The methodology drift problem in multi-year GHG Protocol inventories

The methodology drift problem in multi-year GHG Protocol inventories

Here's the issue: A sustainability manager completes their second-year GHG Protocol inventory, shows a 12% reduction in Scope 3 Category 1 emissions, and files the report. The reduction looks credible—procurement shifted spend toward lower-carbon suppliers, activity data improved, and the total decreased. At face value, the trend claim holds. But when the auditor arrives for limited assurance, the first question is not about the 12% reduction. It is about whether the methodology used to calculate year two is the same methodology used to calculate year one. If it is not, the trend claim is unverifiable, and the 12% figure becomes a compliance liability, not a performance metric.

However, a multi-year GHG inventory consists of two things: the emissions totals disclosed each year, and the methodology consistency that allows year-over-year comparison. The first is what the sustainability team tracks. The second is what the auditor verifies.

The emissions total on its own has no value for trend analysis. Methodology consistency is what the auditor is actually asking for, paying for, and verifying. A 12% reduction calculated with spend-based emission factors in year one and activity-based emission factors in year two is not a reduction—it is a methodology change. The GHG Protocol Corporate Standard requires recalculation of the base year when significant methodology improvements occur, but most sustainability teams lack the documentation to prove whether a change is a methodology shift, a data quality improvement, or an operational reduction. Without that evidence, the auditor cannot verify the trend, and the disclosed reduction becomes a qualified opinion risk.

While emissions measurement has become cheaper—carbon accounting platforms, supplier data APIs, automated activity data ingestion—methodology consistency assurance has become more expensive. If a sustainability team changes emission factors, updates boundary definitions, or refines allocation methods across reporting cycles without recalculating the base year and documenting the lineage, the cost of remediation during assurance might outpace the cost of the platform itself. Under CSRD ESRS E1, auditors expect full methodology lineage and base year recalculation documentation. A qualified opinion on trend claims can delay filing by 6-9 months and inflate assurance fees by 40-60%, per recent wave-one filer experience.

How do you solve this? I think the answer is not to lock methodology at the outset—teams should improve data quality over time—but to version the methodology explicitly, recalculate the base year when changes occur, and document the lineage from activity data to emission factor to total for every reporting period. The operators we work with now treat methodology as versioned code: every change triggers a base year recalculation, and the recalculation is stored as an auditable diff. For now, this approach is the only way to preserve trend claims under assurance scrutiny.

The shape of the argument, visualised below.

