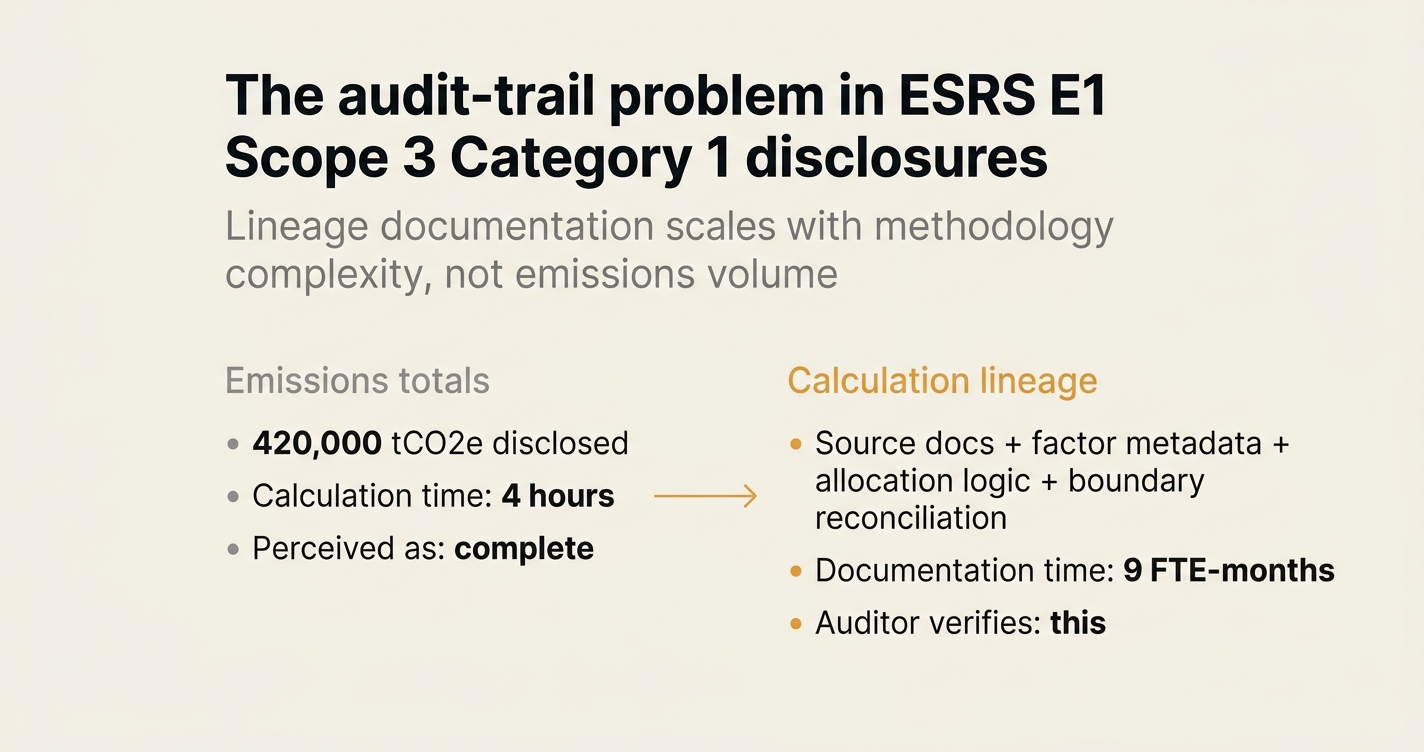

The audit-trail problem in ESRS E1 Scope 3 Category 1 disclosures

The audit-trail problem in ESRS E1 Scope 3 Category 1 disclosures

Here's the issue: under the Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standard (ESRS) E1, European companies must disclose Scope 3 greenhouse gas (GHG) emissions with limited or reasonable assurance, depending on their reporting wave. For most industrials and large retailers, Category 1—Purchased Goods and Services—represents 60 to 80 percent of total Scope 3 footprint. At first glance, the requirement looks manageable: aggregate supplier emissions, multiply activity data by emission factors, sum the results, and disclose the total.

