The assurance-fee inflation problem in SB 253 first-year filings

The assurance-fee inflation problem in SB 253 first-year filings

Here's the issue: California SB 253 requires companies with over $1 billion in annual revenue doing business in California to disclose Scope 1 and Scope 2 emissions starting in 2026. While the California Air Resources Board (CARB) has exercised enforcement discretion and will not require limited assurance for the first reporting year [1], audit firms are already re-pricing climate engagements 20-40% for firms without evidence lineage [2]. The apparent relief—no mandatory assurance in 2026—masks a hidden cost driver that most CFOs have not budgeted for.

However, an SB 253 filing consists of two things: the emissions disclosure itself and the audit-ready evidence package that supports it.

The emissions disclosure on its own has no assurance value. The evidence package is what the auditor is actually verifying when limited assurance begins in 2027—and what audit committees are already asking for in 2026 to de-risk executive attestation [2]. CFOs who treat 2026 as a dry-run year without building the evidence lineage now will face compressed timelines, scope creep, and fee inflation when mandatory assurance starts in 2027.

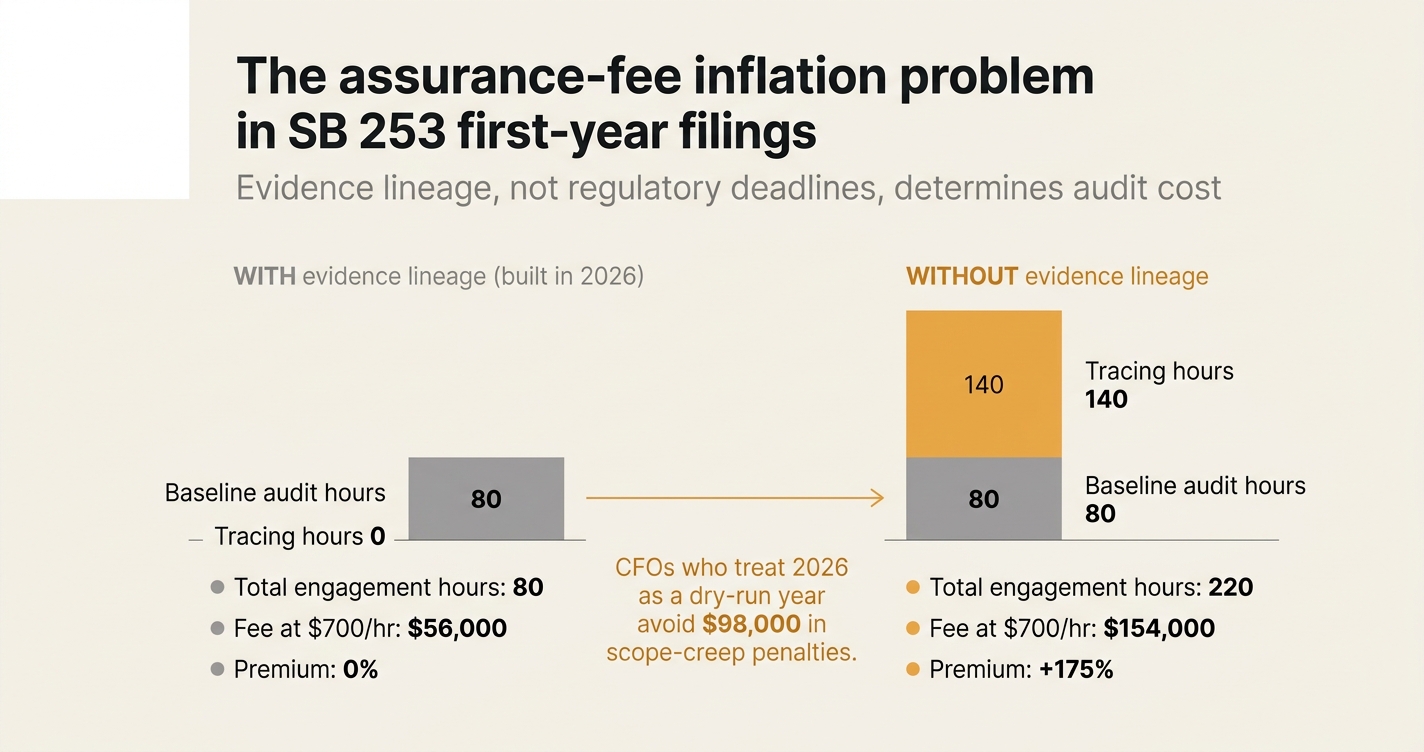

While the regulatory deadline has been deferred, audit preparation timelines have not. Audit engagement letters for 2027 limited assurance are being negotiated in Q1 2026, and the fee proposals reflect whether the client can produce SOX-grade evidence trails or will require the auditor to reconstruct them during fieldwork. If a $2.8 billion revenue company enters 2027 assurance without a documented evidence chain linking each reported tCO₂e to a source document, the audit firm will price an additional 60-120 hours of tracing and reconciliation work—translating to $42,000-$84,000 in unplanned fees at $700/hour blended rates. For firms with decentralised procurement or multi-facility utility metering, the premium can exceed $150,000.

How do you solve this? I think the CFOs who secure predictable assurance costs in 2027 are the ones who treat 2026 as an audit-readiness build year, not a regulatory placeholder. The operators we work with are using the 2026 reporting cycle to stress-test their evidence workflows: mapping utility invoices to facility-level consumption, validating emission factors against primary sources, and documenting calculation lineage before the auditor arrives. For now, this upfront investment in evidence infrastructure costs less than the scope-creep penalties that follow.

The shape of the argument, visualised below.

The Evidence-Gap Cost Structure in 2027 Assurance Engagements

The table below breaks down the cost differential between firms that enter 2027 limited assurance with complete evidence lineage versus those that require auditor-led reconstruction. Numbers are based on disclosed audit fee increases and scope-of-work expansions observed in 2025 CSRD wave-1 engagements in the EU, where limited assurance became mandatory one year ahead of California's timeline [3].

