The Scope 3 methodology-drift problem in ESRS E1 disclosure programs

The Scope 3 methodology-drift problem in ESRS E1 disclosure programs

Here's the issue: a sustainability team closes its first ESRS E1 disclosure cycle with Scope 3 emissions calculated at 47,300 tCO2e. Twelve months later, the same team recalculates the baseline year using updated emission factors and a refined allocation rule for Category 4 emissions, and the number shifts to 51,800 tCO2e. The year-on-year trend now shows a 2% reduction instead of the originally reported 8%. The assurance partner flags the restatement as material, requests a full methodology reconciliation, and the audit timeline slips by six weeks. The team thought they were managing emissions. They were actually managing methodology documentation.

However, ESRS E1 disclosure consists of two things: the emissions inventory itself, and the methodological consistency that makes year-on-year comparison possible. Most teams optimize for the first—cleaner supplier data, higher primary-data share in Category 1, better utility bill coverage for Scope 2. But regulators, auditors, and the ESRS E1 standard itself judge the disclosure on the second: whether the calculation method, emission factors, and boundary definitions remain stable across reporting cycles, or whether changes are transparently documented and baseline years are restated when variance exceeds 5%.

The inventory on its own has no assurance value. Methodological consistency is what the auditor is verifying. A Scope 3 total calculated with DEFRA 2023 factors and one calculated with DEFRA 2025 factors are not comparable, even if the underlying activity data is identical. A Category 4 allocation rule that splits logistics emissions by revenue in year one and by mass in year two produces a trend that cannot be audited. The GHG Protocol Corporate Standard explicitly requires that "changes in calculation methodology, improvements in the accuracy of emission factors or activity data, or discovery of errors" trigger a base year recalculation—and under ESRS E1, any restatement that shifts baseline emissions by more than 5% must be disclosed with a full rationale [1].

