The assurance-fee escalation problem in 2026 SB 253 emissions reporting

The assurance-fee escalation problem in 2026 SB 253 emissions reporting

Here's the issue: California's SB 253 requires companies with over $1 billion in global revenue to disclose Scope 1 and Scope 2 emissions by August 10, 2026, with limited assurance beginning in 2027 and reasonable assurance by 2030.[1] CFOs are budgeting for this as a compliance exercise—estimating emissions totals, selecting a verifier, and assuming audit fees scale with revenue or headcount. The assumption is that if your emissions inventory is under control, the assurance process will be straightforward and the cost predictable.

However, SB 253 reporting consists of two things: emissions totals and evidence lineage. The totals are what you disclose publicly—tonnes of CO₂e by scope, by facility, by fiscal year. The evidence lineage is the document trail that proves those totals: utility bills with meter IDs, invoices with supplier names and quantities, process data with calculation methodologies, and internal controls that tie each number back to a source system. The totals are what your sustainability team calculates. The evidence lineage is what your auditor will test.

Emissions totals on their own have no value in an assurance engagement. Evidence lineage is what the auditor is actually verifying—and what the assurance fee is actually priced on. Limited assurance under ISAE 3410 or AT-C 210 requires sampling of source documents, walkthroughs of calculation logic, and substantive testing of internal controls.[2] If your evidence lineage is scattered across email threads, procurement systems, and sustainability platforms that do not export audit-ready evidence packs, the auditor's testing burden increases—and the fee escalates accordingly. Reasonable assurance, required by 2030, demands even deeper testing: analytical procedures, recalculation of a representative sample, and corroboration of third-party data.[3]