However, ESRS E1 disclosure consists of two things: emissions totals and calculation lineage. The first is what most sustainability teams track in spreadsheets or carbon accounting software. The second is a documented audit trail from source documents—purchase orders, invoices, bills of materials, supplier questionnaires—through each calculation step to the final disclosed number. ESRS E1 references the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011), which requires organisations to document methodologies, data sources, emission factors, and assumptions for each category [1].

Emissions totals on their own have no value under assurance scrutiny. Calculation lineage is what the auditor is actually verifying. When an auditor requests evidence for a disclosed Scope 3 Category 1 total of 420,000 tonnes of carbon dioxide equivalent (tCO2e), they expect to see: (a) the raw activity data tied to financial records, (b) the emission factors applied with version and source metadata, (c) the allocation logic for multi-product purchases, (d) supplier-specific data where claimed, and (e) a reconciliation showing completeness across the procurement boundary. Without this lineage, the auditor flags the inventory as not assurance-ready, and the company faces a qualified opinion or delays the filing.

While spend-based emission factors have become cheaper and easier to apply—DEFRA publishes free industry-average factors, and software platforms embed them—building and maintaining calculation lineage has become more expensive. If a company uses spend-based factors for 70 percent of Category 1 and supplier-specific data for 30 percent, the documentation burden for the supplier-specific portion might consume three full-time equivalents (FTEs) for six months, while the spend-based portion requires only light quarterly updates. Yet auditors apply the same evidence standards to both. The lineage cost does not scale with emissions volume; it scales with data heterogeneity and methodology complexity.

How do you solve this? I think the answer—at least for the next two to three reporting cycles—is to design the Scope 3 inventory with auditability as the primary constraint, not emissions coverage. The operators we work with are starting with a narrow but deeply documented inventory: fewer suppliers, but full lineage for each. They treat the first ESRS E1 filing as a test of the documentation system, not a complete footprint. For now, a 60 percent complete inventory with full audit trails beats a 95 percent complete inventory with no evidence packs. The coverage will expand in subsequent years, but the lineage infrastructure must be in place from the start.

The shape of the argument, visualised below.

Why lineage is harder than totals

The ESRS E1 requirement for Scope 3 emissions builds on the GHG Protocol Scope 3 Standard (2011), which defines 15 categories of indirect emissions across a company's value chain. Category 1—Purchased Goods and Services—covers all upstream emissions from cradle to gate for purchased products and services, excluding capital goods (Category 2) and fuel and energy-related activities (Category 3) [2]. For a manufacturing company, this includes raw materials, components, packaging, consumables, and outsourced services. For a retailer, it includes finished goods and logistics services.

The calculation method depends on data availability. The GHG Protocol hierarchy runs: supplier-specific data (primary), hybrid data (primary data combined with secondary factors), average-data factors (industry or product averages), and spend-based factors (emissions per euro spent by procurement category) [3]. Most companies start with spend-based factors because procurement data lives in enterprise resource planning (ERP) systems, and emission factors are publicly available. A procurement total of €10 million in electronics components multiplied by an average factor of 0.85 kilograms of carbon dioxide equivalent per euro (kgCO2e per euro) yields 8,500 tCO2e. The calculation takes minutes.

The lineage, however, requires:

- Source document retention: invoices or ERP exports proving the €10 million spend, with line-item detail where multi-product invoices exist.

- Factor metadata: the emission factor source (for example, DEFRA 2025 supply chain factors, version 1.2, electronics category), the geographic and temporal scope, and any adjustments for currency or product mix.

- Allocation logic: if the electronics category includes both semiconductors (high-emissions) and passive components (low-emissions), the allocation method must be documented and applied consistently.

- Boundary reconciliation: a control total showing that the €10 million is part of a larger procurement boundary, with explicit exclusions (for example, capital goods reclassified to Category 2) listed and justified.

- Change log: if the factor changes between reporting periods, the impact on trend comparability must be quantified and disclosed.

