The assurance-fee escalation problem in US climate disclosure programs

The assurance-fee escalation problem in US climate disclosure programs

Here's the issue: CFOs are discovering that the assurance fees for California SB 253 compliance are re-pricing at 20-40% above initial quotes, not because the emissions calculations grew more complex, but because the evidence-gathering timelines expanded. A sustainability director at a manufacturing firm told us their auditor's revised proposal included 180 additional hours for lineage verification—none of it tied to Scope 1 or 2 volume.

However, SB 253 compliance consists of two things: emissions totals and evidence lineage. The first is what finance teams see in the emissions inventory—the tonnage figure that appears in the disclosure. The second is the document trail that proves every number is reproducible: utility bills, meter readings, allocation methods, calculation sheets, approval timestamps.

Emissions totals on their own have no audit value. Evidence lineage is what the assurance provider is actually verifying—and billing for. When an auditor requests "support for the 2,847 tCO2e figure in Scope 1," they are not asking for a calculation walk-through. They are asking for source documents, version-controlled lineage, and a signature trail showing who reviewed what, when. The audit clock starts when you cannot produce that evidence pack on demand.

While baseline compliance software has become cheaper—templated GHG Protocol calculators, cloud emissions trackers—the cost of building audit-ready evidence packs has escalated. If a 5,000-employee firm without document lineage faces a limited assurance engagement in June 2026, the cost of retrofitting evidence for 2025 emissions might exceed the entire 2026 compliance budget by 30-50%. The California Air Resources Board estimates annual SB 253 program fees at $3,160 per entity,[1] but assurance providers are quoting $40,000-$80,000 for limited assurance on Scope 1 and 2, depending on evidence quality.

How do you solve this? I think the operators who avoid fee escalation are the ones treating evidence lineage as a first-class compliance artifact from day one. They are not retrofitting audit trails in Q2 2026—they are ingesting utility bills, tagging allocation methods, and timestamping approvals as part of the monthly close. For now, that means document-first ingestion tooling, not just emissions calculators.

