The audit-trail gap in third-party CBAM verification engagements

The audit-trail gap in third-party CBAM verification engagements

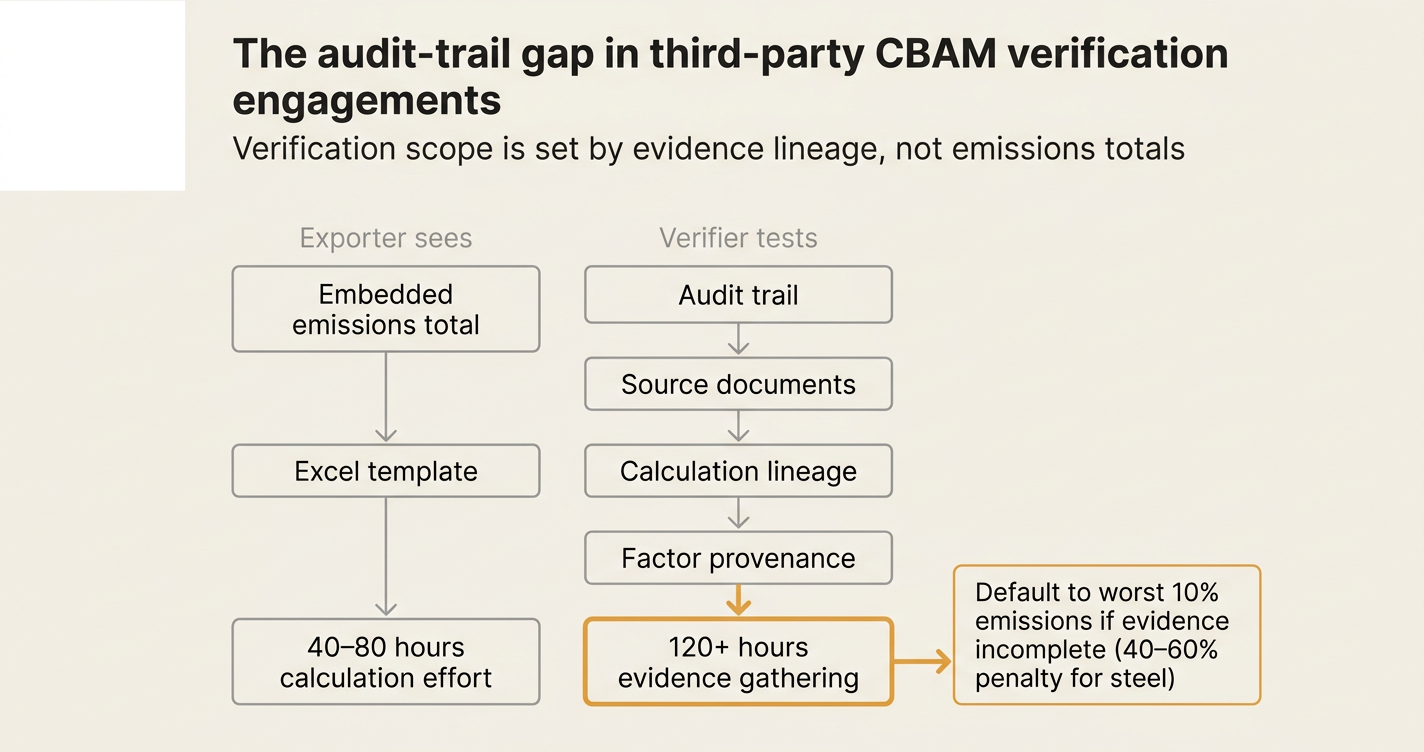

Here's the issue: Non-EU exporters preparing for CBAM quarterly filings typically budget 40-80 hours of internal effort to calculate embedded emissions totals for steel, cement, aluminium, fertilisers, electricity, and hydrogen. The calculation itself—applying production-route emission factors to tonnage shipped—appears straightforward. Many teams assume that third-party verification, required under Article 8 of the CBAM Regulation, will follow the same pattern: a brief review, a stamp, done. But auditors are not reviewing calculations. They are reviewing the evidence that supports every line item in the calculation.