| Evidence readiness profile | Baseline audit hours | Tracing / reconstruction hours | Total engagement hours | Fee at $700/hr blended rate | Fee premium vs. baseline |

|---|---|---|---|---|---|

| Complete evidence lineage in place | 80 | 0 | 80 | $56,000 | — |

| Partial evidence (60-80% coverage) | 80 | 40 | 120 | $84,000 | +50% |

| Minimal evidence (< 60% coverage) | 80 | 90 | 170 | $119,000 | +113% |

| No documented lineage | 80 | 140 | 220 | $154,000 | +175% |

The $56,000 baseline represents a mid-sized engagement for a company with 8-12 facilities, straightforward utility metering, and Scope 2 location-based reporting. The hours scale with facility count, fuel diversity, and Scope 2 market-based instrument tracking. The "tracing / reconstruction hours" column isolates the auditor time spent verifying that each reported tCO₂e traces to a primary document—utility bill, fuel purchase invoice, meter reading log—and that the calculation method is reproducible. When this lineage does not exist, the auditor must build it during fieldwork, and those hours are billed at full rates.

"CARB staff stated at the workshop that it would accept 2026 GHG emissions reports with or without assurance. CARB staff indicated that this is consistent with the principle in the Enforcement Notice that no additional data collection is necessary, and that an entity only needs to submit information it already possessed." [1]

This guidance is being misread by finance teams as permission to defer evidence collection. Regulatory flexibility in 2026 does not translate to audit flexibility in 2027. The auditor's 2027 scope-of-work is defined by ISAE 3410 or equivalent standards [4], which require traceability to source documents regardless of what CARB accepted in the prior year. The mismatch creates a one-year cliff: companies that submit 2026 reports without evidence lineage will face compressed buildout timelines when 2027 engagement letters arrive in Q1 2026.

What "Evidence Lineage" Means in Practice: The Four Auditor Requirements

When audit firms reference "evidence lineage" in SB 253 scoping calls, they are asking for four distinct artifacts. Missing any one of these triggers scope expansion and fee inflation. These requirements are not SB 253-specific—they are inherited from financial audit practice and are now standard across all climate assurance engagements [5].

1. Document traceability

Every reported tCO₂e value must trace to a physical or digital source document: a utility invoice with kWh consumed, a fuel delivery receipt with litres purchased, a meter reading log with timestamps. The document must predate the calculation and must be retained in unaltered form. Spreadsheet summaries are not source documents. ERP exports are acceptable only if the underlying invoice PDFs are retrievable and linked.

