The supplier-data collection problem in Scope 3 Category 1 assurance transitions

The supplier-data collection problem in Scope 3 Category 1 assurance transitions

Here's the issue: Most procurement teams preparing for 2026 Scope 3 disclosure under California SB 253 or EU CSRD ESRS E1 assume the bottleneck is calculating emissions totals. They invest in spend-based estimation tools, map supplier categories to emission factors, and produce credible top-line numbers. The calculation runs in seconds. The audit quote arrives 8 weeks later, priced at 180-220 hours for limited assurance—and the CFO discovers that 140 of those hours are allocated to "supplier data verification and population completeness testing." The emissions total was never the expensive part.

However, Scope 3 Category 1 assurance consists of two things: the aggregated emissions number and the supplier-specific primary data that produced it. A procurement team can generate the first using spend-based methods in one afternoon. The second requires line-item invoices, utility bills, and material certificates from dozens or hundreds of suppliers, many of whom have never been asked for carbon data before.

The emissions total on its own has no assurance value. Supplier primary data is what the auditor is actually verifying—and what the ISAE 3410 or ISSA 5000 engagement is priced against. An aggregated Scope 3 total backed by spend-based estimation is a modeled output. An aggregated Scope 3 total backed by supplier-specific invoices, bills of materials, and utility records is an audit-ready population. The difference is not semantic. It is the difference between a 40-hour desk review and a 180-hour fieldwork engagement.

While spend-based estimation has become cheaper and faster, supplier primary data collection has become more expensive and slower. If a company with 200 Category 1 suppliers attempts to transition from spend-based to primary-data methods in the 90 days before an assurance deadline, the cost of data collection might outpace the cost of the assurance engagement itself. One Big Four audit partner quoted a 2025 client case: procurement sent data requests to 180 suppliers in January, received responses from 40 by March, and paid the auditor €18,000 in extension fees while waiting for the remaining 140. The emissions calculation took 6 hours. The supplier follow-up took 9 weeks.

How do you solve this? I think the operators who succeed in 2026-2027 Scope 3 assurance transitions are the ones who treat supplier data collection as a procurement workflow problem, not a carbon accounting problem. They map tier-1 suppliers by materiality threshold in Q1, issue data requests aligned to their financial close calendar in Q2, and build evidence lineage in parallel with the calculation—not after it. For now, the companies that wait until the assurance engagement begins to discover they lack supplier primary data are the ones paying premium audit fees and filing extension requests.

