The methodology documentation gap in California SB 253 Scope 3 disclosures

The methodology documentation gap in California SB 253 Scope 3 disclosures

Here's the issue: California's Climate Corporate Data Accountability Act (SB 253) requires Scope 3 emissions reporting starting in 2027, with limited assurance phasing in shortly after. For CFOs at firms with over $1 billion in California-linked revenue, this looks like a straightforward extension of Scope 1 and 2 disclosure: collect supplier data, calculate totals, submit. However, auditors are re-pricing engagements by 20 to 40 percent for firms without evidence lineage, and the safe harbour provisions protecting good-faith Scope 3 misstatements expire in 2030. The perceived bottleneck is supplier engagement. The actual bottleneck is methodology documentation.

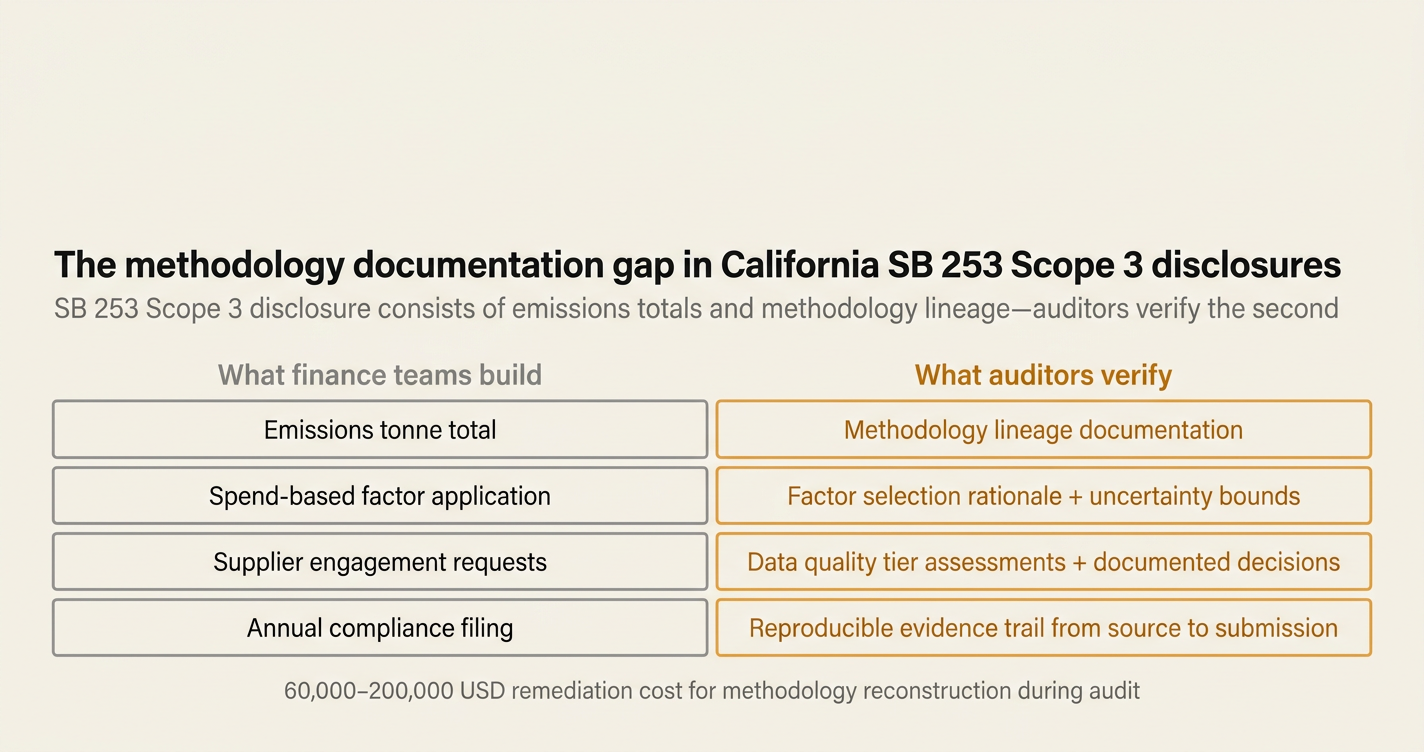

However, SB 253 Scope 3 disclosure consists of two things: the emissions number and the methodology lineage. The emissions number is the tonne-equivalent total you submit to the California Air Resources Board (CARB). The methodology lineage is the documented chain of calculation choices, factor selections, spend-based versus activity-based decisions, and data quality assessments that produced that number. Both are required under the Greenhouse Gas Protocol Corporate Standard, which SB 253 adopts by reference.

