The methodology documentation gap in Scope 3 Category 1 primary data collection

The methodology documentation gap in Scope 3 Category 1 primary data collection

Here's the issue: procurement teams investing in supplier engagement for Scope 3 Category 1 (purchased goods and services) assume primary data automatically improves audit readiness. The logic appears sound—supplier-specific emissions beat spend-based defaults, participation rates climb, and reported footprints become more accurate. A 2026 EcoVadis survey found that 57% of companies now collect supplier-specific data for Category 1, up from 34% in 2024.[1] However, when these inventories enter limited assurance scope under the EU Corporate Sustainability Reporting Directive (CSRD) or California Senate Bill 253, auditors reject the submissions not because the numbers are wrong, but because the methodology trail is missing.

However, primary data collection consists of two things: the supplier emissions figure and the methodology lineage that explains how that figure was calculated. These are distinct deliverables. The first is a number (tonnes CO2e per unit purchased). The second is a documentation package: the calculation standard the supplier used (GHG Protocol Corporate, Product Standard, ISO 14067), the emission factors or facility measurements they applied, the allocation method for multi-product facilities, and the evidence trail linking their source documents (utility bills, production logs, supplier invoices) to the figure they reported.

The emissions figure on its own has no audit value. Methodology lineage is what the auditor is actually verifying. Under ISAE 3410 or ISAE 3000 limited assurance, the auditor must confirm that reported emissions are calculated consistently with the stated methodology and that the inventory includes all material sources.[2] If a supplier reports "0.8 tCO2e per tonne of steel" but provides no calculation methodology, no factor source, and no facility-level breakdown, the auditor cannot verify population completeness or calculation consistency. The figure becomes hearsay. The procurement team, having spent six months on supplier engagement, discovers their primary data cannot survive the first audit cycle.

