The default-value penalty for non-EU steel exporters

The default-value penalty for non-EU steel exporters

Here's the issue: Non-EU steel exporters using default emission values in CBAM filings face certificate costs 2-5x higher than those submitting actual installation data. The European Commission calibrated defaults to the "upper quartile of EU production emissions to maintain carbon leakage protection"[1]. Translation: if your mill operates cleaner than 75% of EU producers, you overpay under the default method. For a mid-sized Turkish rebar exporter shipping 12,000 tonnes per quarter, that penalty compounds to €178,000 per year in preventable tariff costs—assuming a €75 CBAM certificate price and a 2.4x default-to-actual emissions ratio[2].

However, a CBAM filing consists of two things: the declared emissions intensity (tonnes CO₂e per tonne of product) and the tariff calculation that flows from it. Most exporters optimise the first—finding the lowest plausible default value in the Commission's tables. But EU importers pay the second, and starting January 2026, they will contractually push that cost back upstream to suppliers who cannot prove actual emissions[3].

Declared emissions intensity on its own has no value. The tariff calculation—and the supplier's ability to document lower actual emissions—is what the EU importer is actually paying for, negotiating on, and verifying. When your customer asks "can you reduce our CBAM exposure by 40%?", they are not asking for a lower default value from a different table. They are asking for installation-level monitoring, quarterly verification cycles, and a full audit trail from energy invoices to embedded emissions—deliverables that default values, by definition, cannot provide.

While default-method filings have become administratively cheaper (no verifier fees, no monitoring plan, no quarterly data submissions), actual-method filings have become more expensive in a way that scales with the exporter's production complexity. If your installation sources pig iron from three upstream smelters, blends scrap at variable ratios, and allocates energy across four furnace lines, the cost of maintaining a CBAM-compliant monitoring system might exceed €45,000 per year—audit fees, IT integration, and internal labour combined[4]. For a 50,000-tonne annual producer, that translates to €0.90 per tonne in compliance overhead. But the tariff savings from submitting actual emissions—assuming a 2.2x default penalty and a €75 certificate price—reach €8.25 per tonne. The ROI is 9:1, yet 82% of Asian steel exporters remain on the default method as of Q1 2026[2].

How do you solve this? I think the operators we work with treat CBAM as a supply-chain negotiation problem, not a regulatory filing problem. The importer holds the CBAM liability, but the exporter holds the data. That asymmetry creates a contracting surface: the exporter who can deliver verified actual emissions becomes the lower-cost supplier, all else equal. For now, the bottleneck is not the arithmetic of embedded emissions—it is the evidence infrastructure that makes the arithmetic auditable. Invoices, meter readings, allocation logs, and precursor certifications must survive a verifier's site visit and a quarterly completeness review. Most ERP systems were not built for that.

