The default-value penalty in CBAM certificate costs for non-EU exporters

The default-value penalty in CBAM certificate costs for non-EU exporters

Here's the issue: starting January 2026, CBAM imposes a direct financial obligation on EU importers—and by extension, on non-EU exporters whose goods cross the border. Most exporters assume that reporting embedded emissions is the core compliance burden. They calculate a carbon intensity figure, submit it to the importer, and consider the obligation discharged. The importer purchases CBAM certificates at the prevailing EU ETS price, multiplied by the declared tonnes of CO₂. At €75 per tonne, a steel exporter shipping 100,000 tonnes annually with 2 tonnes CO₂ per tonne of product faces €15 million in certificate costs. That arithmetic looks straightforward.

However, the CBAM filing consists of two things: the embedded emissions total and the method by which that total was determined—actual installation-level data or country-specific default values.

Embedded emissions on their own have no cost advantage. The methodology is what the importer pays for—or overpays for. From 2026, the European Commission applies a mark-up to default values: 10% in 2026, 20% in 2027, and 30% from 2028 onwards[1]. If an exporter relies on default values because they lack metered installation data, the importer must purchase certificates for the inflated figure. The exporter's actual emissions become irrelevant; the certificate cost is calculated on the penalized default.

While installation-level monitoring has become more accessible—utility meters, process data, and third-party verification systems are widely available—the administrative gap has become more expensive. A typical Indian steel exporter using default values for 100,000 tonnes annually could incur excess CBAM certificate costs of €1.2–2.8 million per year compared to actual emissions monitoring[2]. By 2028, that penalty scales to 30%, compounding with EU ETS price evolution. If the exporter invests €200,000–500,000 upfront in measurement infrastructure and €50,000–150,000 annually in verification, the payback period is 6–18 months for medium to large facilities[2]. The arithmetic inverts: delaying the monitoring investment becomes more expensive than the capital outlay.

How do you solve this? I think the operators we work with treat CBAM as an installation-visibility problem, not an emissions-reporting problem. The first quarterly CBAM reports in 2024 revealed that most exporters could calculate a carbon intensity figure but could not trace it back to metered fuel consumption, electricity invoices, or process-specific data at the installation level. The EU methodology requires a top-down flow: total installation emissions monitored according to the EU ETS Monitoring and Reporting Regulation, then attributed to production processes, then converted to specific embedded emissions for the goods produced[1]. Without that lineage, the importer has no basis to claim actual values, and the default-value penalty applies automatically. For now, the most pragmatic path is to begin installation-level monitoring in Q1 2026, establish a verifier relationship before the first full-year filing in August 2027, and treat the 2026 reporting cycle as a dry run for verification readiness.