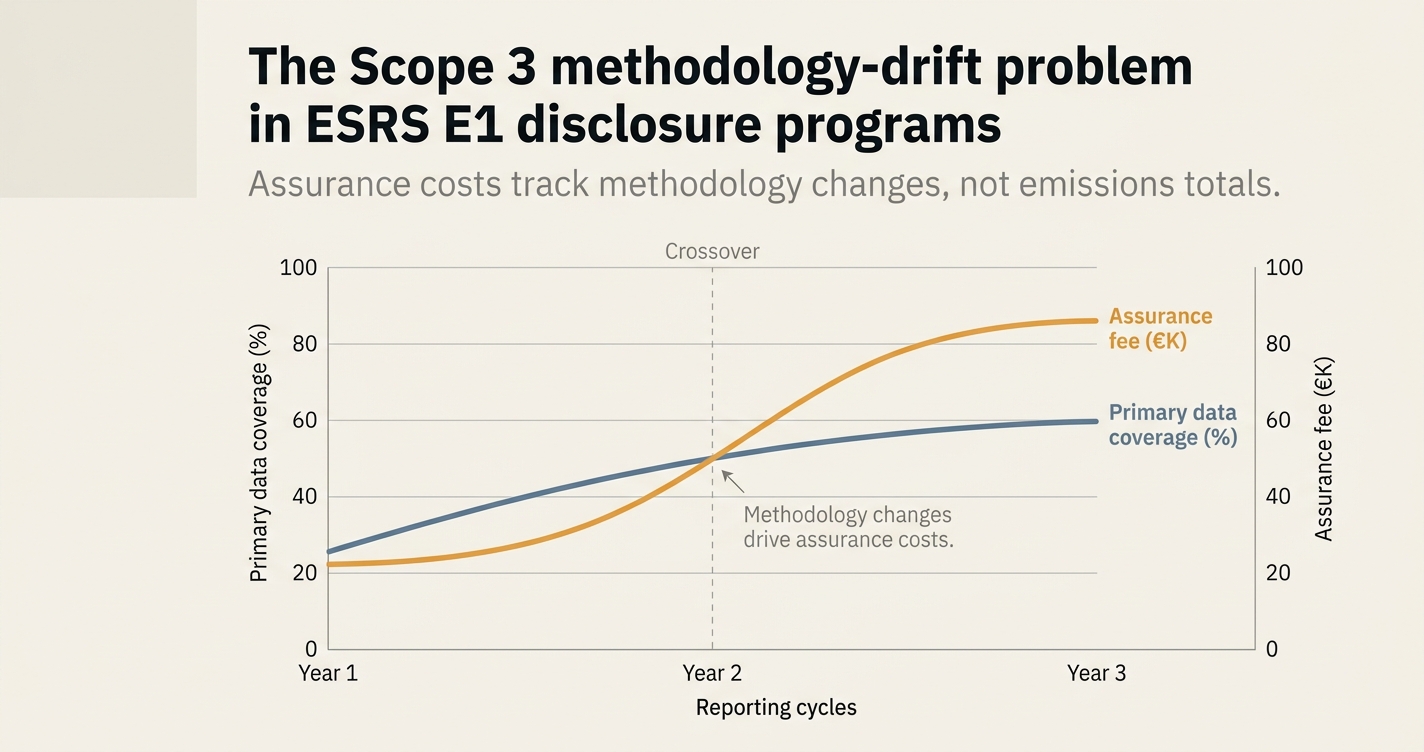

While supplier engagement platforms have made primary data collection cheaper, methodology governance has become more expensive. According to PwC's 2026 Sustainability Reporting Guide, assurance costs for Scope 3 disclosures are driven not by the size of the footprint but by the number of methodological changes between reporting years. If a mid-market manufacturer updates its Scope 3 calculation method twice in three years—once for revised emission factors, once for improved supplier data—the assurance partner may require a full historical restatement, which can add €40,000–€80,000 to the audit fee and delay opinion issuance by 4–8 weeks [2].

How do you solve this? I think the operators we work with treat methodology as infrastructure, not iteration. They lock emission factor datasets at the start of the reporting year, document every allocation rule in a version-controlled methodology note, and build a variance tracker that flags any calculation change likely to shift baseline emissions by more than 2%. For now, this approach seems to keep assurance cycles predictable and restatement risk contained. It also means the sustainability team spends less time defending retrospective changes and more time driving forward-looking reductions.

The shape of the argument, visualised below.

The three sources of methodology drift in Scope 3 disclosure

Methodology drift in Scope 3 reporting stems from three distinct sources, each with different assurance implications:

| Source of drift | Typical scenario | Baseline restatement trigger | Assurance impact |

|---|---|---|---|

| Emission factor updates | DEFRA publishes revised factors; UK electricity grid factor fell 14.5% in 2025 dataset | If factor change shifts baseline >5%, restatement required | Auditor requires reconciliation of old vs. new factors, year-by-year |

| Allocation rule changes | Category 4 logistics emissions allocated by revenue in year 1, by mass in year 2 | Any allocation method change requires restatement and disclosure | Full historical recalculation; assurance timeline may slip 4–6 weeks |

| Boundary expansion | New supplier tiers added to Category 1; previously excluded facilities brought into Scope 1 | Boundary expansion always triggers restatement if >5% variance | Auditor tests completeness of expanded boundary back to base year |

The first source—emission factor updates—is the most common and, paradoxically, the least problematic from an assurance perspective. The GHG Protocol explicitly allows emission factor updates without triggering a base year recalculation, provided the factors are applied to the same activity data and the change is disclosed. ESRS E1 AR 39(d) even encourages entities to use the most recent IPCC Global Warming Potential values and to document which GWP version the inventory is based on [3].

The second source—allocation rule changes—is where most assurance disputes occur. A sustainability team may refine its Category 4 allocation methodology to better reflect actual logistics intensity, but if the new rule is not applied retroactively, the year-on-year trend becomes non-comparable. ESRS E1 requires "consistent methodology across reporting years" and specifies that any change causing more than 5% variance in baseline emissions must be disclosed with a written rationale [4]. This is the primary driver of restatement cycles in second- and third-year ESRS filers.

The third source—boundary expansion—is the most disruptive. Adding a new supplier tier to Category 1, or bringing previously excluded facilities into the Scope 1 boundary, almost always shifts baseline emissions by more than 5%. Under both the GHG Protocol and ESRS E1, this requires a full baseline recalculation and transparent disclosure of what changed. The SBTi goes further: if a boundary change shifts baseline emissions by more than 5%, the target trajectory itself must be recalculated to maintain ambition level [5].

"Entities must first adhere to any specific reporting requirements prescribed by ESRS. In the absence of specific guidance in ESRS, entities must consider the principles and provisions of the GHG Protocol Corporate Standard and Scope 3 Standard." — PwC Sustainability Reporting Guide, Chapter 7, March 2026 [2]

The 5% materiality threshold and its assurance consequences

The 5% variance threshold appears in three places: the GHG Protocol Corporate Standard (base year recalculation guidance), the SBTi target-setting criteria (baseline restatement trigger), and implicitly in ESRS E1 (disclosure of significant methodology changes). But the threshold is not a permission to drift—it is a floor for mandatory restatement, not a ceiling for acceptable variance.

