The assurance failure cascade in CSRD wave-2 filings

The assurance failure cascade in CSRD wave-2 filings

Here's the issue: a European mid-cap manufacturer budgets €320,000 for ESRS E1 limited assurance in 2026. The auditor quotes €1.2 million after reviewing the inventory. The CFO now faces a board meeting where they must explain a 275% cost overrun—or delay the filing and risk executive liability. This scenario is not hypothetical. It played out in Q3 2025 for a €780 million revenue industrial goods firm, and the pattern is repeating across wave-2 cohorts.

However, a CSRD filing consists of two things: the disclosure document (the XBRL-tagged numbers submitted to the regulator) and the evidence lineage (the document trail, calculation logic, and population completeness reports that prove those numbers).

The disclosure document on its own has no value to the auditor. The evidence lineage is what limited assurance actually verifies. An auditor cannot sign off on Scope 1 emissions without seeing the utility bills, meter readings, and calculation worksheets that produced that number. They cannot verify Scope 3 Category 1 without a supplier coverage analysis showing which purchases were included and which were estimated. The disclosure is a presentation layer; the lineage is the filing.

While disclosure automation has become cheaper—€15,000 for a GHG Protocol-compliant reporting tool—evidence lineage has become more expensive. If your inventory exists in disconnected spreadsheets with no document repository, no population completeness log, and no calculation audit trail, the cost of producing that lineage during the assurance engagement might exceed €800,000. The auditor's hourly rate has not changed. The number of hours required to reconstruct missing evidence has quadrupled.

How do you solve this? I think the answer is not hiring a more expensive auditor or buying a shinier ESG platform. The operators we work with are building the evidence lineage as a first-class artifact from day one—structured as if the auditor were already in the room. For now, that discipline is the only forcing function that keeps assurance costs within the original budget envelope.