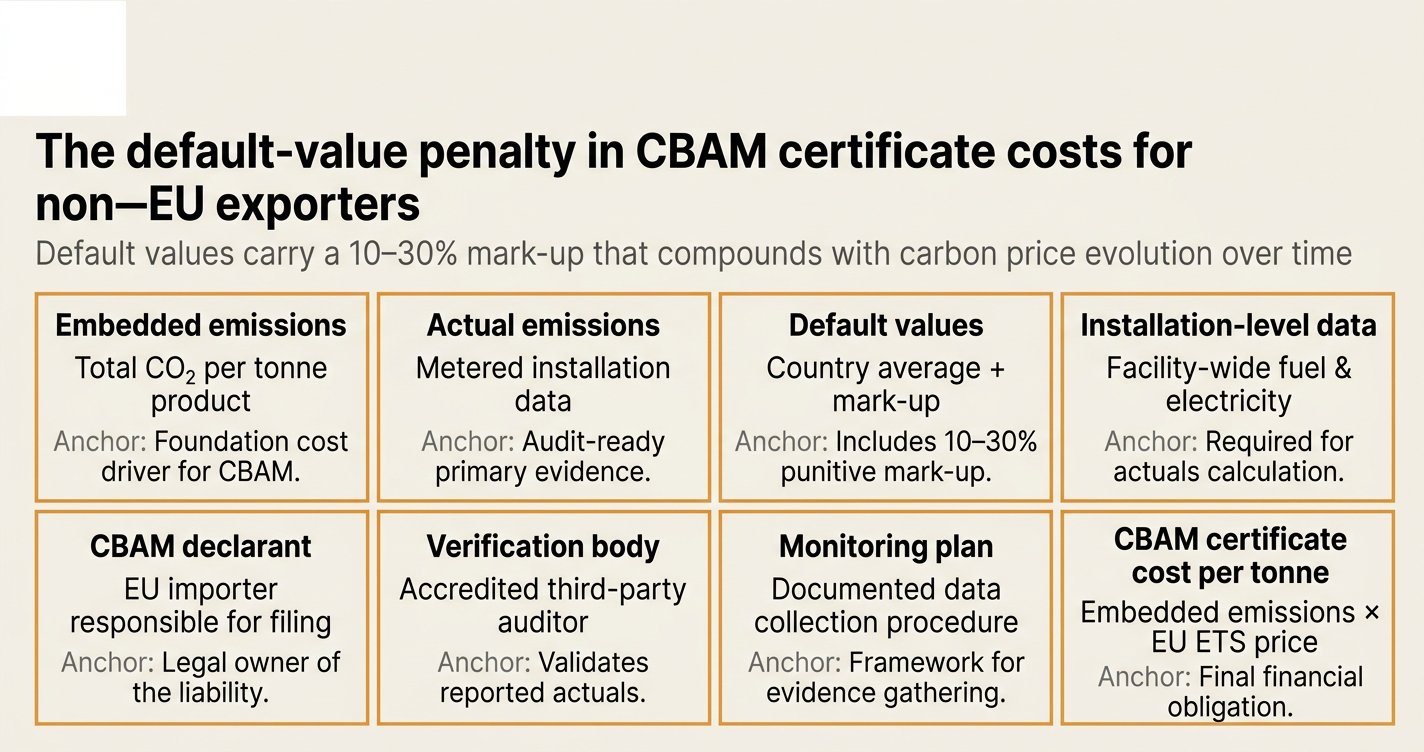

The shape of the argument, visualized below.

The CBAM default-value lexicon: eight terms that determine your certificate cost

Every CBAM audit will hinge on a handful of regulatory terms. Most exporters hear these phrases in importer emails, regulator guidance, or verifier intake calls—but few have seen them defined in plain English with worked examples. Below are eight terms that will appear in your first verification cycle, each with a definition, a calculation example, and the source regulation.

1. Embedded emissions

The total greenhouse gas emissions released during the production of a good, measured in tonnes of CO₂ equivalent per tonne of product. Embedded emissions include direct emissions from the installation (Scope 1) and indirect emissions from purchased electricity (Scope 2), attributed to the specific goods covered by CBAM[1].

Worked example: A steel mill in India produces 50,000 tonnes of hot-rolled coil in 2026. The installation emits 80,000 tonnes of CO₂ from coal combustion and consumes 120,000 MWh of grid electricity with an emission factor of 0.82 tonnes CO₂ per MWh. Direct emissions: 80,000 tonnes. Indirect emissions: 120,000 × 0.82 = 98,400 tonnes. Total installation emissions: 178,400 tonnes. Embedded emissions per tonne of product: 178,400 ÷ 50,000 = 3.57 tonnes CO₂ per tonne of steel.

Source regulation: Commission Implementing Regulation (EU) 2025/2547, Annex IV, Section 2.

2. Actual emissions

Emissions values derived from metered, installation-specific data that reflect the real production conditions at the facility. Actual emissions must be monitored according to the EU ETS Monitoring and Reporting Regulation, calculated at the installation level, attributed to production processes, and verified by an accredited third party[1].

Worked example: The Indian steel mill above installs fuel flow meters on blast furnaces and receives monthly utility bills showing grid electricity consumption. The mill's emissions report documents 178,400 tonnes of CO₂ for 2026, traced to meter readings and invoices. A verifier confirms the calculation methodology and issues a verification opinion. The importer can report 3.57 tonnes CO₂ per tonne of steel as an actual value—no mark-up applies.

Source regulation: Commission Implementing Regulation (EU) 2025/2547, Article 7.

3. Default values

Country- and product-specific average emission intensities set by the European Commission, used when an importer cannot obtain verified actual emissions from the exporter. Default values are calculated as the average emissions intensity of production in the country of origin, increased by a mark-up[3].