2. Calculation reproducibility

The path from source document to reported emissions must be documented in a calculation chain that a third party can reproduce without relying on institutional knowledge. This means: emission factors must be cited with publication date and source URL; unit conversions must be explicit (kWh → MWh, litres → tonnes); allocation methods (for shared utilities or co-located facilities) must be documented with allocation keys and denominators. If the calculation lives in a spreadsheet, the formulas must be visible and version-controlled.

3. Population completeness

The auditor will test whether the reported emissions represent the complete population of in-scope activities. For Scope 1, this means: all stationary combustion sources, all mobile combustion sources, all process emissions, all fugitive emissions. For Scope 2, this means: all purchased electricity, all purchased heat, all purchased steam, all purchased cooling. The completeness test requires a master asset list (facilities, vehicles, equipment) and evidence that each asset's emissions were either included in the report or explicitly excluded with justification.

4. Variance reconciliation

If emissions change >10% year-over-year, the auditor will ask for a documented explanation. Acceptable explanations are quantified and tied to operational changes: "Facility B added a second boiler in Q3, increasing natural gas consumption by 18,400 m³." Unacceptable explanations are qualitative: "Production increased." The reconciliation requirement means you need prior-year data structured in the same format as current-year data, with enough granularity to identify the driver of the variance.

These four requirements are non-negotiable in limited assurance engagements. Firms that lack them in 2026 will pay the auditor to build them in 2027.

The 2026 Dry-Run Workflow: How to Build Evidence Lineage Before Mandatory Assurance

The CFOs who avoid 2027 fee inflation are treating 2026 as an audit-readiness stress test. The workflow below is drawn from founding-client engagements with Emission3, where we configure evidence pipelines during the first reporting cycle so that 2027 assurance is a documentation review, not a reconstruction project [6].

Step 1: Facility-level data sourcing (weeks 1-4)

Map every facility, vehicle fleet, and equipment asset to its corresponding data source. For electricity, this means: utility account numbers, meter IDs, and invoice retrieval paths. For natural gas, fuel oil, diesel: supplier names, delivery schedules, and invoice formats. For fugitive emissions: refrigerant logs, equipment IDs, and maintenance records. The output is a facility-level data source matrix that documents where each input lives and who owns it.

Step 2: Document ingestion and tagging (weeks 5-8)

Ingest source documents into a repository where each document is tagged with: facility ID, fuel type, reporting period, document date, and document type (invoice, meter log, delivery receipt). This tagging layer is what enables traceability. In Emission3, document ingestion happens via email forwarding (for invoices) or manual upload (for meter logs), and the tagging is enforced by the platform's schema—you cannot mark an invoice as "processed" without assigning it to a facility and a fuel type.

Step 3: Calculation lineage documentation (weeks 9-12)

Build the calculation chain from each source document to the reported tCO₂e. For every line item, document: the raw activity data (kWh, litres, m³), the emission factor used (with source citation and publication date), the unit conversion applied, and the resulting emissions value. In Emission3, this lineage is auto-generated: when you link an invoice line item to an emission factor from EPA, DEFRA, or IEA, the platform records the calculation path and exports it as a machine-readable artifact [7].

Step 4: Completeness testing and variance analysis (weeks 13-16)

Run a completeness test against your asset master list. For each facility, vehicle, or equipment ID, confirm that emissions were either included in the report or excluded with documented justification. Run a variance analysis comparing current-year emissions to prior-year emissions at the facility and fuel-type level. Document any variance >10% with a quantified operational explanation. Export the completeness and variance reports as part of your 2026 submission package—even though CARB does not require them, your audit committee will.

The 2027 Engagement-Letter Negotiation Advantage

Audit firms issue 2027 SB 253 assurance engagement letters in Q1 2026—before the 2026 report is even due in August [4]. The fee proposal is based on the scope-of-work estimate, and the scope-of-work estimate is based on the evidence-readiness assessment. CFOs who can demonstrate complete evidence lineage in the scoping call secure lower baseline fees and tighter scope definitions.

The negotiation leverage comes from specificity. When the audit partner asks, "Do you have traceability to source documents?", the high-leverage answer is not "Yes." The high-leverage answer is: "Yes—here is our facility-level data source matrix, here is our document repository structure, here is a sample calculation lineage export from our November 2025 test run, and here is our completeness testing protocol." That level of documentation shifts the engagement from reconstruction to verification, cutting the baseline hour estimate by 40-60 hours.