However, CBAM verification consists of two things: the embedded emissions totals that appear in the quarterly filing, and the document-level audit trail that traces every number back to a source invoice, utility bill, or bill of materials. The first is what exporters see when they open the Excel template. The second is what the accredited verifier opens when they begin substantive testing under International Standard on Assurance Engagements 3410 (ISAE 3410), the framework for greenhouse gas assurance engagements that remains applicable for CBAM work until the transition to International Standard on Sustainability Assurance 5000 in December 2026.

The embedded emissions total on its own has no value to the verifier. The audit trail—line-item evidence, calculation lineage, methodology documentation, control environment—is what the verifier is actually testing. An exporter can submit a perfectly accurate tonnage figure for Scope 1 process emissions from a steel mill, but if the verifier cannot trace that figure to a time-stamped fuel consumption record, a calibrated meter log, and a documented emission factor source, the figure is treated as unverified. Under Article 7(6) of the CBAM Regulation, unverified emissions default to the worst-performing 10% of EU installations in the same product category, which for steel can mean an embedded emissions value 40-60% higher than the exporter's actual installation value.

While the cost of calculating embedded emissions has become cheaper—spreadsheet templates, factor libraries, consultant-led workshops—the cost of assembling the audit trail has become more expensive. If an exporter's internal controls are manual (emails, PDFs, handwritten logs), and the verifier samples 30-50 line items per product category as required under limited assurance procedures, the evidence-gathering effort can exceed 120 hours, double the original calculation budget. The audit-trail gap is not a documentation problem. It is a workflow architecture problem: the exporter's internal systems were not designed to produce verifier-ready evidence packs at the transaction level.

How do you solve this? I think the operators we work with have converged on a document-first ingestion architecture: every invoice, bill of materials, utility bill, and customs declaration is captured at the point of receipt, tagged with product-level metadata, and linked to the corresponding CBAM filing line item. The architecture is not a post-calculation add-on. It is the calculation substrate. When the verifier requests evidence for a sampled line item, the system exports the source document, the calculation lineage, and the factor provenance in a single artifact. The audit trail is built into the workflow, not bolted on at verification time.

The shape of the argument, visualised below.

What Article 8 actually requires

Article 8 of the CBAM Regulation, titled "Verification of embedded emissions," establishes the procedural requirements for third-party assurance. The text is specific:

"Before submitting the CBAM declaration referred to in Article 6, the declarant shall obtain a verification report from an accredited verifier certifying that the embedded emissions in the goods are determined in accordance with the methods laid down in this Regulation. The verifier shall examine whether the information in the report referred to in Article 7(5) is free from material misstatements, whether it is in conformity with this Regulation and whether it is supported by reliable and credible data, including through on-site visits."

The clause binds three parties: the declarant (the EU importer or indirect customs representative), the accredited verifier (an independent auditor accredited under the framework set out in Article 18), and the exporter (who provides the underlying emissions data). The binding moment is "before submitting the CBAM declaration," which for quarterly filings means within one month of the end of each quarter (Article 6(2)).[1] The verifier's examination scope is not limited to the emissions total. It extends to "the information in the report," which under Article 7(5) includes production processes, emission factors, precursor materials, calculation methods, and monitoring approaches.[2]

What this means for you

| Stakeholder | Regulatory trigger | Verification scope | Timeline | Default-value penalty if verification fails |

|---|---|---|---|---|

| Non-EU exporter (steel, cement, aluminium, fertilisers) | First CBAM quarterly filing in Q1 2026 | Embedded emissions, calculation methods, source documents | Verification report due before quarterly declaration (within 1 month of quarter end) | Default to worst-performing 10% of EU installations (40-60% emissions increase for steel)[3] |

| EU importer (declarant) | Quarterly CBAM declaration under Article 6 | Verification report from accredited verifier must be obtained before submission | Within 1 month of quarter end | Financial liability for CBAM certificates at default emissions values |

| Third-party auditor (accredited verifier) | Engagement begins when exporter requests verification | Full audit trail: invoices, utility bills, meter logs, factor sources, control environment | Engagement duration typically 4-8 weeks for first filing | Verifier's accreditation at risk if engagement does not meet ISAE 3410 or ISSA 5000 requirements |

| EU competent authority | Review of CBAM declarations and verification reports | Compliance with Article 8 verification requirements | Ongoing, with enforcement beginning after transitional period (2026-2027) | Penalties for non-compliance under Article 26 (€10-€50 per unreported tonne CO₂e) |