This documentation package does not exist in most finance or procurement systems. It must be built and maintained separately. For a company with 500 active suppliers and 20 procurement categories, the lineage workload scales with supplier count and category complexity, not with emissions volume. A €1 million spend in a high-complexity category (for example, custom components with supplier-specific lifecycle assessment data) may require more documentation effort than a €50 million spend in a low-complexity category (for example, standard office supplies with stable DEFRA factors).

Audit expectations under ESRS E1

ESRS E1 requires companies to disclose gross Scope 1, 2, and 3 emissions following GHG Protocol methodology, with Scope 3 broken down by significant categories [4]. For Category 1, significance is typically determined by materiality thresholds: if purchased goods and services represent more than 5 percent of total Scope 3 emissions, or if they are financially or reputationally material (for example, a food retailer's agricultural supply chain), they must be disclosed with full methodological documentation.

The European Financial Reporting Advisory Group (EFRAG), which oversees ESRS implementation, has signalled that spend-based data for material categories will attract qualified audit opinions in later reporting waves [3]. The 2026 draft revisions to ESRS E1 clarify that companies must label data by type—supplier-specific, hybrid, average-data, or spend-based—and by verification status—fully verified, partially verified, or not verified [1]. Auditors will test whether the disclosed labels match the underlying data and whether the calculation lineage supports the claimed accuracy.

The audit procedure for Category 1 typically follows this sequence:

| Audit Step | What Auditor Tests | Evidence Required |

|---|---|---|

| Boundary completeness | Does the inventory cover all material purchased goods and services? | Procurement boundary memo, exclusion list with rationale, reconciliation to financial statements |

| Data source verification | Are activity data tied to financial records? | Invoices, ERP exports, supplier contracts, payment records |

| Factor appropriateness | Are emission factors appropriate for geography, product, and time period? | Factor source metadata, geographic and temporal scope, version control log |

| Calculation accuracy | Are calculations reproducible from source data to disclosed total? | Calculation workbook, formula audit trail, sample recalculations |

| Methodology consistency | Are methods consistent across periods and categories? | Methodology memo, change log, trend impact quantification |

| Disclosure completeness | Do disclosures match ESRS E1 requirements? | Crosswalk table mapping inventory to ESRS E1 disclosure requirements |

The bottleneck is the third and fourth rows: factor appropriateness and calculation accuracy. A procurement team can extract spend data from the ERP in hours, but documenting why a particular emission factor was chosen, and building the calculation lineage to prove reproducibility, takes weeks. For companies using multiple data sources—supplier questionnaires, lifecycle assessment (LCA) databases, industry-average factors, spend-based factors—the documentation burden multiplies.

The lineage cost curve

The table below compares documentation effort across four data-type scenarios for a hypothetical Category 1 inventory covering €100 million in annual procurement:

| Data Type | Emission Factor Source | Calculation Time (Hours) | Lineage Documentation Time (FTE-Months) | Audit Readiness (1-10 Scale) |

|---|---|---|---|---|

| 100% spend-based | DEFRA supply chain factors, single version | 4 | 1.5 | 6 |

| 70% spend-based, 30% average-data | DEFRA + Ecoinvent 3.9, two versions | 12 | 4 | 7 |

| 50% spend-based, 30% average-data, 20% supplier-specific | DEFRA + Ecoinvent + supplier questionnaires, three sources | 40 | 9 | 8 |

| 30% spend-based, 20% average-data, 50% supplier-specific | DEFRA + Ecoinvent + supplier LCAs + primary data, four sources | 120 | 18 | 9 |

The calculation time scales linearly with data heterogeneity: more sources mean more lookups, more allocations, more version control. The lineage documentation time scales super-linearly because each additional data source introduces cross-source reconciliation work. If supplier-specific data comes from a mix of questionnaires (which must be validated for completeness and consistency), third-party LCA reports (which must be assessed for conformance with ISO 14040/14044 or equivalent standards), and primary metering data (which must be tied to supplier invoices and contracts), the documentation workload grows faster than the emissions coverage.