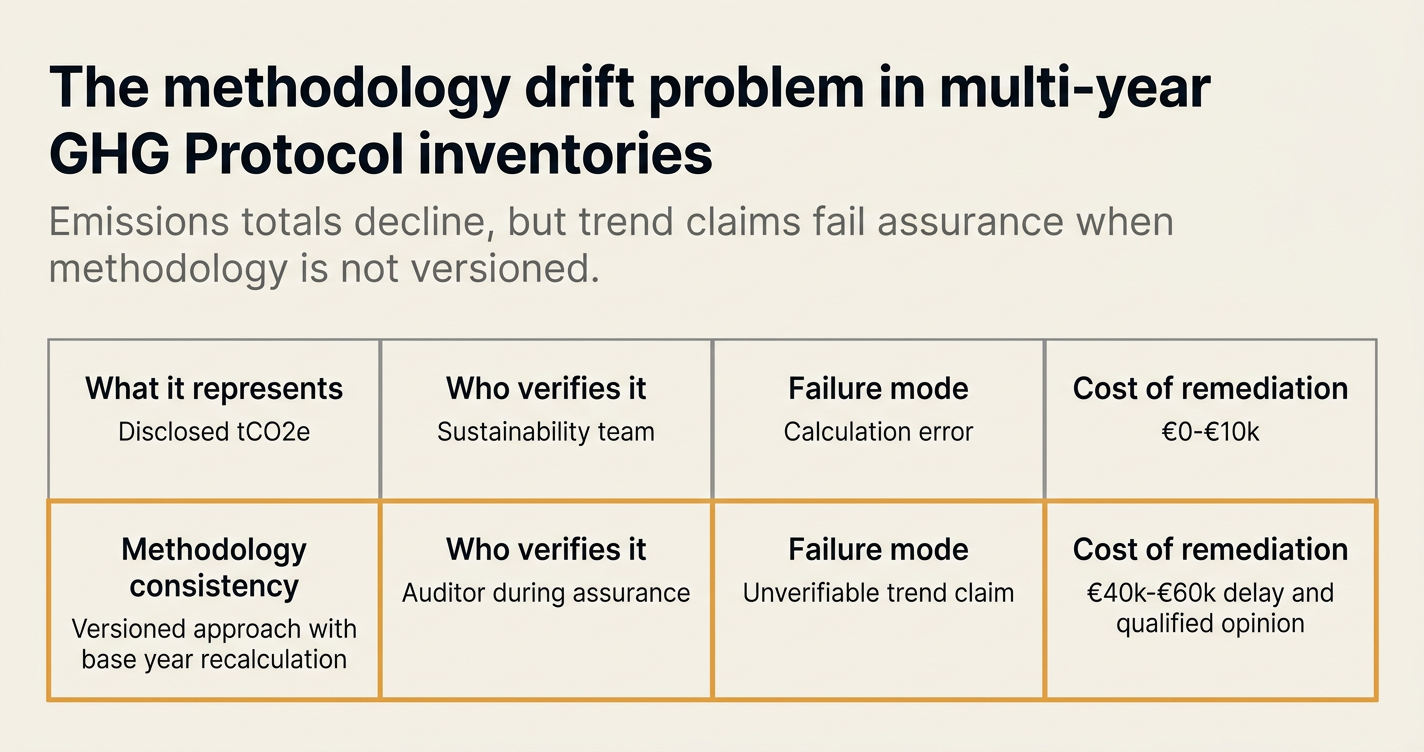

The two components of a multi-year GHG inventory

A GHG Protocol inventory disclosed across multiple years contains two analytically distinct components:

| Component | What it represents | Who verifies it | Failure mode |

|---|---|---|---|

| Emissions totals | The disclosed tCO2e figure for each scope and category, aggregated to a single number per year | The sustainability team, internal reviewers, external stakeholders | Total is wrong (calculation error, missing data, boundary error) |

| Methodology consistency | The extent to which the approach used to calculate year N is the same approach used to calculate year N-1, or documented as changed with base year recalculation | The auditor, during limited or reasonable assurance engagement | Trend claim is unverifiable (methodology drift, undocumented factor changes, no base year recalculation) |

The first component is relatively straightforward to produce. Most carbon accounting platforms can ingest activity data, apply emission factors, and generate a total. The second component is where most inventories fail under assurance.

Methodology consistency does not mean methodology stasis. The GHG Protocol Corporate Standard explicitly allows—and encourages—improvements in data quality over time. What it requires is transparency: when a change occurs, the base year must be recalculated using the new methodology, and the recalculation must be documented.[1]

From the GHG Protocol Corporate Standard: "Recalculation is necessary when there are changes in company structure, changes in calculation methods or improvements in the accuracy of emission factors or activity data that trigger recalculation."[2]

Most sustainability teams treat recalculation as optional or defer it until assurance. That deferral is the source of the methodology drift problem.

How methodology drift accumulates across reporting cycles

Methodology drift accumulates in three ways:

1. Emission factor changes without base year recalculation. A team uses spend-based factors in year one (default factors from a commercial database), then switches to activity-based factors in year two (supplier-specific primary data). The year-two total decreases, but the decrease reflects the methodology change, not operational improvement. Without recalculating year one using the new factors, the trend claim is invalid.

2. Boundary refinement without documentation. A team excludes a subsidiary in year one (deemed immaterial), then includes it in year two (materiality assessment updated). The year-two total increases, but the increase reflects the boundary change, not emissions growth. Without documenting the boundary logic and recalculating year one, the auditor cannot verify the trend.

3. Allocation method drift. A team allocates Scope 2 emissions by headcount in year one, then switches to floor area in year two. The allocation method is defensible under GHG Protocol, but the change creates a discontinuity. Without recalculating year one using the new method, the year-over-year comparison is meaningless.

The GHG Protocol Corporate Value Chain (Scope 3) Standard notes: "When changes to the calculation methodology result in significant changes to the base year emissions data, the company shall recalculate base year emissions and explain the recalculation to users."[3]

The word "significant" is defined as a change that triggers a threshold—typically 5% of the base year total. But most teams lack the documentation to determine whether a change crossed that threshold, because they do not version the methodology or track the lineage from change to impact.