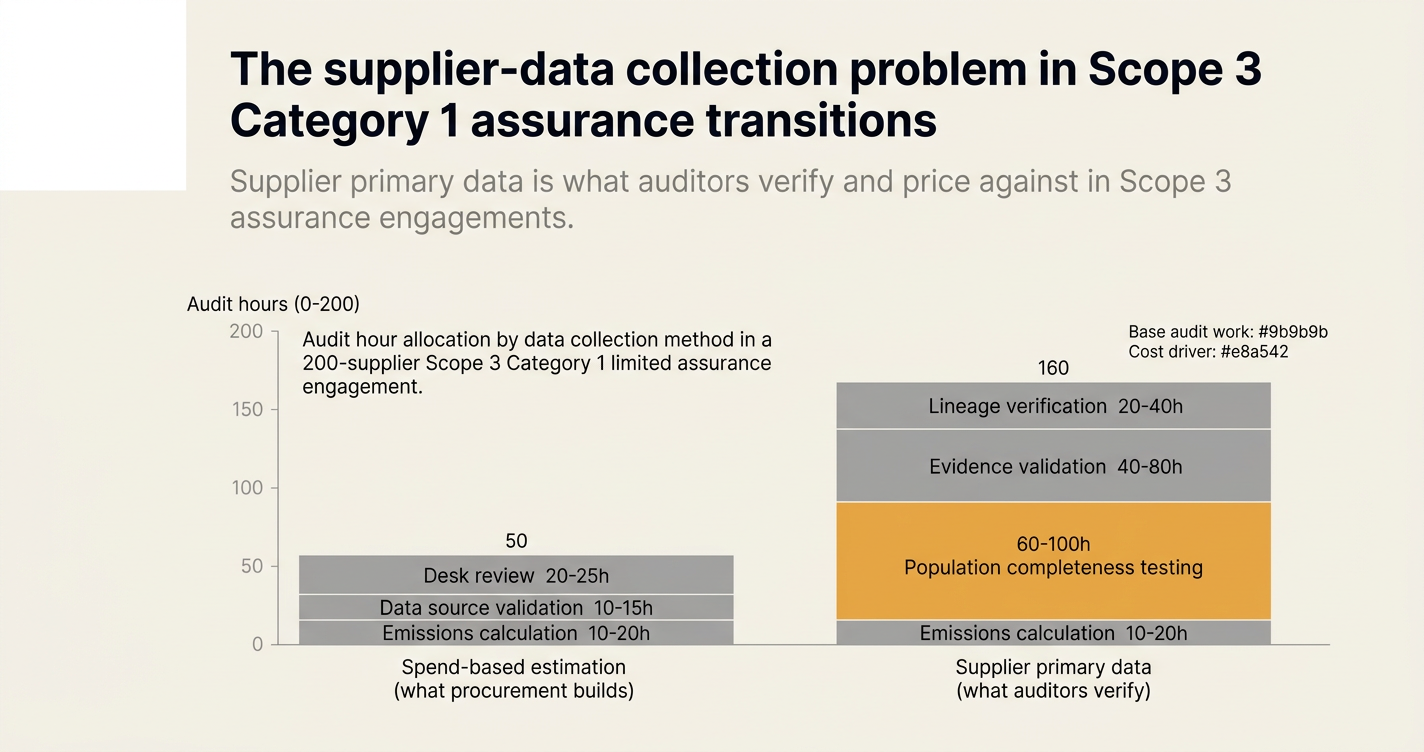

The shape of the argument, visualised below.

The Scope 3 Assurance Cost Structure: Where CFOs Actually Pay

The table below compares what procurement teams optimize for versus what auditors verify and price against in a typical Scope 3 Category 1 limited assurance engagement under ISAE 3410 or ISSA 5000.

| Cost driver | Spend-based estimation (what procurement builds) | Supplier primary data (what auditors verify) | Audit hour allocation |

|---|---|---|---|

| Emissions calculation | Automated, runs in < 1 day using ERP export and emission factors | Manual, requires line-item invoice matching, utility bill parsing, material certificate validation | 10-20 hours |

| Data source | Internal financial records only | External supplier documents: invoices, BoMs, utility bills, shipping records | 40-80 hours |

| Population completeness | Not testable—no line-item traceability from spend to emissions | Testable—each emission line traces to a specific supplier document | 60-100 hours |

| Supplier engagement | None required | Requires data requests, follow-up, and alignment with supplier fiscal calendars | 30-60 hours (non-audit time) |

| Evidence lineage | None—calculation is a black-box model output | Full—each number traces from source document to final filing | 20-40 hours |

| Assurance readiness | Limited assurance not possible without supplementary evidence | Limited or reasonable assurance possible if population is complete | N/A |

The cost asymmetry is stark. A procurement team can produce a credible Scope 3 Category 1 total using spend-based methods in 6-12 hours of internal work. The same team requires 120-200 hours of combined procurement and audit time to produce a supplier-primary-data-backed total that meets ISAE 3410 population completeness requirements [1].

