The methodology documentation gap in Scope 3 Category 1 primary data collection

The methodology documentation gap in Scope 3 Category 1 primary data collection

Here's the issue: Primary data collection costs €15,000–€40,000 per supplier engagement cycle for a mid-market manufacturer, yet most procurement teams reach the limited assurance stage with no reproducible methodology trail. The supplier sends an emissions number, the sustainability team enters it into the inventory, and the engagement appears complete.

However, primary data collection consists of two things: the supplier's reported emissions number and the methodology lineage that makes that number auditable—the allocation method, the boundary definition, the calculation standard applied, and the evidence trail linking the number back to source documentation.

The emissions number on its own has no value in a limited assurance engagement. The methodology lineage is what the auditor is actually verifying. A supplier can report 1.8 tCO₂e per unit, but without documentation showing whether that figure uses market-based or location-based electricity accounting, whether it includes only Scope 1 and 2 or extends into upstream Scope 3, and whether the boundary covers the full production process or only final assembly, the number cannot be assured. The auditor's work product is not a validation of the magnitude—it is a validation of the methodology's consistency with the GHG Protocol and the filer's stated approach.

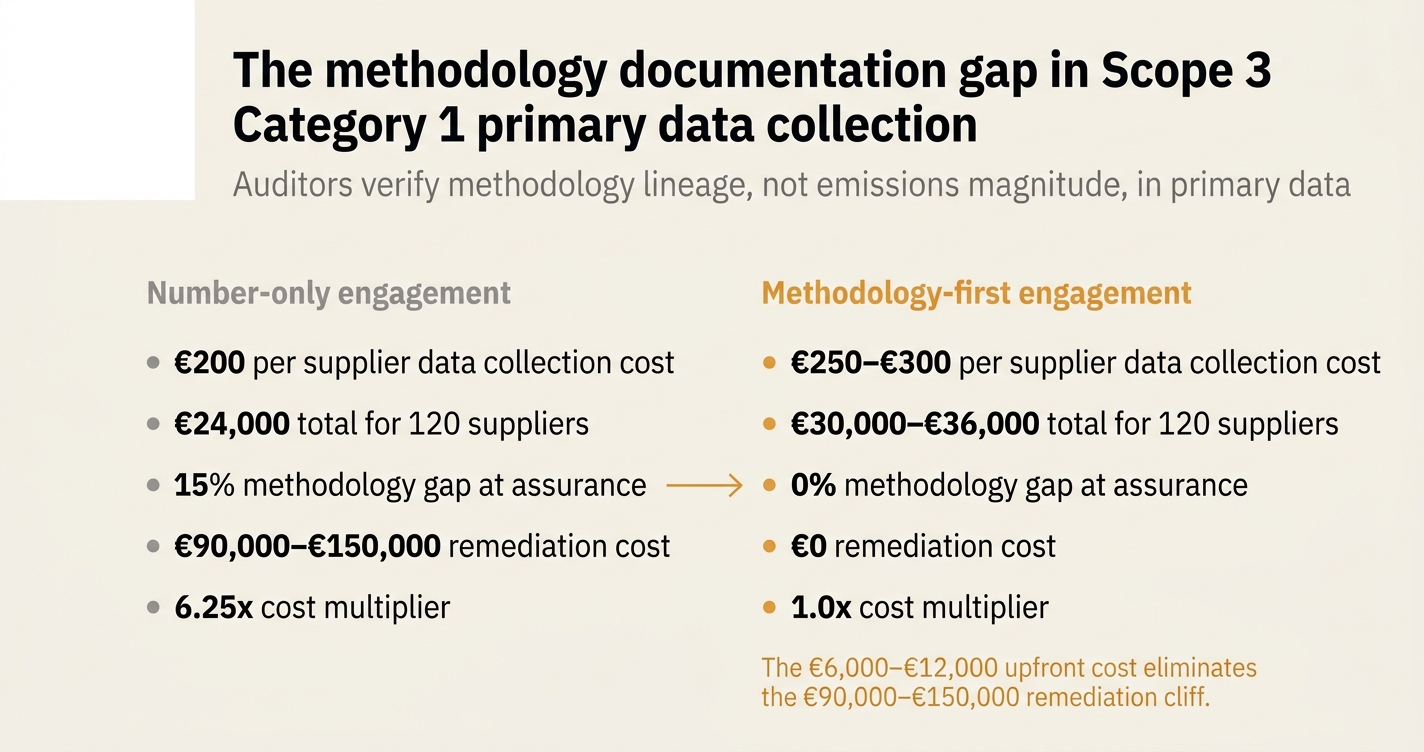

While supplier engagement platforms have become cheaper, methodology documentation has become more expensive. If a procurement team collects primary data from 120 suppliers at €200 per engagement but lacks methodology lineage for even 15% of those suppliers, the cost of remediation at the assurance stage—re-engaging suppliers, reconstructing allocation decisions, validating boundaries retrospectively—can reach €90,000–€150,000, outpacing the original data collection budget by a factor of three.

How do you solve this? I think the answer lies in treating methodology documentation as a first-class artifact of the supplier engagement process, not a post-hoc assurance exercise. The operators we work with have shifted from "collect the number" workflows to "collect the number plus the methodology justification" workflows, embedding allocation questions, boundary confirmations, and calculation standard declarations directly into the supplier data request template. For now, this approach costs slightly more per engagement—perhaps €250–€300 instead of €200—but it eliminates the remediation cliff at assurance.

The shape of the argument, visualised below.

The structural problem: primary data without methodology