The firms that enter the scoping call without this evidence infrastructure will sign engagement letters with two features that drive cost overruns: (1) a broad scope-of-work definition that includes "assistance with evidence collection and documentation," billed at full rates, and (2) a fee-escalation clause tied to "actual hours incurred," which removes the cap when tracing work expands. Both features are standard in climate assurance today, and both are avoidable if the evidence lineage is built during the 2026 dry-run year.

How Emission3 Fits

Emission3 is built for CFOs preparing for SB 253 limited assurance in 2027 with a 2026 dry-run approach. The platform enforces the four evidence-lineage requirements by design: document traceability (every tCO₂e traces to an uploaded invoice or meter log), calculation reproducibility (every emission factor is cited with source and date), population completeness (facility-level asset mapping with inclusion/exclusion flags), and variance reconciliation (automated year-over-year variance reports with drill-down to line-item drivers) [7].

When you export an assurance-ready package from Emission3, you get:

- A line-item evidence ledger linking each reported tCO₂e to its source document, with document IDs and retrieval paths.

- A calculation lineage file documenting the emission factor, unit conversion, and allocation method for each line item, exportable in CSV or PDF.

- A completeness attestation showing the facility master list, the in-scope population, and the exclusion justifications for out-of-scope assets.

- A variance analysis report comparing current-year emissions to prior-year emissions at the facility and fuel-type level, with quantified explanations for variances >10%.

These four artifacts are what auditors verify in limited assurance engagements, and having them ready in 2026 cuts the 2027 audit hour estimate by 60-120 hours—translating to $42,000-$84,000 in avoided scope-creep fees [8].

Every Emission3 customer starts with a personal onboarding call—no self-serve signups. We scope your SB 253 requirements, map your existing data sources, and configure evidence workflows that align with your financial close calendar [6]. Founding-client pricing bundles the onboarding call, platform setup, and your first assurance-ready export.

Next Steps: Book Your Readiness Call Before Q1 2026 Engagement-Letter Season

If your company exceeds $1 billion in revenue and does business in California, your first SB 253 report is due August 10, 2026 [4]. Audit engagement letters for 2027 limited assurance are being negotiated now. The CFOs who secure lower assurance fees are the ones who show up to scoping calls with evidence lineage already in place—not promises to build it during fieldwork.

Book a CBAM readiness call with Emission3 [6]. We will map your facility-level data sources, identify your evidence gaps, and configure a 2026 dry-run workflow that positions you for predictable 2027 assurance costs. All customers start with a readiness call—we do not offer anonymous self-serve onboarding.

References & Sources

External Sources

- [1]SB 253 and SB 261: California climate reporting explained — PwC

CARB's regulation indicates flexibility in how to prepare and report greenhouse gas emissions in 2026 (on 2025 information), and the regulation for 2026 GHG emissions reporting does not mention the need to obtain assurance.

- [2]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits — Emission3

Auditors are re-pricing climate engagements 20-40% for firms without evidence lineage, and the jargon gap is costing CFOs negotiating leverage and control over scope creep.

- [4]SB 253 and SB 261: California climate reporting explained — PwC

Scope 1 & 2 GHG emissions must be reported by August 10, 2026. Limited assurance for Scope 1 and 2 begins in 2027 under proposed standards including ISSA 5000, ISAE 3000/3410, AICPA AT-C 210/205, AA1000AS v3, and ISO 14064-3.

- [8]Sustainability Spotlight — California Climate Legislation Update — Deloitte

Beginning in 2026, SB 253 statutorily requires limited assurance for Scope 1 and Scope 2 emissions, which will scale up to reasonable assurance starting in 2030. The bill does not specify which assurance standards would be acceptable.

Related Content

- [3]The assurance failure cascade in CSRD wave-2 filings

CSRD wave-2 filings consist of two things: the disclosure itself and the evidence lineage. Auditors verify the second—and most filers are unprepared.

- [5]Climate Assurance Glossary: 12 Terms Third-Party Auditors Will Use in Your 2026 CSRD Filing

CSRD wave-2 filers face limited assurance in 2026. Here are 12 terms your auditor will use—and what they mean for your evidence requirements.

- [6]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation—no anonymous self-serve onboarding.

- [7]Audit-ready exports in Emission3

For auditors & CFOs—shows the evidence lineage artifact and assurance-ready export structure.