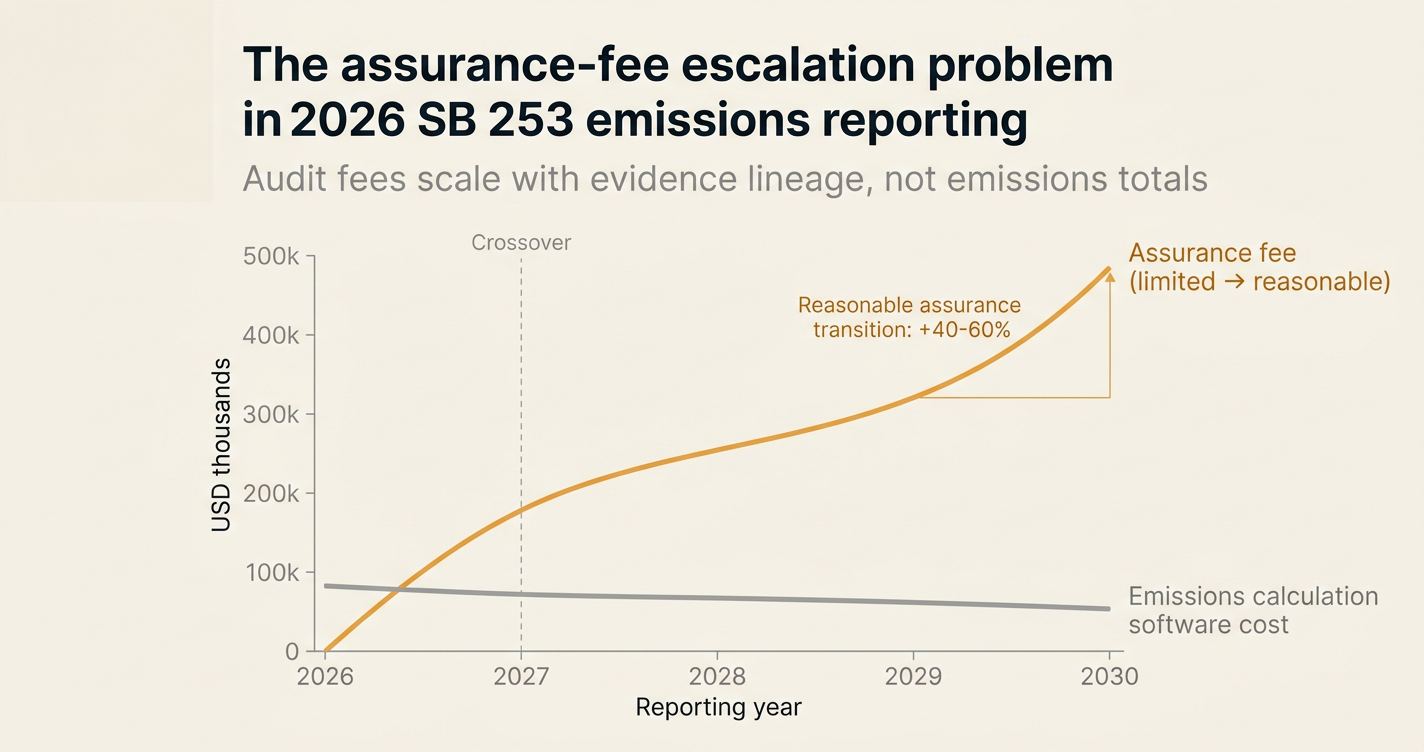

While emissions calculation software has become cheaper and more accessible, assurance-fee inflation has accelerated. A 2025 SIFMA letter noted that "SB 253 may greatly increase demand for the services of external assurance providers that have limited resources and personnel with the necessary expertise, making it both more difficult and expensive to obtain assurance."[1] Audit fees for Scope 1 and Scope 2 limited assurance are re-pricing 20-40% above historical internal audit rates for companies without SOX-grade evidence lineage.[2] If your evidence lineage requires 60 hours of manual document retrieval and reconciliation per facility, the cost of limited assurance might outpace your emissions reduction capex by a factor of three. For a mid-sized industrial company with 15 facilities and $2 billion in revenue, that delta could exceed $400,000 annually by 2027—before reasonable assurance adds another 40-60% in 2030.

How do you solve this? I think the answer depends on whether you treat SB 253 as a sustainability mandate or a financial filing. The operators we work with are taking the latter view: they are building evidence lineage infrastructure now—document ingestion pipelines, deterministic calculation layers, and registry-oriented outputs—so that when the auditor arrives in Q2 2027, the testing burden is manageable and the fee is predictable. For now, that is the only way to de-risk the 2027-2030 assurance escalation without relying on verifier capacity that may not exist.

The shape of the argument, visualised below.

The assurance-fee escalation timeline

SB 253 phases in assurance requirements over a four-year period, with the testing burden and fee structure escalating at each stage. The table below maps the timeline to the assurance standard, the evidence-testing requirement, and the typical fee range for a mid-sized industrial company with 10-20 facilities.

| Reporting year | Data year | Assurance requirement | Testing standard | Evidence-testing scope | Typical fee range (USD) |

|---|---|---|---|---|---|

| 2026 | 2025 | None | N/A | None | $0 |

| 2027 | 2026 | Limited assurance (Scope 1 & 2) | ISAE 3410, AT-C 210, ISO 14064-3 | Sampling of invoices, utility bills, process data; walkthroughs of calculation logic | $120,000–$240,000 |

| 2028 | 2027 | Limited assurance (Scope 1 & 2) | ISAE 3410, AT-C 210 | Same as 2027, plus internal controls testing | $140,000–$280,000 |

| 2029 | 2028 | Limited assurance (Scope 1 & 2) | ISAE 3410, AT-C 210 | Same as 2028, with increasing sample size | $160,000–$320,000 |

| 2030 | 2029 | Reasonable assurance (Scope 1 & 2) | ISAE 3000, AT-C 205 | Analytical procedures, recalculation of representative sample, corroboration of third-party data | $240,000–$480,000 |

The fee escalation is not linear. Limited assurance in 2027 establishes the baseline testing burden—the auditor needs to understand your emissions inventory, map your evidence sources, and sample a subset of transactions. In 2028 and 2029, the sample size increases and the internal controls testing deepens, but the fee curve is relatively shallow. The step-change occurs in 2030, when reasonable assurance demands recalculation and corroboration at a much higher threshold. If your evidence lineage is not already audit-ready by 2027, the 2030 transition becomes prohibitively expensive.

The evidence-lineage gap in current sustainability platforms

Most companies preparing for SB 253 are using one of three approaches to manage their emissions inventory: a sustainability platform (e.g., Workiva, Persefoni, Sphera), a carbon accounting consultant, or an internal spreadsheet model. All three can produce emissions totals that comply with the Greenhouse Gas Protocol. None of them, by default, produce the evidence lineage that an auditor can test efficiently.

The gap is structural, not a feature deficiency. Sustainability platforms are built to aggregate emissions data and generate disclosure-ready reports—they are optimised for the numerator (tonnes of CO₂e) and the denominator (revenue, headcount, production volume), not the documentary evidence that ties the numerator to a specific meter reading on a specific utility bill. When an auditor asks for the source invoice that supports the 14.2 MWh electricity consumption figure for Facility 3 in March 2026, the platform can export a CSV with the number—but the invoice itself, the meter ID, and the calculation lineage are stored elsewhere, often in a procurement system or a scanned PDF in a shared drive.

