The population-level evidence gap in ISAE 3410 to ISSA 5000 transitions

The population-level evidence gap in ISAE 3410 to ISSA 5000 transitions

Here's the issue: The International Auditing and Assurance Standards Board withdrew ISAE 3410, Assurance Engagements on Greenhouse Gas Statements, effective December 15, 2026. From that date forward, greenhouse gas assurance engagements will be conducted under ISSA 5000, General Requirements for Sustainability Assurance Engagements. For organisations that have obtained limited assurance under ISAE 3410 for their 2025 or 2026 reporting years, the standard transition appears straightforward: continue the engagement under the new framework. At first glance, the shift looks procedural—a question of updating engagement letters and assurance report language.

However, an ISAE 3410 to ISSA 5000 transition consists of two things: assurance continuity and population-level evidence completeness. Assurance continuity addresses whether the engagement team can apply the new standard's requirements to the same GHG inventory scope and boundary. Population-level evidence completeness addresses whether the organisation's existing data collection systems can prove that every transaction in the GHG statement has been captured, not just the items the auditor sampled.

Assurance continuity on its own has no value. Population-level evidence completeness is what the auditor is actually verifying under ISSA 5000. ISAE 3410 permitted sampling-based limited assurance, where the practitioner performed inquiry and analytical procedures on selected data points to conclude whether anything had come to their attention indicating material misstatement. ISSA 5000 requires the assurance provider to obtain sufficient appropriate evidence to support the conclusion, and paragraph 69 explicitly requires the practitioner to evaluate whether the evidence obtained is sufficient and appropriate. For Scope 3 inventories built from hundreds of supplier invoices, utility bills, and third-party datasets, this means proving population completeness: that the dataset the auditor is reviewing is the entire population, not a curated sample.