Scope 3 Category 1 (Purchased Goods and Services) is the largest emissions category for most manufacturers and retailers, often accounting for 60–80% of the total inventory [1]. The GHG Protocol Corporate Value Chain (Scope 3) Standard encourages primary data collection—requesting emissions data directly from suppliers—as the preferred method over spend-based estimation [1]. Yet the standard also requires "sufficient detail to enable proper categorization and calculation" and "documentation of data sources and calculation methods" [1].

Most procurement teams interpret this as a requirement to collect emissions numbers, not to collect methodology lineage. A typical supplier data request asks for:

- Total emissions per product unit or per invoice line

- Scope coverage (Scope 1+2, or Scope 1+2+3)

- Reporting period

What it rarely asks for:

- The allocation method used (physical, economic, or other)

- The boundary definition (cradle-to-gate, gate-to-gate, or cradle-to-grave)

- The electricity accounting approach (market-based or location-based)

- The calculation standard applied (GHG Protocol, ISO 14064, PAS 2050, or proprietary)

- The evidence artifacts supporting the calculation (invoices, utility bills, production logs)

The result is a primary data set that looks complete on the surface—every supplier has provided a number—but collapses under assurance scrutiny. The auditor cannot verify what was included, what was excluded, or whether the methodology aligns with the filer's stated approach.

| Procurement team's view | Auditor's view |

|---|---|

| "We collected primary data from 120 suppliers." | "We cannot verify 18 of these suppliers because the allocation method is undocumented." |

| "Supplier reported 1.8 tCO₂e per unit." | "Does this include upstream transport? Packaging? Raw material extraction?" |

| "We have better data quality than spend-based estimation." | "We have no basis to confirm that without methodology lineage." |

| "Primary data collection cost €24,000." | "Remediation will cost €54,000 to re-engage and document." |

The three documentation gaps that break assurance

Gap 1: Allocation method ambiguity

When a supplier produces multiple products, the emissions from shared processes (e.g., a steel mill producing both structural steel and rebar) must be allocated across product lines. The GHG Protocol permits physical allocation (by mass, volume, or energy content) or economic allocation (by revenue or market value) [1]. The choice matters: physical allocation typically assigns more emissions to low-value, high-mass products, while economic allocation assigns more to high-value, low-mass products.

If the supplier does not document which method was used, the auditor cannot verify consistency. A filer using economic allocation for its own Scope 1 and 2 inventory but receiving physically allocated Scope 3 data from suppliers creates a methodological inconsistency that limited assurance will flag.