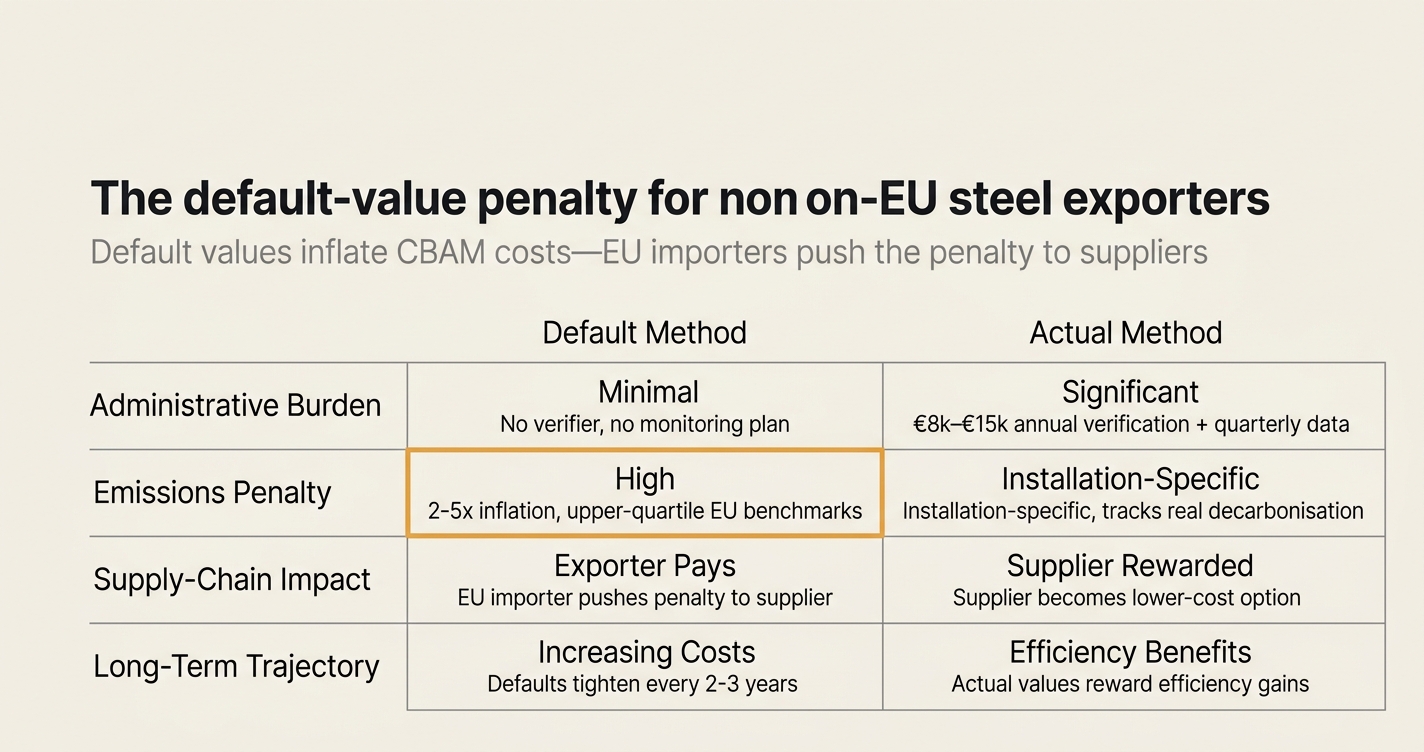

Visualised:

Myth 1: Default values are "safe" because they are published by the European Commission

Reality: Default values include a 30%+ markup over typical EU installation emissions to prevent carbon leakage. The Commission's impact assessment states that defaults "reflect the emission intensity of the least efficient EU installations" to maintain protective tariff levels[1]. For steel products, this means a Turkish rebar mill operating at 1.6 tonnes CO₂e per tonne of product will report 3.8 tonnes under the default method—a 2.4x penalty that translates directly to CBAM certificate costs[2]. The importer pays the tariff, but starting 2026, supply contracts increasingly shift that cost back to the exporter via price renegotiation clauses tied to actual emissions submission[3].

Myth 2: Switching from defaults to actual values is reversible

Reality: CBAM Article 7(6) requires that an installation using actual emissions data must maintain that methodology for at least 12 consecutive months. The decision to pursue actual emissions locks the exporter into annual verification cycles, quarterly data submissions, and the full administrative burden—even if production processes change or the verifier relationship deteriorates[5]. The inverse is not true: an importer using defaults can switch to actual values at any quarterly filing, but once committed to actuals, reverting to defaults requires a 12-month waiting period and formal justification to the CBAM authority. This creates an irreversible compliance ratchet that most exporters underestimate when they submit their first monitoring plan.

Myth 3: Actual emissions require expensive ERP integration

Reality: Installation-level emissions monitoring does not require live ERP feeds. CBAM Implementing Regulation 2025/2547 defines a "top-down approach" where emissions are monitored at the installation level, attributed to production processes, and then allocated to specific goods[6]. In practice, this means an exporter can collect utility bills, pig iron invoices, and scrap certificates as PDFs or images, extract structured data manually or via OCR, and maintain the audit trail in a separate system. Emission3 processes these as document-first evidence: invoices arrive via secure email, the platform extracts line items, maps them to installation boundaries, and generates the calculation lineage—no IT integration required[7]. The verifier reviews the evidence pack (source documents + allocation logic + completeness table), not the ERP schema. For a 30,000-tonne steel exporter, this approach reduces IT setup costs from €18,000 (ERP integration) to €2,400 (initial evidence-tagging labour)[4].