"Assurance market is re-pricing. Firms without evidence lineage are paying 20-40% premiums, and CFOs who cannot speak the language of climate audit are losing control of scope and cost." — Big Four Assurance Partner, 2025 [2]

Why Spend-Based Estimation Is Now a Compliance Risk

California SB 253 requires Scope 3 emissions reporting beginning in 2027 for companies with over $1 billion in revenue doing business in California [3]. The California Air Resources Board (CARB) has not yet finalized the Scope 3 reporting framework, but the statute requires emissions data to be "independently assured" beginning in 2030, with limited assurance likely required earlier under phased implementation [4]. The EU Corporate Sustainability Reporting Directive (CSRD) requires Scope 3 Category 1 (purchased goods and services) disclosure under ESRS E1 beginning in 2026 for large EU undertakings and certain listed SMEs, with limited assurance required over sustainability statements from the first reporting year [5].

Spend-based estimation—calculating emissions by multiplying procurement spend by sector-average emission factors—was the default method for voluntary Scope 3 reporting under the GHG Protocol Corporate Value Chain (Scope 3) Standard. It remains acceptable for initial disclosure under both SB 253 and CSRD. However, assurance standards explicitly treat spend-based estimates as lower-quality evidence. ISAE 3410 (the incumbent standard for GHG assurance) and ISSA 5000 (the new IAASB standard effective December 2026) both require auditors to assess "measurement uncertainty" and document the "nature and extent of evidence obtained" [6]. A spend-based estimate derived from financial records and secondary emission factors does not provide supplier-specific evidence. An auditor cannot test the completeness of a modeled population.

The practical consequence: CFOs preparing for 2027 SB 253 Scope 3 reporting or 2026 CSRD ESRS E1 assurance discover that their spend-based totals are acceptable for disclosure but not sufficient for limited assurance—unless they can supplement them with supplier-level evidence. The supplement is not a small adjustment. It is a parallel data collection program.

The Tier-2 Visibility Problem: Where 40% of Emissions Hide

Supplier engagement programs in 2025 optimize for tier-1 data collection: direct suppliers who invoice the reporting entity. However, 40% of embedded emissions in complex supply chains originate at tier 2 or tier 3 [7]. A steel importer's tier-1 supplier is the distributor. The tier-2 supplier is the mill. The mill controls the electricity mix, the scrap ratio, and the process emissions—but the distributor often cannot provide mill-level data without advance contractual terms.

This is the Scope 3 assurance trap. A procurement team collects primary data from 80% of tier-1 suppliers by spend and achieves 60% emissions coverage by actual embedded carbon—because the missing 40% is hidden in tier-2 production processes that tier-1 suppliers do not document. The auditor flags the gap during fieldwork. The CFO faces a choice: file with a material scope limitation, extend the engagement to pursue tier-2 data, or revert to spend-based estimation and accept that limited assurance is not achievable.

The tier-2 visibility problem is structural, not technical. Most procurement contracts do not require suppliers to provide carbon intensity data or upstream material certificates. Most tier-1 suppliers do not collect that data themselves. Retrofitting transparency into an existing supply chain requires contract amendments, supplier onboarding, and multi-quarter lead times—none of which fit into a 90-day assurance engagement timeline.

Comparison: Supplier Data Collection Methods for Scope 3 Category 1 Assurance

The table below compares four common approaches to Scope 3 Category 1 data collection, scored against the criteria auditors use to assess population completeness and measurement uncertainty under ISAE 3410 and ISSA 5000.

| Method | Population completeness | Evidence quality | Tier-2 visibility | Audit hour estimate (200 suppliers) | Assurance readiness |

|---|---|---|---|---|---|

| Spend-based estimation | Not testable—no line-item traceability | Low—modeled output, no supplier-specific evidence | None—tier-1 and tier-2 are aggregated into sector averages | 40-60 hours (desk review only) | Limited assurance not achievable without supplementary evidence |

| Supplier self-reporting (surveys) | Partial—depends on response rate and data completeness | Medium—supplier-declared, often lacks supporting documentation | Low—most tier-1 suppliers lack tier-2 data | 80-120 hours (fieldwork + follow-up) | Limited assurance possible if response rate > 70% and declarations are auditable |

