The 2026 California SB 253 compliance timeline for CFOs

The 2026 California SB 253 compliance timeline for CFOs

Here's the issue: California SB 253 requires Scope 1 and Scope 2 emissions disclosure by August 10, 2026, for companies with annual revenues exceeding $1 billion that do business in California [1]. The first reporting window is 12 months away, and most finance teams treat this as a sustainability initiative—an ESG exercise delegated to the CSO's office. But SB 253 is not an ESG exercise. It is a financial disclosure with executive officer attestation requirements, and the cost structure for non-compliance is re-pricing faster than most CFOs anticipated [2].

However, SB 253 filings consist of two things: the emissions disclosure itself and the evidence lineage supporting that disclosure. The first is what most companies have been building—a GHG inventory aggregating utility bills and applying emission factors. The second is what auditors will verify in 2027 and beyond: population completeness reports, calculation lineage from source document to final figure, methodology consistency evidence, and boundary reconciliation documentation [3].

The emissions disclosure on its own has no compliance value. The evidence lineage is what the California Air Resources Board (CARB) is actually asking for, what auditors will verify, and what determines whether a company can file without restatement risk. A spreadsheet-based inventory can produce the disclosure. It cannot produce the evidence lineage at the speed and granularity that limited assurance requires in 2027.

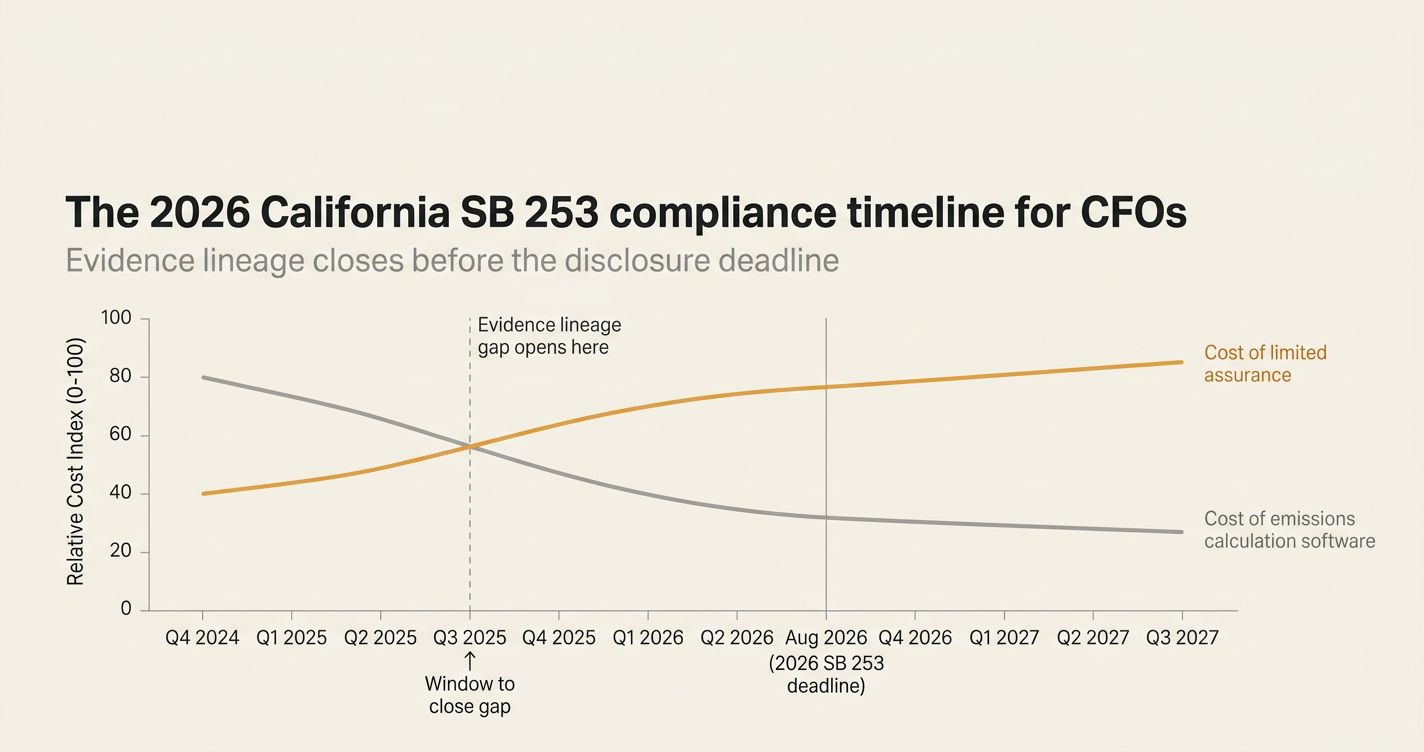

While the cost of emissions calculation software has become cheaper—most platforms now charge $15,000–$50,000 per year for Scope 1+2 inventory—the cost of limited assurance has become more expensive. Auditors are re-pricing climate engagements 20–40% for firms without evidence lineage, and the gap between disclosure systems and assurance-ready systems is widening [4]. If a company reaches Q1 2026 without population completeness infrastructure, the cost of building that infrastructure under audit pressure might outpace the entire inventory software budget by 3–5x.

How do you solve this? I think the answer is to stop treating the 2026 deadline as a standalone compliance event and start treating it as the first milestone in a three-year assurance escalation cycle. The operators we work with are building 2027 limited assurance readiness into their 2026 workflows—implementing document-first accounting at source, maintaining real-time asset registers tied to emissions inventories, and negotiating materiality thresholds with auditors before the first engagement. For now, the companies that close the evidence lineage gap in 2025 will control their audit fees in 2027.

The shape of the argument, visualised below.

The 12-month countdown: what CFOs must close by Q4 2025

The California Air Resources Board released its enforcement advisory in December 2024, and the regulatory timeline is now locked [5]. Companies with fiscal years ending between January 1 and February 1 must report fiscal year 2026 data; companies with fiscal years ending later in 2026 must report fiscal year 2025 data. Every filer has six months after fiscal year end to submit, which compresses the preparation window to Q1–Q2 2026 for most companies.

