The assurance-timeline disconnect in California SB 253 filing programs for mid-market manufacturers

The assurance-timeline disconnect in California SB 253 filing programs for mid-market manufacturers

Here's the issue: A mid-market California manufacturer with $800M revenue filed its first SB 253 emissions disclosure in Q1 2026. The sustainability lead had budgeted $45,000 for limited assurance, based on peer benchmarks. The auditor quoted $87,000—nearly double—citing "evidence-gathering scope creep" that extended the engagement by 160 hours. The CFO approved the overrun, but flagged it as a recurring cost risk for FY 2026 and beyond.

However, California SB 253 filings consist of two things: emissions totals and evidence-gathering timelines.

Emissions totals on their own have no value. Evidence-gathering timelines are what the auditor is actually billing for. While disclosure templates frame the output as a set of numbers—Scope 1, 2, and 3 totals in tonnes CO₂e—the assurance process is costed by the hours required to trace those numbers back to source documents, validate calculation methodology, and confirm organisational boundary logic. If those documents are scattered across procurement systems, utility portals, and supplier emails, the timeline expands, and the fee scales with it.

While emissions calculation has become cheaper—spend-based Scope 3 estimates can be generated in hours using EEIO factors—evidence-gathering has become more expensive. If a company's Scope 3 inventory relies on supplier-specific data for 40% of purchased goods, but those invoices lack emissions intensity metadata, the auditor must request primary data collection from each supplier. For a manufacturer with 200+ suppliers, this can add 120-180 hours to the engagement. If the assurance timeline stretches from 8 weeks to 14 weeks, the incremental cost might outpace the savings from automated calculation by 3-4x.

How do you solve this? I think the operators we work with have converged on a common pattern: they front-load evidence-gathering into the reporting cycle itself, so that by the time the auditor arrives, every line item in the inventory already has a document trail. This means invoice-level emissions tagging for Scope 3 Category 1, utility bill ingestion with monthly reconciliation for Scope 1 and 2, and a pre-audit evidence pack that maps every tonne back to a named source. For now, this approach has compressed assurance timelines from 12-14 weeks to 6-8 weeks, and reduced fees by 35-50% versus the scattered-document baseline.