The table makes the timeline explicit: verification is not an annual event. It is a quarterly requirement, and the audit trail must be production-ready every 90 days.

The ISAE 3410 framework and the transition to ISSA 5000

ISAE 3410, Assurance Engagements on Greenhouse Gas Statements, is the International Auditing and Assurance Standards Board (IAASB) standard that has governed GHG verification work since 2012. The standard defines two levels of assurance: limited assurance ("nothing has come to our attention that causes us to believe the GHG statement is materially misstated") and reasonable assurance ("in our opinion, the GHG statement is free from material misstatement").[4] CBAM verification under Article 8 does not specify a required assurance level, but the language "free from material misstatements" and the requirement for on-site visits suggest that reasonable assurance is the de facto expectation for installations seeking to avoid default values.

ISAE 3410 is being withdrawn on December 15, 2026, when ISSA 5000, General Requirements for Sustainability Assurance Engagements, becomes effective. ISSA 5000 incorporates the core requirements of ISAE 3410—systematic process, documented evidence, population completeness—but expands the scope to all sustainability information, not just GHG data.[5] For CBAM exporters, the transition means that verification engagements beginning in 2027 will be conducted under ISSA 5000, which has 212 requirements compared to ISAE 3410's approximately 100. The increase is not administrative burden for its own sake. It reflects the IAASB's recognition that sustainability assurance engagements require more granular procedural guidance than financial audits, particularly around evidence sourcing, materiality judgments, and control environment assessment.[6]

The implication: exporters who build their audit trails under ISAE 3410 principles in 2026 will not need to rebuild them when ISSA 5000 takes effect. The fundamental requirement—line-item evidence, calculation lineage, factor provenance—is identical across both standards.

The sampling problem at Scope 3 scale

Third-party auditors conducting CBAM verification engagements under limited or reasonable assurance must perform substantive testing on a sample of the exporter's emissions data. ISAE 3410 does not prescribe a specific sample size, but industry practice for limited assurance typically involves reviewing 20-30% of the population by value, and for reasonable assurance, 50-70%.[7] For a steel exporter filing CBAM declarations for 12 product categories across 4 production routes, substantive testing might require evidence for 40-60 line items per quarter.

The problem: most exporters do not maintain line-item evidence. They maintain aggregated monthly totals ("total electricity consumption for January: 1,200 MWh") or category-level summaries ("Scope 1 emissions from blast furnace: 85,000 tCO₂e"). When the verifier requests evidence for a specific line item—say, the embedded emissions in 500 tonnes of hot-rolled coil shipped to Rotterdam on March 15—the exporter must reconstruct the calculation from emails, PDFs, and handwritten production logs. The reconstruction effort is manual, time-intensive, and error-prone. If the exporter cannot produce the evidence within the engagement timeline (typically 4-8 weeks for a first filing), the verifier cannot issue a clean opinion, and the exporter defaults to the worst-performing 10% emission factor.

The sampling problem is structural: the exporter's internal systems were not designed to produce auditor-ready evidence packs at the transaction level. Solving it requires workflow re-architecture, not better spreadsheet hygiene.