The emissions number on its own has no value to an auditor. The methodology lineage is what the auditor is actually asking for, paying for, and verifying. When CARB states that reports must follow the GHG Protocol, it is not requesting a tonne total. It is requesting reproducible evidence that the tonne total was derived using methods consistent with the Corporate Standard, that allocation decisions were documented, that data quality was assessed, and that any deviations were justified and disclosed. Without this lineage, the emissions number is unverifiable, and the disclosure fails the assurance test.

While spend-based estimation has become cheaper and faster through SaaS platforms, methodology documentation has become more expensive and time-intensive. If your Scope 3 inventory relies on spend-based factors for 80 percent of procurement, the cost of documenting why those factors were chosen, how they were applied, and what uncertainty bounds exist might outpace the cost of the calculation itself. A 2026 limited assurance engagement on Scope 1 and 2 emissions costs between 40,000 and 120,000 USD for mid-sized firms. A 2027 Scope 3 engagement without pre-existing methodology lineage can add 60,000 to 200,000 USD, because the auditor must reconstruct the documentation your finance team did not build.

How do you solve this? I think the operators we work with are building methodology lineage as a first-class artifact, not a post-hoc audit response. For California SB 253 filers, this means treating every supplier data request, every factor selection, and every spend-based fallback as a documented decision with a recorded rationale. The evidence trail is not assembled after the calculation. It is the calculation. For now, that approach requires infrastructure that most sustainability platforms do not provide, because they were built to generate numbers, not to generate the lineage those numbers rest on.

The shape of the argument, visualised below.

Myth 1: SB 253 only requires emissions totals, not evidence trails

Reality: SB 253 mandates that emissions reporting follow the Greenhouse Gas Protocol Corporate Standard, which explicitly requires documentation of calculation methodologies, data sources, assumptions, and uncertainty assessments. CARB's 2026 regulation text and workshop materials confirm that disclosures must be independently assured, meaning auditors will verify not only the tonne totals but also the documented methods and evidence that produced them. Limited assurance on Scope 3 emissions is expected in subsequent rulemaking, with reasonable assurance scaling up over time [1]. Without methodology lineage, the emissions number is unverifiable, and the disclosure fails the assurance requirement. The safe harbour provision for good-faith Scope 3 misstatements, which runs from 2027 to 2030, does not exempt firms from documenting how they arrived at their numbers—it only shields them from penalties if those numbers are later found to be incorrect but were calculated in good faith using documented methods [2].

Myth 2: Spend-based estimation is sufficient for Scope 3 compliance

Reality: Spend-based estimation is a recognised method under the GHG Protocol for Category 1 (Purchased Goods and Services), but it is considered the lowest-quality data tier, and its use must be justified and disclosed. Auditors will require documentation explaining why spend-based factors were chosen over supplier-specific data, which factors were applied to which procurement categories, how factor selection uncertainty was assessed, and what data quality limitations exist. CARB has not restricted the use of spend-based methods, but assurance standards like ISAE 3000, ISAE 3410, and ISO 14064-3, which CARB is considering for 2027 and beyond, require auditors to evaluate the appropriateness of methods and the completeness of documentation [3]. A spend-based inventory without documented factor selection rationale, uncertainty bounds, and data quality assessments is unlikely to pass limited assurance. The cost of post-hoc documentation can exceed the cost of the original calculation by a factor of two or three.

Myth 3: The 2027 Scope 3 reporting deadline is far enough out to defer preparation

Reality: Scope 3 reporting in 2027 covers fiscal year 2026 data for most firms. This means data collection, supplier engagement, and methodology documentation must be completed during 2026. Firms that have not started building their Scope 3 inventory by mid-2025 are facing a 12 to 18-month implementation window, which is insufficient for comprehensive supplier engagement and evidence lineage construction. CARB's proposed reporting date of August 10, 2027 for Scope 3 leaves no buffer for restatements or documentation gaps discovered during assurance. The auditor's timeline is further compressed: most assurance providers require at least 60 to 90 days to complete a limited assurance engagement, meaning the evidence trail must be complete by May or June 2027 [4]. Firms that defer Scope 3 preparation to 2026 will find themselves competing for auditor capacity and paying premium rates for expedited engagements.

Myth 4: The safe harbour provision eliminates liability risk for Scope 3 disclosures

Reality: The safe harbour provision, which runs from 2027 to 2030, shields firms from administrative penalties if their Scope 3 disclosures contain good-faith misstatements, but it does not eliminate the requirement to document methodology or the risk of investor or stakeholder scrutiny. A good-faith misstatement is one made using reasonable methods and available data, with documented limitations and uncertainties. A misstatement resulting from undocumented assumptions, unjustified factor selections, or missing data quality assessments is not protected by the safe harbour, because it was not made in good faith. Furthermore, SB 253 disclosures are public and will be reviewed by investors, rating agencies, and NGOs. A Scope 3 inventory with large uncertainty bounds and weak methodology documentation invites questions about management competence and climate strategy credibility. The safe harbour protects against CARB penalties, but it does not protect against reputational damage or shareholder litigation [5].