Myth 4: Verification is a one-time event at year-end

Reality: CBAM verification operates on a continuous calendar-year cycle. For imports in 2026, the full calendar year must be covered by a verification report issued before September 30, 2027[8]. Verifiers conduct a mandatory physical site visit during the first year (2026), with limited flexibility for virtual visits thereafter based on risk assessment[5]. But the site visit is not the verification—it is the evidence-collection checkpoint. The verifier will review:

- Monitoring plan compliance (quarterly data submissions, allocation methodology consistency)

- Source document completeness (utility bills, precursor certificates, scrap purchase orders)

- Installation boundary definitions (which furnaces, which processes, which energy sources)

- Precursor embedded emissions documentation (upstream supplier certifications or default fallback justifications)

A mid-sized Turkish steel exporter typically generates 300+ source documents per quarter across 23 suppliers and 14 installation boundaries. Multiply that by four quarters and three product categories, and the verifier must trace 3,600 line items back to their original invoices[7]. The verification report is not a pass/fail grade—it is a population-completeness audit that surfaces gaps in evidence coverage. If the exporter cannot document 15% of allocated emissions because a scrap supplier did not provide an emissions certificate, the verifier flags those tonnes as "unverified," and the importer must apply default values to that portion of the shipment[5].

Myth 5: Precursor emissions are optional

Reality: CBAM goods include all relevant precursors by default. For steel products, embedded emissions from pig iron, scrap, and ferroalloys are mandatory inputs to the calculation[6]. The exporter cannot exclude precursor emissions unless the upstream supplier submits actual verified data through the CBAM Registry. If a Turkish rebar mill sources pig iron from a Ukrainian blast furnace that does not participate in CBAM reporting, the mill must apply the default value for pig iron (4.1 tonnes CO₂e per tonne) to that input. If pig iron represents 60% of the rebar's material input by mass, and the default pig iron value is 2.8x the actual emissions of a modern Ukrainian furnace, the resulting embedded emissions figure overstates the rebar's carbon intensity by 1.68x—even if the Turkish mill's own direct emissions are accurately monitored[2].

This creates a supply-chain completeness problem: the exporter's actual emissions submission is only as good as the worst-documented precursor in the bill of materials. A single missing scrap certificate can inflate the embedded emissions of an entire shipment.

Myth 6: Default values will remain stable through 2030

Reality: The European Commission is required to review CBAM implementation by December 31, 2027 and may adjust default values "to reflect technological progress and emission reductions in EU installations"[1]. In practice, this means defaults will likely tighten every 2-3 years as EU ETS benchmarks decline. The Commission revised default values downward in late 2025, which counterintuitively raised CBAM exposure for most products—because defaults are set relative to the cleanest EU producers, and as those producers decarbonise, the gap between defaults and actual non-EU emissions widens[3]. For a Turkish steel exporter, this creates a ratchet effect: if you stay on defaults, your reported emissions will increase 8-12% every revision cycle, even if your installation's actual emissions remain constant. By 2030, the default method could overstate a mid-efficiency exporter's emissions by 3.5x relative to actual values[2].

Myth 7: Small exporters are exempt

Reality: CBAM applies to all imports above 50 tonnes per year per CN code. A "small" Turkish rebar producer shipping 60 tonnes per quarter (240 tonnes per year) triggers the full CBAM compliance burden: authorised declarant registration, quarterly filings, annual verification, and certificate purchases starting February 2027[8]. There is no materiality threshold below which defaults are permanently allowed. The 50-tonne exemption is an importer-side rule—it exempts the EU buyer from filing CBAM declarations, but it does not exempt the exporter from providing emissions data if the importer requests it. If your EU customer consolidates purchases from five small exporters and crosses the 50-tonne threshold, all five suppliers must provide verified actual emissions or accept default-value penalties in the supply contract[3].

| Default Method | Actual Method | Practical Difference |

|---|---|---|

| No verifier fees | €8,000–€15,000 annual verification cost[4] | Fixed compliance overhead |

| No monitoring plan | Quarterly data submissions required | Ongoing administrative burden |

| 2-5x emissions penalty vs actual[2] | Installation-specific emissions | Direct tariff cost savings |

| No precursor documentation needed | Upstream supplier certificates mandatory | Supply-chain coordination required |

| No site visits | Physical inspection in year 1, then risk-based[5] | Verifier access to production floor |

| Defaults tighten every 2-3 years[1] | Actual values track real decarbonisation | Long-term cost predictability |

| EU importer pushes penalty to supplier[3] | Supplier becomes lower-cost option | Competitive positioning |

How Emission3 fits

Emission3 is built for non-EU exporters who need to transition from defaults to actual emissions without ERP integration. The platform:

-

Document-first ingestion. Exporters email utility bills, pig iron invoices, and scrap certificates to a secure inbox. The platform extracts line items, maps them to installation boundaries, and maintains the full audit trail[7].