The countdown breaks into four phases:

| Phase | Window | Deliverable | Failure Mode |

|---|---|---|---|

| Jurisdictional scoping | Q4 2024 (complete) | Confirm whether the company meets California's "doing business" threshold and whether SB 253, SB 261, or both apply | Late discovery in Q1 2025 forces compressed timelines and missed supplier outreach windows |

| Evidence architecture | Q1 2025 | Audit current inventory systems to assess whether they can produce population completeness reports, calculation lineage, and methodology consistency evidence | Discovering gaps in Q2 2025 leaves no time to implement document-first workflows before fiscal year end |

| Assurance provider selection | Q2 2025 | Initiate RFPs for limited assurance providers with California SB 253 experience; negotiate materiality thresholds and engagement scope | Selecting a provider in Q3 2025 or later locks in premium pricing and limits negotiating leverage |

| Boundary reconciliation | Q3 2025 | Map reporting boundary; reconcile operational control vs. financial control boundaries across all entities | Late boundary changes force recalculation of base year emissions and restatement of prior disclosures |

The critical path is evidence architecture in Q1 2025. Companies that reach Q2 2025 without population completeness infrastructure cannot build it in time for fiscal year 2025 data collection, which closes in December 2025 for most calendar-year filers. The window to implement document-first accounting at source is now 8–10 months for most companies [6].

What "limited assurance" means in 2027: the jargon CFOs must learn now

CARB's November 2025 workshop clarified that no assurance is required for 2026 filings—but limited assurance becomes mandatory for Scope 1 and Scope 2 emissions starting in 2027 [7]. The assurance standards under consideration include ISSA 5000, ISAE 3000/3410, AICPA AT-C 210/205, AA1000AS v3, and ISO 14064-3. CFOs unfamiliar with these standards are losing negotiating leverage in assurance engagement scoping.

The terminology gap is costing finance teams control over audit scope creep. Here are the six terms every CFO must understand before the first assurance engagement:

| Term | Definition | Audit Cost Driver | Mitigation Strategy |

|---|---|---|---|

| Limited vs. reasonable assurance | Limited assurance requires plausibility testing and sample-based procedures; reasonable assurance requires exhaustive testing and full population verification | Sampling extent, procedure depth, testing hours | Start with limited assurance in 2027; build controls for reasonable assurance transition in 2030 |

| Materiality threshold | The quantitative or qualitative threshold below which misstatements are considered immaterial to the disclosure | Precision required, testing scope, sample size | Negotiate threshold early; document qualitative factors that influence materiality |