Myth 5: SB 253 assurance requirements are less stringent than SEC Climate Rule requirements

Reality: SB 253 assurance requirements are more comprehensive than the proposed SEC Climate Rule in two key respects. First, SB 253 requires assurance on Scope 1 and 2 emissions starting in 2027, with limited assurance scaling to reasonable assurance by 2030, and limited assurance on Scope 3 emissions expected in subsequent rulemaking. The proposed SEC Climate Rule, which remains stayed, required assurance only for large accelerated filers and only on Scope 1 and 2 emissions, with no Scope 3 assurance requirement [6]. Second, SB 253 applies to both public and private companies with over $1 billion in revenue doing business in California, regardless of where they are headquartered or whether they are SEC registrants. The SEC Climate Rule applied only to SEC registrants. This means SB 253 captures a broader population of firms, including private equity-backed companies and non-US multinationals, and subjects them to assurance requirements that many have never encountered. The assurance standards CARB is considering, including ISSA 5000, ISAE 3000, ISAE 3410, AICPA AT-C 210, AA1000AS v3, and ISO 14064-3, all require auditors to obtain sufficient appropriate evidence to support the disclosed emissions, which in practice means comprehensive methodology lineage [7].

Myth 6: Auditors will accept spreadsheet-based Scope 3 calculations if the numbers are reasonable

Reality: Auditors do not verify whether numbers are reasonable. They verify whether numbers are reproducible from documented evidence using disclosed methods. A spreadsheet-based Scope 3 calculation without version control, formula lineage, input source references, and change logs is unverifiable, regardless of whether the final tonne total passes a reasonableness test. Assurance standards require auditors to trace emissions totals back to source documents, verify that calculation methods align with the GHG Protocol, and confirm that assumptions and limitations are appropriately disclosed. A spreadsheet model that calculates 50,000 tonnes of Category 1 emissions using spend-based factors might be directionally correct, but if the auditor cannot determine which version of the model was used, which factors were applied to which spend categories, or how factor selection was justified, the calculation fails the evidence test. The cost of retrofitting lineage into a spreadsheet model is typically higher than building lineage-first infrastructure from the start, because it requires reconstructing decisions that were made months or years earlier without contemporaneous documentation.

Myth 7: Methodology documentation is a compliance cost with no operational value

Reality: Methodology documentation is the only durable artifact from a Scope 3 inventory. The emissions number will change every year as suppliers, procurement patterns, and factors evolve. The methodology lineage is the institutional knowledge that allows your finance team to update the inventory without starting from scratch, to onboard new auditors without re-explaining every decision, and to respond to stakeholder questions without conducting forensic archaeology on old spreadsheets. Firms that treat methodology lineage as a first-class artifact report 40 to 60 percent reductions in audit preparation time in subsequent years, because the evidence trail is already built. They also report faster integration of primary supplier data, because the lineage infrastructure makes it clear where spend-based estimates exist and what the data quality impact of replacing them would be. The CFOs we work with describe methodology lineage as the difference between a compliance filing and a decision-ready inventory. The filing is an annual obligation. The inventory is a strategic asset.

| Myth | Reality | Consequence if ignored |

|---|---|---|

| SB 253 only requires emissions totals | Requires emissions totals plus documented methodology lineage per GHG Protocol | Assurance failure, 60,000–200,000 USD remediation cost |

| Spend-based estimation is sufficient | Must document factor selection rationale, uncertainty bounds, data quality tier | Post-hoc documentation cost 2–3× original calculation cost |

| 2027 deadline is far enough out | Covers FY2026 data, requires 12–18 month implementation window starting mid-2025 | Compressed auditor timeline, premium engagement rates |

| Safe harbour eliminates liability risk | Protects good-faith misstatements with documented methods, not undocumented guesses | Reputational damage, shareholder scrutiny, no penalty protection |

| Less stringent than SEC Climate Rule | More comprehensive: Scope 3 assurance, public + private firms, reasonable assurance by 2030 | Broader exposure, higher assurance cost, unfamiliar standards |

| Spreadsheets acceptable if numbers reasonable | Auditors verify reproducibility from source documents, not reasonableness of outputs | Unverifiable calculations, assurance failure, model reconstruction cost |

| Documentation is compliance cost only | Methodology lineage enables 40–60% reduction in subsequent audit prep time, faster data updates | Lost institutional knowledge, repeated forensic work, higher ongoing cost |

