The assurance-standard gap in 2026 CSRD filing programs

The assurance-standard gap in 2026 CSRD filing programs

Here's the issue: compliance officers preparing for Corporate Sustainability Reporting Directive (CSRD) filings in 2026 face a procedural gap that looks administrative but carries material cost. Teams assume assurance standards will be published in time for their first audit cycle. The European Commission's original timeline promised limited assurance standards by October 2026, giving First Wave companies a full year to prepare their evidence chains before the 2027 filing deadline. That timeline now looks optimistic.

However, a CSRD filing consists of two things: the sustainability statement itself and the assurance methodology that validates it. Companies allocate budget and internal hours to the first—data collection, European Sustainability Reporting Standards (ESRS) alignment, double materiality assessments. But the second determines auditor scope, evidence requirements, and the actual cost of the engagement.

The sustainability statement on its own has no regulatory value. The assurance opinion is what the regulator is actually asking for. Without adopted standards, auditors fall back on national frameworks or Committee of European Auditing Oversight Bodies (CEAOB) guidelines from September 2024, which are non-binding. This creates a methodology divergence problem: two companies in different Member States, filing identical ESRS disclosures, may face different evidence thresholds depending on which national standard their auditor applies.

While data collection has become cheaper—carbon accounting platforms, supplier engagement tools, automated ESRS taxonomies—assurance has become more expensive. If the Commission delays adoption past mid-2026, First Wave companies will enter their first audit cycle without harmonised methodology. Auditors price uncertainty into their fees. A deferred standard might add 15-20% to the first-year assurance engagement, not because the work changes, but because the scope remains undefined until the auditor chooses a national fallback.

How do you solve this? I think the operators we work with are treating 2026 as a dry-run year for assurance readiness. They are building evidence chains now—document lineage, calculation reproducibility, internal control documentation—assuming the most rigorous interpretation of limited assurance will eventually be adopted. For now, that means mapping every ESRS datapoint to a source document, even before the auditor arrives.

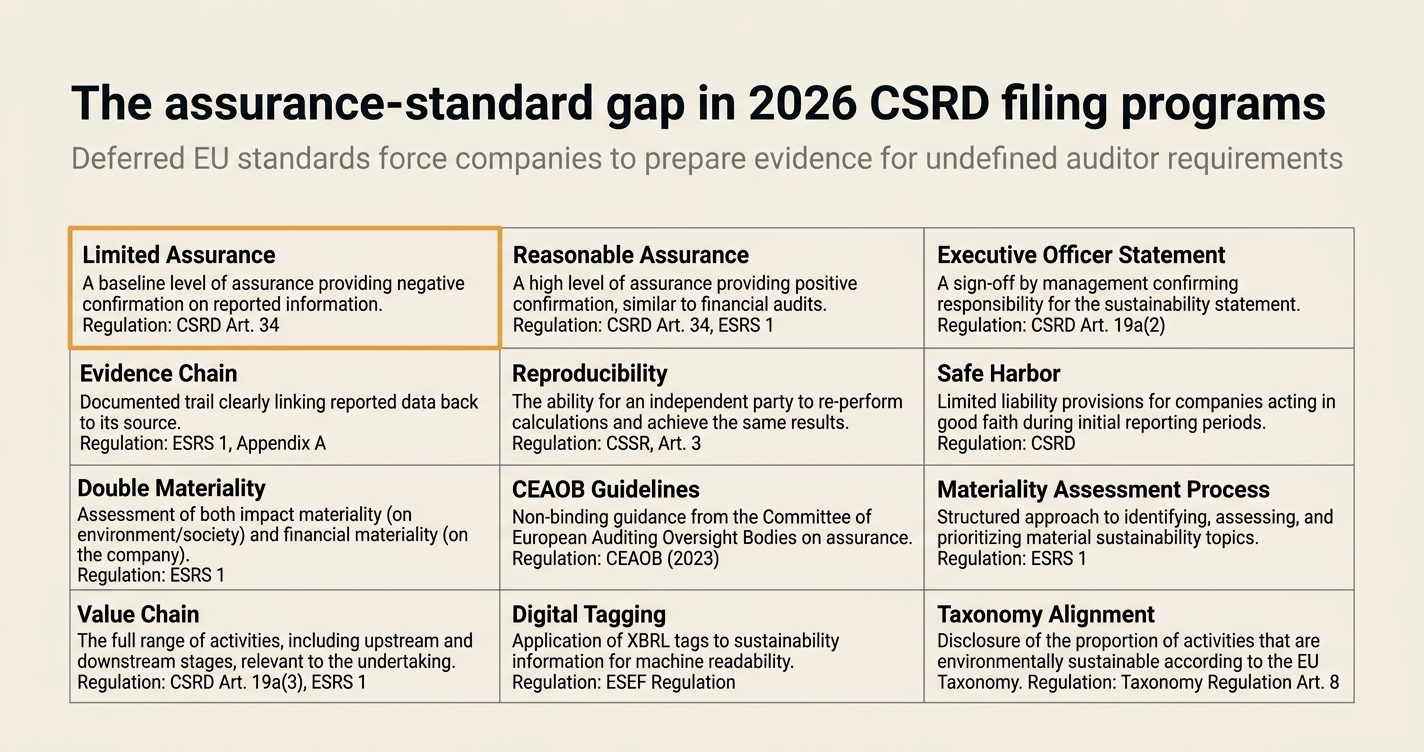

The shape of the argument, visualised below.