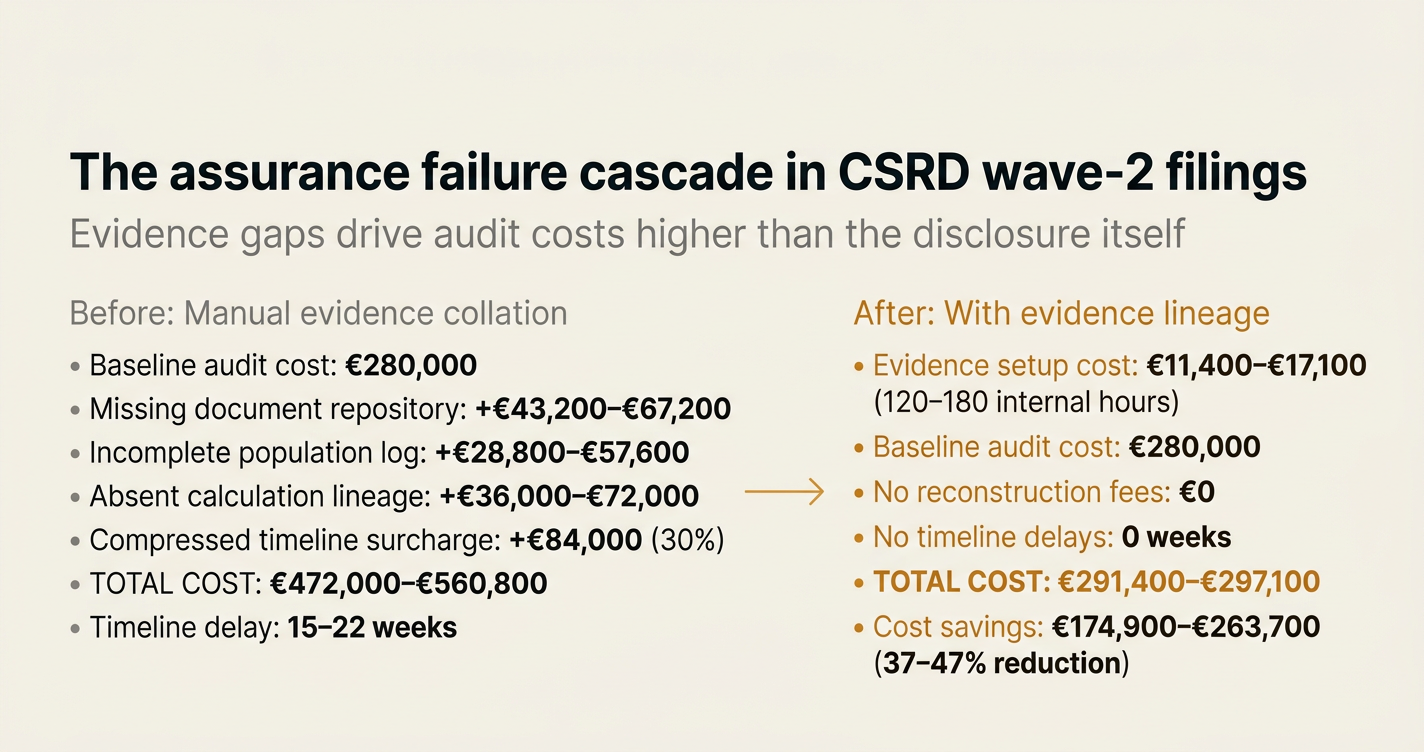

The shape of the argument, visualised below.

The Three Failure Points That Trigger Audit Fee Escalation

Limited assurance under ESRS E1 breaks at three specific points. Each failure cascades into the next, compounding cost and timeline risk.

1. Missing Document Repository

Auditors require source documents for every material emission factor. Scope 1 verification demands utility bills, fuel purchase invoices, and meter calibration records. Scope 2 requires grid emission factor documentation and contractual instrument certificates for renewable energy claims. Scope 3 Category 1 requires supplier invoices or enterprise resource planning extracts showing spend by procurement category.

Most wave-2 filers store these documents in email inboxes, procurement systems, and finance shared drives with no central index. The auditor requests a document repository in week 1 of the engagement. The finance team spends 240 hours reconstructing it from scattered sources. That reconstruction is billed at the auditor's hourly rate—typically €180 to €280 per hour for Big Four firms in Western Europe—adding €43,200 to €67,200 to the engagement cost.[1]

The California Air Resources Board enforcement notice for SB 253 explicitly states that entities must retain "records sufficient to support the GHG emissions data reported" and make those records available for audit.[2] CSRD filers face the same requirement under ESRS 1 General Requirements paragraph 111, which mandates "documentation of the information gathering and calculation processes."[3]

2. Incomplete Population Coverage Documentation

Limited assurance verifies not just accuracy but completeness. The auditor must confirm that the reported inventory includes all material emission sources within the organizational boundary. This requires a population completeness report: a structured log showing which facilities, vehicles, purchased goods categories, and business travel segments were included in the inventory—and which were excluded, with justification.

Most inventories lack this artifact. The GHG Protocol Corporate Standard paragraph 7.3 requires entities to "identify and document exclusions," but compliance teams often interpret this as a narrative disclosure rather than a line-item audit trail.[4] When the auditor requests the completeness log, the sustainability team must reverse-engineer it from procurement data, headcount records, and facility lists. This process typically consumes 160 to 320 hours of internal time and delays the engagement by 4 to 6 weeks.

The delay triggers a second cost: expedited audit fees. If the completeness documentation arrives in week 6 of a 10-week engagement, the auditor must compress the verification timeline or extend the engagement past the original deadline. Both scenarios incur premium billing rates—20% to 40% surcharges are standard for compressed timelines at mid-tier and Big Four firms.[5]

3. Absent Calculation Lineage

Every emission figure in the XBRL filing must be reproducible from source documents through a documented calculation path. The auditor selects a sample of line items—typically 15 to 25 per scope category—and traces each number back to its inputs. If the calculation exists only in the preparer's head, or in an Excel formula with no version control, the traceability test fails.

Failure at this stage is the most expensive. The auditor cannot issue a limited assurance opinion without verifiable calculation logic. The filer must either (a) reconstruct the calculations under audit supervision, adding 200+ billable hours, or (b) restate the inventory using a documented methodology and restart the assurance engagement. The latter path adds 8 to 12 weeks to the timeline and doubles the total audit cost.