Gap 2: Boundary definition mismatch

A "cradle-to-gate" boundary includes all upstream emissions up to the supplier's gate (raw materials, transport, energy). A "gate-to-gate" boundary includes only the supplier's direct operations (Scope 1 and 2). A "cradle-to-grave" boundary extends through product use and end-of-life.

If the filer's inventory methodology specifies that Category 1 should use cradle-to-gate boundaries to avoid double-counting with Category 4 (Upstream Transport) and Category 5 (Waste), but the supplier reports a gate-to-gate figure, the reported emissions will understate the true footprint. Without boundary documentation, the auditor cannot identify the gap.

Gap 3: Evidence trail absence

Primary data is only "primary" if it is grounded in the supplier's own source documentation—invoices, utility bills, production logs, purchase orders. If the supplier calculates emissions using a secondary source (an industry average factor, a database value, or a consultancy's model), the data is effectively a form of spend-based estimation, not primary data [1].

The auditor will request evidence that the supplier's reported number is derived from actual operational data, not modeled. If the procurement team did not collect evidence artifacts during the engagement, the supplier must be re-engaged at assurance time, often 12–18 months after the original request, when personnel have changed and records are harder to retrieve.

"The most common finding in our first round of Scope 3 limited assurance engagements was insufficient documentation of supplier-specific allocation methods. Companies had the emissions numbers but could not demonstrate how those numbers were derived." — KPMG guidance on CSRD assurance readiness [2]

The remediation cost curve

The cost of fixing methodology gaps scales non-linearly with the number of affected suppliers and the time elapsed since the original data request.

| Remediation scenario | Typical cost per supplier | Total cost (120 suppliers, 15% affected) |

|---|---|---|

| Re-engagement within 3 months of original request | €500–€800 | €9,000–€14,400 |

| Re-engagement after 12 months, personnel turnover | €2,500–€4,000 | €45,000–€72,000 |

| Re-engagement after 18 months, records archived | €5,000–€8,000 | €90,000–€144,000 |

| Supplier non-responsive, substitute with default factors | €0 (data cost) + audit qualification risk | Unquantifiable reputational cost |

The last scenario—substituting primary data with default factors at the assurance stage—undermines the entire rationale for primary data collection. The filer has spent €24,000 to collect supplier-specific data, only to revert to spend-based estimation for 15% of the inventory because the methodology trail is missing.

The workflow shift: methodology-first engagement

The alternative is to embed methodology documentation into the supplier data request from the outset. This requires expanding the data request template to capture:

- Allocation method declaration: "For multi-product facilities, which allocation method did you use? (Physical by mass / Physical by energy / Economic by revenue / Other—please specify.)"

- Boundary definition confirmation: "Does this figure include only your direct operations (Scope 1+2), or does it also include upstream emissions from your suppliers (Scope 3 upstream)?"

- Electricity accounting approach: "For Scope 2 emissions, did you use market-based accounting (reflecting your renewable energy purchases) or location-based accounting (using the grid average)?"

- Calculation standard reference: "Which standard or framework did you use to calculate these emissions? (GHG Protocol / ISO 14064 / PAS 2050 / Proprietary method—please attach documentation.)"

- Evidence artifact request: "Please attach a sample invoice, utility bill, or production log that demonstrates how this figure was calculated."

This approach increases the per-supplier engagement cost by €50–€100 (from €200 to €250–€300), but it eliminates the remediation cliff. The total cost of a 120-supplier engagement rises from €24,000 to €30,000–€36,000, but the assurance-stage remediation cost drops from €45,000–€144,000 to effectively zero.

The tier-2 visibility problem

A second challenge emerges when the reporting company's suppliers are themselves aggregating data from their own suppliers (tier-2). A steel fabricator's reported emissions for "purchased steel" may already embed upstream emissions from the steel mill, which in turn sourced iron ore and coke from tier-3 suppliers. If the fabricator does not document how much of its reported figure is attributable to tier-2 emissions, the filer risks double-counting when it separately calculates Category 1 emissions for steel purchases and Category 4 emissions for inbound logistics.