The assurance-standard vocabulary for 2026 CSRD filings

Compliance officers will hear these terms in the next audit cycle. Each definition includes a plain-English explanation, a worked example from CSRD implementation, and the source regulation.

Limited assurance

An audit procedure where the assurance provider gathers sufficient evidence to conclude that nothing has come to their attention indicating the reported information is materially misstated. Less rigorous than reasonable assurance, but still requires systematic evidence review.

Worked example: An auditor reviews your Scope 1 emissions calculation for a manufacturing facility. Under limited assurance, they sample utility bills, confirm the methodology aligns with ESRS E1, and check that calculation errors are below materiality thresholds. They do not verify every invoice or recompute every conversion factor.

Source regulation: CSRD Article 19a(7) requires limited assurance on sustainability statements. The European Commission was mandated to adopt limited assurance standards by October 1, 2026, but this deadline has been postponed to July 1, 2027 under Omnibus I revisions [1].

Reasonable assurance

An audit procedure where the assurance provider obtains sufficient appropriate evidence to conclude with high confidence that the reported information is free from material misstatement. Equivalent to a financial audit in rigor.

Worked example: Under reasonable assurance, the auditor would verify every utility bill, recompute emission factors independently, test internal controls over data entry, and confirm third-party data with original sources. The evidence threshold is substantially higher.

Source regulation: The original CSRD empowered the European Commission to adopt reasonable assurance standards for sustainability reporting. However, Omnibus I revisions remove this requirement entirely to avoid increased costs for reporting entities [2]. The CSRD will remain at limited assurance indefinitely.

Executive officer statement

A formal declaration, signed by a company's management, affirming that the sustainability statement complies with CSRD requirements and that internal controls over sustainability data are adequate. Carries personal liability under some Member State implementations.

Worked example: Your CFO signs the management report accompanying the CSRD filing, stating: "To the best of our knowledge, the sustainability information has been prepared in accordance with the applicable reporting standards and gives a true and fair view." If the auditor later identifies material misstatements, the CFO may face penalties depending on national transposition.

Source regulation: CSRD Article 29a requires Member States to ensure that management declares responsibility for sustainability reporting. This mirrors the management representation letter in financial audits but extends to non-financial data. Omnibus I introduces a maximum penalty cap of 3% of an entity's net worldwide turnover for breaches [3].

Evidence chain

The documented lineage connecting a disclosed datapoint to its source documents, through all calculation steps, assumptions, and internal controls. Required for auditor replicability.

Worked example: You disclose 1,847 tonnes of Scope 2 emissions in your ESRS E1 filing. The evidence chain includes: (1) monthly utility invoices from January-December, (2) the IEA emission factor for your regional grid, (3) the spreadsheet calculation applying the factor to kWh consumed, (4) the internal control log showing who reviewed the calculation and when.

Source regulation: While CSRD does not explicitly mandate "evidence chains," ESRS 2 General Requirements (ESRS 2 BP-2) requires disclosure of the basis of preparation, including data sources and estimation techniques [4]. Assurance providers will request this documentation under any limited assurance standard.

Reproducibility

The principle that an independent auditor, given the same source documents and methodology, should arrive at the same disclosed value. Central to deterministic carbon accounting.

Worked example: Your disclosed Scope 3 Category 1 emissions total 12,430 tonnes. An auditor takes your supplier invoices, applies your documented emission factors, and recalculates. If they arrive at 12,428 tonnes (within rounding), the calculation is reproducible. If they arrive at 14,100 tonnes, it is not, and the filing fails assurance.

Source regulation: ESRS 2 BP-2 requires entities to explain the methods and assumptions used to prepare sustainability information. Reproducibility is implicit: if the method is explained but not replicable, the disclosure does not meet the standard [4].

Safe harbor

A regulatory provision that protects companies from penalties if they disclose information in good faith, even if later found to be inaccurate, provided they followed prescribed procedures.

Worked example: Under California Senate Bill 253 (SB 253), companies that engage a third-party assurance provider and disclose emissions using a recognised methodology are shielded from penalties if emission factors later change. CSRD does not currently include an equivalent safe harbor provision.