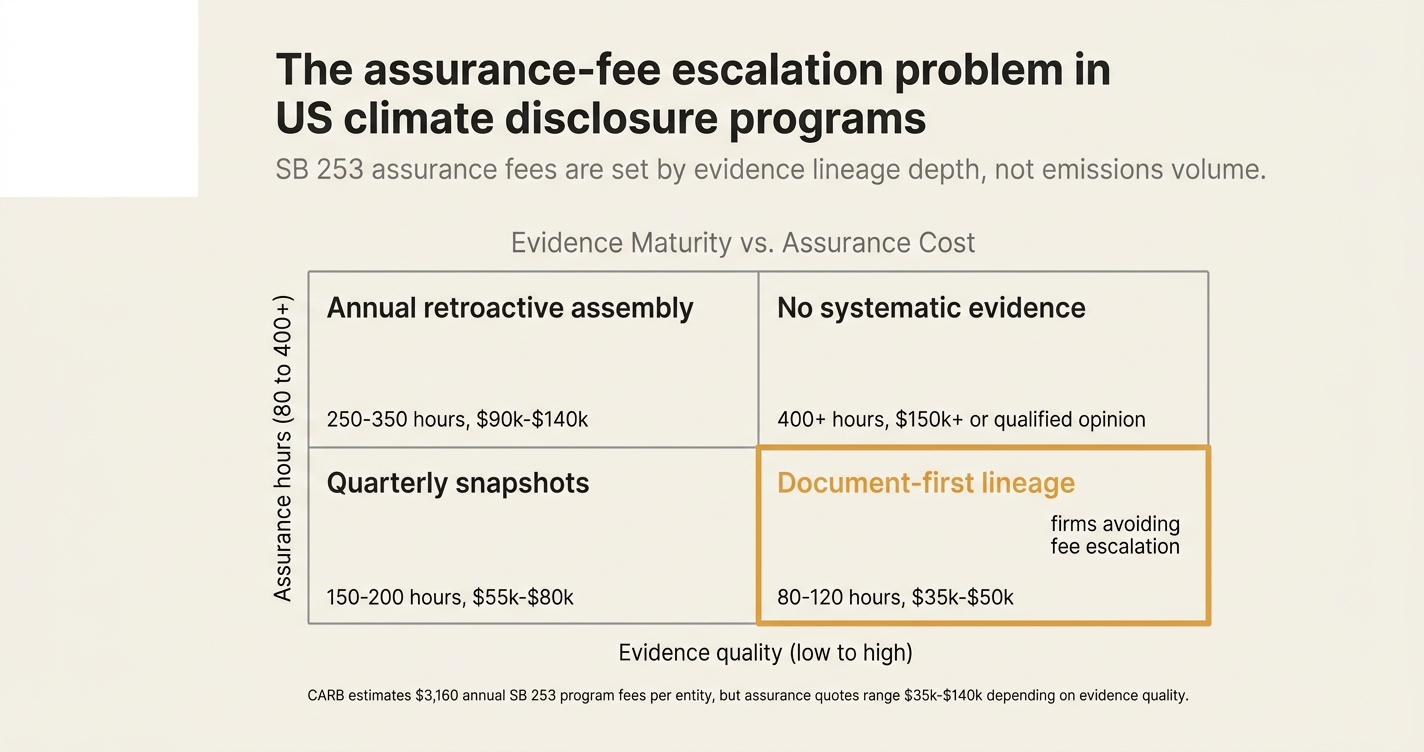

The shape of the argument, visualised below.

Five myths about SB 253 assurance costs

Most CFOs we speak with are operating on assumptions about SB 253 assurance that do not match what auditors are actually pricing. Below are the five most common myths, followed by the reality we see in audit proposals and fee re-negotiations.

Myth 1: Assurance fees are proportional to emissions volume

Reality: Assurance fees are proportional to evidence complexity, not tonnage. A firm with 50,000 tCO2e across 200 facilities and incomplete meter records will pay more for limited assurance than a firm with 150,000 tCO2e from 20 facilities with utility bill lineage. The California Air Resources Board published preliminary fee estimates of $3,160 annually for SB 253 program administration,[1] but third-party assurance quotes we have reviewed range from $35,000 to $120,000 depending on evidence quality. Auditors are not pricing the emissions total—they are pricing the document retrieval effort. One assurance provider told us that firms without quarterly evidence snapshots require 2-3x more audit hours because the verification team has to reconstruct lineage retroactively.

Myth 2: Limited assurance in 2026 is a lighter-touch engagement

Reality: Limited assurance still requires substantive evidence, just with lower statistical confidence thresholds than reasonable assurance. The International Auditing and Assurance Standards Board (IAASB) defines limited assurance as achieving a level of confidence "lower than reasonable assurance but nonetheless meaningful."[2] In practice, this means auditors will sample 10-20% of emissions sources instead of 50-70%, but the evidence standard for that sample remains the same: source documents, calculation lineage, approval timestamps. A manufacturing CFO told us their auditor's limited assurance scope included full lineage verification for 15 of 80 facilities, but the document requests for those 15 sites were identical to reasonable assurance. The lighter touch is in sample size, not evidence depth. Firms treating limited assurance as "optional documentation" are discovering scope changes mid-engagement.

Myth 3: Scope 3 assurance is the expensive part

Reality: Scope 3 assurance is expensive, but Scope 1 and 2 evidence gaps are triggering fee escalations now, in 2026. Under SB 253, limited assurance for Scope 1 and 2 is required starting with 2026 data (reported in 2027), while Scope 3 limited assurance does not begin until 2030.[3] Yet the assurance proposals we review show that Scope 1 and 2 verification is where firms without document lineage are getting re-priced. One auditor explained: "Scope 3 is complex, but it's also mostly estimated—our verification procedures are standardized. Scope 1 and 2 should be simple, but when the client can't produce meter records or allocation sheets, we have to build the evidence pack ourselves." That reconstruction work is billed at $200-$400 per hour. The firms hitting budget overruns are the ones who assumed Scope 1 and 2 would be a checkbox engagement.

Myth 4: Assurance fees are one-time implementation costs

Reality: Assurance fees recur annually, and they escalate if evidence quality does not improve. SB 253 requires annual reporting starting in 2026, with assurance transitioning from limited (2026-2029) to reasonable (2030+).[4] Auditors we have spoken with are clear: if a firm's evidence lineage in 2027 is not materially better than 2026, the 2027 assurance fee will include the same reconstruction hours. One assurance partner said, "We assume clients will fix the process after the first audit. If they don't, we price the second year as if it's still a first-time engagement." The CFOs avoiding fee escalation are the ones treating 2026 as the baseline for process improvement, not a one-time compliance event. They are building evidence lineage into monthly close procedures so that by 2027, the audit is sampling a mature system, not chasing retroactive documents.