In practice, assurance partners treat any methodology change that shifts baseline emissions by 2–5% as a yellow flag. If the change is not documented in advance, or if the historical calculation cannot be reproduced with the new method, the auditor may expand the scope of evidence testing. This typically adds 20–40 hours of audit time and €8,000–€15,000 to the assurance fee. If the variance exceeds 5% and no restatement was prepared, the auditor may issue a qualified opinion or delay sign-off until the baseline is recalculated [2].

The SBTi adds an additional constraint: if a methodology change causes baseline emissions to increase by more than 5%, the target trajectory must be recalculated to maintain the same percentage reduction from the new baseline. This means a company with a 42% reduction target by 2030, originally set from a baseline of 100,000 tCO2e, must now achieve a 42% reduction from the restated baseline of 108,000 tCO2e—an absolute increase in the reduction obligation of 3,360 tCO2e. The methodology drift compounds into a delivery gap [5].

The primary-data share requirement under ESRS E1 and CSRD timelines

ESRS E1 does not mandate a minimum primary-data share for Scope 3 reporting, but it does require entities to disclose the proportion of emissions calculated using primary data versus secondary data (modeled or default factors). The standard also states that "data quality is expected to improve year on year" and that indefinite reliance on spend-based estimates is not considered sufficient [6].

This creates a second vector for methodology drift: as primary data coverage increases, the calculation method for specific Scope 3 categories shifts from spend-based to activity-based to supplier-specific. Each shift changes the emission intensity of the category, which in turn may trigger the 5% restatement threshold.

Example: A manufacturer reports Category 1 emissions of 18,500 tCO2e in year 1, using spend-based EEIO factors for 80% of the category and supplier-specific data for 20%. In year 2, the team collects supplier-specific data for 60% of the category. The new calculation shows Category 1 emissions of 14,200 tCO2e for the same procurement spend. The 23% reduction is not a real reduction—it is a methodology change. Under ESRS E1 and the GHG Protocol, the year 1 baseline must be recalculated using the year 2 method, or the trend must be disclosed as non-comparable [1][4].

DHL Group's 2025 ESRS E1 disclosure illustrates the scale of this issue. In fiscal 2025, the company reported that 95.1% of Scope 1 and 2 emissions were calculated using primary data, but only 19.9% of Scope 3 emissions used primary data. Of the remaining 80.1%, 60.2% used modeled data (activity-based factors) and 19.9% used default data (spend-based factors). The methodology note specifies that any shift from default to modeled, or modeled to primary, requires a retrospective recalculation if the variance exceeds 5% [7].

The Scope 3 Standard revision and its implications for methodology governance

In March 2026, the GHG Protocol published a Phase 1 progress update for the Scope 3 Standard revision, noting that the core 15 categories will remain intact but that methodology guidance will be updated to reflect the ISO-GHG Protocol partnership announced in September 2025. The update specifically flags that financial institutions following PCAF Part A must now consider the December 2025 version, which added three asset classes and refined the data quality scoring system [8].

The practical implication: any entity that built its Scope 3 inventory using PCAF Part A (December 2022) and has not yet updated to the December 2025 version is now carrying a methodology-drift risk. The revised asset classes and data quality tiers may shift the reported emissions for Category 15 (investments), and if the variance exceeds 5%, a baseline restatement is required. For financial institutions with ESRS E1 filings due in 2026 or 2027, this means the methodology lock must happen before the revised PCAF guidance is applied—or the baseline must be recalculated retroactively [8].

The ISO-GHG Protocol partnership also signals a longer-term trend: harmonization of calculation methods across jurisdictions. This reduces future methodology drift (fewer competing standards) but increases near-term restatement risk (companies must migrate from legacy methods to the harmonized standard). The Phase 1 update notes that a formal public consultation process will follow ISB approval, likely in Q3 2026, with final guidance expected in 2027 [8].

Why methodology governance is now a Category 1 assurance workstream

In Emission3's work with mid-market manufacturers preparing for ESRS E1 limited assurance, methodology governance has moved from a post-calculation documentation task to a pre-cycle scoping exercise. The approach we see working:

-

Emission factor lock at fiscal year start. Teams select the emission factor dataset (DEFRA, EPA, ecoinvent) and GWP values (IPCC AR5 or AR6) at the beginning of the reporting year, and lock them for the entire cycle. Factor updates are applied prospectively, not retrospectively, unless the variance exceeds 5%.