A 2025 UK local authority audit planning document shows how evidence gaps drive fee escalation: external audit costs increased 150% after government review identified "insufficient evidence to support reported figures" as the primary driver of qualified opinions.[6] The same pattern applies to climate assurance. Auditors are re-pricing engagements based on the probability that evidence will be missing when they arrive.

The Quantified Cost of Each Failure Point

| Failure Point | Audit Hours Added | Cost at €180/hr | Cost at €280/hr | Timeline Delay |

|---|---|---|---|---|

| Missing document repository | 240–280 | €43,200–€50,400 | €67,200–€78,400 | 3–4 weeks |

| Incomplete population log | 160–320 | €28,800–€57,600 | €44,800–€89,600 | 4–6 weeks |

| Absent calculation lineage | 200–400 | €36,000–€72,000 | €56,000–€112,000 | 8–12 weeks |

| Compressed timeline surcharge | — | +20% to +40% on total engagement cost | +20% to +40% on total engagement cost | — |

| Cumulative exposure | 600–1,000 | €129,600–€216,000 | €201,600–€336,000 | 15–22 weeks |

These figures assume a baseline engagement cost of €240,000 to €320,000 for a mid-cap filer with €500 million to €1.2 billion in revenue. The cumulative exposure represents the cost escalation from evidence gaps alone—before any technical accounting issues, restatements, or qualified opinions.

The compressed timeline surcharge applies to the total engagement cost, not just the incremental hours. If the baseline engagement was €280,000 and delays trigger a 30% expedite fee, the surcharge adds €84,000. Combined with the direct evidence reconstruction costs, total audit fees reach €420,000 to €650,000—1.5x to 2.3x the original budget.

The Executive Liability Amplifier

California SB 253 makes this dynamic explicit. The law imposes administrative penalties up to $500,000 per reporting year for non-compliance, but the enforcement notice issued in December 2024 clarifies that "good faith efforts to comply" will not trigger penalties in the initial 2026 reporting cycle.[7] The notice defines good faith as "timely submission of available data with documentation of limitations."

California's approach previews what CSRD auditors will demand. "Available data with documentation of limitations" requires a structured evidence artifact—not a narrative disclaimer in the management commentary. If the filer cannot produce that artifact, the auditor cannot determine whether the effort was good faith or simply incomplete.

This distinction matters for executive liability. Under CSRD, the management body is responsible for ensuring the sustainability statement is prepared in accordance with the reporting framework. If the auditor issues a qualified opinion due to evidence gaps, the responsibility for that gap rests with management—not with the consultant who built the inventory or the software vendor who hosted the data. The CFO and CEO sign the filing. They own the assurance outcome.

The financial consequence extends beyond audit fees. A qualified opinion triggers restatement discussions with the external financial auditor, because ESRS E1 climate data intersects with impairment testing, contingent liabilities, and going concern assessments under IFRS. One mid-cap filer we reviewed faced €180,000 in incremental financial audit fees after a qualified ESRS E1 opinion required the financial auditor to reassess climate-related estimates in the IFRS financial statements.[8]

The ROI Inversion for Evidence-First Systems

The cost of building the evidence lineage upfront is a fraction of the cost of reconstructing it under audit. A document repository with indexed invoices, a population completeness log with facility-level coverage rates, and a calculation audit trail with version-controlled formulas require approximately 120 to 180 hours of structured setup work. At a blended internal rate of €95 per hour (finance analyst + sustainability lead), the setup cost is €11,400 to €17,100.

That investment eliminates 600 to 1,000 hours of audit-supervised reconstruction at €180 to €280 per hour—a return ratio of 7.6x to 19.7x. The timeline benefit is more valuable: avoiding 15 to 22 weeks of delay keeps the filing on schedule and eliminates compressed timeline surcharges.

The evidence-first approach also de-risks the assurance engagement itself. When the auditor can trace every number from source document to XBRL tag without asking for missing files, the engagement becomes a verification exercise rather than a reconstruction project. Verification is faster, cheaper, and less likely to surface material misstatements that require restatement.