Source regulation: CSRD Article 29a allows Member States to define penalties for non-compliance but does not provide explicit safe harbor language. Companies rely on "without undue cost or effort" clauses in ESRS for proportionality, but this is not a safe harbor in the strict sense [5].

Double materiality

The assessment framework requiring companies to evaluate both financial materiality (how sustainability matters affect the company) and impact materiality (how the company affects people and the environment). A disclosure is material if it meets either test.

Worked example: Your company manufactures batteries. Water consumption is financially immaterial—it represents 0.2% of operating costs. However, your facility withdraws water from a watershed under severe stress, affecting local agriculture. Under impact materiality, water consumption is material and must be disclosed under ESRS E3.

Source regulation: CSRD Article 29b and ESRS 1 General Requirements define double materiality as the foundation of ESRS reporting. Both dimensions must be assessed, and disclosures are required if either threshold is met [4].

CEAOB guidelines

Non-binding guidance issued by the Committee of European Auditing Oversight Bodies in September 2024, intended to promote consistency in limited assurance engagements until the European Commission adopts formal standards.

Worked example: Your auditor references CEAOB guidelines to determine evidence sampling rates for your ESRS E1 climate disclosures. The guidelines suggest materiality thresholds and testing procedures but are not legally binding. Another auditor in a different Member State may interpret the same guidelines differently.

Source regulation: CSRD Article 26(6) requires CEAOB to develop non-binding guidelines to promote consistency. The September 2024 guidelines are the current reference, but they will be superseded once the Commission adopts formal limited assurance standards in July 2027 [1].

Materiality assessment process

The documented procedure a company uses to identify which ESRS topics and datapoints are material. Must include stakeholder engagement, impact analysis, and financial risk assessment. Subject to assurance.

Worked example: Your materiality assessment process includes: (1) interviews with 15 key suppliers and 8 investors, (2) a scored impact matrix for each ESRS topic, (3) board-level review of the materiality threshold, (4) documentation of topics excluded and why. The auditor will test whether this process was followed and whether excluded topics were reasonably assessed.

Source regulation: ESRS 2 SBM-3 requires disclosure of the process used to identify material impacts, risks, and opportunities. The assurance engagement must cover this process, not just the resulting disclosures [1].

Value chain

All upstream and downstream activities connected to a company's operations, including suppliers (upstream) and customers/end-of-life (downstream). ESRS reporting extends across the value chain for material topics.

Worked example: You manufacture steel. Your value chain includes: upstream—iron ore mines, coking coal suppliers, electricity grids powering your furnaces; downstream—automotive OEMs using your steel, vehicles in use, eventual recycling. ESRS E1 requires you to disclose Scope 3 emissions from material segments of this chain.

Source regulation: ESRS 1 defines value chain in paragraph 63. ESRS E1-6 requires disclosure of Scope 3 emissions, which by definition cover value chain activities [4]. Omnibus I simplifications reduce the number of mandatory Scope 3 categories but do not eliminate value chain reporting.

Digital tagging

The requirement to mark up ESRS disclosures using XHTML and inline XBRL, allowing machine-readable extraction and comparison in the European Single Access Point (ESAP) database.

Worked example: You disclose your Scope 1 emissions as "1,847 tonnes CO₂e" in your management report. Digital tagging requires you to wrap this value in an XBRL tag identifying it as ESRS E1 metric E1-6, with metadata for the reporting period, unit of measure, and consolidation scope. The auditor will verify that tags match the underlying data.

Source regulation: CSRD Article 29b(4) mandates digital tagging using the European Single Electronic Format (ESEF). Assurance must cover compliance with tagging requirements, not just the narrative disclosures [1].

Taxonomy alignment

The process of determining which proportion of a company's revenues, capital expenditures, and operating expenditures qualify as environmentally sustainable under the EU Taxonomy Regulation. CSRD filings must include Taxonomy alignment disclosures.

Worked example: Your company operates wind farms (Taxonomy-eligible activity under Climate Change Mitigation). You calculate that 87% of your revenues meet the technical screening criteria for substantial contribution to climate mitigation and do no significant harm to other environmental objectives. This 87% is your Taxonomy-aligned revenue.

Source regulation: CSRD Article 8 requires large companies to disclose Taxonomy-aligned proportions of revenues, CapEx, and OpEx. ESRS E1-9 specifies the disclosure format. Assurance must cover the Taxonomy alignment calculation [4].

