The supplier-data verification bottleneck in 2026 CBAM filings

The supplier-data verification bottleneck in 2026 CBAM filings

Here's the issue: from January 1, 2026, every tonne of in-scope goods imported into the EU carries a certificate cost based on embedded emissions. Importers who cannot provide installation-level, verified data from their non-EU suppliers must use default values—which the European Commission has set deliberately high to encourage actual data collection. For most steel, cement, and aluminium exporters, relying on defaults inflates declared emissions by 200% to 500% versus actual production values, directly increasing the CBAM certificate cost per tonne shipped[1]. Procurement teams have spent the last 18 months building supplier engagement programs to collect actual data, assuming that primary data collection is the compliance bottleneck.

However, CBAM filings consist of two things: embedded emissions totals and verified supplier data. The first is what importers declare; the second is what accredited verifiers must certify before the data can be used.

Embedded emissions totals on their own have no value. Verified supplier data is what the EU CBAM Registry and customs authorities are actually asking for, what auditors will review during spot checks, and what determines whether an importer can avoid the default-value penalty. Without third-party verification conducted by an EU-recognised verifier, actual emissions data cannot be submitted in an annual CBAM declaration, and the importer falls back to default values regardless of how much supplier engagement work was done[2].

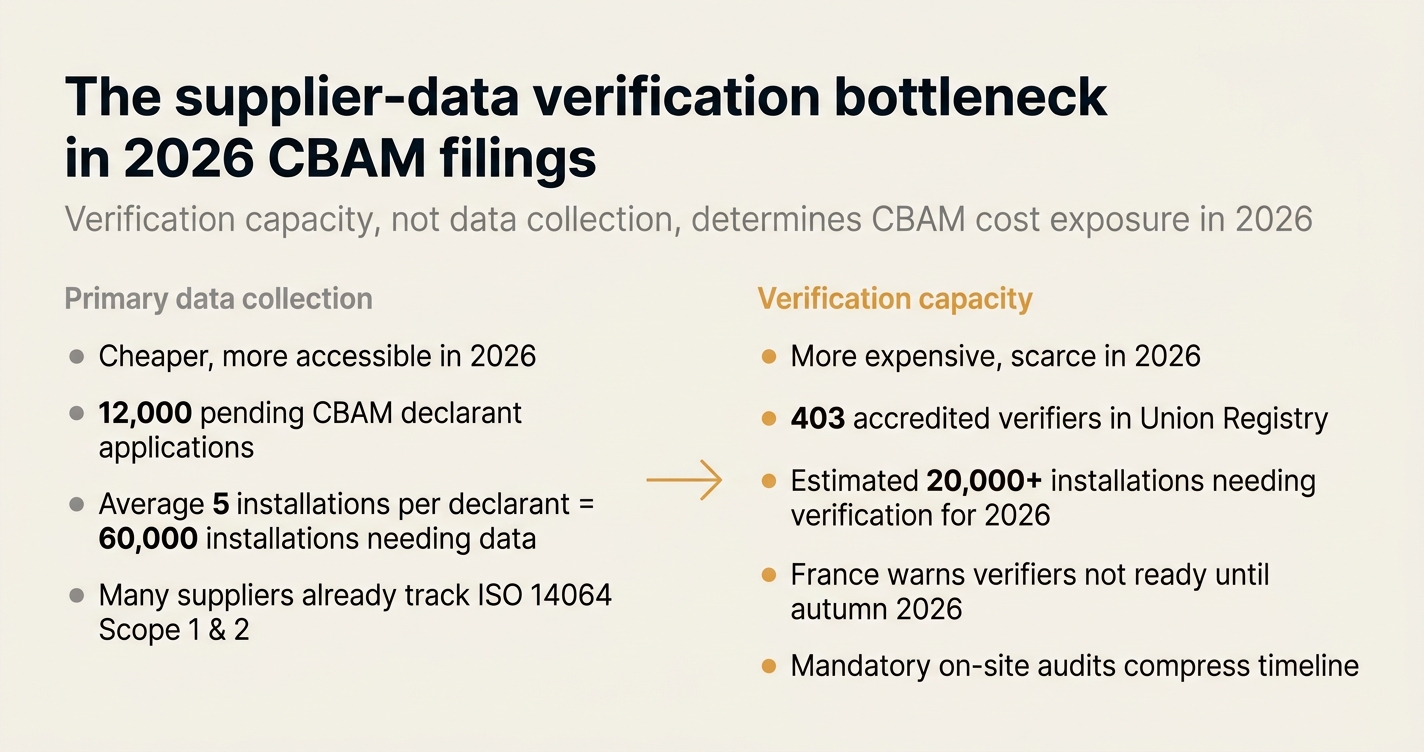

While primary data collection has become cheaper—many suppliers now track production emissions as part of ISO 14064 or Scope 1 and 2 disclosure—verification capacity has become more expensive and scarce. As of January 2026, only 403 accredited verifiers are registered in the Union Registry, compared to 4,100 authorised CBAM declarants and nearly 12,000 pending applications[3]. If each declarant sources from an average of five installations, the verification queue could exceed 20,000 installations for the 2026 calendar year, with fewer than 500 verifiers available. France's national competent authority has warned that accredited verifiers may not be ready until autumn 2026, leaving a narrow window between year-end emissions calculation and the September 30, 2027 filing deadline[3].