Worked example: The default value for hot-rolled coil from India is 2.8 tonnes CO₂ per tonne of product (Commission Implementing Regulation (EU) 2025/2621, Annex). In 2026, the mark-up is 10%, so the default value becomes 2.8 × 1.10 = 3.08 tonnes CO₂ per tonne. If the mill's actual emissions are 3.57 tonnes, the default value would reduce the certificate cost—but if the mill's actual emissions are 2.2 tonnes, the default value inflates the certificate requirement by 40%.

Source regulation: Commission Implementing Regulation (EU) 2025/2621, Article 2.

4. Installation-level data

The total emissions and production data collected at the physical facility where the CBAM goods are manufactured. Installation-level data is the starting point for CBAM calculations: total fuel consumption, electricity use, and process emissions are measured at the installation, then allocated to individual production processes and goods[1].

Worked example: The steel mill operates a blast furnace, a basic oxygen furnace, and a hot-rolling line on a single site. The installation-level data includes: coal input to the blast furnace (35,000 tonnes), natural gas to the reheat furnace (4 million m³), and grid electricity to the rolling mill (120,000 MWh). These inputs are converted to CO₂ emissions using IPCC emission factors, then attributed to the production of 50,000 tonnes of hot-rolled coil.

Source regulation: Commission Implementing Regulation (EU) 2025/2547, Article 6.

5. CBAM declarant

The EU importer authorized to submit CBAM declarations and surrender CBAM certificates. The declarant is legally responsible for the accuracy of the emissions data reported, whether that data is based on actual values from the exporter or default values[4].

Worked example: A German steel distributor imports 10,000 tonnes of hot-rolled coil from India in February 2026. The distributor is the CBAM declarant. By August 2027, the declarant must submit an annual CBAM declaration covering all 2026 imports, including the embedded emissions per tonne and the quantity of CBAM certificates to be surrendered. If the exporter did not provide verified actual emissions, the declarant must use the default value plus mark-up.

Source regulation: Regulation (EU) 2023/956, Article 5.

6. Verification body

An independent, accredited organization that reviews the exporter's emissions monitoring plan and emissions report, confirms that the data aligns with EU ETS standards, and issues a verification opinion. Verification is mandatory for actual emissions data; default values do not require verification[1].

Worked example: The Indian steel mill hires an ISO 14065-accredited verifier in Q4 2026. The verifier conducts a site visit, reviews fuel invoices and meter calibration records, recalculates a sample of emissions using the mill's stated methodology, and issues a verification report in January 2027. The importer attaches this report to the August 2027 CBAM declaration to substantiate the use of actual emissions.

Source regulation: Commission Implementing Regulation (EU) 2025/2546, Article 3.

7. Monitoring plan

A documented procedure that defines how the exporter will collect emissions data at the installation level, which meters and invoices will serve as evidence, which emission factors will be applied, and how emissions will be attributed to specific goods. The monitoring plan must be approved by the verifier before the reporting period begins[1].

Worked example: The steel mill drafts a monitoring plan in January 2026. The plan specifies: coal input will be measured by weigh-belt feeders at the blast furnace, natural gas by utility invoices from the gas supplier, and electricity by monthly meter readings. Emission factors are sourced from the IPCC 2006 Guidelines. The plan states that emissions will be attributed to hot-rolled coil based on the mass of steel produced. A verifier reviews the plan and confirms it meets EU ETS standards.

Source regulation: Commission Implementing Regulation (EU) 2025/2547, Article 5.

8. CBAM certificate cost per tonne

The financial obligation incurred by the importer for each tonne of CBAM goods imported, calculated as the embedded emissions per tonne multiplied by the EU ETS allowance price, minus any carbon price already paid in the country of origin, minus any free allocation adjustment. This is the metric that determines whether actual emissions or default values are more cost-effective[6].

Worked example: The German distributor imports 10,000 tonnes of hot-rolled coil in 2026. The exporter provides actual emissions of 2.2 tonnes CO₂ per tonne of steel. The average EU ETS price in 2026 is €80 per tonne of CO₂. No carbon price is paid in India, and the free allocation adjustment is 2.5% of EU benchmark emissions. CBAM certificate cost per tonne: (2.2 - 0) × €80 × (1 - 0.025) = €171.60 per tonne of steel. Total cost for 10,000 tonnes: €1.716 million. If the distributor used the default value of 3.08 tonnes CO₂ per tonne (with the 10% mark-up), the cost would be €239.68 per tonne, or €2.397 million total—a €681,000 penalty.

Source regulation: Regulation (EU) 2023/956, Article 21.