| Evidence lineage | The traceable path from source document (utility invoice, purchase order) to final emission figure in the disclosure | Document retrieval time, traceability gaps, manual reconciliation hours | Implement document-first accounting at source; tag every line item with calculation metadata |

| Population completeness | Proof that all emission sources within the reporting boundary are captured in the inventory | Boundary testing, facility audits, asset register verification | Maintain real-time asset register tied to emissions inventory; reconcile monthly |

| Recalculation policy | The documented method for recalculating base year emissions when significant changes to the reporting boundary or methodology occur | Base year restatement complexity, historical data retrieval | Document policy before first audit; apply consistently across all reporting periods |

| Organizational boundary | The entities, facilities, and operations included in the reporting boundary, using either operational control or financial control consolidation method | JV / subsidiary inclusion scope, boundary testing hours | Align boundary with financial consolidation method; document exceptions |

The average cost of limited assurance for a mid-sized public company is currently $150,000–$300,000 for Scope 1 and Scope 2 emissions. Companies without evidence lineage infrastructure are paying $200,000–$400,000, a 30–50% premium driven by manual document retrieval and boundary testing inefficiencies [8].

"CARB will exercise enforcement discretion for the first report due in 2026, allowing reporting entities to submit Scope 1 and Scope 2 emissions for their prior fiscal year based on information they already have or were collecting when this Notice was issued, whether or not the data received limited assurance." — California Air Resources Board, FAQ 20, November 2025 [7]

The enforcement discretion for 2026 is a grace period, not a permanent exemption. Companies that treat 2026 as optional preparation time are setting themselves up for compressed timelines in 2027.

The Scope 3 cliff: why 2027 is the real deadline for most CFOs

SB 253 phases in Scope 3 emissions reporting starting in 2027, and CARB has signalled that Scope 3 assurance requirements will follow in subsequent rulemaking [1]. For most companies, Scope 3 emissions represent 60–90% of total emissions, and the supplier data collection required to support Scope 3 disclosure is 12–18 months longer than Scope 1+2 data collection.

The procurement timeline for Scope 3 Category 1 (purchased goods and services) is:

- Month 0–3: Supplier identification and tiering (map tier-1 suppliers by spend, identify high-emitting categories)

- Month 3–6: Supplier outreach and onboarding (send data requests, provide templates, negotiate response rates)

- Month 6–12: Data collection and validation (receive supplier-specific data, validate calculation methods, fall back to spend-based factors for non-responsive suppliers)

- Month 12–18: Inventory aggregation and assurance preparation (aggregate supplier data, reconcile boundary, build evidence lineage)

Companies that initiate Scope 3 supplier outreach in Q1 2026—after the 2026 SB 253 deadline—will not have calendar year 2026 data in time for the 2027 filing deadline. The window to secure 2026 supplier data closed in Q3 2025 for most companies [3].

The cost of missing the Scope 3 timeline is not a late fee. It is a restatement cycle. Companies that file 2027 Scope 3 disclosures using spend-based estimation (because supplier-specific data is unavailable) and then receive supplier-specific data in 2028 must restate the 2027 base year. Restatements trigger audit fee escalation, investor confidence erosion, and regulatory scrutiny.

What CFOs should do in Q1 2025

The 2026 SB 253 deadline is 8 months away, but the 2027 limited assurance deadline is 20 months away. CFOs should prioritise evidence lineage infrastructure over emissions calculation software:

- Confirm jurisdictional scope: Determine whether the company meets California's "doing business" threshold and whether SB 253 or SB 261 (or both) apply. CARB's preliminary list of covered entities was released in September 2025 [5].

- Audit current inventory systems: Assess whether the existing GHG inventory can produce population completeness reports, calculation lineage, and methodology consistency evidence. If not, initiate procurement for document-first accounting infrastructure.

- Select an assurance provider: Initiate RFPs for limited assurance providers with California SB 253 experience. Negotiate materiality thresholds and engagement scope before the first engagement.

- Map the reporting boundary: Reconcile operational control vs. financial control boundaries across all entities. Align the reporting boundary with the financial consolidation method to minimise audit complexity.

- Initiate Scope 3 supplier outreach: For companies subject to the 2027 Scope 3 requirement, begin tier-1 supplier onboarding in Q1 2025 to secure 2026 calendar-year data. Build API integrations for supplier data collection where possible; document spend-based factor fallback logic for non-responsive suppliers.