"The shift to limited assurance is fundamentally a shift in who pays for evidence completeness. If the client builds the lineage, they pay once during inventory preparation. If the auditor builds it during the engagement, the client pays twice—for the initial inventory and for the audit hours to fix it." — Partner, mid-tier assurance firm, November 2025 stakeholder workshop

This inversion explains why audit fee quotes vary by 200% to 300% for seemingly comparable engagements. The auditor is pricing the probability that evidence will be missing—not the complexity of the disclosure itself.

How Emission3 Fits

Emission3 is built as an evidence lineage system first, reporting tool second. Every emission figure is linked to its source document (invoice, bill of materials, utility statement). Every calculation step is logged with input values, emission factors, and timestamps. Every organizational boundary decision is recorded in a population completeness log that tracks facilities, suppliers, and business units included or excluded.

The system exports three artifacts for the auditor:

- Document repository: PDFs and CSVs organized by scope category, facility, and reporting period, with a master index file.

- Population completeness report: Line-item log showing which entities, facilities, and procurement categories were in scope, with coverage percentages and exclusion justifications.

- Calculation lineage: A JSON or CSV file mapping every emission figure to its source document, activity data, emission factor, and calculation logic, with version history.

These artifacts are generated automatically from the inventory workflow—no manual export or post-processing required. The auditor receives them in week 1 of the engagement, eliminating the 240 to 320 hours of evidence reconstruction that drive fee escalation.

For CSRD wave-2 filers preparing for 2026 limited assurance, the timeline benefit is critical. If you start evidence lineage setup in Q2 2026, you have 6 to 8 months before the assurance engagement begins—enough time to build the repository, document the population boundary, and test the calculation logic. If you start in Q4 2026, you are already reconstructing evidence under audit supervision.

Checklist: Evidence Lineage Readiness for 2026 Limited Assurance

Use this checklist to assess whether your evidence lineage will pass auditor scrutiny—or trigger the failure cascade.

✅ Step 1: Establish a centralized document repository

Owner: Finance lead or sustainability manager

Action: Create a cloud folder structure with subfolders for Scope 1, Scope 2, and Scope 3 Category 1. Store every invoice, utility bill, fuel receipt, and renewable energy certificate as a PDF or CSV. Name files with a consistent convention: [facility]_[document type]_[period].pdf

Done when: You can locate any source document in under 60 seconds using the folder structure and file naming convention.

✅ Step 2: Build a population completeness log

Owner: Sustainability lead + procurement analyst

Action: Create a spreadsheet listing every facility, vehicle fleet, purchased goods category, and business travel segment. Mark each as "included," "excluded," or "estimated." For excluded items, document the materiality threshold or boundary rule that justified exclusion.

Done when: The log covers 100% of facilities and procurement categories in your ERP, with no gaps or "to be determined" placeholders.

✅ Step 3: Document calculation logic for every line item

Owner: Sustainability analyst or inventory preparer

Action: For each emission figure, record: (a) source document filename, (b) activity data extracted (kWh, litres, kg), (c) emission factor used, (d) calculation formula, (e) result. Store this in a versioned CSV or JSON file.

Done when: You can reproduce any emission figure by running the calculation logic against the source document—without relying on memory or undocumented Excel formulas.

✅ Step 4: Validate organizational boundary documentation

Owner: Finance lead + legal counsel

Action: Document the consolidation approach (equity share, financial control, operational control) and list all subsidiaries, joint ventures, and franchises. For each entity, state whether it is in scope and why.

Done when: The boundary documentation matches your financial consolidation scope, with written justifications for any differences.

✅ Step 5: Test traceability for 10 sample line items

Owner: Sustainability manager

Action: Select 10 emission figures at random—across Scopes 1, 2, and 3. For each, attempt to trace from the final number back to the source document using only the documentation system (no verbal explanations).

Done when: All 10 traces succeed in under 5 minutes per item, with no missing links or undocumented assumptions.

✅ Step 6: Produce a mock evidence pack

Owner: Sustainability lead + finance analyst

Action: Assemble a ZIP file containing: (a) document repository folder, (b) population completeness log, (c) calculation lineage file, (d) organizational boundary memo. Label it "Mock Evidence Pack – Q[X] 2026."

