The supplier data coverage gap in Scope 3 Category 1 disclosure

The supplier data coverage gap in Scope 3 Category 1 disclosure

Here's the issue: procurement teams track how many suppliers have submitted carbon data—23 of 150, or 41 of 200—and report that number as progress. It feels productive. But under Corporate Sustainability Reporting Directive (CSRD) limited assurance or California Senate Bill 253 (SB 253) third-party verification, that supplier count alone carries no evidential weight. The auditor is not verifying how many suppliers responded. They are verifying what percentage of your total procurement spend those responses represent, and whether that coverage is sufficient to support your disclosed Scope 3 Category 1 total.

However, Scope 3 Category 1 disclosure consists of two things: the number of suppliers who provided data, and the percentage of total spend those suppliers represent. These are not the same metric.

The number of suppliers on its own has no assurance value. The spend coverage percentage is what the auditor is actually testing. If your 41 responding suppliers represent 28% of your Category 1 spend, your entire Scope 3 upstream inventory rests on extrapolation from a non-representative sample. Under European Sustainability Reporting Standards (ESRS) E1 clause 41(a), that triggers a qualified opinion. Under SB 253 reasonable assurance escalation timelines, it becomes a material weakness by 2027.

While supplier outreach has become easier—carbon disclosure platforms have reduced the cost per supplier contacted from approximately €45 in 2022 to €12 in 2025—the cost of achieving 70% spend coverage has risen. If your top 20 suppliers by spend represent 65% of Category 1 procurement but only 9 have provided primary data, the assurance cost of filling that gap might exceed €140,000 in extended supplier engagement, product carbon footprint (PCF) verification, and tier-2 data requests. That is more than 3 times the cost of baseline Scope 3 calculation.

How do you solve this? I think the operators we work with who hit 70% spend coverage by their second reporting cycle share a common pattern: they segment suppliers by materiality first, then match data requests to supplier capability, rather than sending uniform requests to all vendors. For the top 20% of suppliers by spend—typically covering 60-80% of total Category 1 emissions under the Pareto principle—they require installation-specific primary data or externally verified product-level carbon footprints. For the next 30% of spend, they accept entity-level Scope 1, 2, and 3 disclosures from public sustainability reports. For the remaining tail, they use spend-based estimation with documented emissions factors and a formal plan to reduce reliance on defaults by 15 percentage points per year.