The window to build 2027 limited assurance readiness into 2026 workflows is closing. Companies that treat the 2026 deadline as a standalone compliance event will face compressed timelines and audit fee inflation in 2027.

How Emission3 fits

Emission3 is built for CFOs preparing for the 2026 SB 253 Scope 1+2 deadline and the 2027 limited assurance escalation cycle. The platform compresses inventory preparation timelines from 18–24 months (spreadsheet workflows) to 8–12 months (document-first workflows).

The evidence lineage architecture supports SB 253 limited assurance readiness:

- Population completeness: Real-time asset register tied to emissions inventory, reconciled monthly against facility lists and operational control boundaries.

- Calculation lineage: Every emission figure is traceable to source document (utility invoice, purchase order, shipping manifest), with calculation metadata tagged at line-item level.

- Methodology consistency: Documented calculation methods applied consistently across all reporting periods, with recalculation policy version control.

- Boundary documentation: Operational control vs. financial control reconciliation, with JV / subsidiary inclusion logic documented and auditable.

The platform also supports Scope 3 supplier onboarding, with API integrations for tier-1 supplier data collection and automated spend-based factor fallback for non-responsive suppliers. For companies initiating Scope 3 supplier outreach in Q1 2025, the platform compresses the data collection window from 12–18 months to 6–9 months.

Emission3 customers start with a CBAM readiness call—we map suppliers, gaps, and implementation scope before any software onboarding. The readiness call covers jurisdictional scope confirmation, evidence architecture audit, and assurance provider selection strategy. No anonymous self-serve onboarding.

What to start this week

The 2026 SB 253 deadline is 8 months away, but the decisions that determine audit fees in 2027 are being made this week:

- This week: Confirm whether your company is on CARB's preliminary list of covered entities (released September 2025). If yes, initiate internal scoping for SB 253 vs. SB 261 applicability.

- Next week: Audit current GHG inventory systems for evidence lineage readiness. If the system cannot produce population completeness reports, initiate procurement for document-first accounting infrastructure.

- This month: Select an assurance provider and negotiate materiality thresholds before the first engagement. Early negotiation controls audit scope and fee structure.

- Next quarter: Initiate Scope 3 supplier outreach for 2027 filings. The window to secure 2026 supplier data closes in Q3 2025 for most companies.

The companies that close the evidence lineage gap in Q1 2025 will control their audit fees in 2027. The companies that wait until Q3 2026 will pay the premium.

Book a CBAM readiness call to map your 2026 SB 253 timeline and evidence architecture gaps [9].

References & Sources

External Sources

- [1]California SB 253 and SB 261: What Businesses Need to Know

Persefoni's guidance on SB 253 and SB 261 compliance requirements, reporting timelines, and assurance standards for California climate disclosure.

- [2]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

Emission3's analysis of the terminology gap in climate assurance and the cost drivers for SB 253 limited assurance engagements.

- [3]The US Climate Disclosure Stack: SB 253, SB 261, and the 2026 CFO Reckoning

Emission3's comprehensive guide to the California climate disclosure stack, including Scope 3 supplier outreach timelines and evidence lineage requirements.

- [5]California SB 253 & SB 261 compliance: what you need to know

GreenPlaces' overview of SB 253 and SB 261 compliance requirements, including CARB's preliminary list of covered entities and reporting deadlines.

- [7]SB 253 and SB 261: California climate reporting explained

PwC's guidance on SB 253 and SB 261 reporting requirements, including CARB's enforcement discretion for 2026 and the transition to limited assurance in 2027.

Related Content

- [4]The assurance cost inflation problem in California SB 253 first-year filings

SB 253 filings consist of two things: the emissions disclosure and the evidence lineage. Auditors verify the second—and most CFOs budgeted for the first.

- [6]The assurance timeline compression problem in CSRD wave-2 filings

CSRD filings consist of two things: the disclosure itself and the evidence lineage. Auditors verify the second—and most companies are 6-9 months behind schedule.

- [8]The audit-trail gap in CSRD limited assurance engagements

CSRD limited assurance consists of two things: the sustainability disclosure and the evidence lineage. Auditors verify the second—and most filers lack it.

- [9]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation, no anonymous self-serve onboarding.