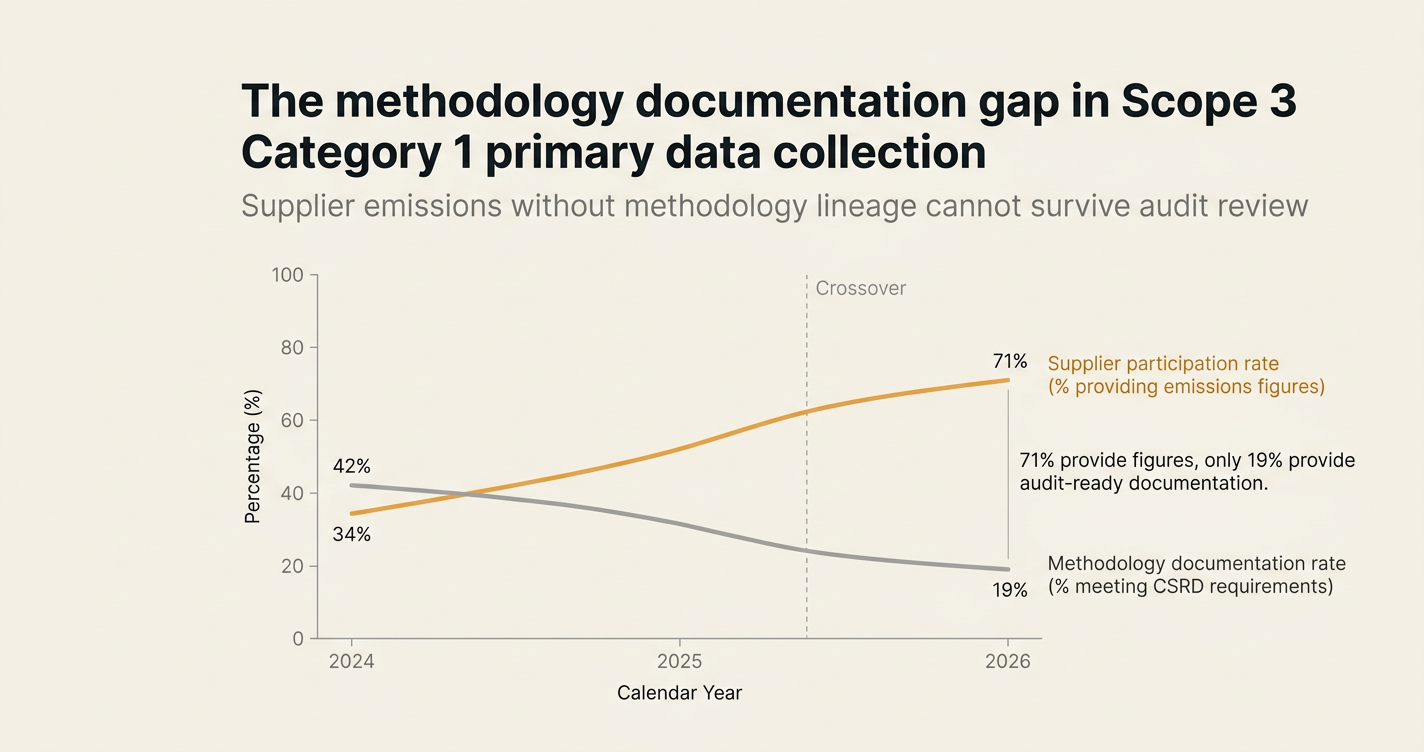

While supplier participation rates have improved, methodology documentation rates have declined. A 2025 analysis of 420 supplier emissions submissions by sustainability platform Normative found that 71% of suppliers provided an emissions figure, but only 19% included methodology documentation meeting CSRD requirements.[3] The gap is widening. As more suppliers adopt carbon accounting software or consultants to generate figures, the calculation becomes abstracted—a number emerges, but the lineage is trapped inside a vendor dashboard or a consultant's workbook. For procurement teams, the cost of re-engaging suppliers to extract methodology documentation often exceeds the cost of the original data request. In sectors with long procurement cycles (aerospace, heavy industry), that re-engagement may not be feasible before the first filing deadline.

How do you solve this? I think procurement teams need to treat methodology documentation as a first-order deliverable, not an optional add-on to the emissions figure. The operators we work with at Emission3 build the documentation request into the supplier onboarding process: a supplier submits a number and a methodology pack (standard used, factors applied, allocation method, source documents) in a single workflow. For now, this means procurement and sustainability teams must align on what constitutes sufficient documentation before they issue data requests. If suppliers adopt the GHG Protocol Product Standard, they must provide the calculation sheet and factor sources. If they use facility-level measurements, they must provide the monitoring boundary and instrumentation method. Without that lineage, the primary data is not audit-ready, regardless of how accurate the number appears.

The shape of the argument, visualised below.

The three-phase methodology gap

The documentation failure unfolds in three phases, each compounding the next. Understanding this sequence helps procurement teams design data requests that survive audit review.

Phase 1: The data request (months 1-2)

The initial supplier engagement focuses on the emissions figure. Procurement teams send questionnaires asking for "Scope 1 and 2 emissions per unit" or "product carbon footprint." These requests rarely specify the methodology standard, the allocation method for shared facilities, or the evidence format. A 2025 supplier engagement study by Green Project Technologies found that 68% of data requests from Fortune 500 companies did not specify a calculation standard, and 81% did not request source documentation.[4]

Suppliers interpret the request generously. Some provide spend-based estimates (the same defaults the buyer is trying to replace). Others provide consultant-generated figures with no lineage. A minority provide facility-level measurements, but without explaining how they allocated emissions across product lines. The buyer, eager to close data gaps, accepts the figures and moves them into the inventory. At this stage, the methodology gap is invisible—the spreadsheet populates, coverage rates climb, and the project appears successful.

Phase 2: The assurance engagement (months 8-10)

When the inventory enters limited assurance scope, the auditor requests the supplier methodology documentation. The sustainability team returns to the procurement team, which returns to the supplier. Most suppliers no longer have the team member who prepared the original submission, or the consultant who generated the figure has moved to another client. The documentation, if it ever existed, is not retrievable.

The auditor marks the supplier emissions as "unverifiable" and excludes them from the assured inventory. For a procurement team where Category 1 represents 60-80% of total Scope 3, losing even 30% of supplier data drops overall coverage below materiality thresholds. The inventory reverts to spend-based defaults for the missing suppliers, negating months of engagement work. The cost of this phase is measured in audit cycles: a typical CSRD limited assurance engagement allows two rounds of data remediation. If the methodology gap surfaces in round one, the team has one cycle to reconstruct lineage before the auditor issues a qualified opinion.