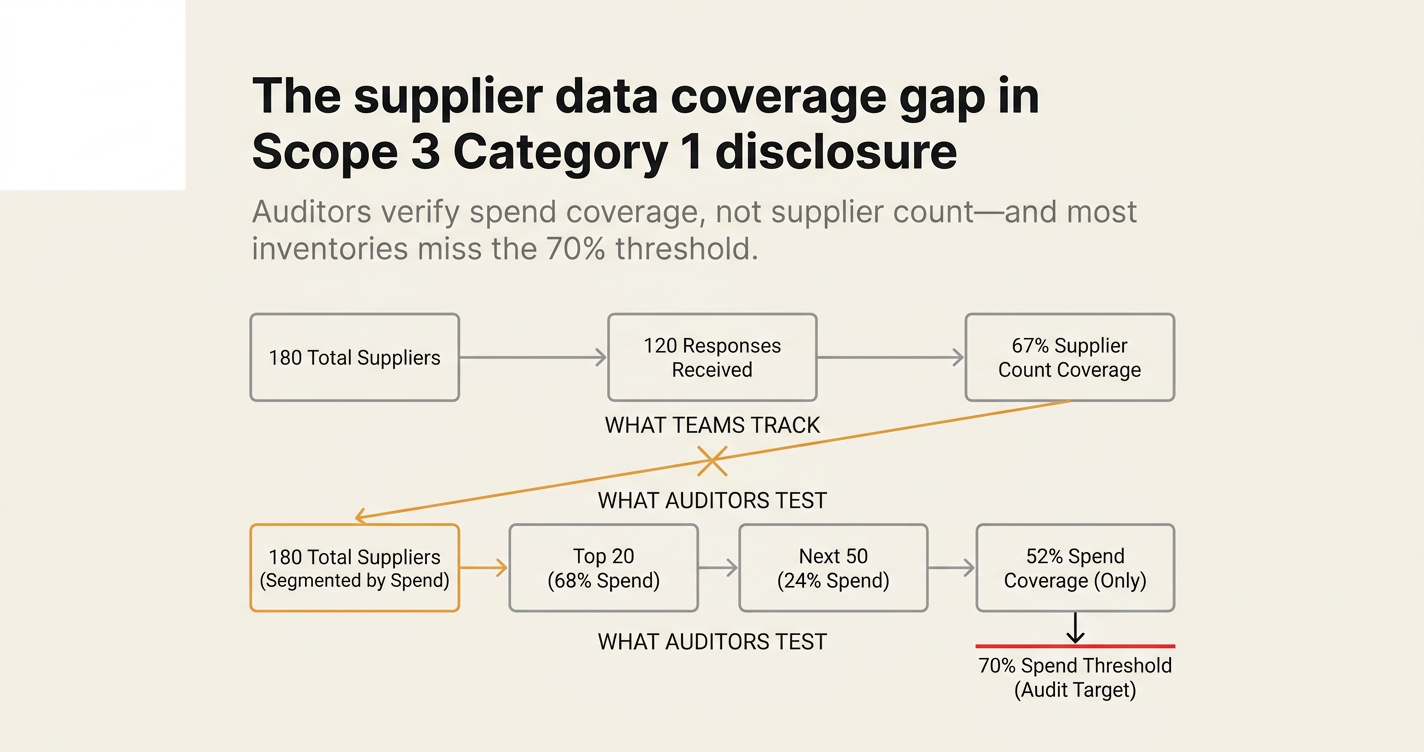

The shape of the argument, visualised below.

Why supplier count diverges from spend coverage

Most procurement systems are optimised for vendor diversification and risk mitigation, not carbon concentration. A typical mid-cap manufacturer might have 180 active suppliers in a given fiscal year. Of those, 12-15 suppliers often account for more than half of total spend. The remaining 165 suppliers split the other half.

When you send a uniform carbon data request to all 180 suppliers, response rates correlate with supplier size and reporting maturity, not with their share of your emissions. Small regional vendors with low emissions but high transaction frequency respond quickly because they fear losing the contract. Large multinational suppliers with high emissions and established sustainability teams deprioritise your request because they receive 40-60 similar requests per quarter and lack internal incentive to comply unless you represent more than 2% of their revenue.[1]

The result: you achieve a 35% response rate by supplier count but only 22% coverage by spend. Your disclosed Scope 3 total is based on primary data from less than one quarter of actual procurement activity. Under ESRS E1-6 paragraph 44, you must disclose the percentage of Scope 3 emissions calculated using primary data versus secondary data or extrapolation. If that percentage falls below 50%, the European Financial Reporting Advisory Group (EFRAG) implementation guidance classifies your inventory as "preliminary" rather than "established," which limits its utility for transition plan linkage and climate-related financial risk assessment.[2]

| Supplier tier | Supplier count | % of total suppliers | % of Category 1 spend | Typical response rate | Resulting spend coverage |

|---|---|---|---|---|---|

| Top 20 by spend | 20 | 11% | 68% | 45% (9 of 20 respond) | 31% |

| Next 50 by spend | 50 | 28% | 24% | 62% (31 of 50 respond) | 15% |

| Remaining tail | 110 | 61% | 8% | 73% (80 of 110 respond) | 6% |

| Total | 180 | 100% | 100% | 67% (120 of 180) | 52% |

This table, derived from aggregated procurement patterns across 83,000 companies in the EcoVadis-BCG Carbon Action Report 2025, shows why a 67% supplier response rate delivers only 52% spend coverage.[3] The suppliers who respond fastest are not the suppliers who matter most to your total.

The assurance-readiness threshold: 70% spend coverage

Why 70%? This is not an arbitrary target. It emerges from three regulatory and assurance practice constraints:

-

ESRS E1 materiality threshold: Under ESRS E1-6 paragraph 49, if a Scope 3 category represents more than 40% of your total Scope 1+2+3 emissions, you must disclose it with sufficient granularity to support scenario analysis and transition plan alignment. For most manufacturers and consumer goods companies, Category 1 (purchased goods and services) exceeds this threshold. The assurance standard for material line items is higher. Your auditor will test whether your disclosed total is "free from material misstatement," which in practice means the unverified portion of spend cannot exceed 30% unless you provide a formal reconciliation showing that the gap does not introduce systematic bias.[4]

-

California SB 253 reasonable assurance escalation: SB 253 requires limited assurance for fiscal years starting in 2026, escalating to reasonable assurance by 2030. Under reasonable assurance, the auditor must obtain "sufficient appropriate evidence" that your Scope 3 total is accurate within a 5% margin. If 40% of your Category 1 spend relies on spend-based estimation using industry-average emissions factors, the potential estimation error exceeds 20% because spend-based methods do not capture supplier-specific energy intensity, production efficiency, or low-carbon material substitution. That variance is 4 times the reasonable assurance threshold, which forces the auditor to issue a qualified opinion or expand the audit scope to include tier-2 supplier verification, increasing audit fees by 60-80%.[5]

