The assurance cost inflation problem in California SB 253 first-year filings

The assurance cost inflation problem in California SB 253 first-year filings

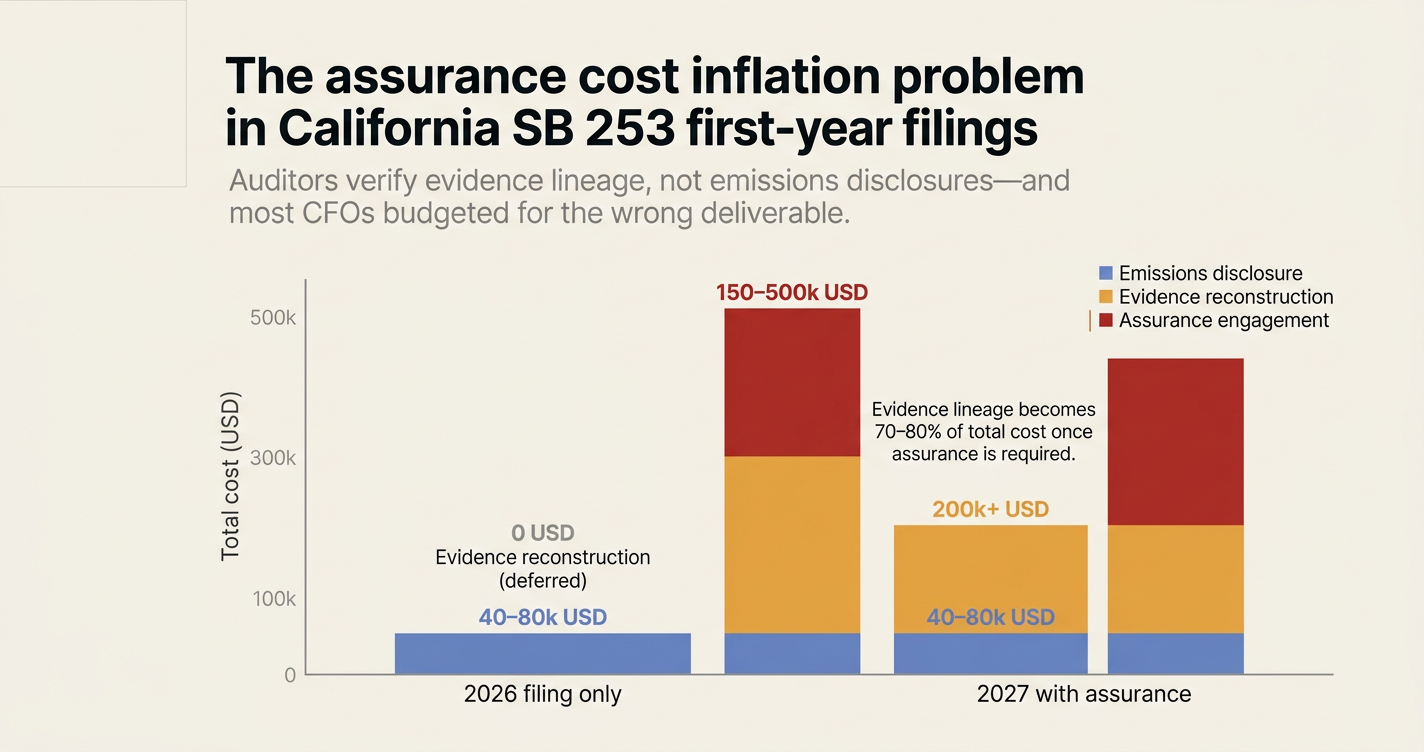

Here's the issue: California Senate Bill 253 (the Climate Corporate Data Accountability Act) requires entities with over one billion dollars in annual revenue doing business in California to report Scope 1 and Scope 2 greenhouse gas emissions by August 10, 2026 [1]. The California Air Resources Board (CARB) has exercised enforcement discretion for this first year—no limited assurance is required in 2026, though it will be mandatory starting in 2027 [2]. Most CFOs initially budgeted 50,000 to 100,000 dollars for the first-year filing, assuming the work was the emissions calculation itself. That assumption is proving expensive.