"CARB will exercise enforcement discretion for the first report due in 2026, allowing reporting entities to submit Scope 1 and Scope 2 emissions based on information they already have or were collecting when this Notice was issued, whether or not the data received limited assurance. However, during the Q&A portion of the November 2025 workshop, CARB emphasized that this discretionary relief is only applicable in the first year of reporting." [8]

How Emission3 fits

Emission3 is built to generate methodology lineage as the primary artifact, with emissions totals as a derived output. Every supplier data request, every factor selection, and every spend-based fallback is recorded as a documented decision with timestamp, rationale, and data quality assessment. The platform exports evidence packs that include calculation lineage, source document references, and factor provenance trails, structured for ISAE 3410 and ISO 14064-3 verification. For California SB 253 filers, this means the methodology documentation required for 2027 Scope 3 assurance is built during the 2026 data collection process, not reconstructed afterward. The result is an inventory where every number is reproducible from source evidence, and the evidence trail is already formatted for auditor review.

Start with a CBAM readiness call

If you are a CFO at a firm with over $1 billion in California-linked revenue, facing SB 253 Scope 3 reporting in 2027, the question is not whether you need methodology lineage. The question is whether you will build it as you go or pay to reconstruct it under audit pressure. We start every engagement with a readiness call: we map your current Scope 3 inventory, identify documentation gaps, and scope the implementation timeline required to meet the 2027 filing deadline with assurance-ready evidence. No anonymous self-serve onboarding. No generic SaaS trial. Book a CBAM readiness call at /book-demo, and we will walk through what lineage-first Scope 3 infrastructure looks like for your procurement footprint [9].

References & Sources

External Sources

- [1]California SB 253 and SB 261: What Businesses Need to Know

CARB's February 2026 Board hearing confirmed the first Scope 1 and 2 reporting deadline of August 10, 2026, with limited assurance for Scope 1 and 2 beginning in 2027 under proposed standards including ISSA 5000, ISAE 3000/3410, and ISO 14064-3, scaling to reasonable assurance by 2030.

- [2]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law

SB 253 mandates annual disclosure of Scope 1 and 2 emissions beginning August 10, 2026, and Scope 1, 2, and 3 emissions from 2027 onward, with independently assured data required under standards to be finalized by CARB in subsequent rulemaking.

- [3]Mandatory Climate Disclosures: Unpacking CA SB 253 and 261

SB 253 requires emissions quantification aligned to the GHG Protocol, with third-party verification scaling from limited assurance (20% of data) to reasonable assurance (80% of data) by 2030, and a safe harbour for good-faith Scope 3 misstatements expiring in 2030.

- [4]Sustainability Spotlight: California Climate Legislation Update (December 2025)

CARB will exercise enforcement discretion for the first 2026 Scope 1 and 2 report, but emphasized during the November 2025 workshop that this relief is only applicable in the first year, with full assurance requirements beginning in 2027 for subsequent reporting cycles.

- [5]California Climate Disclosure: Build Audit-Ready Disclosures

SB 253 requires public and private US businesses with revenues over $1 billion doing business in California to report Scope 1, 2, and 3 GHG emissions with third-party assurance, representing one of the most comprehensive state-led climate disclosure requirements globally.

- [6]SB 253 and SB 261: California climate reporting explained

CARB's regulation requires initial Scope 1 and 2 reporting by August 10, 2026 covering 2025 fiscal year data for most entities, with Scope 3 reporting beginning in 2027, and assurance standards including ISAE 3000, ISAE 3410, and ISO 14064-3 under consideration for implementation in 2027 and beyond.

- [7]California SB 253: Key requirements for 2026 and how to comply

SB 253 follows the Greenhouse Gas Protocol and requires independent third-party verification of emissions data across scopes, with non-compliance penalties reaching up to $500,000 per reporting year, making it one of the most comprehensive state-led climate laws globally.

- [8]SB 253/261/219 Public Workshop: Update on California Corporate Climate Disclosures

CARB workshop slides from November 2025 previewing Q1 2026 initial regulation board hearing, proposed August 10, 2026 Scope 1 and 2 reporting deadline, and subsequent rulemaking to establish Scope 3 data assurance requirements, enforcement provisions, and recurring reporting standards.

Related Content

- [9]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation timeline for SB 253 Scope 3 filing, no anonymous self-serve onboarding.

- [10]Audit-ready exports in Emission3

For auditors and CFOs: see the evidence lineage artifact that makes SB 253 Scope 3 methodology documentation reproducible from source documents to filing.