The GHG Protocol permits suppliers to report either:

- Scope 1+2 only (gate-to-gate), in which case the filer must separately account for upstream transport and raw materials in Categories 4 and 5.

- Scope 1+2+3 upstream (cradle-to-gate), in which case the filer should not separately account for the supplier's upstream in other categories.

Without clear documentation of the supplier's scope boundary, the filer cannot determine which approach was used, and the auditor cannot verify that double-counting has been avoided. This is the tier-2 visibility gap: the filer knows the supplier's total emissions but does not know how much of that total is attributable to the supplier's own operations versus the supplier's supply chain [3].

The safe harbor for incomplete methodology documentation

Under California SB 253, the executive officer statement that accompanies the annual emissions disclosure carries personal liability for material misstatements [4]. The regulation does not currently define a safe harbor for good-faith errors in Scope 3 methodology, but the legislative history suggests that the standard is "reasonable assurance that the disclosure is materially accurate" [4]. This implies that a filer who documents the methodology gaps—"We collected primary data from 120 suppliers; 18 suppliers did not provide allocation method documentation, so we applied our internal allocation assumptions based on [stated rationale]"—has a stronger defense than a filer who presents incomplete data as complete.

Under the EU CSRD, limited assurance does not require the auditor to verify every supplier's methodology, only to confirm that the filer's overall approach is consistent and that any material gaps are disclosed [2]. EFRAG's December 2025 revised draft ESRS emphasizes "fair presentation and proportionality," which means the filer must disclose estimation uncertainty rather than concealing it [5]. A filer who documents "15% of Category 1 primary data lacks supplier-specific allocation documentation; we have applied economic allocation as a default based on [rationale]" is more likely to receive limited assurance than a filer who claims complete primary data coverage without supporting evidence.

How Emission3 fits

Emission3 treats methodology documentation as a line-item artifact, not a summary field. When a procurement team uploads a supplier data file (CSV, Excel, or PDF invoice), the system:

- Extracts the emissions number and the associated product or invoice line.

- Prompts for methodology metadata: allocation method, boundary definition, electricity accounting approach, calculation standard.

- Links the emissions number to the source document (invoice, utility bill, or supplier report) as evidence.

- Generates a methodology lineage report for each supplier, showing the full chain from source document to aggregated inventory.

At the assurance stage, the auditor receives an evidence pack per supplier: the original data request, the supplier's response, the methodology metadata, and the source documents. The system's deterministic calculation engine ensures that every number in the final inventory is reproducible from the evidence pack, with no manual spreadsheet steps that could introduce error or ambiguity.

For tier-2 visibility, Emission3 flags supplier-reported figures that include Scope 3 upstream and prompts the user to confirm whether those upstream emissions have been excluded from other categories (e.g., Category 4 or 5). If the user cannot confirm, the system generates a disclosure note: "Supplier X reported cradle-to-gate emissions; we have not separately calculated upstream transport for this supplier to avoid double-counting." This disclosure satisfies the CSRD's fair presentation requirement and provides the auditor with a clear rationale for the methodological choice.

The checklist: methodology documentation for primary data

Use this checklist to ensure that your primary data collection workflow produces assurance-ready methodology lineage, not just emissions numbers.

Before supplier engagement

✅ 1. Define the inventory methodology in writing.

Owner: Sustainability manager

Done when: A one-page methodology document specifies allocation method (physical or economic), boundary definition (gate-to-gate or cradle-to-gate), electricity accounting (market-based or location-based), and calculation standard (GHG Protocol, ISO 14064, or other).

Evidence artifact: Methodology document, dated and version-controlled.

✅ 2. Design the supplier data request template to capture methodology metadata.

Owner: Procurement lead

Done when: The template includes fields for allocation method, boundary definition, electricity accounting, calculation standard, and evidence artifact upload.

Evidence artifact: Data request template (Word, PDF, or online form).

✅ 3. Align the data request with the inventory methodology.