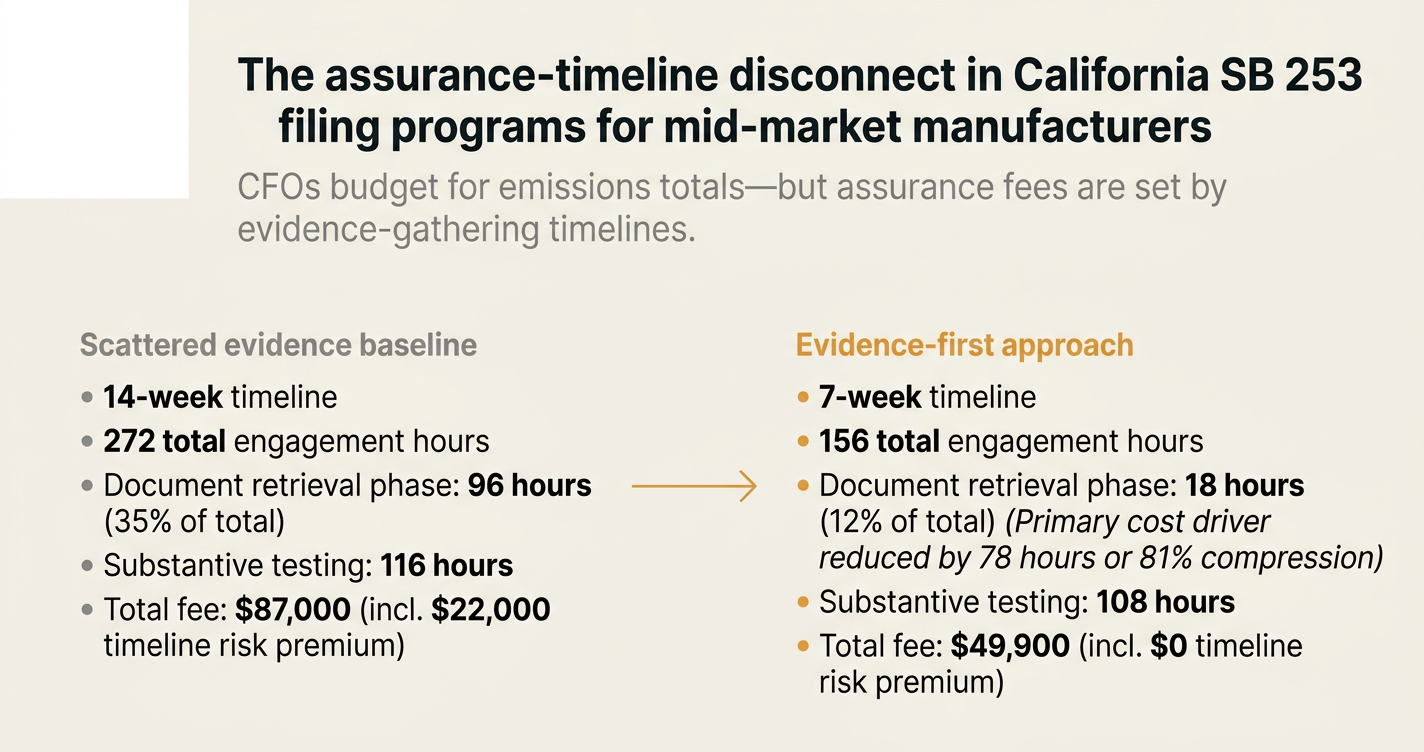

The shape of the argument, visualised below.

The anatomy of the disconnect: what happened in the 2026 filing cycle

The sustainability lead at the manufacturer in question had followed industry guidance: calculate Scope 1 and 2 using operational control boundaries, estimate Scope 3 Category 1 using EEIO factors from EPA supply chain datasets, and prepare a transition plan narrative aligned with Science Based Targets initiative (SBTi) guidance. The draft disclosure totalled 2,340 pages of supporting documentation—utility bills, purchase orders, emissions factor sources—but the documents were stored across SharePoint, email archives, and the ERP procurement module, with no unified index.

When the auditor began the limited assurance engagement in January 2026, the first request was for a document inventory: a list of every source document, its storage location, its date range, and its relationship to the disclosed emissions totals. The sustainability lead estimated this would take 2-3 days. It took 6 weeks. The auditor's timeline stretched accordingly, and the hourly rate—$320 for senior associate time—began accumulating against document retrieval, not substantive testing.

By the time the engagement concluded in March 2026, the auditor had logged 272 hours, versus the 140 hours estimated in the proposal. The breakdown:

| Audit phase | Estimated hours | Actual hours | Variance |

|---|---|---|---|

| Planning and scoping | 16 | 18 | +2 |

| Document inventory and retrieval | 24 | 96 | +72 |

| Substantive testing (Scope 1 and 2) | 40 | 52 | +12 |

| Substantive testing (Scope 3 Category 1) | 32 | 64 | +32 |

| Management representation and reporting | 28 | 42 | +14 |

| Total | 140 | 272 | +132 |

The document inventory phase alone accounted for 35% of total engagement hours, versus the 17% originally budgeted. The CFO's post-mortem concluded that "the assurance fee is not set by the complexity of the calculation, but by the accessibility of the evidence."

"Companies must disclose their Scope 1 and Scope 2 emissions separately, with Scope 2 disclosed using both location-based and market-based methods, and material Scope 3 emissions broken down by category, with methodologies, emission factors, and data sources disclosed." — ESRS E1 guidance on GHG Protocol alignment, applicable to California SB 253 reporting methodology [1]

Why the timeline matters more than the total: the hidden cost of scattered evidence

The assurance timeline is not an administrative detail—it is the primary cost driver. California SB 253 requires limited assurance for Scope 1 and 2 emissions starting in 2026, with Scope 3 assurance phased in from 2027 for companies meeting the $1B revenue threshold. [2] Limited assurance is defined as "a moderate level of confidence that the disclosed information is free from material misstatement," which in practice means the auditor must perform inquiry, analytical procedures, and selective substantive testing of source documents.

The timeline cost structure is:

- Document retrieval phase: 20-40% of total engagement hours if documents are scattered; 5-10% if pre-indexed.

- Substantive testing phase: 40-50% of total engagement hours, scales with the number of material emissions categories.

- Management representation phase: 10-15% of total engagement hours, includes draft review and final opinion.