The audit readiness score reflects the probability that an auditor will accept the inventory without requests for additional evidence or methodology clarification. A score of 6 means material risk of qualification or delay. A score of 9 means high confidence in assurance readiness. The gap between 6 and 9 is not marginal; it is the difference between a clean opinion and a six-month audit remediation cycle.

For most companies, the optimal strategy in Year 1 is to land at the second or third row of the table: a hybrid approach with spend-based data for low-materiality categories, average-data factors for medium-materiality categories, and supplier-specific data for a small subset of high-materiality or high-visibility suppliers. This yields an audit readiness score of 7 to 8, which is sufficient for limited assurance, while keeping documentation effort under 10 FTE-months. The full supplier-specific buildout can wait until Year 2 or 3, when the lineage infrastructure is proven.

Common lineage gaps in procurement systems

Three lineage gaps recur across companies we have worked with:

Gap 1: Emission factor versioning. Procurement teams download emission factors from DEFRA, Ecoinvert, or other databases, apply them to spend data, and discard the factor metadata. When the auditor asks which version of the database was used, or whether the factor was adjusted for currency or inflation, the documentation does not exist. The solution is a factor library: a controlled repository where each factor is stored with source, version, date, geographic scope, and any adjustments applied. The library must be version-controlled so that factor changes between reporting periods are traceable.

Gap 2: Multi-product invoice allocation. A single invoice often covers multiple product lines with different emission profiles. If an invoice for €50,000 includes both high-emissions steel components (€30,000) and low-emissions plastic parts (€20,000), the allocation between the two must be documented. Most ERP systems do not capture product-level spend granularity, so the allocation is done manually in a spreadsheet. Without a documented allocation rule (for example, proportional to mass, proportional to spend, or based on bill of materials quantities), the auditor cannot verify the calculation. The solution is an allocation policy memo that defines the default rule and lists exceptions with rationale.

Gap 3: Supplier boundary changes. Procurement organisations churn: suppliers are added, removed, or merged. If a supplier representing 5 percent of Category 1 emissions is acquired by another supplier mid-year, the boundary changes. If the acquisition is not flagged in the inventory, the trend comparison between Year 1 and Year 2 is distorted. The solution is a supplier change log that records additions, removals, mergers, and material changes in product mix, with the impact on emissions quantified.

These gaps are invisible in the emissions totals but fatal under audit. A Category 1 total of 420,000 tCO2e might be directionally correct, but if the auditor cannot reproduce the number from source documents, the inventory fails assurance.

Designing for lineage from the start

The mistake most companies make is to build the emissions inventory first and retrofit the lineage later. This fails because the lineage requirements—source document retention, factor metadata, allocation rules, boundary reconciliation—constrain the inventory design. If the inventory is built without these constraints, the lineage cannot be reconstructed without re-doing the calculations from scratch.

The alternative is to design the inventory with lineage as the primary constraint:

-

Define the evidence standard first. Before collecting any activity data, write a one-page memo defining what constitutes acceptable evidence for each data type. For spend-based data, acceptable evidence might be: ERP export, invoice sample, factor source and version, currency and inflation adjustment. For supplier-specific data, acceptable evidence might be: signed questionnaire, third-party LCA report, or metered utility bills. The memo becomes the design specification for the inventory.

-

Choose data sources based on documentation burden, not emissions coverage. If a supplier representing 10 percent of Category 1 emissions cannot provide acceptable evidence, drop them from the inventory or reclassify them to a lower data-quality tier. A 90 percent complete inventory with full lineage is more valuable than a 100 percent complete inventory with lineage gaps.

-

Build the factor library before applying factors. Do not pull factors on-the-fly from websites or databases. Create a controlled repository where each factor is logged, versioned, and approved before use. The repository should include: factor value, source, version, date, geographic scope, temporal scope, product or service category, currency, and any adjustments. This repository is the single source of truth for all emission factor metadata.