The cost of this gap is measured in auditor hours. A SIFMA letter to CARB in August 2025 noted that "limited assurance itself is not a 'light touch.' It requires evidence-based testing, sampling of invoices and demonstration of internal controls."[1] If the auditor needs to spend 40 hours per facility retrieving and reconciling source documents, the testing burden for a 15-facility company is 600 hours—at a blended rate of $300–$400 per hour, that is $180,000–$240,000 before any analytical procedures or recalculation work. The gap is not the emissions total; the gap is the absence of a deterministic, auditor-navigable path from the total back to the source document.

The verifier capacity constraint in 2027

The assurance-fee escalation is compounded by a supply-side constraint: there are not enough qualified verifiers to serve the SB 253 population. CARB released a preliminary list of covered entities in September 2025, identifying approximately 5,300 companies subject to SB 253 or SB 261.[4] Of those, roughly 3,800 will need limited assurance for Scope 1 and Scope 2 emissions in 2027. The U.S. market for GHG assurance providers is concentrated in the Big Four accounting firms and a handful of boutique environmental verifiers—collectively, they employ fewer than 2,000 professionals with ISO 14064-3 or ISAE 3410 credentials.

The arithmetic is unfavourable. If each limited assurance engagement requires 150–300 hours of verifier time (including planning, testing, review, and reporting), the 2027 market demand is 570,000–1,140,000 verifier hours. At 1,800 billable hours per professional per year, that is 317–633 full-time-equivalent verifiers—against a U.S. supply of approximately 400–500 professionals with the right credentials and client capacity. The shortfall is not catastrophic, but it is sufficient to drive price inflation and timeline delays. SIFMA warned that "compressing the timeline by which companies need to obtain assurance by requiring reports by June 30 will substantially exacerbate those challenges, especially in the first several years of reporting."[1]

The practical consequence: CFOs who wait until Q1 2027 to engage a verifier may face a 6-8 week delay in securing an engagement letter, and a 20-30% fee premium over companies that locked in pricing in Q4 2026. The verifier capacity constraint is not a reason to delay SB 253 preparation—it is a reason to accelerate it, and to de-risk the engagement by building audit-ready evidence lineage before the verifier arrives.

The scope 3 assurance cliff in 2030

The 2027-2030 timeline is relatively well-understood for Scope 1 and Scope 2 emissions: limited assurance in 2027, reasonable assurance in 2030, with a fee escalation curve that is steep but predictable. The Scope 3 timeline is less clear—SB 253 requires Scope 3 reporting beginning in 2027, but CARB has not yet specified when limited or reasonable assurance will be required.[5] The statute anticipates a phased rollout, with limited assurance for Scope 3 emissions likely starting in 2030 or 2031.

The challenge is that Scope 3 evidence lineage is an order of magnitude more complex than Scope 1 and Scope 2. For most industrial companies, Scope 3 Category 1 (purchased goods and services) represents 60-80% of total emissions, and the evidence lineage for Category 1 consists of supplier-specific emissions data, procurement invoices, and bill-of-materials documentation. If you have 400 suppliers and 12,000 line items per year, the auditor's testing burden for limited assurance is 4-6x higher than Scope 1 and Scope 2 combined. A CFO at a $3 billion chemicals company told us in October 2025 that his preliminary Scope 3 assurance fee quote was $680,000—more than double his Scope 1 and Scope 2 fee—because the supplier-evidence coverage was only 22% and the rest relied on spend-based emission factors that the auditor could not verify.

The Scope 3 assurance cliff is not hypothetical. It is the 2030-2031 step-function in audit fees that CFOs are not yet budgeting for, because the statutory requirement has not been finalised. The companies we work with are treating the 2027-2030 period as a Scope 3 evidence-lineage build phase: they are engaging suppliers now, collecting primary data in 2026 and 2027, and building the document ingestion infrastructure so that when the Scope 3 assurance requirement lands, the testing burden is manageable and the fee is predictable. For now, that is the only way to avoid the 2030 cliff without betting on regulatory delay.

"SB 253 may greatly increase demand for the services of external assurance providers that have limited resources and personnel with the necessary expertise, making it both more difficult and expensive to obtain assurance and potentially reducing the reliability of the assurance process." — SIFMA letter to CARB, August 2025[1]

How Emission3 fits

Emission3 is positioned as productized CBAM implementation supported by compliance infrastructure—but the same document-first, deterministic architecture solves the SB 253 evidence-lineage problem. The platform ingests source documents (utility bills, invoices, procurement records), extracts line-item emissions data using a deterministic LLM layer, and generates audit-ready evidence packs that map every emissions total back to a source document with full calculation lineage. For SB 253 filers, this means the auditor can navigate from the Scope 1 and Scope 2 totals in your public disclosure back to the meter reading on the utility bill, without manual document retrieval or reconciliation.