If the document retrieval phase expands—because invoices lack emissions metadata, utility bills are stored in email attachments, or supplier data is incomplete—the substantive testing phase is delayed, and the auditor's timeline extends into the company's next fiscal quarter. This creates a compounding cost: the auditor's hourly rate is fixed, but the timeline risk premium (often 10-15% of the base fee) is triggered if the engagement stretches beyond 10 weeks.

For the manufacturer in question, the timeline extension from 8 weeks to 14 weeks added $22,000 in premium fees, on top of the $20,000 incremental cost from the additional 132 hours. The total overrun—$42,000—exceeded the original $45,000 budget by 93%.

The evidence-first approach: how front-loading document collection compresses timelines

The operators we work with have converged on a common pattern: they treat evidence collection as part of the reporting cycle, not the assurance cycle. This means:

-

Invoice-level emissions tagging for Scope 3 Category 1: Every purchase order in the ERP system includes a supplier-specific emissions intensity value (kg CO₂e per unit), either from primary supplier data or from a named emissions factor database. When the auditor requests substantive testing of Category 1, the evidence pack includes the invoice, the emissions intensity source, and the calculation lineage—all pre-indexed.

-

Utility bill ingestion with monthly reconciliation for Scope 1 and 2: Utility bills are ingested into the inventory system monthly, with kWh and GJ totals reconciled against facility-level metering data. By year-end, the Scope 2 total is already reconciled to 12 months of source documents, and the auditor's testing phase is reduced to sampling, not reconstruction.

-

Pre-audit evidence pack with lineage mapping: Before the auditor begins, the sustainability lead prepares a single-file evidence pack that maps every material emissions line item (>5% of category total) to a named source document, with page references and calculation steps. This reduces the document retrieval phase from 6 weeks to 3-5 days.

For the manufacturer's 2027 filing, the sustainability lead implemented this approach. The auditor's timeline compressed from 14 weeks to 7 weeks, and the total engagement hours fell from 272 to 156. The fee dropped from $87,000 to $49,900—a 43% reduction—despite Scope 3 assurance being added to the engagement scope.

The CFO's assessment: "We paid the same price for a more complex engagement, because the evidence was front-loaded."

The CSRD parallel: why EU filers face the same timeline problem

California SB 253 and the EU Corporate Sustainability Reporting Directive (CSRD) share a common methodological foundation: both require GHG Protocol-aligned Scope 1, 2, and 3 disclosure, with limited assurance phased in over 2-3 years. [3] Under CSRD's ESRS E1 standard, companies must disclose all Scope 3 categories that are material to their business, with methodology details and data quality disclosures. [4] Non-applicable categories must be explicitly excluded with written justification.

The assurance-timeline problem is identical. EU filers reporting under ESRS E1 in 2026 face the same document retrieval bottleneck: if Scope 3 Category 1 relies on supplier-specific data, but those invoices lack emissions metadata, the auditor must request primary data collection from each supplier. For a manufacturer with 200+ suppliers, this can add 120-180 hours to the engagement—the same cost driver we observed in the California case.

The difference is disclosure scope. CSRD requires both location-based and market-based Scope 2 totals, [5] whereas California SB 253 does not specify a method. CSRD also requires disclosure of the percentage of Scope 3 emissions covered by reduction targets, and year-on-year consistency of methodology—both of which require evidence lineage that extends across multiple reporting cycles.

The result: EU filers with scattered evidence face longer timelines and higher fees than California filers, because the evidence scope is broader. A mid-market manufacturer filing under ESRS E1 in 2026 might incur 300-350 engagement hours, versus 250-280 for the same company filing under SB 253.

How Emission3 fits: the compliance infrastructure that front-loads evidence

Emission3 is positioned as productized California SB 253 and CSRD implementation, backed by compliance infrastructure. We do not sell generic carbon accounting software. We sell document-first inventory systems that treat evidence collection as the bottleneck, not emissions calculation.

For California SB 253 filers, this means:

-

Invoice-level Scope 3 ingestion: Procurement invoices are ingested into the inventory system with supplier-specific emissions intensity metadata, either from primary supplier data or from named EEIO factors. Every line item in the Category 1 total is traceable to a source document.

-

Utility bill reconciliation with monthly lineage: Utility bills are ingested monthly, with kWh and GJ totals reconciled against facility-level metering data. By year-end, the Scope 1 and 2 totals are already reconciled to 12 months of source documents.

-

Pre-audit evidence packs with calculation lineage: Before the auditor begins, the system exports a single-file evidence pack that maps every material emissions line item to a named source document, with page references and calculation steps.