Myth 5: Internal controls reduce assurance scope

Reality: Internal controls reduce assurance scope only if they generate audit evidence as a by-product. The Greenhouse Gas Protocol Corporate Standard, which SB 253 requires firms to follow,[5] emphasizes that emissions data quality depends on "transparent, documented procedures for calculating emissions and tracking data." Auditors interpret this as document lineage, not just control descriptions. A firm with SOX-compliant financial controls might still face a full-scope limited assurance engagement if those controls do not produce timestamped calculation sheets, version-controlled allocation methods, and approval trails for emissions data. One auditor explained: "I care less about whether you have a control and more about whether I can see the control in action when I pull a sample." The firms reducing assurance hours are the ones generating evidence artifacts—utility bill PDFs, meter reading logs, allocation change logs—as part of routine operations, not just maintaining control documentation.

The assurance-fee escalation pattern we see in 2026 engagements

| Evidence maturity level | Assurance hours (limited, Scope 1+2) | Typical fee range | Primary cost driver |

|---|---|---|---|

| Document-first lineage: utility bills, meter logs, allocation sheets ingested monthly | 80-120 hours | $35,000-$50,000 | Sample testing of existing evidence packs |

| Quarterly evidence snapshots: some documents available, gaps require follow-up | 150-200 hours | $55,000-$80,000 | Document retrieval for missing evidence |

| Annual retroactive assembly: calculations exist, source documents must be reconstructed | 250-350 hours | $90,000-$140,000 | Lineage reconstruction, multiple audit rounds |

| No systematic evidence: calculations without supporting documents | 400+ hours or scope limitation | $150,000+ or qualified opinion | Full retroactive build-out, potential re-audit |

These ranges are based on assurance proposals we have reviewed for firms with $1-5 billion in revenue and 10,000-50,000 tCO2e in Scope 1 and 2 combined. The firms in the first row—document-first lineage—are the ones booking their 2027 audits at flat or declining fees. The firms in the last row are the ones receiving mid-engagement scope changes and 40%+ fee increases.

"The majority of costs and staff resources or about 58% will be related to the implementation of SB253. Therefore, with these assumptions and methodology, the estimated fee for each entity covered under SB253 will be approximately $3,160 annually." — California Air Resources Board, SB 253/261 Workshop, August 21, 2025[1]

That $3,160 is the CARB program administration fee. It does not include third-party assurance costs, which are set by the auditor and depend entirely on evidence quality.

Why evidence lineage is becoming the primary cost driver

The assurance-fee escalation we see in SB 253 engagements is not random. It follows a predictable pattern: auditors price the effort required to verify that emissions data is reproducible, and that effort scales with evidence gaps, not emissions volume.

Consider a manufacturing firm with 20,000 tCO2e in Scope 1 emissions across 50 facilities. If utility bills for those 50 facilities are ingested monthly, tagged with allocation methods, and timestamped by the approver, the auditor can sample 10 facilities, verify the lineage for those 10, and complete limited assurance in 80-100 hours. But if utility bills are stored in email archives, allocation methods are undocumented, and approvals are informal, the auditor must reconstruct that lineage retroactively—facility by facility—before they can even begin verification. That reconstruction effort is what drives 250+ hour engagements.

The firms we work with who are avoiding fee escalation are the ones treating evidence lineage as a compliance artifact from day one. They are not waiting until Q2 2026 to gather documents. They are ingesting utility bills as they arrive, logging meter readings as they are collected, and timestamping allocation decisions as they are made. By the time the auditor requests evidence in June 2027, the evidence pack already exists.

One CFO described the shift this way: "We used to think of emissions reporting as a year-end calculation exercise. Now we treat it like a monthly financial close, with the same evidence standards and approval workflows. The audit fee dropped 35% in year two because the auditor was sampling a system, not chasing documents."

How Emission3 fits

Emission3 is built for CFOs and sustainability leads who need to deliver audit-ready SB 253 disclosures without retrofitting evidence in Q2 2026.

We start with a compliance readiness call—no anonymous self-serve onboarding. In that call, we map your facility footprint, identify evidence gaps, and scope the implementation timeline. For most firms, that means document-first ingestion: utility bills, meter readings, and allocation sheets flow into the system as they arrive, not at year-end.

Every emissions calculation in Emission3 is deterministic and reproducible. When an auditor requests support for a 2,847 tCO2e figure, the system exports a full evidence pack: source documents, calculation lineage, allocation method, approval timestamp, and the name of the reviewer. That pack is formatted for limited assurance from day one.

Our pricing is scoped after the readiness call, not before. Founding-tier clients are live in 4-6 weeks, including document ingestion setup and auditor coordination. We work with your assurance provider to confirm evidence format and lineage depth before the first monthly close, so there are no mid-engagement scope changes.

