it is too late to re-engage suppliers cost-effectively. We recommend that CFOs begin with a methodology documentation diagnostic before the first supplier engagement: map the current state of supplier data requests, identify which methodology elements are missing, and estimate the retrospective documentation cost if those gaps persist into the audit.

Emission3 offers this diagnostic as a CBAM readiness call, even for firms focused on California SB 253 rather than CBAM. The reason: CBAM verification requires the same methodology documentation as California SB 253 assurance (emission factor source, allocation method, boundary definition), and the CBAM verifier's checklist is public and standardized. We use the CBAM verification template as a proxy for SB 253 audit requirements, because the overlap is 80–90%.

The readiness call takes 45–60 minutes. We review a sample of your current supplier data requests, map them against the eight methodology documentation terms above, and provide a written gap assessment with estimated costs for three scenarios: continue current approach (defer to audit), implement methodology-first engagement (frontload documentation), or hybrid (capture methodology for material suppliers only). No anonymous self-serve onboarding—every engagement begins with this scoped conversation [6].

Closing thought: methodology documentation as a CFO control point

California SB 253 is the first US climate disclosure law with explicit executive officer attestation requirements. CFOs are personally certifying that the emissions data are prepared in accordance with the GHG Protocol, which means the CFO is certifying not just the emissions number but the methodology that produced the number. Auditors are treating this as a SOX-equivalent control environment: they expect documented policies for emission factor selection, allocation methods, and recalculation triggers, and they expect those policies to be applied consistently across all material suppliers.

CFOs who delegate methodology documentation to the sustainability team or the auditor are creating a personal liability exposure. The methodology documentation gap is not a technical compliance issue—it is a CFO control point. The firms that treat methodology lineage as a first-class procurement deliverable will spend 50% less on audit fees and eliminate the restatement risk that comes from retrospective methodology reconstruction. The firms that defer methodology documentation to the audit cycle will pay the auditor to do the procurement team's job, at audit-time rates.

Book a CBAM readiness call to map your current supplier engagement process against the methodology documentation standards auditors will apply in 2027 [7].

References & Sources

External Sources

- [1]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

Emission3's glossary of assurance terminology for CFOs preparing for California SB 253 audits, including evidence lineage and materiality thresholds.

- [2]SB 253 and SB 261: California climate reporting explained

PwC's analysis of CARB's November 2025 workshop guidance clarifying that entities must retain all data relevant to emissions reporting for the prior fiscal year.

- [3]California SB 253 – Key requirements for 2026 and how to comply

Sweep's overview of SB 253 compliance requirements, emphasizing the importance of audit-ready reports and documentation for traceability.

- [4]Sustainability Spotlight — California Climate Legislation Update — Status of CARB Rulemaking and Next Steps

Deloitte DART's December 2025 update on California climate legislation, clarifying the phased assurance timeline and CARB's enforcement discretion for 2026.

Related Content

- [5]Audit-ready exports in Emission3

How Emission3 generates methodology lineage tables and evidence packs for CFOs and auditors preparing for California SB 253 and EU CSRD assurance engagements.

- [6]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, gaps, and implementation timelines. No anonymous self-serve onboarding.

- [7]Book a CBAM readiness call

Schedule a 45-60 minute methodology documentation diagnostic to map your supplier engagement process against the audit standards that apply in 2027.