Why the penalty compounds over time

The 10% mark-up in 2026 is a transitional rate. By 2028, the mark-up rises to 30%, and the EU ETS price is projected to reach €99–224 per tonne[6]. For an exporter relying on default values, the certificate cost gap widens in two dimensions: the mark-up percentage increases, and the carbon price per tonne increases. A 2026 penalty of €1.2 million could become a 2034 penalty of €5–8 million for the same export volume, depending on carbon price evolution.

The European Commission designed the mark-up as an incentive mechanism, not a punitive measure. The implicit assumption is that exporters will respond to the financial signal by investing in actual emissions monitoring. However, the incentive only works if the exporter (a) understands the cost arithmetic, (b) has access to measurement infrastructure and verifiers, and (c) begins installation-level monitoring early enough to accumulate a full calendar year of data before the first verification cycle in 2027.

Most exporters we speak to are still operating on the assumption that CBAM is a reporting obligation, not a capital investment decision. They treat the quarterly reports filed during 2024–2025 as administrative paperwork, not as a rehearsal for financial compliance. By the time the importer requests verified actual emissions for the 2027 declaration, the exporter has missed the 12-month monitoring window required to generate a verifiable dataset. At that point, the default-value penalty is unavoidable, and the exporter has locked in three years of inflated certificate costs (2026, 2027, 2028) before actual emissions can take effect in 2029.

The geographic distribution of default-value exposure

The Bipartisan Policy Center highlighted in January 2025 that US-assigned default values for iron and steel goods are not consistent with existing US government estimates and are consistently higher than the estimates reported by the International Trade Commission[3]. This means that US steel exporters face an artificial certificate cost premium even if their installations operate more efficiently than the US average.

The issue is more acute for exporters in China and India, where default values are set at the country average emissions intensity—which can be 2–5 times higher than the emissions of modern, efficient installations. A Chinese steel mill operating a new blast furnace with waste-heat recovery and high-grade coking coal might emit 1.8 tonnes CO₂ per tonne of steel, but the default value for China is 3.2 tonnes CO₂ per tonne (before the mark-up). The certificate cost gap for that exporter is 78% higher than it should be.

The only exporters insulated from this penalty are those in countries where the national average emissions intensity is lower than the installation's actual emissions. In that scenario, the default value (even with the mark-up) is cheaper than actual monitoring. But this is a rare configuration: most exporters who operate efficiently relative to their domestic peers will pay a penalty by using default values.

What verification requires in practice

Verification of actual emissions is not a box-ticking exercise. The verifier's role is to confirm that the exporter's emissions report is reproducible from source documents, that the methodology aligns with EU ETS standards, and that the data quality is sufficient for assurance. This means the verifier will:

- Conduct a site visit to inspect meters, calibration records, and process equipment.

- Review fuel invoices, electricity bills, and process data logs for a sample period.

- Recalculate emissions for the sample period using the exporter's stated methodology and emission factors.

- Compare the recalculated emissions to the reported emissions and investigate any discrepancies.

- Issue a verification opinion stating whether the emissions report is free from material misstatement[1].

If the exporter cannot produce meter readings, invoices, or a documented calculation methodology, the verifier cannot issue a positive opinion, and the importer cannot claim actual emissions. The default-value penalty applies by default.

The verification timeline is critical. Most verifiers require 6–8 weeks to complete a site visit, data review, and opinion drafting. If the exporter waits until December 2026 to engage a verifier, the opinion will not be ready by the importer's August 2027 filing deadline. The exporter must begin the verification process no later than Q4 2026 to allow time for document collection, site visits, and any corrective actions.

The procurement conversation: who pays the penalty?

The CBAM certificate cost is legally borne by the EU importer, but the economic incidence is negotiable. If the exporter's contract with the importer is CIF (cost, insurance, and freight), the importer pays the certificate cost on top of the purchase price. If the contract is DDP (delivered duty paid), the exporter is responsible for all import costs, including CBAM certificates.

In practice, most procurement contracts written before 2024 do not explicitly allocate CBAM certificate costs. This creates a negotiation gap: the importer will push to renegotiate the purchase price downward by the amount of the certificate cost, or the importer will demand that the exporter provide verified actual emissions to minimize the certificate requirement. If the exporter cannot provide actual emissions, the importer will either absorb the default-value penalty (reducing margins) or pass it back to the exporter through a lower purchase price.