How do you solve this? I think the operators we work with who have already secured pre-verification agreements with accredited verifiers for their key suppliers will avoid the bottleneck. For installations in India, Turkey, and China—where verification infrastructure is still emerging—the timeline may compress further, because verifiers must conduct mandatory on-site audits in 2026 before any remote or waived-visit options become available in 2027[2]. For now, importers who wait until Q1 2027 to arrange verification will likely miss the filing deadline or fall back to default values, erasing the cost benefit of supplier engagement.

The shape of the argument, visualised below.

The verification timeline versus the filing deadline

The 2026 calendar year defines the first full reporting period under CBAM's definitive phase. Installations cannot calculate their annual emissions until December 31, 2026. Verification must occur after emissions are calculated but before the importer's annual declaration is due on September 30, 2027. That leaves a nine-month window for the following sequential steps:

| Step | Owner | Duration estimate | Blocking dependency |

|---|---|---|---|

| Emissions calculation finalised | Installation operator | 4–6 weeks post year-end | Annual activity data closure |

| Verification engagement initiated | Importer or installation | 2–4 weeks | Verifier availability |

| On-site audit scheduled and conducted | Accredited verifier | 6–10 weeks | Travel logistics, audit queue |

| Verification report issued | Accredited verifier | 2–3 weeks | Audit findings resolution |

| Verification report uploaded to CBAM Registry | Importer | 1 week | Electronic template availability (Jan 2027+) |

| Annual CBAM declaration submitted | Authorised declarant | 2–4 weeks | Verified data from all suppliers |

The blocking dependency is verifier availability. Even if an installation has perfect emissions data by February 2027, an on-site audit in March, and a report by April, a second installation in the same supply chain cannot begin verification until the first report is complete—because verification must occur "in the same order that the good is manufactured"[4]. For multi-tier supply chains, this sequential constraint can push the final verification report into August or September 2027, leaving no margin for error.

✅ Actionable checklist for securing verified supplier data in 2026

1. Map installation-level suppliers by mid-Q1 2026

Owner: Procurement and compliance teams

Action: Identify every non-EU installation that manufactures in-scope goods or precursor materials (e.g., steel billet, clinker, primary aluminium). Record installation name, address, production process, and annual volume.

Evidence artifact produced: Supplier installation register with contact details for plant-level compliance owners.

✅ Done when: Every in-scope product line has a named installation operator and you can trace embedded emissions to a physical facility, not a corporate headquarters.

2. Confirm supplier methodology alignment by end of Q1 2026

Owner: Supplier engagement lead

Action: Request a copy of each installation's monitoring plan or calculation methodology. Verify it follows the top-down approach defined in Implementing Regulation 2025/2547: installation-level emissions monitored, attributed to production processes, then converted to specific embedded emissions per tonne of product.

Evidence artifact produced: Methodology review checklist with gaps identified (e.g., missing Scope 2 for cement, incorrect allocation method for co-products).

✅ Done when: You have written confirmation that the supplier's calculation method matches the EU CBAM methodology, or you have flagged deviations for correction.

3. Identify accredited verifiers by market and sector by end of Q1 2026

Owner: Compliance lead or external consultant

Action: Search the Union Registry for accredited verifiers with experience in your suppliers' countries and sectors. Prioritise verifiers already conducting EU ETS audits who have extended their scope to CBAM verification.

Evidence artifact produced: Shortlist of 3–5 verifiers per key supplier market, with contact details and sector accreditations.

✅ Done when: You can match each high-priority installation to at least one accredited verifier who accepts engagements in that country.

4. Initiate pre-verification agreements by end of Q2 2026

Owner: Importer (if paying) or installation operator (if self-funded)

Action: Engage verifiers for a preliminary review of the installation's monitoring plan and a provisional audit schedule for Q1 2027. Some verifiers offer "pre-verification" services that identify gaps before the formal audit.

Evidence artifact produced: Signed engagement letter or statement of work with a named verifier, including indicative audit dates.

✅ Done when: The verifier has reserved capacity for your installation and you have a written commitment for an on-site audit in Q1 or Q2 2027.

5. Conduct trial calculations for Q2 or Q3 2026 by mid-year

Owner: Installation operator

Action: Run the CBAM calculation methodology on a representative quarter (e.g., Q2 2026 data) to surface data gaps, allocation errors, or missing emission factors before the full year closes.