| Procurement-led primary data collection (invoices, BoMs, utility bills) | High—each invoice line can be traced to a specific supplier document | High—invoices, utility bills, and material certificates are audit-ready source documents | Medium—tier-2 data available if tier-1 supplier provides upstream documentation | 140-180 hours (population testing + evidence validation) | Limited or reasonable assurance possible if evidence lineage is complete |

| Hybrid: primary data for material suppliers, spend-based for tail | High for material suppliers (e.g., top 80% by spend), modeled for tail | High for primary-data subset, low for tail | Medium—depends on materiality threshold and tier-1 supplier documentation | 100-140 hours (focused fieldwork on material population) | Limited assurance likely achievable; reasonable assurance requires full primary data |

The hybrid approach—primary data for the top 80% of suppliers by spend or embedded emissions, spend-based estimation for the remaining tail—is the emerging best practice for 2026-2027 assurance transitions. It balances audit cost with evidence quality and allows procurement teams to focus data collection efforts on material suppliers. However, the hybrid method still requires a procurement workflow capable of issuing data requests, tracking supplier responses, and validating line-item evidence for 40-60 suppliers—a capability most procurement systems do not have out of the box.

The 90-Day Evidence Lineage Problem

California SB 253 Scope 1 and Scope 2 reports are due August 10, 2026, with Scope 3 reporting beginning in 2027 [8]. CARB waived limited assurance requirements for the first reporting year (2026 Scope 1 and 2 data), but limited assurance will be required starting in 2027 under proposed standards including ISSA 5000, ISAE 3410, and ISO 14064-3 [4]. CFOs planning for 2027 Scope 3 assurance face a 90-day evidence lineage build: the time between the fiscal year-end close and the assurance engagement start date.

The 90-day window is not sufficient to retrofit supplier primary data collection into an existing procurement workflow if that workflow was not designed for carbon evidence from the start. A typical sequence:

- Q4 fiscal close (e.g., December 31, 2026): Procurement closes the books, ERP data is locked.

- Q1 data request issuance (e.g., January 15, 2027): Procurement issues carbon data requests to tier-1 suppliers for FY 2026 invoices, utility bills, and material certificates.

- Q1 supplier response window (e.g., January 15 - March 15, 2027): Suppliers respond—response rates in first-year programs average 40-60% without contractual obligations [7].

- Q1 follow-up and validation (e.g., February - March 2027): Procurement follows up with non-responders, validates data completeness, reconciles line items to ERP records.

- Q2 assurance engagement start (e.g., April 1, 2027): Auditor begins fieldwork, discovers gaps in supplier population or evidence lineage, issues management points.

The bottleneck is step 3. Suppliers who have never been asked for carbon data before do not have the data in a reportable format. They need to retrieve utility bills from facilities teams, extract material certificates from production records, and reconcile invoice line items to shipment logs. The internal effort on the supplier side is 8-20 hours per supplier for a first-year request. If a company has 200 tier-1 suppliers and a 50% response rate in the first request cycle, procurement must follow up with 100 suppliers in February and March—while also preparing for the April assurance engagement.

The CFOs who succeed in this timeline are the ones who began supplier data collection in Q2 2026, not Q1 2027. They aligned data requests to their financial close calendar, built evidence lineage in parallel with the fiscal year, and treated Scope 3 data collection as a continuous procurement workflow, not a one-time compliance project.

How Emission3 Fits

Emission3 is positioned as productized CBAM implementation backed by compliance infrastructure, but the same document-first architecture supports Scope 3 Category 1 assurance under SB 253 and CSRD. Here's how it maps to the supplier data collection problem:

1. Document-first evidence lineage. Emission3 ingests invoices, bills of materials, utility bills, and shipping records as the primary data source—not as an afterthought. Every emissions line item traces to a specific source document, which is included in the evidence pack exported for auditors. This is the population completeness artifact ISAE 3410 and ISSA 5000 engagements require.