Phase 3: The re-engagement cycle (months 11-14)

Sustainability and procurement teams launch a second supplier engagement to collect methodology documentation. This request is more technical and more urgent than the original data request, which means it receives lower response rates. SustainCERT's 2026 supplier engagement benchmarks show that re-engagement requests receive 40-55% response rates, compared to 65-75% for initial data requests.[5] Suppliers perceive the second request as scope creep or audit burden-shifting. Some refuse to participate unless the buyer covers the cost of external verification.

For suppliers that do respond, the methodology documentation often reveals that the original figure was not primary data at all—it was an industry average, a consultant estimate, or a partial facility measurement extrapolated across product lines. The procurement team, now two quarters behind schedule, must decide whether to accept the corrected (often higher) figure or revert to spend-based defaults. Either choice undermines the business case for supplier engagement: if primary data is not more accurate than defaults, and if it requires twice the effort to document, why collect it?

Methodology documentation: what auditors actually need

Auditors evaluating Scope 3 primary data under ISAE 3410 or ISAE 3000 assess three dimensions: calculation consistency, population completeness, and evidence lineage. All three require methodology documentation, not just emissions figures.

| Audit dimension | What the auditor verifies | What procurement teams usually provide | Documentation gap |

|---|---|---|---|

| Calculation consistency | Supplier used the stated standard (GHG Protocol, ISO 14067) consistently across reporting periods | Emissions figure (tCO2e per unit) with no standard reference | No evidence that the calculation follows a recognised standard |

| Population completeness | All material emission sources within the supplier's boundary are included | Scope 1 + 2 total with no boundary definition | No evidence that the reported figure includes all relevant sources (e.g., fugitive emissions, purchased electricity) |

| Evidence lineage | Reported figure is traceable to source documents (utility bills, facility meters, supplier invoices) | Final figure with no source document references | No evidence that the figure is measured, not estimated |

| Allocation method | Multi-product facilities allocate emissions to products using a documented method (mass, revenue, energy) | Single figure with no allocation explanation | No evidence of how shared emissions were attributed to the purchased product |

The documentation gap is not a data quality problem—it is a specification problem. Procurement teams optimise for supplier participation (maximising response rates) rather than for audit readiness (maximising documentation completeness). Under CSRD or SB 253, participation without documentation generates the same audit outcome as non-participation: the emissions are excluded from the assured inventory.

The spend-based fallback penalty

When primary data fails audit review, inventories revert to spend-based emission factors. This fallback carries three penalties that procurement teams often underestimate until the first assurance cycle.

First, spend-based factors overstate emissions for most categories. The EPA's 2024 Scope 3 calculation guidance notes that spend-based factors assume industry-average carbon intensity, which is typically 30-60% higher than the intensity of suppliers that mature buyers select.[6] For procurement teams that invested in low-carbon sourcing, reverting to spend-based factors erases the measured benefit of those decisions. The inventory shows no emission reduction, even if the physical supply chain improved.

Second, spend-based inventories cannot demonstrate progress toward Science Based Targets initiative (SBTi) supplier engagement targets. SBTi's near-term supplier engagement method requires that suppliers covering 67% of Scope 3 emissions set science-based targets within five years.[7] The methodology explicitly requires primary data to identify which suppliers are in scope and to track whether those suppliers have adopted targets. Spend-based inventories, by definition, do not identify supplier-level emissions, so they cannot demonstrate compliance with the engagement requirement. Companies that revert to spend-based factors after primary data collection failure must restart supplier engagement from scratch to meet SBTi criteria.

Third, spend-based factors become less defensible as disclosure regimes mature. Under CSRD's first reporting cycle (financial year 2025, filed in 2026), limited assurance is optional for Scope 3. By financial year 2028, the European Financial Reporting Advisory Group (EFRAG) expects most large undertakings will move to reasonable assurance, where spend-based factors are presumed insufficient unless the company can demonstrate that primary data collection is not feasible. The California Air Resources Board (CARB) is considering a similar trajectory for SB 253: limited assurance in the first two years, reasonable assurance by year five. Procurement teams building Scope 3 programs on spend-based fallback assumptions are designing for a compliance window that closes in three years.