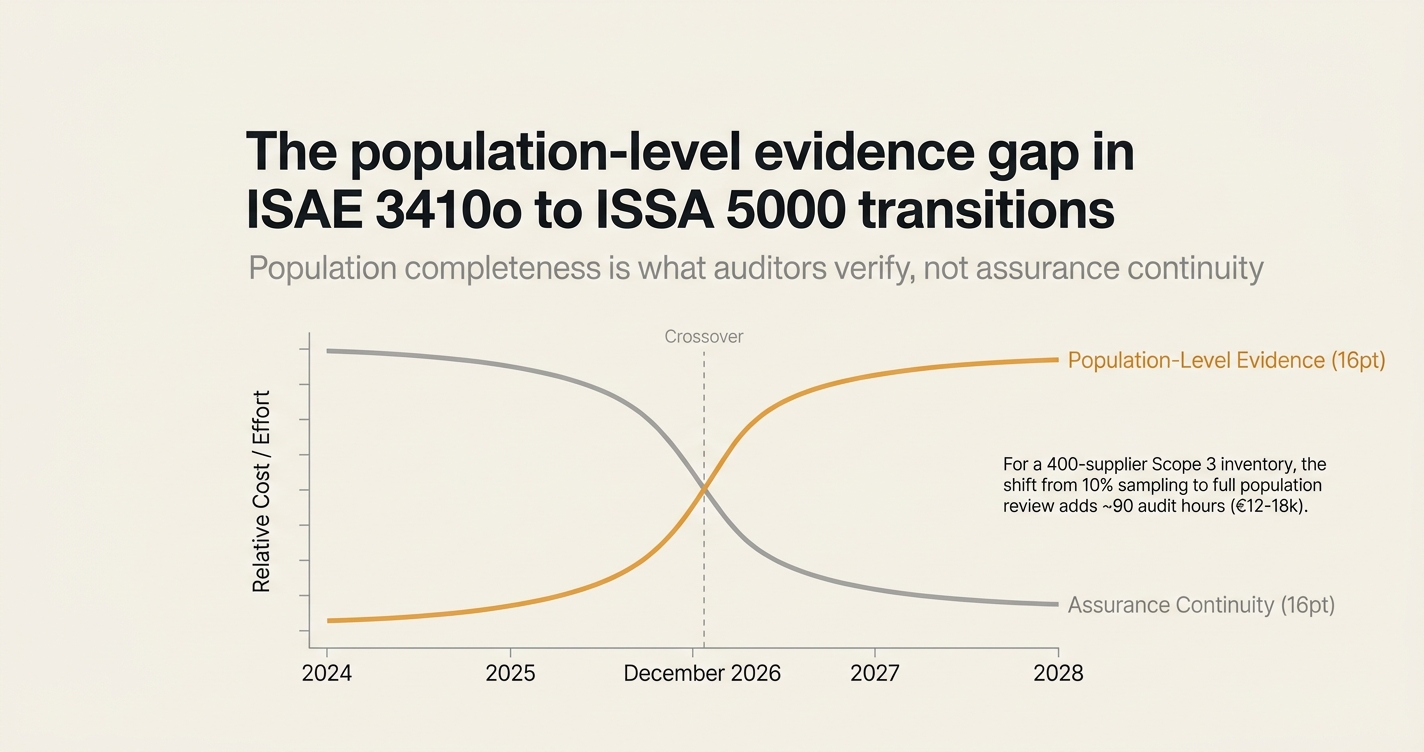

While assurance continuity has become easier—ISSA 5000's structure is more explicit than ISAE 3410's principles-based approach—population-level evidence has become more expensive. KPMG's ISSA 5000 implementation guide notes that the new standard has 212 requirements, more than double those of ISAE 3000, and that the requirements are more specific and targeted for sustainability assurance engagements. For a Scope 3 Category 1 inventory covering 400 suppliers, if the organisation cannot produce a reconciliation between the procurement ledger and the GHG inventory at the line-item level, the auditor may need to expand testing from a statistical sample to a full population review. At 15 minutes per supplier record, the audit cost difference between sampling 40 records and reviewing 400 records is approximately 90 hours, or 12,000 to 18,000 euros depending on geography and firm.

How do you solve this? I think the answer depends on whether the organisation's current ISAE 3410 engagement was based on sampling or full population review. For operators we work with who have already built line-item reconciliations between source documents and GHG calculations, the ISSA 5000 transition is largely a question of updating the assurance report language and ensuring the engagement team applies the new standard's expanded requirements. For operators whose current ISAE 3410 engagement relies on sampling, the transition will require building population-level evidence infrastructure before the December 2026 effective date. For now, that infrastructure looks like deterministic calculation lineage: a system that can prove, at the line-item level, that every supplier invoice in the procurement ledger appears in the GHG inventory, and that every emission factor applied to that invoice is traceable to a named source.

The shape of the argument, visualised below.

The structural difference between ISAE 3410 and ISSA 5000

ISAE 3410 was a principles-based standard that provided flexibility for assurance providers to design procedures appropriate to the engagement circumstances. ISSA 5000 is a requirements-based standard that specifies the evidence-gathering and documentation obligations at a more granular level. The table below compares the two frameworks on dimensions that affect population-level evidence requirements.

| Dimension | ISAE 3410 (withdrawn Dec. 15, 2026) | ISSA 5000 (effective Dec. 15, 2026) |

|---|---|---|

| Total requirements | ~100 (inherited from ISAE 3000) | 212 specific requirements [1] |

| Scope | GHG statements only | All sustainability information, including GHG [2] |

| Evidence sufficiency | Practitioner judgment based on engagement risk | Explicit requirement to evaluate sufficiency and appropriateness of evidence obtained (para. 69) |

| Sampling vs. population | Sampling permitted for limited assurance | Population completeness testing required when risk of material misstatement is high |

| Other information | No specific requirement | Rigorous approach: assurance provider must read and consider other information presented with sustainability information [1] |

| Effective date | Withdrawn December 15, 2026 | December 15, 2026 (periods beginning on or after this date) [2] |

The key structural shift is in evidence sufficiency. ISAE 3410 allowed the practitioner to conclude that "nothing has come to my attention" based on inquiry and analytical procedures applied to a sample. ISSA 5000 requires the practitioner to evaluate whether the evidence obtained is sufficient and appropriate to support the assurance conclusion. For inventories where the underlying transaction population is large and heterogeneous—such as Scope 3 Category 1 purchased goods—this shifts the burden from the auditor's professional judgment to the organisation's data completeness infrastructure.