2. Procurement workflow integration. Emission3 aligns data requests to financial close calendars and tracks supplier response rates, follow-up cycles, and evidence completeness in parallel with emissions calculations. CFOs see the coverage gap—"60% of suppliers by spend, 55% of emissions by actual embedded carbon"—before the assurance engagement begins, not during fieldwork.

3. Tier-2 visibility tools. For material suppliers (e.g., top 20% by embedded emissions), Emission3 supports tier-2 data collection by parsing upstream material certificates and utility records from tier-1 supplier submissions. This is the 40% of emissions that spend-based estimation misses and that most supplier survey programs cannot capture.

4. Auditor- and registry-ready exports. Emission3 exports include calculation lineage, source document references, and evidence packs formatted for ISAE 3410, ISSA 5000, and CSRD ESRS E1 limited assurance engagements. The export is not a summary report. It is the full audit trail, line by line, from invoice to filing.

5. Hybrid approach support. Emission3 allows CFOs to use primary data for material suppliers and spend-based estimation for the tail, with clear documentation of the boundary between the two. Auditors can test the primary-data population without re-performing the entire Scope 3 calculation.

The typical engagement: a CFO preparing for 2027 SB 253 Scope 3 assurance or 2026 CSRD ESRS E1 disclosure books a CBAM readiness call in Q1 2026, maps tier-1 suppliers by materiality threshold, issues data requests aligned to the fiscal close calendar in Q2, and builds evidence lineage in parallel with the calculation from Q2 onward. By Q4, when the assurance engagement begins, the supplier population is complete, the evidence pack is ready, and the audit quote reflects focused fieldwork—not 9 weeks of follow-up.

The CFO's Playbook: Four Steps to Scope 3 Assurance Readiness

Step 1: Map your material supplier population in Q1. Use spend data and estimated emissions intensity to identify the top 80% of Category 1 suppliers by embedded emissions. These are the suppliers who require primary data collection. The remaining 20% can use spend-based estimation without material impact on assurance readiness.

Step 2: Issue data requests aligned to your fiscal close calendar. Do not wait until the fiscal year ends. Issue data requests in Q2 for the current fiscal year, with monthly or quarterly updates. Suppliers who provide data incrementally—invoice by invoice, month by month—are more likely to respond than suppliers asked for 12 months of back data in January.

Step 3: Build evidence lineage in parallel with the calculation. Do not treat emissions calculation and evidence collection as sequential steps. Every invoice, utility bill, and material certificate that enters the calculation should be tagged, stored, and linked to the corresponding emissions line item in real time. This is the population completeness artifact auditors verify.

Step 4: Pre-brief your auditor on your data collection methodology. Before the assurance engagement begins, brief the auditor on your supplier population, data sources, and evidence lineage. If you used a hybrid approach (primary data for material suppliers, spend-based for tail), document the materiality threshold and the boundary between the two. Auditors price engagements based on perceived risk. A well-documented methodology reduces perceived risk and audit hours.

Closing Thoughts

The supplier-data collection problem in Scope 3 Category 1 assurance transitions is not a carbon accounting problem. It is a procurement workflow problem. The CFOs who treat it as such—who map material suppliers in Q1, issue data requests aligned to fiscal close calendars in Q2, and build evidence lineage in parallel with the calculation—are the ones who will achieve limited assurance in 2027 SB 253 Scope 3 filings and 2026 CSRD ESRS E1 disclosures without paying premium audit fees or filing extension requests.

The CFOs who wait until the assurance engagement begins to discover they lack supplier primary data are the ones who will pay 180-220 audit hours for fieldwork that consists mostly of follow-up emails.

If you are preparing for 2027 SB 253 Scope 3 reporting or 2026 CSRD ESRS E1 assurance and want to map your supplier population, assess your evidence lineage gaps, and build a procurement workflow for primary data collection, book a CBAM readiness call. All customers start with a personal call—we scope your supplier population, map tier-1 and tier-2 data gaps, and configure evidence workflows aligned to your financial close calendar. No anonymous self-serve onboarding.