However, an SB 253 filing consists of two things: the emissions disclosure (Scope 1 and Scope 2 numbers, reported under the Greenhouse Gas Protocol) and the evidence lineage that makes those numbers reproducible and verifiable by an independent third party.

The emissions disclosure on its own has no value to an auditor. The evidence lineage is what the auditor is actually asking for—and what CARB will require starting in 2027 when limited assurance becomes mandatory under standards including ISSA 5000, ISAE 3000/3410, AICPA AT-C 210/205, AA1000AS v3, and ISO 14064-3 [3].

While the cost of producing the emissions disclosure has remained stable (consultants still charge 40,000 to 80,000 dollars for a Scope 1 and 2 inventory), the cost of building the evidence lineage has become the dominant expense. If a company has not maintained invoice-level utility records, procurement documentation linking energy use to production output, or reconciled facility boundaries across subsidiaries, the cost of reconstructing that evidence base for 2025 data might exceed 200,000 dollars before any auditor engagement begins. Assurance costs themselves are estimated between 150,000 and 500,000 dollars per year, depending on complexity [4].

How do you solve this? I think the operators we work with are starting to recognise that the 2026 filing—even without a formal assurance requirement—is the dress rehearsal for 2027, when limited assurance becomes mandatory. The companies that will avoid cost inflation in 2027 are those that treat the 2026 filing as an evidence-construction project, not just a disclosure exercise. For now, that means building invoice-to-emission traceability in 2026, even though CARB is not enforcing it yet.

The shape of the argument, visualised below.

The two-part structure of an SB 253 filing

An SB 253 filing is not a single deliverable. It is:

| Component | What it contains | Who verifies it | Cost range (2026) |

|---|---|---|---|

| Emissions disclosure | Scope 1 and 2 GHG emissions under the GHG Protocol, reported in metric tonnes CO₂e | CARB (submission only in 2026) | 40,000–80,000 USD |

| Evidence lineage | Invoice-level utility records, facility boundary documentation, procurement records linking energy use to production, calculation methodologies with lineage to source documents | Independent auditor (mandatory in 2027, voluntary in 2026) | 150,000–500,000 USD |

In 2026, only the first component is required for submission. But CARB has made clear that limited assurance will be mandatory in 2027 [2], and auditors are already telling clients that they cannot issue an assurance opinion without the second component—the evidence lineage.

The result: companies that treat 2026 as a disclosure-only exercise will face a compressed timeline and cost spike in 2027 when they have to reconstruct 2026 data under audit.

Why CFOs initially underestimated the cost

Most finance teams based their initial SB 253 budget on the cost of producing the emissions number—not the cost of proving it. The logic was:

- SB 253 requires Scope 1 and 2 reporting starting in 2026.

- Assurance is not required until 2027.

- Therefore, the 2026 cost is just the cost of the inventory calculation.

This reasoning is directionally correct for compliance purposes—CARB will accept 2026 submissions without assurance—but it ignores the structural work required to make the 2027 assurance engagement feasible.

Consider the practical constraints:

- An auditor performing limited assurance under ISAE 3410 or AICPA AT-C 210 must verify that emissions calculations are based on "sufficient appropriate evidence" [3].

- For a Scope 1 calculation from natural gas use, that means the auditor must trace the emissions factor, the volume consumed, and the facility boundary back to source documents—utility invoices, meter records, and lease agreements.

- If those documents were not retained in 2025, or were not organised by facility and reporting period, the auditor cannot complete the engagement.

The evidence gap becomes visible only when the auditor engagement begins—and by then, the cost of remediation is no longer discretionary.