The methodology divergence problem in 2026 audits

The deferral of harmonised limited assurance standards creates three operational gaps for First Wave companies filing in 2027:

| Gap dimension | What it means | Cost implication |

|---|---|---|

| Evidence scope | Without EU-wide standards, auditors apply national frameworks with different sampling thresholds. A German auditor may test 25% of transactions; a French auditor may test 40%. | First-year assurance fees vary by 15-30% depending on Member State, even for identical ESRS disclosures. |

| Methodology interpretation | CEAOB guidelines are non-binding. Auditors interpret "sufficient evidence" differently. Some require source documents for every datapoint; others accept management representations for immaterial items. | Companies in conservative jurisdictions prepare 30-50% more documentation than peers elsewhere, driving internal cost up. |

| Digital tagging verification | No adopted standard specifies how auditors test XBRL accuracy. Some firms sample 10% of tags; others verify every tag. | Tagging errors discovered late in the audit cycle can delay filing and trigger restatements, adding 4-6 weeks to the close process. |

The European Commission's July 2027 target for adopting limited assurance standards means First Wave companies enter their inaugural audit cycle without a playbook. Auditors price this ambiguity into engagement letters. The risk is not that the audit fails—it is that two equivalent companies pay materially different fees for the same level of assurance, depending on which national standard their auditor defaults to.

"Until these standards are adopted, assurance providers should base their work on national assurance standards for sustainability reporting." — RSM Global, CSRD assurance guidance [5]

This is why reproducibility and evidence lineage are worth over-investing in now. When the auditor arrives in Q1 2027, they will request documentation for every material datapoint. If your carbon accounting system cannot reproduce a disclosed value from source documents, the auditor must either expand testing (increasing fees) or issue a qualified opinion. Neither outcome supports a smooth first filing.

How Emission3 fits

Emission3 is designed for CSRD filers who need assurance-ready documentation without manually maintaining evidence chains. The platform ingests source documents—utility bills, supplier invoices, shipping manifests—and constructs a deterministic lineage from each document to its corresponding ESRS metric. When the auditor requests evidence for a disclosed Scope 2 total, Emission3 exports the invoice set, the calculation lineage, and the applied emission factors as a single artifact.

Three architectural decisions make this possible:

-

Document-first ingestion: Every emission value originates from a source document. Emission3 does not accept manual entries unless they are linked to a supporting file. This matches how auditors test: they start with the disclosed number and trace backward to the source.

-

Deterministic LLM layer: Emission3's AI does not estimate or infer. It extracts structured data (invoice line items, kWh consumed, shipment weights) and applies deterministic calculations. The LLM's role is data structuring, not approximation. An auditor can replay the extraction logic and arrive at the same result.

-

Audit-pack exports: The platform generates evidence packs for each ESRS metric, bundling source documents, calculation steps, emission factors, and lineage metadata. These packs are designed for CEAOB guideline compliance, anticipating the eventual EU limited assurance standard.

For compliance officers preparing for 2027 filings, this removes the manual spreadsheet reconciliation that consumes 40-60% of assurance preparation time. The evidence chain is constructed during data entry, not after the fact.

Closing: start with the evidence chain, not the disclosure

The deferred assurance standard does not change what must be disclosed under ESRS—it changes how you must prove it. First Wave companies filing in 2027 should assume their auditor will apply the most rigorous interpretation of limited assurance available in their Member State. That means building evidence lineage now, before the engagement letter arrives.

If you are preparing a 2027 CSRD filing, the question is not whether your sustainability data is accurate—it is whether you can reproduce it on demand, from source documents, in a format that satisfies an auditor applying an unknown national standard. Emission3's audit-ready exports are designed for that scenario. See how the platform constructs evidence chains at /solutions/audit, or book a CSRD readiness call at /book-demo to map your documentation gaps before the audit cycle begins [6][7].

References & Sources

External Sources

- [1]Revisions to CSRD and CSDDD finalized - Grant Thornton

Summarises Omnibus I changes to CSRD assurance timelines, including the postponement of limited assurance standard adoption to July 2027 and the removal of reasonable assurance requirements.

- [2]EU Omnibus I: CSRD & CSDDD Changes - Adherent

Details the removal of reasonable assurance transition requirements under Omnibus I, avoiding increased costs for reporting entities.

- [3]CSRD Agreed: A Major Recalibration of the EU Sustainability Reporting Regime - Proskauer

Explains Omnibus I's introduction of a maximum penalty cap of 3% of net worldwide turnover for CSRD breaches.

- [4]CSRD Explained (2026): Requirements, Scope & How to Comply - Normative

Overview of CSRD requirements, including ESRS double materiality principles, limited assurance obligations, and value chain reporting scope.

- [5]How will assurance reporting work under CSRD? - RSM Global

Guidance on CSRD assurance scope, including the use of national standards until EU-wide limited assurance standards are adopted.

Related Content

- [6]Audit-ready exports in Emission3

Shows the evidence lineage artifact Emission3 generates for auditors, including document-to-metric traceability.

- [7]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation, no anonymous self-serve onboarding.