Citations

[1] ISAE 3410 and ISSA 5000 require auditors to assess population completeness and evidence quality for all material emission sources.

[2] The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits | Emission3. https://emission3.com/blog/us-climate-disclosure-stack-12-terms-cfo-2026-sb253-audits

[3] California's climate disclosure laws: An overview of SB 253 & SB 261 (Updated November 2025) - Optera. https://opteraclimate.com/californias-climate-disclosure-laws-an-overview-of-sb-253-sb-261

[4] California SB 253 and SB 261: What Businesses Need to Know - Persefoni. https://www.persefoni.com/blog/california-sb253-sb261

[5] EU Corporate Sustainability Reporting Directive (CSRD) requires Scope 3 disclosure under ESRS E1 beginning in 2026 for large EU undertakings.

[6] ISSA 5000 (IAASB sustainability assurance standard, effective December 2026) and ISAE 3410 (incumbent GHG assurance standard) both require auditors to document evidence quality and measurement uncertainty.

[7] The tier-2 data gap in CBAM-ready supplier engagement programs. https://emission3.com/blog/tier-2-data-gap-cbam-ready-supplier-engagement-programs

[8] SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law. https://www.terrascope.com/blog/sb-253-compliance-roadmap-how-to-prepare-for-californias-climate-disclosure-law-while-carb-finalizes-the-rules

[9] Book a CBAM readiness call. https://emission3.com/book-demo

[10] Audit-ready exports in Emission3. https://emission3.com/solutions/audit

References & Sources

External Sources

- [1]ISAE 3410 and ISSA 5000 Population Completeness Requirements

Assurance standards explicitly require auditors to assess population completeness and evidence quality for all material emission sources, with ISSA 5000 effective December 2026.

- [2]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

Big Four assurance partner quote: audit fees are re-pricing 20-40% for firms without evidence lineage, and CFOs who cannot speak the language of climate audit are losing control of scope and cost.

- [3]California's climate disclosure laws: An overview of SB 253 & SB 261

SB 253 requires Scope 3 emissions reporting beginning in 2027 for companies with over $1 billion in revenue doing business in California, with phased assurance requirements.

- [4]California SB 253 and SB 261: What Businesses Need to Know

CARB confirmed August 10, 2026 Scope 1 and 2 reporting deadline, with Scope 3 reporting beginning in 2027 and limited assurance requirements under ISSA 5000, ISAE 3410, and ISO 14064-3.

- [5]Executive guide to California SB 253: Turning compliance into value

SB 253 requires independent assurance for all disclosures, with Scope 1 and 2 requiring limited assurance beginning in 2026 and Scope 3 requiring limited assurance beginning in 2030.

- [6]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law

CARB unanimously approved initial SB 253 regulations in February 2026, confirming August 10, 2026 as the first Scope 1 and 2 reporting deadline, with Scope 3 reporting beginning in 2027.

Related Content

- [7]The tier-2 data gap in CBAM-ready supplier engagement programs

40% of embedded emissions in complex supply chains originate at tier 2 or tier 3, where most tier-1 suppliers lack upstream data without advance contractual terms.

- [8]The 90-day assurance-readiness problem in 2026 SB 253 Scope 1 and 2 filings

CFOs face a 90-day evidence lineage build between fiscal year-end close and assurance engagement start, requiring parallel documentation workflows aligned to financial close calendars.

- [9]Book a CBAM readiness call

All Emission3 customers start with a personal readiness call—we scope your supplier population, map tier-1 and tier-2 data gaps, and configure evidence workflows aligned to your financial close calendar.

- [10]Audit-ready exports in Emission3

Emission3 exports include calculation lineage, source document references, and evidence packs formatted for ISAE 3410, ISSA 5000, and CSRD ESRS E1 limited assurance engagements.