The California SB 253 and EU CSRD parallel

The ISAE 3410 to ISSA 5000 transition mirrors regulatory transitions already underway in California and the European Union. California's Senate Bill 253, the Climate Corporate Data Accountability Act, requires limited assurance for 2025 Scope 1 and 2 data (reported in 2026) with a transition to reasonable assurance for 2029 data. The California Air Resources Board waived the assurance requirement for the 2026 reporting year but retained the documentation quality requirements. As one public comment to CARB noted, "ISSA 5000 has 212 requirements, which is more than double those of ISAE 3000. This adds a significant increase to the amount of work" [3].

Similarly, the European Union's Corporate Sustainability Reporting Directive requires limited assurance on ESRS E1 climate disclosures beginning with 2024 reporting (2025 filings for calendar-year reporters), with a transition to reasonable assurance by 2028. The assurance-level problem in EU CSRD limited-to-reasonable transitions is that auditors charge for reasonable procedures—and most first-wave reporters lack the controls to support them [4]. The structural issue is the same: the transition from sampling-based limited assurance to population-level reasonable assurance requires organisations to prove completeness at the transaction level, not just at the aggregate level.

"ISSA 5000 is flexible to be used to report on all sustainability topics and frameworks and scales its requirements for both reasonable and limited assurance engagements. Reasonable assurance is equivalent to a financial statement audit, while limited assurance provides an acceptable level of assurance that is less than reasonable but is still meaningful for the intended users." [1]

The withdrawal of ISAE 3410 and the introduction of ISSA 5000 is not a like-for-like replacement. It is a structural shift from principles-based assurance to requirements-based assurance, with explicit expectations for evidence sufficiency that mirror the reasonable assurance procedures most organisations will face under SB 253 and CSRD within three years.

What population-level evidence looks like in practice

Population-level evidence for a Scope 3 Category 1 inventory means proving that the dataset the auditor is reviewing is the entire population of purchased goods transactions, not a curated export or filtered subset. This requires three artifacts:

-

Procurement ledger reconciliation: A line-item mapping between the organisation's procurement ledger and the GHG inventory, showing that every invoice in the ledger either appears in the inventory or is explicitly excluded with a documented reason (e.g., out-of-scope category, de minimis threshold).

-

Emission factor traceability: For every line item in the inventory, a documented link between the emission factor applied and the source database (e.g., DEFRA 2024, EPA 2023, supplier-specific EPD), including the version, publication date, and retrieval method.

-

Calculation lineage: A deterministic calculation trail from the source document (invoice, bill of lading, utility bill) to the final tCO₂e figure, such that an auditor can reproduce the calculation independently without relying on the organisation's spreadsheet or software interface.

For organisations whose current ISAE 3410 engagement relies on sampling, the absence of these artifacts is not yet a non-conformance—ISAE 3410 did not require them for limited assurance. Under ISSA 5000, their absence will be a gap. The auditor will either need to expand sampling to approach full population review, or the organisation will need to build the artifacts before the engagement begins.

The cost difference is material. An Australian assurance provider noted in their ASAE 3410 (the Australian equivalent of ISAE 3410) engagement letter that limited assurance procedures "focus on aggregated data rather than physically checking source data at sites," and that "the extent of evidence-gathering for a limited assurance engagement is less than for a reasonable assurance engagement" [5]. Under ISSA 5000, the extent of evidence-gathering is determined by the risk of material misstatement, not by the assurance level. If the risk is high—as it often is for Scope 3 inventories where supplier data quality is variable—the assurance provider must obtain sufficient appropriate evidence regardless of whether the engagement is limited or reasonable assurance.