-

Allocation rule version control. Every Scope 3 category that requires an allocation rule (e.g., splitting logistics emissions across product lines, or allocating upstream energy across facilities) has a documented allocation method with a version number and effective date. Rule changes are logged in a methodology change register and tested against the 5% restatement threshold before implementation.

-

Boundary change impact modeling. Before expanding the reporting boundary—adding a new supplier tier to Category 1, or including previously excluded facilities in Scope 1—the team models the historical impact. If the boundary expansion would shift baseline emissions by more than 2%, the restatement is prepared in advance, not after the auditor flags it.

-

Primary data share roadmap. The team documents a multi-year roadmap for increasing primary data coverage, with specific milestones (e.g., 30% of Category 1 by 2026, 50% by 2027). Each milestone includes a variance test: if the new primary data shifts the category total by more than 5% compared to the spend-based estimate, the baseline is restated prospectively, and the methodology note is updated.

This is not perfectionism—it is assurance logistics. A methodology change register cuts the evidence-testing phase of the assurance cycle from 8 weeks to 3 weeks, because the auditor can trace every variance back to a documented methodology decision. It also reduces restatement cycles from "discovered during audit" to "planned during baseline year," which keeps assurance fees predictable.

The assurance-fee multiplier for undocumented methodology changes

PwC's 2026 Sustainability Reporting Guide notes that assurance costs for Scope 3 disclosures are driven by the number of methodological changes between reporting years, not the size of the footprint. A company with 200,000 tCO2e Scope 3 and zero methodology changes may have a lower assurance fee than a company with 50,000 tCO2e Scope 3 and three undocumented allocation rule changes [2].

The fee multiplier works as follows:

- Zero methodology changes year-over-year: Base assurance fee, typically €20,000–€40,000 for limited assurance on Scope 1, 2, and material Scope 3 categories.

- One documented methodology change with retrospective restatement: +30–50% fee increase, timeline extension of 2–3 weeks.

- Two or more undocumented methodology changes discovered during audit: +80–120% fee increase, timeline extension of 4–8 weeks, risk of qualified opinion.

The financial materiality of methodology drift is not in the emissions variance itself—it is in the assurance cost and timeline risk. A company that restates its baseline from 47,300 tCO2e to 51,800 tCO2e (9.5% increase) does not face a tariff penalty or a compliance fine. But if that restatement was not prepared in advance, and the auditor discovers it during evidence testing, the assurance cycle extends by 6 weeks and the fee increases by €50,000. For a mid-market manufacturer with a Q1 CSRD filing deadline, that delay can push the opinion issuance into the following quarter, which in turn delays the sustainability report publication and may trigger exchange listing penalties [2].

How Emission3 fits: methodology governance as deterministic infrastructure

Emission3's compliance infrastructure treats methodology governance as a deterministic workflow, not a documentation artifact. Every emissions calculation in the system carries a methodology fingerprint: the emission factor dataset, the GWP version, the allocation rule ID, and the primary/secondary data flag. When a team updates an emission factor or refines an allocation rule, the system models the historical variance before applying the change.

If the modeled variance exceeds 2% for any Scope 3 category, the platform flags a potential restatement and generates a methodology change memo with:

- The old and new calculation methods, side by side.

- The category-level variance for each historical year.

- A recommendation to restate or disclose as non-comparable.

- An export-ready methodology note for the ESRS E1 filing.

This approach cuts the restatement-cycle time from 4–8 weeks (manual recalculation + auditor reconciliation) to 1–2 weeks (automated variance modeling + pre-built evidence pack). For clients with multiple methodology changes per year—common in years 2 and 3 of ESRS reporting—it also reduces assurance fees by 20–40%, because the auditor receives a version-controlled methodology change log with full lineage, not a spreadsheet with unexplained variances [1][2].

The system also exports a methodology consistency report for the assurance partner, showing:

- Which emission factors were used in each reporting year, with source references.

- Which allocation rules were applied to each Scope 3 category, with version numbers.

- Which boundary changes occurred, with modeled impact on baseline emissions.

- Which primary data share milestones were met, with variance analysis.

This is not an assurance-readiness checklist—it is the assurance evidence itself, structured for auditor review.