Owner: Sustainability manager + Procurement lead

Done when: The requested boundary (e.g., cradle-to-gate) matches the inventory methodology, and the template includes a disclosure clause: "If you cannot provide cradle-to-gate data, please provide gate-to-gate data and indicate this in your response."

Evidence artifact: Alignment memo or email confirming template review.

During supplier engagement

✅ 4. Send the data request with a methodology guidance document.

Owner: Procurement lead

Done when: The email or portal link includes a one-page PDF explaining why methodology documentation is required ("to meet assurance requirements") and what each field means.

Evidence artifact: Sent email or portal notification log.

✅ 5. Track responses by completeness, not just by submission.

Owner: Procurement lead

Done when: A response tracker flags any submission missing allocation method, boundary definition, or evidence artifact as "incomplete" and triggers a follow-up.

Evidence artifact: Response tracker spreadsheet with completeness status per supplier.

✅ 6. Conduct follow-up for incomplete responses within 2 weeks.

Owner: Procurement lead

Done when: Any supplier who submitted an emissions number without methodology metadata receives a follow-up email or call within 14 days, while records are still accessible.

Evidence artifact: Follow-up email log or call notes.

✅ 7. Collect evidence artifacts (invoices, utility bills, production logs) per supplier.

Owner: Procurement lead

Done when: At least one source document per supplier is uploaded to the evidence repository, linked to the supplier's reported emissions number.

Evidence artifact: Evidence repository with file count per supplier.

After data collection

✅ 8. Validate that supplier-reported boundaries match the inventory methodology.

Owner: Sustainability manager

Done when: Any supplier who reported gate-to-gate data (Scope 1+2 only) is flagged, and a decision is documented: either (a) separately calculate upstream emissions for that supplier in Category 4/5, or (b) accept the gap and disclose it.

Evidence artifact: Boundary validation log with flagged suppliers and resolution notes.

✅ 9. Document any methodology deviations or estimation fallbacks.

Owner: Sustainability manager

Done when: A disclosure note lists any suppliers for whom primary data was incomplete, the fallback method used (e.g., "applied economic allocation based on revenue proxy"), and the rationale.

Evidence artifact: Disclosure note, included in the inventory report.

✅ 10. Generate a methodology lineage report per supplier.

Owner: Sustainability manager

Done when: A report shows the full chain: data request → supplier response → evidence artifact → calculation → aggregated inventory line.

Evidence artifact: Methodology lineage report (PDF or spreadsheet).

✅ 11. Prepare an evidence pack for the auditor.

Owner: Sustainability manager

Done when: A single ZIP file or folder per supplier contains: (a) the data request, (b) the supplier's response, (c) methodology metadata, (d) source documents, (e) the methodology lineage report.

Evidence artifact: Evidence pack, organized by supplier name or ID.

✅ 12. Conduct an internal pre-assurance review.

Owner: Internal audit or finance team

Done when: A sample of 10% of suppliers is reviewed for completeness of methodology documentation, and any gaps are remediated before the external assurance engagement begins.

Evidence artifact: Pre-assurance review memo with findings and remediation actions.

During assurance

✅ 13. Provide the auditor with the evidence pack repository structure upfront.

Owner: Sustainability manager

Done when: The auditor receives a folder map or index showing which evidence artifacts correspond to which suppliers and inventory lines.

Evidence artifact: Evidence pack index (spreadsheet or README file).

✅ 14. Respond to auditor queries within 48 hours with traceable evidence.

Owner: Sustainability manager

Done when: Any auditor question about allocation method, boundary, or source document is answered with a direct link to the relevant file in the evidence pack.

Evidence artifact: Query response log with file references.

✅ 15. Update the methodology document based on assurance findings.

Owner: Sustainability manager

Done when: Any methodology clarification or correction identified during assurance is incorporated into the methodology document and version-controlled for the next reporting cycle.

Evidence artifact: Updated methodology document, dated and marked as post-assurance revision.

The reasonable assurance transition

Under the EU CSRD, limited assurance is required for the first reporting cycles (FY2024, FY2025, FY2026 depending on the wave), with a transition to reasonable assurance planned for 2028, subject to feasibility assessment [2]. The Omnibus I amendments have not changed the assurance trajectory, only the timing of first reporting [6].