Evidence artifact produced: Draft embedded emissions calculation for one quarter, including source documents (utility bills, production logs, invoicing records).

✅ Done when: The trial calculation identifies no blocking gaps, or gaps are documented with a remediation plan and owner.

6. Close annual emissions data by mid-February 2027

Owner: Installation operator

Action: Finalise 2026 production volumes, fuel consumption, electricity use, and any purchased precursor emissions. Lock the dataset so the verifier audits a stable baseline.

Evidence artifact produced: Closed emissions dataset with all source documents indexed and timestamped.

✅ Done when: The installation operator confirms in writing that no further adjustments will be made to 2026 data.

7. Schedule on-site audits for Q1 2027 by end of February 2027

Owner: Accredited verifier

Action: Confirm travel arrangements, audit agenda, and document requests. The verifier must conduct a physical site visit in 2026 for the first audit cycle; remote audits are only permitted from 2027 onwards if the installation was visited in 2026 and risk is low[2].

Evidence artifact produced: Audit schedule with confirmed dates, list of personnel to be interviewed, and document samples to be reviewed.

✅ Done when: The verifier has booked flights, the installation has reserved meeting rooms, and the document request list has been shared.

8. Complete on-site audit and resolve findings by mid-April 2027

Owner: Accredited verifier and installation operator

Action: The verifier reviews calculation methodology, cross-checks source documents, interviews plant managers, and applies a risk-based approach to identify misstatements. Any findings must be resolved before the verification report is issued.

Evidence artifact produced: Draft verification report with findings log and corrective actions.

✅ Done when: The installation operator has addressed all material findings and the verifier confirms no outstanding issues block report issuance.

9. Receive final verification report by end of April 2027

Owner: Accredited verifier

Action: Issue the verification report using the electronic EU template (available via the CBAM Registry from January 2027). The report must confirm that embedded emissions are complete, accurate, and calculated according to CBAM rules.

Evidence artifact produced: Signed verification report in the EU template format, uploaded to the CBAM Registry or transmitted to the importer by other means[2].

✅ Done when: The importer has received the verification report and confirmed it is accessible in the CBAM Registry.

10. Upload verified data to the CBAM Registry by mid-May 2027

Owner: Authorised CBAM declarant (importer or indirect customs representative)

Action: Log into the CBAM Registry, navigate to the annual declaration module, and attach each supplier's verification report. Enter installation-level emissions data, production volumes, and any applicable emission reductions (e.g., carbon price already paid in the country of origin).

Evidence artifact produced: Draft annual CBAM declaration with all verified supplier data fields populated.

✅ Done when: The Registry validates the submission (no missing fields, no format errors) and generates a preliminary certificate cost estimate.

11. Reconcile certificate cost versus budget by end of May 2027

Owner: Finance and compliance teams

Action: Compare the preliminary certificate cost (Registry estimate based on verified data) to the cost estimate if default values were used. Identify any installations where the verification benefit (lower emissions, lower cost) justifies the verification fee.

Evidence artifact produced: Cost-benefit table showing certificate savings per installation, verification fees incurred, and net benefit.

✅ Done when: CFO or finance lead has approved the final certificate purchase strategy and allocated budget for any shortfalls.

12. Submit annual CBAM declaration by September 30, 2027

Owner: Authorised CBAM declarant

Action: Finalise the annual declaration in the CBAM Registry, confirm all verification reports are attached, and submit. The Registry will calculate the total certificate liability for 2026 imports.

Evidence artifact produced: Submitted annual declaration with Registry confirmation receipt and certificate surrender schedule.

✅ Done when: The Registry issues a confirmation of submission and the declarant has a record of the certificate quantity to be surrendered.

13. Surrender CBAM certificates by September 30, 2027

Owner: Authorised CBAM declarant

Action: Purchase the required quantity of CBAM certificates from the Registry (priced at the weekly average EU ETS allowance price) and surrender them to match the declared embedded emissions for 2026.

Evidence artifact produced: Certificate surrender receipt from the CBAM Registry.

✅ Done when: The Registry confirms the certificate balance is zero for the 2026 reporting period and the declarant has no outstanding liability.

14. Archive verification and source documents for four years

Owner: Compliance and legal teams

Action: Retain all verification reports, monitoring plans, source documents (invoices, utility bills, production logs), and correspondence with verifiers. CBAM requires that these records be available for audit for four years from the start of the reporting year[2].

Evidence artifact produced: Indexed document archive with metadata (installation name, reporting period, document type).

✅ Done when: Legal counsel confirms the archive meets retention requirements and is accessible for future customs audits or spot checks.