The CSRD ESRS E1 evidence requirement for trend claims

Under CSRD, ESRS E1 requires GHG Protocol methodology and transparent disclosure of data quality. The standard does not prohibit methodology changes—it requires documentation of those changes and their impact on comparability.[4]

ESRS E1 paragraph 44 states: "When disclosing the information on GHG emissions required under paragraph 44, the undertaking shall refer to ESRS 1 paragraphs from 62 to 67," which govern consistency and comparability of information over time. Paragraph 46 adds: "The undertaking shall include the GHG emissions in accordance with the extent of the undertaking's operational control over them."

The practical implication: if a sustainability team changes emission factors, updates boundaries, or refines allocation methods, and does not recalculate the base year, the auditor cannot verify that the disclosed trend reflects operational change rather than methodology drift. The result is a qualified opinion.

European auditors now routinely request:

- A methodology change log for each reporting period

- A base year recalculation schedule showing the before and after impact of each change

- A lineage document tracing each emission factor to its source, version, and application date

Most sustainability teams lack all three. The gap is not a data problem—it is a versioning and documentation problem.

"The GHG Protocol's Scope 3 Standard ranks methods from most to least accurate: supplier-specific, hybrid, average-data, then spend-based. It does not mandate a single method; it requires organisations to use the most accurate data reasonably available, prioritised by materiality, and to disclose the method used for each category."[5]

The disclosure of method used is the mechanism for proving consistency. Without it, the auditor cannot verify that a reduction is real.

The cost arithmetic of remediation vs. versioned methodology

The cost of remediating methodology drift during assurance is higher than the cost of versioning methodology at the outset. Here is the arithmetic:

Remediation path:

- Sustainability team files year-two inventory without recalculating base year

- Auditor flags trend claim as unverifiable during limited assurance engagement

- Team must reconstruct year-one calculation using year-two methodology

- If source documents (invoices, utility bills, contracts) are no longer accessible, team must use estimates or disclose the limitation

- Assurance engagement is paused, timeline extends by 6-9 months, assurance fee increases by €40,000-€60,000 for a mid-sized filer

- Final report includes qualified opinion on trend claims, which triggers investor and regulator scrutiny

Versioned methodology path:

- Sustainability team documents methodology as versioned policy (emission factors, boundaries, allocation rules)

- Every change to methodology triggers a base year recalculation, stored as a diff

- Recalculation is documented with lineage: before factor, after factor, impacted categories, quantified impact

- Auditor reviews recalculation during assurance, verifies consistency, issues unqualified opinion

- Assurance engagement completes on schedule, no fee inflation, trend claims are verified

The versioned methodology path requires upfront documentation discipline, but eliminates the back-end remediation cost. For wave-two CSRD filers, the window to implement versioned methodology is closing. Most auditors expect to see recalculation documentation starting in year two, which means the methodology versioning must be in place by year one.

The GHG Protocol 2026 revisions and methodology transparency

The GHG Protocol announced in October 2025 a public consultation on Scope 2 updates, with Scope 3 Standard revisions planned for March 2026.[6] The revisions include mandatory data-type disaggregation and verification labeling: organizations will need to report, for each Scope 3 category, the proportion of data that is supplier-specific, hybrid, average-data, or spend-based, and whether that data is fully verified, partially verified, or not verified.[7]

This revision formalizes what auditors are already asking for: a data quality breakdown by category that allows verification of methodology consistency. The revision also signals that spend-based data for material categories will attract qualified audit opinions under CSRD ESRS E1.

From the March 2026 Scope 3 Phase 1 progress update: "Companies should use emission factors that are consistent with the guidance in this Standard and that are appropriate for the company's operations and supply chain. When selecting data sources, companies should use the data quality indicators as a guide to obtaining the highest quality data reasonably available."[8]

The phrase "reasonably available" is the mechanism for allowing data quality to improve over time. But it also requires that the improvement be documented and the base year recalculated. The 2026 revisions will make this requirement explicit.

How Emission3 fits

Emission3 treats methodology as versioned configuration. Every emission factor, boundary rule, and allocation method is stored with a version number and an effective date. When a change occurs—switching from spend-based to activity-based factors, updating a boundary, refining an allocation rule—the system automatically recalculates the base year using the new methodology and generates a diff report showing the before and after impact by scope and category.