If you are facing a June 2027 SB 253 limited assurance deadline and do not yet have systematic evidence lineage, the time to act is now. The firms booking flat or declining assurance fees in 2027 are the ones who started building evidence packs in Q4 2025 or Q1 2026, not in audit season.[6]

Your SB 253 assurance-fee roadmap

If you are responsible for SB 253 compliance and assurance budgeting, here is the sequence we recommend:

-

Audit your current evidence maturity (week 1): Can you produce utility bills, meter logs, and allocation sheets for 2025 emissions on demand, or are they scattered across email, file shares, and invoice systems? Be specific about retrieval time per facility.

-

Request a preliminary assurance quote (week 2): Ask your auditor to scope limited assurance for Scope 1 and 2 based on your current evidence state. If the quote assumes you will "provide supporting documents," clarify what that means: formatted evidence packs, or raw documents requiring auditor assembly?

-

Implement document-first ingestion (weeks 3-8): Begin ingesting 2026 utility bills and meter readings as they arrive, using whatever system you choose—Emission3, internal tooling, or manual assembly. The key is monthly evidence snapshots, not year-end reconstruction.

-

Run a Q2 2026 evidence audit (week 20): Before mid-year, test whether you can produce a full evidence pack for January-March 2026 emissions. If retrieval takes more than 2 hours per facility, your assurance fee will escalate.

-

Book your assurance provider by Q3 2026 (week 30): Limited assurance for 2026 data is due by June 30, 2027. Auditors are booking SB 253 engagements 9-12 months in advance. Late bookings pay a premium.

-

Run a full evidence dry-run in Q4 2026 (week 45): Simulate the auditor's document request for all of 2026. If you cannot produce complete evidence packs for 10 sampled facilities in 48 hours, expect scope changes and fee increases when the audit begins.

The CFOs who follow this sequence are the ones closing their 2027 limited assurance engagements in 80-120 hours at $35,000-$50,000. The ones skipping steps 3 and 4 are the ones facing 250+ hour engagements and $90,000+ fees.[7]

What to do next

If you are facing a June 2027 SB 253 assurance deadline and your evidence lineage is not yet systematic, book a CBAM readiness call with Emission3. We will map your facility footprint, identify evidence gaps, and scope a document-first implementation timeline. All engagements start with a readiness conversation—no anonymous self-serve onboarding.

For CFOs and audit committees evaluating assurance-fee projections, review the audit-ready export format in Emission3 to see what evidence-pack depth looks like in practice. The firms avoiding fee escalation are the ones exporting lineage artifacts as a by-product of monthly close, not as a retrofit in audit season.[8]

References & Sources

External Sources

- [1]CARB Virtual Public Workshop on SB 253, SB 261, and SB 219 - August 21, 2025

California Air Resources Board preliminary fee estimates for SB 253 program administration, scoped at $3,160 annually per covered entity based on 2,596 estimated entities and 58% of implementation costs allocated to SB 253.

- [2]California Climate Disclosure Compliance Software | SB 253 | Novisto

Explanation of limited assurance requirements under SB 253, including role-based approvals, transparent audit trails, and complete change tracking to prepare for June 30, 2026 Scope 1 and 2 assurance deadlines.

- [3]California's climate disclosure regulations: An update on SB 253 and SB 261

SB 253 compliance timeline showing limited assurance for Scope 1 and 2 beginning in 2027 for 2026 data, with Scope 3 assurance not required until 2030, and transition to reasonable assurance in 2030 for Scope 1 and 2.

- [4]How SB 261 & SB 253 are Rewriting Climate Reporting

Overview of SB 253 assurance timeline: limited assurance for Scope 1 and 2 begins in 2026 and transitions to reasonable assurance in 2030, with Scope 3 limited assurance starting in 2030 subject to further CARB review in 2027.

- [5]CARB Publishes List of Companies Subject to California Climate Disclosure Laws

SB 253 requires companies to submit annual Scope 1, Scope 2, and eventually Scope 3 GHG disclosures with assurance, aligned with the Greenhouse Gas Protocol, for companies with over $1 billion in revenue, with obligations beginning in 2026.

Related Content

- [6]The assurance-timeline disconnect in California SB 253 reporting programs

SB 253 reporting consists of two things: emissions totals and evidence-gathering timelines. Companies budget for the first—but assurance fees are set by the second.

- [7]The assurance-fee escalation problem in 2026 SB 253 emissions reporting

SB 253 reporting consists of two things: emissions totals and evidence lineage. CFOs budget for the first—but assurance fees are set by the second.

- [8]Audit-ready exports in Emission3

For auditors and CFOs, the evidence lineage artifact: every calculation is reproducible, with full document trail from source utility bill to filing, formatted for limited and reasonable assurance.