15. Conduct post-filing review and update supplier engagement for 2027 by end of Q4 2027

Owner: Procurement and compliance leads

Action: Identify which suppliers delivered verified data on time, which required escalation, and which fell back to default values. Update supplier scorecards and adjust 2027 engagement plans (e.g., earlier pre-verification, alternative verifiers, or supplier substitution).

Evidence artifact produced: Supplier performance report with lessons learned and 2027 action plan.

✅ Done when: The 2027 CBAM compliance plan reflects the operational reality of the 2026 cycle and assigns accountability for high-risk suppliers.

The default-value penalty as a forcing function

Default values are not neutral estimates. The European Commission revised default benchmarks downward in late 2025, which paradoxically raises CBAM exposure for most products because the benchmarks now sit closer to efficient production levels[1]. An installation using best-available-technology may have actual emissions 20%–30% below the default, but without verification, the importer must declare the default anyway. For a 10,000-tonne annual import of steel billet at €80 per CBAM certificate, the cost difference between default and actual values can exceed €1.6 million per year.

"Relying on defaults instead of verified actuals will significantly increase your CBAM cost exposure. The Commission revised default benchmarks downward in late 2025, which actually raises CBAM exposure for most products."[1]

The penalty is structural: default values include a conservative mark-up, and importers cannot negotiate or appeal them. The only lever is verification, which converts default values into installation-specific actuals. But verification requires verifier capacity, and capacity is the bottleneck. Importers who secure verifier commitments in Q1 2026 will absorb the verification fee (typically €5,000–€15,000 per installation) but avoid the multi-million-euro default penalty. Importers who wait until 2027 will pay the penalty regardless of their supplier engagement success.

How Emission3 fits

Emission3 helps non-EU exporters and EU importers prepare verified, audit-ready supplier data before the verification window opens. The platform ingests source documents—utility bills, production logs, invoicing records—and runs the CBAM calculation methodology at installation level, producing a trial embedded emissions figure with full lineage from source document to final number[5]. This trial calculation surfaces data gaps, allocation errors, and methodology misalignments early enough to fix them before the verifier arrives.

For installations in markets where accredited verifiers are scarce, Emission3's document-first approach reduces the on-site audit time from 10 days to 3–4 days, because the verifier is reviewing a structured evidence pack rather than raw spreadsheets. The platform also tracks which suppliers have secured verifier commitments and flags installations where the September 2027 timeline is at risk, allowing procurement teams to escalate or activate contingency suppliers.

All customers start with a CBAM readiness call: we map suppliers, identify high-risk installations, estimate the verification queue, and build a week-by-week timeline from now through September 2027[6]. For non-EU exporters, we also connect you to accredited verifiers in your region and help you prepare the monitoring plan and source documents they will request during the audit.

Start securing verifier capacity now

The 2026 CBAM filing cycle is not a Q1 2027 problem—it is a Q1 2026 capacity allocation problem. By mid-2026, most accredited verifiers with multi-country capability will have filled their 2027 audit calendars. Importers who engage verifiers in Q2 2026 will secure early audit slots and avoid the September 2027 rush. Importers who wait until year-end will face a choice: pay the default-value penalty or miss the filing deadline.

If you are an EU importer sourcing from installations in India, Turkey, China, or other high-volume CBAM markets, book a CBAM readiness call now to map your supplier verification timeline and identify verifier contacts in your key geographies[6]. If you are a non-EU exporter, the same call will help you prepare the monitoring plan and source documents your customers' verifiers will request, reducing audit time and increasing the likelihood your data is accepted in the annual declaration.

The verification bottleneck is solvable, but only with early action. The importers who close 2026 with verified supplier data will control their CBAM cost exposure. The importers who fall back to default values will pay the penalty—and their suppliers will absorb the tariff cost through price negotiations or lost contracts.

Book a CBAM readiness call to start securing verifier capacity for your 2026 filings[6].

References & Sources

External Sources

- [1]CBAM | Your Guide to the EU Carbon Border Adjustment Mechanism

Explains how relying on default values instead of verified actuals significantly increases CBAM cost exposure, and how the Commission's revised benchmarks affect importers.

- [2]CBAM reporting requirements & Compliance Guide for 2026

Details the mandatory on-site audit requirements for 2026, the transition to virtual audits from 2027, and the four-year document retention requirement.

- [3]Guest Post: Whose CBAM is it anyway? Of Default Values and Accreditation

Quantifies the verifier shortage: 403 accredited verifiers versus 4,100 authorized declarants and nearly 12,000 pending applications as of January 2026.

- [4]High CBAM Default Values Underscore the Need for U.S. Data

Explains the sequential verification requirement: facilities must be verified in the same order that the good is manufactured, creating timeline bottlenecks.

Related Content

- [5]How Emission3 handles CBAM

Shows how Emission3 ingests source documents and runs the CBAM calculation methodology at installation level to produce audit-ready trial calculations.

- [6]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, identify verification gaps, and build a timeline from now through the September 2027 deadline.