Reasonable assurance requires the auditor to perform "more procedures that resemble a financial statement audit," including "a detailed evaluation of internal controls and substantive testing" [7]. For Scope 3 Category 1, this means the auditor will not only verify that the filer has methodology documentation—they will also test whether that documentation is consistently applied across the full population of suppliers, not just a sample.

A procurement team that collected methodology documentation for 85% of suppliers during limited assurance but has no controls to ensure 100% coverage in future cycles will face a significant remediation burden when transitioning to reasonable assurance. The cost of retrofitting controls—standardizing the data request template, automating completeness checks, embedding methodology prompts into procurement systems—can reach €100,000–€200,000 for a global manufacturer with 500+ suppliers.

The alternative is to build the controls during the limited assurance phase. This means treating the checklist above not as a one-time assurance exercise, but as the operational standard for every supplier engagement going forward. By 2028, when reasonable assurance begins, the methodology documentation workflow is already embedded in procurement operations, and the transition cost is minimal.

Next steps: CBAM readiness and primary data

For non-EU exporters, the CBAM (Carbon Border Adjustment Mechanism) imposes a parallel requirement for primary data collection: importers will pay a carbon price on the embedded emissions of imported goods, and the default emissions values are significantly higher than most installations' actual emissions [8]. To avoid the default penalty, exporters must provide installation-specific emissions data, verified by an accredited verifier, with the same methodology lineage that auditors expect in Scope 3 reporting: allocation method, boundary definition, and evidence trail.

If your organization is both a Scope 3 reporter (collecting primary data from suppliers) and a potential CBAM-covered exporter (providing primary data to EU importers), the methodology documentation workflow described above applies to both directions of the supply chain. A consistent approach reduces duplication: the same evidence pack that satisfies your Scope 3 auditor can satisfy your customer's CBAM verifier.

Ready to close the methodology documentation gap? Book a CBAM readiness call with the Emission3 team. We'll map your supplier population, identify the methodology gaps that will break assurance, and show you how Emission3 turns primary data collection into a deterministic, evidence-backed workflow that auditors can replay [9].

References & Sources

External Sources

- [1]GHG Protocol Corporate Value Chain (Scope 3) Standard

The foundational standard for Scope 3 emissions accounting, including Category 1 (Purchased Goods and Services) methodology requirements and documentation guidance.

- [2]Hot Topic: Sustainability in the EU - KPMG International

KPMG guidance on CSRD assurance requirements, including the transition from limited to reasonable assurance and common audit findings in Scope 3 methodology documentation.

- [4]The spreadsheet-to-assurance transition problem in California SB 253 first-year filings

Analysis of California SB 253 executive officer statement liability and the safe harbor implications for Scope 3 methodology gaps.

- [5]CSRD reporting post-Omnibus I: what directors need to know in 2026

Commonwealth Climate and Law Initiative summary of EFRAG's December 2025 revised draft ESRS, emphasizing fair presentation, proportionality, and disclosure of estimation uncertainty.

- [6]Preparing for What's Next: Navigating CSRD Amid Proposed EU Omnibus Changes

Embark analysis of the Omnibus I 'stop-the-clock' directive and its impact on CSRD reporting timelines, with no changes to the assurance trajectory.

- [7]What is Reasonable and Limited Assurance in CSRD?

EcoSkills Academy explainer on the procedural differences between limited and reasonable assurance, including the control testing requirements under reasonable assurance.

Related Content

- [3]The tier-2 visibility gap in Scope 3 Category 1 primary data collection

Explores the challenge of attributing supplier-reported emissions to tier-1 versus tier-2 operations, and the double-counting risk when boundaries are undocumented.

- [8]The 2026 CBAM verification timeline problem for non-EU exporters

Examines the CBAM default value penalty for exporters who cannot provide installation-specific emissions data with verifier-ready methodology documentation.

- [9]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, identify methodology gaps, and scope the implementation, no anonymous self-serve onboarding.