The timeline constraint for December 2026 year-ends

ISSA 5000 is effective for assurance engagements on sustainability information reported for periods beginning on or after December 15, 2026 [2]. For calendar-year reporters, this means the standard applies to 2027 data, reported in 2028. However, many organisations with December 2026 year-ends will be completing their ISAE 3410 engagements in early 2027, during the window when ISSA 5000 is already effective but not yet required for their reporting period. The practical question is whether to accelerate the transition.

The argument for accelerating the transition is that building population-level evidence infrastructure takes time. If the organisation waits until the mandatory effective date (periods beginning on or after December 15, 2026), it will have less than 12 months to build the infrastructure before the first ISSA 5000 engagement begins. If the organisation begins the transition during the 2026 ISAE 3410 engagement, it can use the engagement as a readiness assessment: the auditor identifies the gaps, the organisation builds the artifacts during 2027, and the 2027 ISSA 5000 engagement proceeds without timeline pressure.

The argument against accelerating the transition is cost. As noted in a public comment to CARB, "the use of ISSA 5000 will not yet be required, and ISAE 3000 and ISAE 3410 will still be available for use" for the first SB 253 reporting year (FY 2025, reported in 2026) [3]. Organisations that complete their final ISAE 3410 engagement in early 2027 will have the benefit of 18 months of regulatory and practitioner guidance on ISSA 5000 before their first mandatory engagement. For operators with stable year-over-year inventories and low supplier turnover, this may be sufficient.

The constraint is that ISSA 5000 does not allow for a phased transition. Once the standard is effective for the reporting period, the full set of requirements applies. There is no grace period for population-level evidence infrastructure.

The sampling-to-population cost delta

The cost of building population-level evidence infrastructure depends on the current state of the organisation's GHG data collection systems. The table below estimates the cost difference between sampling-based ISAE 3410 limited assurance and population-level ISSA 5000 limited assurance for a representative Scope 3 Category 1 inventory.

| Inventory characteristic | Sampling-based ISAE 3410 (current) | Population-level ISSA 5000 (required) | Cost delta |

|---|---|---|---|

| Number of supplier records | 400 | 400 | — |

| Records reviewed by auditor | 40 (10% sample) | 400 (full population) | +360 records |

| Time per record (review + documentation) | 15 minutes | 15 minutes | — |

| Total audit hours | 10 hours | 100 hours | +90 hours |

| Blended auditor rate (EU mid-tier firm) | €150/hour | €150/hour | — |

| Audit cost | €1,500 | €15,000 | +€13,500 |

| Organisation time to prepare reconciliation | — | 40 hours (one-time) | +40 hours |

| Organisation time to maintain reconciliation | — | 5 hours/quarter | +20 hours/year |

The cost delta is not linear. If the organisation already has a deterministic calculation lineage system that produces procurement ledger reconciliations automatically, the incremental cost of the ISSA 5000 engagement is close to zero: the auditor reviews the same artifacts under a different standard. If the organisation does not have such a system, the incremental cost includes both the one-time buildout (40 hours to create the initial reconciliation) and the ongoing maintenance (20 hours per year to update it as suppliers and products change).

For operators with high supplier turnover or frequent product mix changes, the ongoing maintenance cost is the binding constraint. A procurement team that onboards 50 new suppliers per year will need to reconcile 50 new supplier records to the GHG inventory each quarter. At 15 minutes per record, this is 12.5 hours per year of incremental work. If the organisation does not automate this reconciliation, the cost accumulates year over year.

How Emission3 fits

Emission3 is built for this transition. The platform is document-first: it ingests supplier invoices, bills of material, and utility bills, and produces line-item evidence packs that show the calculation lineage from source document to final tCO₂e. For auditors, this means the procurement ledger reconciliation, emission factor traceability, and calculation lineage artifacts are produced automatically as part of the normal data collection workflow, not as a separate audit preparation exercise.