"Assurance costs could range from $150,000 to $500,000 per year, depending on the complexity of a company's emissions profile. Securing auditors early will be important to avoid bottlenecks as reporting deadlines approach." [4]

The 2027 assurance bottleneck

SB 253 requires limited assurance for Scope 1 and 2 emissions starting in 2027, scaling to reasonable assurance by 2030 [1]. The number of qualified auditors who can perform these engagements is limited, and demand is concentrated in the same 12-month window.

The practical constraint is not audit capacity in aggregate—it is the availability of auditors who specialise in GHG inventory assurance under the specific standards CARB will adopt. The proposed standards include:

- ISSA 5000 (International Standard on Sustainability Assurance)

- ISAE 3000 and ISAE 3410 (International Standards on Assurance Engagements)

- AICPA AT-C 210 and AT-C 205 (American Institute of CPAs attestation standards)

- AA1000AS v3 (AccountAbility assurance standard)

- ISO 14064-3 (Greenhouse gases verification standard) [3]

Each standard has different evidentiary requirements, but all require the same foundational inputs: source documents, calculation lineage, and facility boundary definitions.

Companies that have not built this evidence base by the time they engage an auditor in 2027 will face:

- Engagement delays: Auditors cannot begin substantive testing without a complete evidence package.

- Scope expansion: The auditor will need to verify not only the 2026 emissions calculation, but also the completeness of the underlying data set—requiring historical reconstruction.

- Fee inflation: Auditors will price the engagement based on the expected hours required to verify incomplete or inconsistent records.

The result is a cascading cost problem: the 2026 filing becomes cheap (because assurance is optional), but the 2027 filing becomes expensive (because the 2026 evidence base was never built).

The evidence lineage gap in most 2026 filings

Most companies approaching the August 10, 2026 deadline have:

- A Scope 1 and 2 inventory calculation, often prepared by a consultant using the GHG Protocol.

- Aggregated utility data from a procurement system or facilities management platform.

- A disclosure document summarising the emissions by scope and, in some cases, by facility or business unit.

What they do not have:

- Invoice-level utility records retained and organised by reporting period.

- Procurement documentation linking energy purchases to specific facilities.

- Facility boundary definitions that reconcile with lease agreements and financial consolidation boundaries.

- Calculation methodologies documented at the transaction level, with lineage back to source documents.

The gap is not academic. Under ISAE 3410, an auditor performing limited assurance must obtain evidence that the emissions calculation is "plausible in the circumstances" [3]. This requires:

- Verifying that the activity data (e.g., kilowatt-hours consumed) matches source documents (utility invoices).

- Confirming that the emissions factors applied are appropriate for the fuel type, geography, and reporting period.

- Testing that the facility boundaries used in the calculation align with the organisational boundaries defined in the GHG Protocol.

If any of these inputs cannot be traced back to a source document, the auditor cannot issue an opinion—and the company must reconstruct the evidence base before the engagement can proceed.

The cost structure of evidence reconstruction

Reconstructing the evidence lineage for a 2025 reporting year typically involves:

- Document retrieval: Requesting and organising utility invoices, meter records, and lease agreements from facilities teams, landlords, and third-party vendors.

- Data reconciliation: Matching aggregated utility data from a procurement system to invoice-level records, and resolving discrepancies.

- Boundary definition: Documenting the facility boundaries used in the calculation, and reconciling them with financial consolidation boundaries and lease terms.

- Calculation lineage: Re-running the emissions calculation at the transaction level, with explicit documentation of the emissions factors, activity data, and calculation methodology applied to each source.

The cost of this work depends on:

- The number of facilities in scope.

- The completeness of existing utility records.

- The consistency of facility boundary definitions across business units.

- The availability of personnel who understand the underlying data sources.

For a company with 50 facilities, incomplete utility records, and inconsistent boundary definitions, the cost of evidence reconstruction can exceed 200,000 dollars before any auditor engagement begins [4].

How Emission3 fits

Emission3 is designed for this transition. We do not produce the emissions disclosure—we build the evidence lineage that makes it auditable.