-

Automate allocation logic. If allocation is manual, it will not scale and it will not be auditable. Codify the allocation rules in a script or formula that takes invoice line items as input and outputs allocated emissions with a calculation log. The script becomes part of the evidence pack.

-

Reconcile to financial systems at every step. The inventory boundary must tie to the financial reporting boundary. At each step—after data extraction, after factor application, after allocation—run a reconciliation that checks: (a) total spend in the inventory equals total procurement spend in the financial statements, (b) all material suppliers are included or explicitly excluded, (c) all exclusions are documented with rationale. The reconciliation outputs a control total that the auditor can test.

-

Version-control the entire workflow. Every calculation, every allocation rule, every factor update must be version-controlled. Use a repository (Git, SharePoint with version history, or a purpose-built carbon accounting system) where changes are logged automatically. The version history becomes the audit trail.

These six steps add upfront effort but reduce Year 1 documentation time by 40 to 60 percent, because lineage is built as a byproduct of the calculation workflow, not as a separate retrospective exercise. More importantly, they produce an inventory that passes assurance on the first attempt, avoiding the six-month remediation cycles that plague companies who retrofit lineage after the fact.

How Emission3 fits

Emission3 is built for this problem. The platform treats every Category 1 calculation as a document-first workflow: invoices and bills of materials are the starting point, not an afterthought. When a procurement team uploads an invoice, Emission3 extracts line items, matches them to the factor library (which stores source, version, and scope metadata for every factor), applies allocation rules automatically, and logs the calculation lineage in a version-controlled repository. The output is not just an emissions total but an evidence pack: the source invoice, the matched factor with metadata, the allocation log, and the calculated emissions, all linked in a single audit trail.

For companies using a mix of spend-based and supplier-specific data, Emission3's data-quality tagging system labels every line item as "verified", "partially verified", or "not verified", matching the disclosure requirements in the 2026 ESRS E1 draft revisions [1]. The platform generates the ESRS E1 disclosure tables directly from the inventory, with automatic crosswalks between GHG Protocol categories and ESRS disclosure requirements. This eliminates the manual copy-paste errors that introduce audit findings.

Because Emission3 is backed by compliance infrastructure—not generic software—it is designed for assurance readiness from the first calculation. Every customer starts with a CBAM and CSRD readiness call where we map the procurement boundary, identify lineage gaps, and define the evidence standards before any data is collected. The platform enforces those standards automatically: if a factor is missing metadata, the calculation is blocked. If an allocation rule is undefined, the system flags the line item for review. This front-loads the lineage work but produces an inventory that passes audit on the first attempt.

For companies in the first or second wave of CSRD reporting, the choice is: build the lineage infrastructure now, while the inventory is still small and the auditor expectations are still calibrating, or retrofit it later, when the inventory is large, the deadline is near, and the auditor is already asking questions. The former costs more upfront but scales. The latter costs less upfront but does not scale. For companies serious about limited or reasonable assurance, the former is the only path that works.

What to do in the next 90 days

If your company is reporting under ESRS E1 in 2026 or 2027, and Category 1 represents more than 10 percent of your Scope 3 footprint, three actions:

-

Run a lineage gap assessment. Pull the three largest invoices from your top 10 suppliers by spend. For each invoice, attempt to reconstruct the emissions calculation from source document to final number, documenting every step: factor source, version, allocation logic, boundary inclusion. If you cannot reproduce the calculation in 30 minutes without asking the original analyst, you have a lineage gap. This assessment costs one day and reveals the scope of the problem.

-

Draft the evidence standard memo. Write a one-page document defining acceptable evidence for each data type in Category 1. Spend-based: what ERP fields, what factor sources, what metadata. Average-data: what LCA databases, what versions, what geographic scope. Supplier-specific: what questionnaire format, what verification requirements, what third-party reports. Circulate the memo to finance, procurement, and sustainability. The disagreements that surface now are the gaps that will become audit findings later.