Methodology consistency and the year-over-year comparison requirement

Article 7(6) of the CBAM Regulation requires that embedded emissions be calculated "using a consistent methodology over time." The phrase is procedural, not merely aspirational. When a verifier conducts a CBAM engagement in Q2 2026 and returns for Q3 2026, they must assess whether the exporter's calculation methods—emission factors, allocation rules, system boundaries—have remained consistent across the two periods. If the exporter changed the allocation method for electricity consumption between direct and indirect processes, or switched from supplier-specific emission factors to industry averages, the verifier must document the change, assess its materiality, and determine whether the change was justified and appropriately disclosed.[8]

The year-over-year comparison requirement creates a hidden cost: the first verification engagement sets the methodological baseline for all subsequent engagements. If the exporter's Q1 2026 filing uses a manual, spreadsheet-based workflow with informal documentation, that workflow becomes the de facto standard. When the exporter attempts to upgrade the workflow in Q2 2026—introducing a structured database, automated factor lookups, or a compliance platform—the verifier treats the upgrade as a methodology change, which triggers additional testing procedures, expanded engagement scope, and higher fees. The cost of the workflow upgrade is not just the software license or consultant time. It is the incremental audit cost of validating the new methodology against the old baseline.

The solution: design the workflow correctly the first time, so that the Q1 2026 verification engagement establishes a deterministic, document-first baseline that scales across all subsequent quarters without triggering methodology-change reviews.

Population completeness and the control environment

ISAE 3410 and ISSA 5000 both require the auditor to assess whether "all relevant emissions sources have been identified" and whether "controls are designed effectively" to prevent material misstatements.[9] For CBAM verification, this means the auditor must evaluate the exporter's internal control environment: Are production logs captured systematically? Are utility bills reconciled monthly? Are emission factors sourced from accredited databases? Are calculation errors detected before the filing is submitted?

The control environment assessment is not a checklist exercise. It is a judgment call. If the exporter's workflow is manual and informal—emission factors stored in emails, production logs maintained in handwritten notebooks, calculations performed in individual analyst spreadsheets—the auditor must increase the substantive testing sample size to compensate for the weak control environment. A weak control environment does not make verification impossible, but it makes verification expensive. The auditor's fees scale with the perceived risk of material misstatement, and a manual workflow signals high risk.

Conversely, if the exporter's workflow is structured and deterministic—source documents ingested at point of receipt, calculations performed by a documented engine, outputs automatically linked to evidence—the auditor can reduce the substantive testing sample size, because the strong control environment reduces the risk of undetected errors. The control environment is not a compliance artifact. It is a cost lever.

How Emission3 fits

Emission3 is designed as a document-first ingestion architecture with deterministic calculation lineage and verifier-ready exports. When an exporter uploads an invoice, bill of materials, utility bill, or customs declaration, the platform tags the document with product-level metadata, extracts the relevant line items (tonnage, energy consumption, production route), applies the appropriate emission factors from the EU's default-value database or the exporter's installation-specific data, and links the calculation to the source document. The calculation is deterministic: every number is reproducible, and the lineage from source document to CBAM filing line item is traceable in a single click.

When the third-party auditor begins the verification engagement, Emission3 exports an evidence pack for each sampled line item: the source document (PDF), the extracted data (JSON), the calculation steps (formula with factor sources), and the resulting embedded emissions total (tCO₂e). The evidence pack is structured in the format that ISAE 3410 and ISSA 5000 require: line-item granularity, factor provenance, calculation reproducibility. The auditor does not need to request additional documents or reconstruct the calculation manually. The audit trail is pre-built.

For the exporter, the benefit is not faster verification. The benefit is predictable verification scope. Because the control environment is strong and the evidence is line-item complete, the auditor can perform limited assurance with a smaller sample size, which reduces the engagement duration and fee. The workflow architecture reduces the cost of the audit, not by cutting corners, but by eliminating the manual evidence-gathering effort that inflates audit hours in manual workflows.

For the auditor, the benefit is reproducibility. The auditor can replay any calculation, inspect the factor source, and validate the allocation rules without relying on exporter interviews or email threads. The engagement is faster because the evidence is structured, not because the evidence is thinner. For auditors conducting multiple CBAM verification engagements per quarter, the reproducibility of the Emission3 workflow reduces the per-engagement cost, which makes CBAM verification commercially viable for mid-market exporters who cannot afford the €15,000–€30,000 fees typical of bespoke assurance engagements.[10]

The Emission3 architecture is not a workaround for Article 8 requirements. It is a direct implementation of the ISAE 3410 principles that Article 8 verification engagements must follow: line-item evidence, calculation lineage, population completeness, control environment. The platform is built for the audit, not as a user-facing dashboard that happens to produce audit-adjacent outputs.