Specifically:

- Invoice-to-emission traceability: Every emissions calculation is linked back to the source document (utility invoice, meter record, procurement order). The auditor can see the lineage from the filing number back to the original PDF.

- Deterministic calculation: All emissions factors, activity data, and boundary definitions are versioned and reproducible. If the auditor re-runs the calculation, they get the same number.

- Evidence packs for auditors: We export a complete evidence package—source documents, calculation lineage, and facility boundary documentation—structured for the assurance engagement.

- CARB-compliant outputs: The system generates the disclosure document required for CARB submission, along with the supporting evidence package for the auditor.

The engagement begins with a CBAM readiness call (we also support SB 253 filings under the same framework). We map your facilities, utility vendors, and data gaps, then scope the implementation timeline. For most clients, the 2026 filing becomes the foundation for the 2027 assurance engagement—not a separate one-time project [5].

The 2026 filing as a 2027 foundation

The companies that will avoid cost inflation in 2027 are those that treat the 2026 filing as an evidence-construction project, not just a disclosure exercise.

This means:

- Retaining invoice-level utility records for 2025, even though CARB is not requiring assurance in 2026.

- Documenting facility boundaries and calculation methodologies at the transaction level, not just at the aggregate level.

- Running the 2026 emissions calculation in a system that produces auditor-ready outputs—calculation lineage, source document traceability, and boundary definitions.

The incremental cost of doing this work in 2026 is substantially lower than the cost of reconstructing it in 2027 under audit pressure. And for companies that will also need to comply with CSRD (Corporate Sustainability Reporting Directive) limited assurance or Scope 3 disclosure under SB 253 (starting in 2027), the evidence lineage built for the 2026 Scope 1 and 2 filing becomes the foundation for all subsequent filings [6].

Closing observation

SB 253 filings consist of two things: the emissions disclosure and the evidence lineage. CARB requires the first in 2026. Auditors will require the second in 2027. Most CFOs budgeted for the first—and are now discovering that the second is where the cost lives.

The companies that avoid the 2027 cost spike are those that build the evidence lineage in 2026, even though it is not yet mandatory. The companies that defer this work will pay for it twice: once to produce the 2026 filing, and again to reconstruct the evidence base when the auditor engagement begins in 2027.

If you are preparing your first SB 253 filing and want to avoid the 2027 assurance bottleneck, book a CBAM readiness call [7]. We map your facilities, data gaps, and evidence requirements, then scope the implementation timeline. All Emission3 engagements begin with this conversation—no anonymous self-serve onboarding.

References & Sources

External Sources

- [1]California's climate disclosure laws: An overview of SB 253 & SB 261

Optera's detailed guide to SB 253 and SB 261 reporting timelines, assurance requirements, and compliance obligations for entities over 1 billion USD in revenue.

- [2]Navigating California's Climate Disclosure Laws: Your Complete Guide to SB 253 and SB 261

Nelson Mullins law firm analysis of CARB's enforcement discretion for 2026 and the transition to limited assurance in 2027.

- [3]California SB 253 and SB 261: What Businesses Need to Know

Persefoni's breakdown of assurance standards (ISSA 5000, ISAE 3000/3410, AICPA AT-C 210/205, AA1000AS v3, ISO 14064-3) proposed for SB 253 limited assurance starting in 2027.

- [4]California's SB 253: Corporate Climate Reporting & Compliance

EcoVadis analysis of SB 253 compliance costs, including the 150k–500k USD range for assurance engagements and third-party verification bottlenecks.

Related Content

- [5]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, data gaps, and implementation timeline—no anonymous self-serve onboarding.

- [6]The audit-trail gap in CSRD limited assurance engagements

CSRD limited assurance consists of two things: the sustainability disclosure and the evidence lineage. Auditors verify the second—and most filers lack it.

- [7]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, data gaps, and implementation timeline—no anonymous self-serve onboarding.