For the manufacturer in question, this approach compressed the auditor's timeline from 14 weeks to 7 weeks, and reduced the engagement fee from $87,000 to $49,900—a 43% reduction. The sustainability lead's assessment: "We paid for compliance infrastructure once, and it reduced our recurring assurance cost by $37,000 per year."

For CSRD filers, the system also generates ESRS E1-compliant disclosure templates with both location-based and market-based Scope 2 totals, and exports evidence packs with year-on-year methodology consistency checks. [6]

The 2027 outlook: why timeline risk is the new assurance bottleneck

California SB 253 phases in Scope 3 assurance starting in 2027 for companies meeting the $1B revenue threshold. The GHG Protocol is currently revising its Scope 3 standard, with final publication targeted for 2027. [7] The expected update will tighten data quality requirements for Category 1, requiring companies to disclose the percentage of emissions calculated using supplier-specific data versus EEIO estimates.

This means the document retrieval bottleneck will intensify. If a company's Scope 3 inventory relies on EEIO estimates for 60% of Category 1, but the auditor requires supplier-specific data for material suppliers (>5% of category total), the timeline risk is the same as we observed in the 2026 case: the document retrieval phase expands, the auditor's timeline extends, and the fee scales accordingly.

The operators we work with are treating 2026 as a dry run: they are front-loading Scope 3 evidence collection now, so that by the time Scope 3 assurance begins in 2027, the document inventory is already complete. The result: they expect their 2027 assurance timelines to remain flat at 7-8 weeks, versus the 14-16 weeks we project for companies that defer evidence collection to the assurance cycle.

Closing: the assurance-readiness conversation

If you are a California manufacturer or EU filer preparing for SB 253 or CSRD assurance, the question is not "how do we calculate emissions faster," but "how do we make evidence-gathering deterministic." The assurance fee is set by the timeline, and the timeline is set by the accessibility of the evidence.

Emission3 customers start with a CBAM and climate disclosure readiness call: we map your suppliers, identify evidence gaps, and build a document-first inventory system that treats assurance-readiness as the bottleneck. If you are filing under California SB 253 or CSRD in 2027, and you want to compress your assurance timeline from 14 weeks to 7 weeks, book a readiness call. [8] We will map your evidence baseline, identify the document retrieval bottlenecks, and show you how the compliance infrastructure works—no anonymous self-serve onboarding.

References & Sources

External Sources

- [1]The GHG protocol explained: A complete guide to corporate emissions reporting

ESRS E1 requires companies to report Scope 1 and Scope 2 emissions separately, with Scope 2 disclosed using both location-based and market-based methods, and material Scope 3 emissions broken down by category with methodologies disclosed.

- [2]What Are Scope 1, 2, and 3 Emissions? A 2026 Guide

California SB 253 requires Scope 3 emissions reporting across material categories with limited assurance for eligible companies doing business in the state, starting in 2027.

- [3]SRG Chapter 7: Greenhouse gas emissions reporting

The GHG Protocol announced a public consultation on proposed updates to its Scope 2 Guidance in October 2025, with revised corporate, scope 2, and scope 3 standards targeted for final publication in 2027.

- [4]All 15 scope 3 categories explained

Under CSRD's ESRS E1 standard, companies must disclose all scope 3 categories that are significant to their business, with methodology details and data quality disclosures. Non-applicable categories must be explicitly excluded with a written justification.

- [5]Scopes 1, 2 and 3: Carbon Emissions Defined

The GHG Protocol requires companies to report both location-based and market-based Scope 2 methods when market-based instruments (PPAs, RECs, GOs) are used. Under CSRD/ESRS E1, both must be disclosed.

- [6]ESRS E1 Applicability and Transitional Reliefs

ESRS E1 establishes mandatory climate-related disclosure requirements, including greenhouse gas emissions (scopes 1-3), transition plans, climate-related risks and opportunities, and related financial impacts.

- [7][Draft] ESRS E1 - Climate Change - EFRAG

ESRS E1 requires disclosure of GHG emission reduction targets in absolute value and, where relevant, in intensity value, with gross Scope 1, 2, and 3 GHG emissions reduction targets disclosed separately.

Related Content

- [8]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, gaps, and implementation. No anonymous self-serve onboarding.

- [9]Reporting & filings

CSRD, CBAM, and SB 253 filing generation with document-first evidence packs and calculation lineage.