For an exporter shipping 100,000 tonnes annually with a default-value penalty of €1.2 million, the importer will typically reduce the purchase price by €12 per tonne to offset the penalty. This is a permanent margin erosion: every year the exporter delays actual emissions monitoring, they lose €12 per tonne in revenue.

How Emission3 fits

Emission3 treats CBAM compliance as an installation-data problem, not a carbon accounting problem. Our platform starts with the documents that already exist at the installation level—fuel invoices, utility bills, meter readings, and bills of material—and converts them into audit-grade evidence for CBAM filings. Every emissions number is reproducible from source documents, and every calculation includes a full lineage from input data to declared emissions.

For non-EU exporters, we provide:

- Document ingestion: Upload fuel invoices, electricity bills, and process data logs. Emission3 extracts quantities, units, and emission factors automatically, with human review of ambiguous fields.

- Installation-level attribution: Map total installation emissions to production processes and specific goods using mass balance, energy balance, or direct metering.

- Verification-ready outputs: Generate emissions reports, calculation lineage, and evidence packs that align with EU ETS Monitoring and Reporting Regulation standards. Verifiers receive pre-formatted documentation that reduces site visit time by 40–60%.

- Default-value comparison: For each product, Emission3 calculates the CBAM certificate cost using actual emissions and default values (including the mark-up), then quantifies the financial difference. This gives exporters a clear business case for monitoring investment[5].

Our infrastructure is already built—most exporters can move from first document upload to a verifier-ready emissions report in 3–6 weeks, depending on data availability. For exporters starting installation-level monitoring in Q1 2026, that timeline allows a full calendar year of data collection before the first verification cycle in late 2026.

If you're a non-EU exporter facing the default-value penalty, start with a CBAM readiness call. We'll map your installations, identify document gaps, estimate your certificate cost under actual versus default scenarios, and outline a verification timeline. No anonymous self-serve onboarding—every customer begins with a structured conversation about their specific supply chain and compliance obligations[8].

Closing

The default-value penalty is not a reporting quirk; it's a compounding financial obligation that scales with export volumes, mark-up percentages, and EU ETS price evolution. Exporters who treat CBAM as a carbon accounting exercise will discover in 2027 that they've locked in three years of inflated certificate costs. The exporters who treat CBAM as an installation-visibility exercise—investing in monitoring infrastructure, engaging verifiers early, and building a document lineage from meter readings to declared emissions—will reduce their certificate cost per tonne by 15–40% relative to default values.

The choice is not whether to comply with CBAM; the choice is whether to pay the penalty or invest in the monitoring infrastructure that eliminates it. For most medium to large exporters, the payback period for that investment is measured in months, not years.

Book a CBAM readiness call to map your installation data, estimate your default-value penalty, and build a verification timeline for 2026[8].

References & Sources

External Sources

- [1]EU CBAM Emissions Data: Monitoring, Reporting & Verification

Overview of CBAM monitoring methodologies, actual values versus default values, and the top-down calculation approach from installation to product level.

- [2]CBAM Default Values vs Actual Data: Cost Analysis for Exporters

Quantified comparison of default-value penalties versus actual emissions monitoring costs, including capital investment and payback periods for Indian steel exporters.

- [3]How the EU's New Default Emissions Values Under CBAM Impact US Exporters

Analysis of default-value mark-up incentives and the Bipartisan Policy Center report on inflated default values for US iron and steel products.

- [4]How to collect supplier emissions data for CBAM compliance (step-by-step guide)

Practical guidance on supplier data collection, enforcement risks, and the transition from transitional to definitive CBAM reporting requirements.

- [6]CBAM Benchmarks and Default Values Leaked – How Actual CBAM Data Matters

Analysis of leaked CBAM benchmarks and default values, with quantified certificate cost projections for 2026 and 2034 under actual versus default scenarios.

Related Content

- [5]How Emission3 handles CBAM

Emission3's document-first approach to CBAM compliance: installation-level data ingestion, verification-ready outputs, and default-value comparison for certificate cost optimization.

- [7]The 2026 CBAM verification timeline problem for non-EU exporters

Emission3 analysis of the 12-month monitoring window required for verification readiness and the cost consequences of delayed preparation.

- [8]Book a CBAM readiness call

All Emission3 customers start with a CBAM readiness call: we map installations, identify document gaps, and build a verification timeline specific to your supply chain.