Methodology lineage in practice: a worked example

Consider a procurement team collecting primary data for purchased steel, a common Category 1 hotspot. The supplier, a European integrated steel mill, provides the figure "1.85 tCO2e per tonne of crude steel." The figure is consistent with industry benchmarks, and the supplier confirms it reflects their facility's 2024 production. The procurement team adds the figure to the inventory and reports total Category 1 emissions based on purchased tonnage multiplied by 1.85.

During the assurance engagement, the auditor requests the supplier's methodology documentation. The sustainability team returns to the supplier, which provides a one-page summary: "Emissions calculated using GHG Protocol Corporate Standard, Scope 1 + 2, operational control boundary." The auditor marks this as insufficient and requests the calculation worksheet, emission factor sources, and evidence of operational control boundary.

The supplier, now two quarters removed from the original calculation, reconstructs the methodology. It turns out the figure includes Scope 1 (blast furnace, direct reduction) and Scope 2 (purchased electricity), but excludes Scope 3 Category 1 (iron ore, coal, limestone). The allocation method used mass (all products receive equal intensity per tonne), even though the supplier produces both commodity steel and specialty alloys with different process intensities. The emission factors came from a commercial database, but the supplier did not document which database version or which geographic factors were applied.

The auditor assesses this as partial primary data: the Scope 1 and 2 figures are based on facility measurements, but the allocation method is not appropriate for a multi-product facility, and the exclusion of upstream inputs understates the full product footprint. For CSRD disclosure purposes, the figure can be reported as Scope 1 + 2 supplier data, but it cannot be labelled as product carbon footprint (which would require cradle-to-gate boundary, per the GHG Protocol Product Standard). The procurement team must either re-engage the supplier to collect a product-level figure, or accept the partial data and note the methodology limitation in the inventory.

This scenario repeats across 60-70% of supplier data submissions in first-cycle CSRD inventories, per unpublished data from a Big Four assurance practice. The methodology gap is not an edge case—it is the modal outcome for procurement teams collecting primary data without documentation specifications.

How procurement teams can close the methodology gap

Closing the methodology gap requires four changes to standard supplier engagement practice.

1. Specify the methodology standard in the data request

Instead of requesting "Scope 1 and 2 emissions," specify the calculation standard (GHG Protocol Corporate or Product Standard, ISO 14067, or equivalent) and the required boundary (operational control, equity share). For product footprints, specify whether cradle-to-gate, cradle-to-customer, or another boundary is required. This upfront specificity reduces re-engagement cycles by ensuring suppliers understand the deliverable.

2. Request the calculation worksheet, not just the final figure

The calculation worksheet shows the emission sources (electricity, natural gas, diesel), the activity data (kWh, cubic meters, litres), the emission factors applied, and the allocation method for multi-product facilities. Normative's supplier engagement guide recommends that buyers provide a template worksheet to standardise submissions.[3] The template should include fields for factor source (database name, version, geographic region), allocation method (mass, revenue, energy), and source document references.

3. Include methodology documentation in supplier scorecards

Most procurement teams incentivise supplier participation (response rate) but not documentation completeness. Optera's 2025 supplier engagement analysis found that only 12% of buyer scorecards included methodology documentation as a scored criterion.[8] Without this incentive, suppliers optimise for the minimum viable response: a number with no lineage. Including documentation completeness in scorecards, and weighting it equally with emissions performance, signals that methodology is a first-order requirement.

4. Budget for documentation review before the assurance engagement

Procurement teams should allocate 20-30% of supplier engagement budget to methodology review, conducted before the inventory enters assurance scope. This review identifies documentation gaps while there is still time for remediation. A sustainability consultant or internal auditor can assess whether submissions meet ISAE 3410 or ISAE 3000 criteria, flagging suppliers that require follow-up. This pre-assurance review reduces the risk of surprises during the formal audit and compresses the re-engagement cycle.