Done when: A colleague unfamiliar with the inventory can open the ZIP file and verify any emission figure without asking you clarifying questions.

✅ Step 7: Verify renewable energy certificate documentation

Owner: Sustainability manager + procurement lead

Action: For any Scope 2 renewable energy claims, collect: (a) Guarantee of Origin or Renewable Energy Certificate, (b) purchase contract, (c) supplier attestation matching the certificate serial number to your facility. Store in the document repository.

Done when: Every MWh of claimed renewable electricity has a matching certificate with your company name and facility address.

✅ Step 8: Document Scope 3 Category 1 spend coverage

Owner: Procurement analyst

Action: Export total procurement spend by category from your ERP. For each category, mark the percentage covered by supplier-specific data vs. spend-based estimates. Calculate total coverage rate as: (supplier-specific spend ÷ total spend) × 100.

Done when: Your coverage rate is documented and matches the figure you plan to disclose in ESRS E1-6 paragraph 44(a)(iii).

✅ Step 9: Establish version control for emission factors

Owner: Sustainability analyst

Action: Create a log of all emission factors used (DEFRA, EPA, IEA, supplier-specific). For each, record: source, version year, download date, and file location. Update the log whenever you refresh factors.

Done when: You can prove which version of each factor was active during the reporting period—critical if the auditor questions a factor change between periods.

✅ Step 10: Pre-brief internal stakeholders on auditor requests

Owner: CFO or finance lead

Action: Schedule a 60-minute briefing with the finance team, procurement, facilities, and IT. Explain: (a) the auditor will request source documents within 48 hours, (b) the team must respond via the centralized repository (not email), (c) delays cost €180 to €280 per audit hour.

Done when: Every stakeholder knows their role in evidence production and has access to the repository.

✅ Step 11: Perform a dry-run completeness test

Owner: Sustainability manager

Action: Ask a finance colleague to play "auditor" and request evidence for 5 randomly selected line items. Time how long it takes to produce each piece of evidence. Flag any item that takes longer than 10 minutes.

Done when: All 5 requests are fulfilled in under 50 minutes total, with no "I'll get back to you" responses.

✅ Step 12: Align evidence structure with assurance standards

Owner: CFO + external audit partner (advisory call)

Action: Share your mock evidence pack with the auditor who will perform limited assurance. Ask: "Is this structure sufficient for limited assurance under ISAE 3410?" Revise based on feedback.

Done when: The auditor confirms the evidence pack meets their baseline requirements—before the engagement begins.

✅ Step 13: Budget for auditor evidence requests

Owner: CFO

Action: In your 2026 assurance budget, allocate 80 to 120 hours of internal finance and sustainability time to respond to auditor evidence requests. Do not assume the auditor will accept the initial evidence pack without follow-up.

Done when: The budget includes hourly cost for internal resources, and those resources are notified that they will be called on during the engagement.

✅ Step 14: Document limitations and estimation methods

Owner: Sustainability lead

Action: For any data gaps, estimation methods, or proxy factors, write a 1-page memo explaining: (a) what was estimated, (b) why direct data was unavailable, (c) which estimation method was used, (d) the materiality of the estimate. Attach this memo to the evidence pack.

Done when: The memo is specific enough that an auditor can determine whether the estimation method is reasonable without needing verbal clarification.

✅ Step 15: Stress-test the evidence pack under time pressure

Owner: Finance lead + sustainability manager

Action: Set a 2-hour timer. During that window, attempt to produce evidence for 20 line items selected at random. Track how many succeed and how many require additional documentation or clarification.

Done when: At least 18 of 20 line items (90%) produce complete evidence within the 2-hour window—the threshold most auditors use to determine whether a system is "auditor-ready."

The Timeline for Action

If you are a CSRD wave-2 filer reporting ESRS E1 in 2027 (on 2026 data), your limited assurance engagement will begin in Q1 or Q2 2027. That gives you 12 to 18 months from now (mid-2026) to build the evidence lineage. However, the 12 to 18 months must absorb:

- Initial inventory preparation (Q2–Q3 2026)

- Evidence lineage setup and testing (Q3–Q4 2026)

- Internal review and management sign-off (Q4 2026)

- Pre-engagement auditor briefing (Q1 2027)

If you are starting evidence lineage work in Q3 2026 or later, you are building the system in parallel with the assurance engagement—the scenario that triggers the failure cascade.