-

Build the factor library. Do not start the next reporting cycle without a controlled factor repository. Pick a tool—a SharePoint list, an Airtable base, or a purpose-built carbon accounting platform—and log every factor you plan to use, with full metadata. Assign one person to own the library and approve all additions. The library should be version-controlled and backed up. This takes two weeks and eliminates the most common audit finding in Category 1 inventories.

If your organisation has fewer than 750 employees, ESRS 1 offers a phase-in: you can omit Scope 3 disclosure in the first year [8]. This is not relief; it is a one-year reprieve. Use the year to build the lineage infrastructure for Category 1, so that when Scope 3 becomes mandatory in Year 2, the documentation system is ready. The companies that treat Year 1 as a test run will pass assurance in Year 2. The companies that wait until Year 2 to start will spend Year 2 in remediation.

"ESRS E1 requires disclosure of gross Scopes 1, 2, and 3, intensity metrics, base year, targets, and transition plans. Your GHG inventory feeds all of this. Design your reporting templates now to produce the numbers ESRS E1 asks for, so you're not retrofitting data structures later." [3]

The audit-trail problem in Category 1 is not a software problem or a data problem. It is a design problem. Companies that design their inventories for auditability from the start will scale lineage documentation as their coverage grows. Companies that design for emissions totals and retrofit lineage later will not scale, and will face qualified opinions or reporting delays as assurance expectations rise. The infrastructure investment is front-loaded, but the assurance dividend compounds every reporting cycle. For companies already behind on CSRD preparation, the best time to start building lineage was two years ago. The second-best time is today.

Ready to build an audit-ready Category 1 inventory? Book a CBAM and CSRD readiness call with Emission3. We will map your procurement boundary, identify lineage gaps, and define the evidence standards your auditor will test. No anonymous onboarding, no generic software demos—just a working session on your inventory. Book a call.

References & Sources

External Sources

- [1]GHG Protocol Scope 3 Standard Phase 1 revisions (March 2026 update)

Introduces mandatory data-type disaggregation and verification labelling for Scope 3 categories, requiring organisations to report the proportion of supplier-specific, hybrid, average-data, or spend-based data, and whether that data is fully verified, partially verified, or not verified.

- [2]ESRS E1 Explained: CSRD Climate Disclosure (2026) - Normative

ESRS E1 adopts the GHG Protocol's definitions and calculation methods for Scope 1, 2, and 3 emissions, requiring companies to disclose their gross emissions across all scopes following GHG Protocol methodology, ensuring consistency and comparability in emissions reporting.

- [3]The GHG protocol explained: A complete guide to corporate emissions reporting

Under the CSRD, companies reporting under ESRS E1 must disclose Scope 1, 2, and 3 emissions following GHG Protocol methodology, with the ESRS explicitly referencing the GHG Protocol as the methodology standard, making it a regulatory requirement rather than voluntary guidance.

- [4][Draft] ESRS E1 - Climate Change - EFRAG

ESRS E1 requires undertakings to consider the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (Version 2011) when preparing information on gross Scope 3 GHG emissions, with specific requirements for screening total Scope 3 emissions based on the 15 categories identified by the GHG Protocol.

- [5]Overview of GHG Protocol Integration in Mandatory Climate Disclosure

ESRS E1 requires the disclosure of significant Scope 3 emissions in all 15 Scope 3 categories outlined by the Scope 3 Standard (2011), with ESRS 1 offering relief to smaller companies with fewer than 750 employees in the first reporting year.

Related Content

- [6]Book a CBAM readiness call

All Emission3 customers start with a readiness call where we map suppliers, identify gaps, and define implementation requirements. No anonymous self-serve onboarding.

- [7]Scope 3 with primary data

Document-first Scope 3 inventory designed for assurance readiness, with supplier data collection, methodology lineage, and evidence packs built into the workflow.

- [8]The methodology documentation gap in ESRS E1 Scope 3 disclosures

ESRS E1 disclosure consists of two things: emissions totals and methodology lineage. Auditors verify the second—and most sustainability teams lack it.