The diff report includes:

- The specific categories affected by the change

- The old and new emission factors or allocation rules

- The quantified impact on the base year total and each subsequent year

- The lineage from the change to the revised total, with references to source documents

This documentation is what auditors ask for during limited assurance. It is also what ESRS E1 requires for comparability disclosure. By versioning methodology at the outset, Emission3 eliminates the back-end remediation cycle and preserves trend claims under assurance scrutiny.

For teams moving from spreadsheets or first-generation ESG platforms, the migration includes a methodology audit: we reconstruct the prior-year calculation, version the current methodology, and generate the base year recalculation as part of the onboarding. That recalculation becomes the foundation for all future trend claims.

Close with a CBAM readiness conversation

If your organization is filing multi-year GHG inventories and does not have versioned methodology documentation, the trend claims in your next disclosure are at risk. The cost of remediating methodology drift during assurance is 3-5x the cost of implementing versioned methodology at the outset.

Emission3 customers start with a CBAM readiness call, where we map suppliers, identify gaps, and scope the implementation—including methodology versioning and base year recalculation. No anonymous self-serve onboarding. Book a call at /book-demo.[9]

Citations

[1] GHG Protocol Corporate Standard (2004), Chapter 5, "Setting Organizational Boundaries."

[2] Overview of GHG Protocol Integration in Mandatory Climate Disclosure, page 8, "Base year recalculation is required when there are changes in calculation methods or improvements in the accuracy of emission factors."

[3] GHG Protocol Corporate Value Chain (Scope 3) Standard (2011), Chapter 9, "Accounting for changes in emissions over time."

[4] ESRS E1 Climate Change, paragraph 44, requires GHG emissions disclosure in accordance with operational control and references ESRS 1 paragraphs 62-67 on consistency and comparability.

[5] The GHG Protocol explained: A complete guide to corporate emissions reporting, coolset.com, section on data quality hierarchy.

[6] GHG Protocol announces Scope 2 Public Consultation, pwc.com, October 2025, outlining the revision timeline for Corporate Standard, Scope 2, and Scope 3.

[7] AI Blog for Governments and Enterprises, net0.com, March 2026 update on GHG Protocol Scope 3 Standard Phase 1 revisions introducing mandatory data-type disaggregation.

[8] Scope 3 Standard Revisions Phase 1 Progress Update, ghgprotocol.org, March 2026, page 18, on the use of emission factors and data quality indicators.

[9] Book a CBAM readiness call at Emission3, /book-demo.

References & Sources

External Sources

- [1]GHG Protocol Corporate Standard (2004)

The foundational standard for corporate-level GHG emissions accounting, defining organizational boundaries, scope categorization, and base year recalculation requirements.

- [2]Overview of GHG Protocol Integration in Mandatory Climate Disclosure

January 2025 overview mapping how GHG Protocol standards are integrated into CSRD ESRS E1, California SB 253, and other mandatory disclosure rules, including base year recalculation requirements.

- [3]GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard

The 2011 standard providing requirements and guidance for companies to measure and report emissions across their full value chain, organized into 15 categories, including base year recalculation triggers.

- [4]ESRS E1 - Climate Change (Draft November 2025)

The European Sustainability Reporting Standard on climate change, requiring GHG Protocol methodology and transparent disclosure of data quality, consistency, and comparability over time.

- [5]The GHG protocol explained: A complete guide to corporate emissions reporting

Comprehensive guide to GHG Protocol methodology, including the data quality hierarchy for Scope 3 categories and the connection to CSRD ESRS E1 disclosure requirements.

- [6]GHG Protocol announces Scope 2 Public Consultation

PwC analysis of the October 2025 GHG Protocol public consultation on Scope 2 updates, with timeline for Corporate Standard and Scope 3 Standard revisions through 2027.

- [7]Activity-based vs production-based vs spend-based emission factors: A comprehensive comparison for effective carbon accounting

March 2026 update on GHG Protocol Scope 3 Standard Phase 1 revisions introducing mandatory data-type disaggregation and verification labeling for each Scope 3 category.

- [8]Scope 3 Standard Revisions Phase 1 Progress Update

March 2026 progress update on GHG Protocol Scope 3 Standard revisions, including recommendations on the use of emission factors and data quality indicators.

Related Content

- [9]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, identify gaps, and scope the implementation—including methodology versioning and base year recalculation. No anonymous self-serve onboarding.

- [10]Reporting & filings

CSRD, CBAM, and SB 253 filing generation with versioned methodology, base year recalculation automation, and auditor-ready evidence packs.