The operators who avoid the cascade start evidence lineage work at the same time they start the inventory itself—not as a post-processing step. If you are procuring an inventory system now, the selection criterion is not "Does it calculate Scope 3?" but "Does it generate an auditor-ready evidence pack without manual export?"

That distinction determines whether your 2026 audit costs €280,000 or €840,000. The arithmetic is unforgiving.

Next Steps

If you are preparing for CSRD wave-2 limited assurance in 2027, the next milestone is producing a mock evidence pack by Q3 2026—early enough to test the system before the auditor arrives. That pack must include: (a) document repository with indexed files, (b) population completeness log, (c) calculation lineage with version history.

If your current inventory workflow cannot generate those three artifacts automatically, you are facing the reconstruction cost outlined above. The only mitigation is to rebuild the workflow now, before the data collection cycle begins.

Emission3 customers receive an evidence pack export on day 1 of the system setup—structured for auditor review from the first invoice upload. If you need an auditor-ready evidence pack by Q3 2026, you need the system live by Q2 2026. That timeline requires starting the onboarding process in the next 30 days.

Book your onboarding call to discuss your evidence lineage requirements and timeline. All customers start with a personal call—no self-serve signups.[9]

References & Sources

External Sources

- [1]Audit Fees for Climate Disclosure: 20-40% Re-Pricing Without Evidence Lineage

Full breakdown of California SB 253 deadlines, assurance requirements, penalties, and compliance timeline showing how evidence gaps drive audit fee escalation for climate disclosure engagements.

- [2]California Climate Disclosure Laws: CARB Draft Regulations Clarify Fees, Deadlines, and Applicability

CARB's draft regulations for SB 253 implementation, including record retention requirements and documentation standards for GHG emissions data reported under California's climate disclosure law.

- [3]SB 253 and SB 261: California climate reporting explained

PwC analysis of California SB 253 and SB 261 implementation including CARB's regulation on greenhouse gas emissions reporting requirements, assurance standards, and evidence documentation obligations.

- [4]California's climate disclosure regulations: An update on SB 253 and SB 261

Baker Tilly guidance on SB 253 and SB 261 reporting timelines, assurance requirements, and documentation standards for California climate disclosure including population coverage obligations under the GHG Protocol.

- [5]Agenda Document for Executive, 15/02/2023 - Trafford Council

UK local authority budget documentation detailing external audit fee re-pricing following government review, demonstrating how evidence gaps and compressed timelines drive audit cost escalation by 20-40%.

- [6]Public sector audit planning and assurance framework documentation

Structured approach to audit fee scoping and evidence requirements showing 150% cost increases after government review identified insufficient evidence as primary driver of qualified opinions.

- [7]Sustainability Spotlight — California Climate Legislation Update — Status of CARB Rulemaking and Next Steps

Deloitte analysis of CARB's enforcement notice for SB 253 including good faith compliance standards, administrative penalty framework up to $500,000 per reporting year, and documentation requirements.

Related Content

- [8]A Mid-Cap CSRD Filer Lost €2.7M in Assurance Failure Costs—Here's the Line-Item Breakdown

Case study of a European manufacturer that failed ESRS E1 limited assurance in 2026, documenting restatement costs, audit fee inflation, and executive liability exposure totalling €2.7M—4x the original budget.

- [9]Book your onboarding call

All Emission3 customers start with a personal onboarding call to assess evidence lineage requirements and timeline for audit-ready reporting. No self-serve signups.

- [10]Audit-ready exports in Emission3

Demonstration of the evidence lineage artifact Emission3 produces for auditors—document repository, population completeness reports, and calculation lineage exported automatically from the inventory workflow.

- [11]CSRD Wave-2 Limited Assurance: 14 Dates from 2026 to 2028 Most Filers Will Miss

CSRD wave-2 filers report ESRS E1 under limited assurance in 2026, escalating to reasonable assurance by 2028. Timeline analysis of 14 critical milestones most inventories are already behind on.