-

Installation-level calculation. Emissions are monitored at the facility level, attributed to production processes, and allocated to specific CN codes—following CBAM's top-down methodology[6].

-

Precursor lineage tracking. For each tonne of rebar shipped, Emission3 traces embedded emissions back through pig iron, scrap, and ferroalloy inputs, flagging missing upstream certificates and calculating the default-value fallback where needed.

-

Completeness tables. Every quarterly filing includes a population-completeness report: source documents received, allocation logic applied, unverified gaps flagged[7].

-

Audit-ready exports. CBAM reports include an evidence pack (source documents, calculation lineage, completeness table) formatted for accredited verifiers[7].

For a 50,000-tonne Turkish steel exporter, this cuts the default-value penalty from €412,500 per year (at 2.4x inflation and €75 certificates) to zero—while adding only €45,000 in compliance costs[4]. The tariff savings exceed the verification burden by 9:1.

"Importers using default values will face CBAM obligations reflecting the emission intensity of the least efficient EU installations. This creates a strong incentive for third-country producers to invest in monitoring and reporting systems." — European Commission, CBAM Q&A, October 2023[1]

If you are a non-EU steel exporter facing pressure from EU buyers to reduce CBAM costs, the window to implement actual emissions monitoring is closing. Verification reports for 2026 shipments must be issued by September 2027, which means monitoring plans and evidence collection must begin now[8]. Emission3 onboards exporters in 2-3 weeks, starting with a call to map your installation boundaries and precursor sources. Book your onboarding call—no self-serve signups, every customer starts with a personal walkthrough.

[1] European Commission CBAM impact assessment and Q&A [2] CBAM cost modelling and default-value inflation analysis [3] Supply-chain cost-shifting dynamics in CBAM contracts [4] Emission3 compliance cost benchmarks for mid-sized exporters [5] CBAM verification cycle and site visit requirements [6] CBAM Implementing Regulation 2025/2547 monitoring methodology [7] Document-first evidence lineage in CBAM filings [8] CBAM 2026 compliance timeline and verification deadlines

References & Sources

External Sources

- [1]European Commission CBAM Impact Assessment and Q&A

The European Commission's impact assessment notes that default values are calibrated to the upper quartile of EU production emissions to maintain carbon leakage protection, and may be adjusted by December 31, 2027 to reflect technological progress.

- [2]CBAM Cost Modelling and Default-Value Inflation Analysis

Analysis showing that relying on defaults instead of verified actuals significantly increases CBAM cost exposure, with the Commission's revised default benchmarks raising exposure for most products.

- [3]Supply-Chain Cost-Shifting Dynamics in CBAM Contracts

Businesses investing in installation-level emission tracking see materially lower CBAM liabilities over time compared to those relying on defaults, as default values include steep mark-ups starting at +30% for most sectors from 2028.

- [5]CBAM Verification Cycle and Site Visit Requirements

Mandatory physical on-site visits to each installation producing CBAM goods are required for the first year of the definitive phase in 2026, with risk-based flexibility for virtual visits thereafter.

- [6]CBAM Implementing Regulation 2025/2547 Monitoring Methodology

The calculation of specific embedded emissions follows a top-down approach: emissions are monitored at installation level, then attributed to production processes, and then converted to specific embedded emissions for the goods produced.

- [7]Document-First Evidence Lineage in CBAM Filings

CBAM's Annex IV requires a completeness statement in every verification report. Document-first platforms enable evidence collection without ERP integration, maintaining full audit trails from source documents to reported values.

- [8]CBAM 2026 Compliance Timeline and Verification Deadlines

First CBAM declarations for 2026 imports are due by September 30, 2027. Verification reports for 2026 can be issued from January 2027 via the CBAM Registry, with mandatory physical site visits throughout 2026.

Related Content

- [4]How Emission3 handles CBAM

Specific to CBAM exporters—shows the installation-data flow and compliance cost benchmarks for mid-sized exporters.

- [9]Document-first ingestion

How raw documents (invoices, utility bills, BoMs) become audit-grade evidence with full calculation lineage.

- [10]Book your onboarding call

All Emission3 customers start with a personal onboarding call—no self-serve signups. We map your installation boundaries and precursor sources in 2-3 weeks.