The architecture is deterministic: every calculation is reproducible, and every emission factor is traceable to a named source with version and publication date. When the auditor asks "how did you calculate this number," the answer is a lineage trace, not a spreadsheet cell reference. For ISSA 5000 paragraph 69 (evaluating sufficiency and appropriateness of evidence), this means the auditor can replay the calculation independently, without relying on the organisation's software interface.

The platform also produces submission-oriented outputs for CBAM, SB 253, and CSRD, so the same evidence base that supports the ISSA 5000 engagement also supports the regulatory filing. This matters for operators facing multiple disclosure regimes: the cost of building population-level evidence infrastructure is amortised across CBAM, SB 253, CSRD, and the annual ISSA 5000 engagement, rather than being a standalone audit preparation cost.

For teams evaluating whether to accelerate the ISAE 3410 to ISSA 5000 transition, the decision hinges on whether the current ISAE 3410 engagement is sampling-based or population-based. If it is already population-based, the transition is largely procedural. If it is sampling-based, the organisation has until December 2026 to build the population-level evidence infrastructure that ISSA 5000 requires. The operators we work with are building that infrastructure now, during the final ISAE 3410 engagements, so the first ISSA 5000 engagement in 2027 or 2028 proceeds without timeline pressure.

Start with a readiness conversation

The ISAE 3410 to ISSA 5000 transition is not a like-for-like standard replacement. It is a structural shift from sampling-based limited assurance to population-level evidence completeness, and the cost of that shift depends on whether your current data collection systems can prove completeness at the line-item level. If your current ISAE 3410 engagement relies on sampling, you have approximately 12 months to build the population-level evidence infrastructure before the December 2026 effective date.

Emission3 helps exporters, importers, and US firms become CBAM-ready, SB 253-ready, and CSRD-ready in weeks, using the compliance infrastructure we already built. For auditors and assurance providers, we produce audit-ready evidence packs with full calculation lineage and procurement ledger reconciliations. All engagements start with a CBAM readiness call, where we map your current data collection systems, identify the gaps, and estimate the time and cost to close them [6].

Book a CBAM readiness call to evaluate whether your current ISAE 3410 evidence base is sufficient for ISSA 5000, or whether you need to build population-level evidence infrastructure before the December 2026 effective date.

References & Sources

External Sources

- [1]Are you ready for ISSA 5000? – KPMG

KPMG's implementation guide noting that ISSA 5000 has 212 requirements, more than double those of ISAE 3000, with more specific and targeted requirements for sustainability assurance engagements.

- [2]ISAE 3410 Assurance Engagements on Greenhouse Gas Statements (to be withdrawn Dec. 15, 2026) – IAASB

IAASB withdrawal announcement confirming that ISAE 3410 has been withdrawn with effect from December 15, 2026, the effective date of ISSA 5000.

- [3]Public Comments to August 21, 2025 Climate Disclosure Workshop – California Air Resources Board

Public comment noting that ISSA 5000 has 212 requirements, more than double those of ISAE 3000, adding significant work for organisations transitioning from ISAE 3410 for SB 253 compliance.

- [5]LRQA Independent Assurance Statement – P&G

Example ISAE 3410 limited assurance engagement letter noting that limited assurance procedures focus on aggregated data rather than physically checking source data at sites.

- [7]ASAE 3410 Assurance Engagements on Greenhouse Gas Statements – AUASB

Australian equivalent of ISAE 3410, confirming that the standard is operative until December 14, 2026 and noting the shift in evidence sufficiency requirements between sampling-based and population-based assurance.

Related Content

- [4]The assurance-level problem in EU CSRD limited-to-reasonable transitions

Analysis of the structural cost difference between limited and reasonable assurance procedures, and why most first-wave CSRD reporters lack the controls to support reasonable assurance.

- [6]Book a CBAM readiness call

Start with a readiness call to map your current ISAE 3410 evidence base and evaluate whether you need to build population-level evidence infrastructure before the December 2026 ISSA 5000 effective date.

- [8]Audit-ready exports in Emission3

Platform feature overview showing how Emission3 produces line-item evidence packs with procurement ledger reconciliations and calculation lineage traces for auditors and assurance providers.