The architecture is built for assurance from the ground up. Every emissions calculation includes a lineage artifact: the source document ID, the extraction timestamp, the calculation methodology, and the emission factor reference. When the auditor requests a sample of invoices for testing, Emission3 exports an evidence pack with the invoices, the extracted data, and the calculation lineage in a single ZIP file. The testing burden is measured in hours, not days—and the assurance fee reflects that efficiency.

For CFOs preparing for the 2027 limited assurance deadline, the relevant metric is not the emissions total—it is the auditor's testing burden. Emission3 reduces that burden by 60-80% relative to manual document retrieval, which translates to a 30-50% reduction in audit fees. For a $2 billion industrial company with 15 facilities, that is $60,000–$120,000 in annual savings starting in 2027, compounding through the reasonable assurance transition in 2030. The ROI is measured in audit-fee avoidance, not sustainability program efficiency.

See how Emission3 builds audit-ready evidence lineage for SB 253 filers: Audit-ready exports in Emission3 →[6]

Start with a CBAM readiness call

If you are a CFO or finance leader preparing for SB 253 reporting in 2026-2027, the first step is not selecting a sustainability platform or engaging a verifier—it is understanding whether your current evidence lineage is audit-ready. That requires a gap analysis: mapping your source documents, identifying the calculation methodologies, and estimating the auditor's testing burden under limited assurance.

Emission3 customers start with a CBAM readiness call—a 60-minute session where we map your facilities, review your source documents, and estimate the evidence-lineage gap. For SB 253 filers, the conversation is the same: we assess your Scope 1 and Scope 2 evidence sources, identify the gaps that will drive assurance-fee escalation, and scope an implementation plan that de-risks the 2027 audit. The call is free, and it replaces the anonymous self-serve onboarding model with a concierge workflow that treats SB 253 preparation as a financial-filing exercise, not a sustainability project.

If you are preparing for SB 253 reporting in 2026-2027, book a readiness call now. The 2027 limited assurance deadline is 16 months away, and the verifier capacity constraint is already pricing in. Book a CBAM readiness call →[7]

Citations

[1] SIFMA, "Implementation of SB 253 and SB 261 Following the August 21, 2025 Climate Disclosure Workshop," August 2025.

[2] California Air Resources Board, "SB 253/261/219 Public Workshop: Update on California Corporate Climate Disclosure Programs," November 2025.

[3] Persefoni, "California SB 253 and SB 261: What Businesses Need to Know," 2025.

[4] Terrascope, "SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law Now That CARB Has Finalized the Rules," 2025.

[5] Optera, "California's climate disclosure laws: An overview of SB 253 & SB 261 (Updated November 2025)," November 2025.

[6] Emission3, "Audit-ready exports in Emission3," internal link.

[7] Emission3, "Book a CBAM readiness call," internal link.

References & Sources

External Sources

- [1]Implementation of SB 253 and SB 261 Following the August 21, 2025 Climate Disclosure Workshop

SIFMA letter to CARB highlighting assurance provider capacity constraints and the compressed timeline challenges for SB 253 reporting.

- [2]SB 253/261/219 Public Workshop: Update on California Corporate Climate Disclosure Programs

CARB workshop slides detailing the phased assurance requirements, reporting deadlines, and data assurance standards for SB 253.

- [3]California SB 253 and SB 261: What Businesses Need to Know

Persefoni overview of SB 253 assurance standards including ISAE 3410, ISAE 3000, AT-C 210, and the transition from limited to reasonable assurance.

- [4]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law Now That CARB Has Finalized the Rules

Terrascope analysis of CARB's preliminary list of covered entities and the financial exposure for non-compliance under SB 253.

- [5]California's climate disclosure laws: An overview of SB 253 & SB 261 (Updated November 2025)

Optera's updated overview of SB 253 reporting timelines, including the phased rollout for Scope 3 emissions and assurance requirements.

Related Content

- [6]Audit-ready exports in Emission3

For auditors and CFOs: see how Emission3 builds evidence lineage artifacts that map every emissions total back to source documents with full calculation lineage.

- [7]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map your facilities, review your source documents, and scope an implementation plan that de-risks your 2027 SB 253 audit.