What to do next

If you are a non-EU exporter preparing for CBAM quarterly filings beginning in Q1 2026, or an EU importer working with exporters to obtain verification reports under Article 8, the workflow re-architecture decision is time-sensitive. The Q1 2026 verification engagement will establish the methodological baseline for all subsequent quarters. If that baseline is manual and informal, every subsequent quarter will incur incremental audit costs. If the baseline is structured and deterministic, the audit costs stabilise.

If you are a third-party auditor preparing to conduct CBAM verification engagements under ISAE 3410 or ISSA 5000, the evidence format matters. Exporters who use document-first ingestion architectures like Emission3 produce line-item evidence packs that reduce your substantive testing effort. Exporters who use spreadsheet-based workflows require you to reconstruct the audit trail manually, which increases your engagement hours and reduces your margin. The commercial viability of mid-market CBAM verification work depends on the exporter's workflow architecture, not just their emissions calculation accuracy.

Emission3 offers a CBAM readiness conversation for exporters and auditors preparing for the Q1 2026 filing cycle. The conversation is workflow-focused: how to structure the document ingestion process, how to build the calculation lineage, how to export the evidence pack in the format that ISAE 3410 and ISSA 5000 require. The goal is not to sell software. The goal is to help you design the workflow correctly the first time, so that the Q1 2026 verification engagement establishes a scalable, auditor-ready baseline that reduces your verification costs across all subsequent quarters. Book a CBAM readiness conversation at /contact.

References & Sources

External Sources

- [1]CBAM Regulation Article 6 and Article 8 quarterly filing timelines

Reference implementation of CBAM quarterly filing timelines and verification requirements under Article 8, including the one-month deadline after quarter end.

- [2]CBAM Article 7(5) reporting requirements

Documentation of CBAM reporting requirements under Article 7(5), including production processes, emission factors, and calculation methods that must be verified.

- [3]CBAM default values and worst-performing 10% penalty

Analysis of CBAM default-value penalties under Article 7(6), showing 40-60% emissions increase for steel when verification fails.

- [4]ISAE 3410 Assurance Engagements on Greenhouse Gas Statements

IAASB standard ISAE 3410 defining limited and reasonable assurance frameworks for GHG verification, applicable to CBAM engagements until December 2026.

- [5]ISSA 5000 effective date and transition from ISAE 3410

IAASB approval of ISSA 5000, effective December 15, 2026, replacing ISAE 3410 for sustainability assurance engagements including CBAM verification.

- [6]ISSA 5000 requirement count and procedural expansion

California Air Resources Board documentation noting ISSA 5000 has 212 requirements, more than double ISAE 3000, reflecting increased procedural rigor for sustainability assurance.

- [7]ISAE 3410 sampling and substantive testing procedures

Industry guidance on ISAE 3410 sampling practices for limited and reasonable assurance, including typical sample sizes for GHG verification engagements.

- [8]Methodology consistency requirements in ISAE 3410

Example ISAE 3410 assurance statement showing methodology consistency assessment and year-over-year comparison requirements.

- [9]Population completeness and control environment in ISAE 3410

Australian Auditing and Assurance Standards Board documentation of ISAE 3410 requirements for population completeness and control environment assessment.

- [10]CBAM verification cost benchmarks for mid-market exporters

Third-party assurance cost analysis for sustainability reporting, including CBAM verification fee ranges and cost drivers for mid-market companies.

Related Content

- [11]Audit-ready exports in Emission3

Emission3 solution page for auditors and CFOs, demonstrating the document-first evidence lineage artifact and verifier-ready export format.

- [12]The Emission3 AI layer

Technical documentation of the deterministic LLM layer that enables line-item document ingestion and calculation reproducibility for audit replay.