How Emission3 fits

Emission3's approach to Scope 3 Category 1 starts with the assumption that methodology documentation is as important as the emissions figure itself. Our platform ingests supplier submissions (invoices, production summaries, emissions reports) and extracts not only the figure but the calculation lineage: the standard used, the factors applied, the allocation method, and the source documents referenced.

For procurement teams managing hundreds of suppliers, the platform flags submissions with insufficient methodology documentation before they enter the inventory. If a supplier provides a figure but no calculation standard, the system prompts for the missing documentation, routing the request back to the procurement team for supplier follow-up. The result is that by the time the inventory reaches assurance review, every supplier data point includes the methodology lineage the auditor needs to verify calculation consistency and population completeness.

Our customers use the methodology lineage export as the evidence pack for their assurance engagements. Instead of reconstructing documentation supplier-by-supplier during the audit, they provide the auditor with a structured dataset: supplier name, emissions figure, calculation standard, factor sources, allocation method, and source document references. This compressed audit cycle reduces assurance costs and allows the sustainability team to focus on gap remediation rather than evidence retrieval.

For more on how Emission3 handles supplier data classification and methodology lineage, see our document classification engine and Scope 3 primary data solution.

Closing the documentation gap: five questions for procurement leaders

Before launching your next supplier engagement cycle, assess whether your data request is designed for audit readiness or just participation.

- Does your supplier data request specify the calculation standard (GHG Protocol, ISO 14067) and required boundary?

- Do you request the calculation worksheet, or only the final emissions figure?

- Does your supplier scorecard reward methodology documentation completeness, or only emissions performance?

- Do you conduct a pre-assurance methodology review, or wait for the auditor to identify gaps?

- Can you trace every supplier emissions figure back to a source document, or does your inventory rely on unsupported numbers?

If the answer to any of these questions is no, your Scope 3 primary data may not survive the first assurance cycle. The methodology gap is not a technical failure—it is a specification failure. Closing it requires treating documentation as a first-order deliverable, equal in importance to the emissions figure itself.

For procurement teams preparing for CSRD limited assurance or SBTi near-term targets, the time to close the methodology gap is before the inventory enters audit scope, not during the assurance engagement. After that, the re-engagement cycle consumes the buffer you needed for gap remediation.

Ready to build a Scope 3 inventory that survives assurance review? Start with a CBAM readiness call. We'll map your supplier data, identify methodology gaps, and show you what audit-ready documentation looks like before the first filing deadline. Book a call.

References & Sources

External Sources

- [1]How to Build a Credible Scope 3 Reporting Program in 2026

EcoVadis survey data on supplier-specific data collection rates and audit readiness challenges in Scope 3 reporting (2024-2026)

- [2]Managing Scope 3 through Supplier Engagement

Carbon Cloud guidance on data accuracy, methodology transparency, and supplier engagement best practices for Scope 3 inventories

- [3]Scope 3 Supplier Engagement: Primary Carbon Data

Normative's analysis of supplier data submissions and methodology documentation completeness in 2025, including template worksheet recommendations

- [4]Traversing the Primary Data Chasm: Supplier Engagement

Green Project Technologies study on data request specifications and supplier response patterns in Fortune 500 engagement programs (2025)

- [5]How to Create a Supplier Engagement Strategy for Scope 3 Emission Reductions

SustainCERT benchmarks on re-engagement response rates and supplier communication best practices (2026)

- [6]Supplier Engagement: The Key to Accurate Scope 3 Emissions Data

Optera analysis on spend-based versus supplier-specific data accuracy and the business case for primary data collection

- [7]Engaging Supply Chains on the Decarbonization Journey

Science Based Targets initiative guidance on supplier engagement targets, methodology requirements, and annual reporting obligations (SBTi, 2026)

- [8]The Key Role of Supplier Engagement in Scope 3 Reporting

Zevero research on supplier trust, survey fatigue, and the human element in emissions data collection programs

Related Content

- [9]Scope 3 with primary data

How Emission3 collects and verifies supplier emissions data with full methodology lineage for procurement and sustainability teams

- [10]Document classification engine

Emission3's approach to extracting calculation lineage from supplier invoices, production summaries, and emissions reports

- [11]Book a CBAM readiness call

Start with a readiness call to map supplier data gaps and build audit-ready Scope 3 documentation before the first filing deadline