What to start this week

If you are building or refining an ESRS E1 disclosure program, methodology governance is not a year-end documentation task—it is a fiscal-year-start infrastructure decision. Three actions that reduce restatement risk and keep assurance cycles predictable:

-

Lock your emission factor dataset and GWP values for the reporting year. Select DEFRA, EPA, or ecoinvent at the start of the fiscal year, document the version, and do not update mid-cycle unless a factor change shifts baseline emissions by more than 5%. The assurance partner will test factor consistency first.

-

Version-control your Scope 3 allocation rules. Every category that requires allocation (Category 4 logistics, Category 3 upstream energy, Category 1 supplier-tier splits) should have a documented allocation method with an effective date. Log any rule changes in a methodology change register before applying them, not after the auditor flags the variance.

-

Build a primary data share roadmap with variance thresholds. Document your plan to increase primary data coverage over the next three reporting cycles, with specific milestones and variance tests. If hitting a milestone would shift a category total by more than 5%, plan the restatement in advance, and include it in your methodology note.

Methodology drift is not a theoretical risk—it is the primary driver of assurance delays and fee escalation in second- and third-year ESRS filers. The cost is measurable: €40,000–€80,000 per undocumented methodology change, and a 4–8 week timeline extension. The mitigation is infrastructure: treat methodology as version-controlled, auditor-ready, and locked at the start of each reporting cycle.

If you are preparing for ESRS E1 limited assurance in 2026 or 2027, or refining your Scope 3 inventory for CSRD compliance, book a CBAM readiness and workflow-review call with the Emission3 team. We walk through your current methodology, model the restatement risk for any planned changes, and scope the infrastructure needed to keep assurance cycles predictable [9].

References & Sources

External Sources

- [1]What Are Scopes 1, 2 and 3 Emissions? The Ultimate Guide (2026)

Comprehensive breakdown of Scope 1, 2, and 3 emissions under the GHG Protocol Corporate Standard, including common errors in methodology consistency and the implications of outdated emission factors.

- [2]SRG Chapter 7: Greenhouse gas emissions reporting (PwC, March 2026)

PwC's sustainability reporting guide covering ESRS E1 GHG emissions disclosure requirements, including minimum boundaries for Scope 3 reporting, assurance scope considerations, and the hierarchy of guidance entities must follow.

- [3][Draft] ESRS E1 - Climate Change (EFRAG, November 2025)

EFRAG's draft ESRS E1 standard detailing GHG emissions reporting requirements, including guidance on using the most recent IPCC Global Warming Potential values and documenting methodology changes.

- [4]The GHG protocol explained: A complete guide to corporate emissions reporting (Coolset)

Explanation of how the GHG Protocol connects to CSRD reporting requirements, including ESRS E1's requirement for consistent methodology across reporting years and transparent exclusion rationale for non-applicable Scope 3 categories.

- [5]All 15 Scope 3 Categories Explained (2026) (Normative)

Detailed breakdown of all 15 Scope 3 categories under the GHG Protocol, including SBTi requirements for baseline restatement when methodology changes cause more than 5% variance in base year emissions.

- [6]Environment (ESRS E1) - DHL Group Q4 2025

DHL Group's ESRS E1 disclosure showing primary data share for Scope 1, 2, and 3 emissions, illustrating the scale of secondary data reliance in Scope 3 reporting and the methodology for calculating market-based effects.

- [7]The GHG Protocol Scope 3 Revision: What the March 2026 update means (ClimateCAMP)

Analysis of the GHG Protocol Scope 3 Standard revision process, including the requirement to label verified categories and the practical implications of increasing primary data coverage year-on-year.

- [8]Scope 3 Standard Revisions Phase 1 Progress Update (GHG Protocol, March 2026)

GHG Protocol's Phase 1 progress update on the Scope 3 Standard revision, detailing the ISO-GHG Protocol partnership and noting that the 15 categories will remain intact while methodology guidance is updated.

Related Content

- [9]Book a CBAM readiness call

All Emission3 customers start with a CBAM readiness and workflow-review call. We map suppliers, identify gaps, model restatement risk for methodology changes, and scope the compliance infrastructure needed to keep assurance cycles predictable.

- [10]Reporting & filings

Emission3's reporting infrastructure generates CSRD / CBAM / SB 253 filings with full methodology lineage, version-controlled allocation rules, and auditor-ready evidence packs. Every number is reproducible, with deterministic calculation paths from source document to filing.