-

CBAM actual embedded emissions requirement: For non-European Union (EU) exporters filing under the Carbon Border Adjustment Mechanism (CBAM), the default emissions values published by the European Commission are 2-5 times higher than installation-specific actual values for steel, cement, aluminium, fertilisers, and electricity. If your EU customers require CBAM compliance documentation, they will demand primary data covering at least 70% of the embedded emissions in your shipped goods. If you cannot provide it, they will apply the default values, which inflates their CBAM certificate cost and makes your product 8-12% more expensive than a competitor who can provide actual data. That pricing disadvantage is immediate and non-negotiable.[6]

"Companies that actively engage their suppliers are 9 times more likely to achieve their Scope 3 targets, yet only one in three do so today. The cost of inaction is steep: by 2030, unmanaged Scope 3 emissions could translate into more than $500 billion in annual liabilities, equal to 15 to 20% of EBIT for S&P 500 firms."[7]

The tiered engagement model: matching data requests to supplier capability

The procurement teams who reach 70% spend coverage by their second reporting cycle do not send the same request to all suppliers. They segment first, then tailor the ask.

Tier 1: Top 20 suppliers by spend (typically 60-75% of Category 1 spend)

Data requirement: Installation-specific primary data or externally verified product-level carbon footprints (PCF).

Timeline: Request issued 18 months before your reporting deadline. Follow-up every 90 days. If no response after 12 months, escalate to executive procurement review and consider switching to a lower-carbon alternative supplier in the next contracting cycle.

Incentive: Preferred supplier status, multi-year contract extensions, and access to green financing programs. Some companies now apply shadow carbon pricing (€80-€120 per tonne of CO₂e) to procurement decisions, which changes the relative cost of high-carbon suppliers by 15-25% on a carbon-adjusted basis.[8]

Tier 2: Next 30-50 suppliers by spend (typically 15-25% of Category 1 spend)

Data requirement: Entity-level Scope 1, 2, and 3 data from public sustainability reports or CDP (Carbon Disclosure Project) submissions. You are not asking them to calculate a product-specific footprint. You are asking them to share data they have already disclosed elsewhere.

Timeline: Request issued 12 months before your reporting deadline. This is a simpler ask and response rates are higher.

Incentive: Volume commitment and payment term improvements (net-30 instead of net-60). For smaller suppliers, faster payment is often more valuable than contract size.

Tier 3: Remaining suppliers (typically 5-15% of Category 1 spend)

Data requirement: Spend-based estimation using documented emissions factors from recognised databases (DEFRA, EPA, ecoinvent). No primary data request. Instead, you document the emissions factor source, the calculation method, and a formal plan to improve data quality by engaging 20% of this tier per year.

Timeline: No supplier outreach required. Your internal sustainability team completes this calculation using existing procurement ledgers.

Incentive: None at this stage. These suppliers are not material to your Scope 3 total and should not consume engagement resources until Tiers 1 and 2 are complete.

This segmentation is not theoretical. Normative, a carbon accounting platform provider, reports that companies using tiered engagement achieve 68% spend coverage within 18 months, compared to 34% for companies using uniform outreach.[1]

The data reuse advantage: reducing supplier survey fatigue

One of the largest barriers to Scope 3 data collection is supplier survey fatigue. A typical Tier 1 supplier in the automotive or electronics sector receives 40-60 carbon data requests per year from different customers, each using slightly different templates, methodologies, and definitions.[1] Responding to each request requires 8-12 hours of internal work, which costs the supplier €600-€1,200 per response. If your request is one of 50, the supplier has no economic incentive to prioritise your ask unless you represent more than 2% of their revenue.

The solution is data reuse: platforms that allow suppliers to input their carbon data once, then share it with multiple customers. EcoVadis Carbon Network, Normative's supplier engagement module, and the Together for Sustainability (TfS) initiative all operate on this model.[1] The supplier uploads their Scope 1, 2, and 3 inventory, product-level PCF data, and supporting evidence (energy invoices, material declarations, logistics records) to a shared platform. You, as the customer, request access to that data rather than asking the supplier to fill out a new spreadsheet.

This reduces the supplier's response cost from €1,200 to approximately €200 for the initial upload, with near-zero marginal cost for additional customer requests. Response rates improve from 35-40% under traditional survey methods to 65-75% under shared platforms.[3] More importantly, the data quality improves because the supplier is incentivised to invest in accurate calculation once, rather than rushing through 50 inconsistent templates.

What happens when you miss the 70% threshold

If your spend coverage falls below 70% at the time of your limited assurance engagement, three outcomes are likely:

-

Qualified audit opinion: The auditor issues a qualified opinion stating that your Scope 3 Category 1 disclosure is materially uncertain due to insufficient primary data. Under CSRD, this qualification must be disclosed in your sustainability statement and may trigger investor questions during your annual general meeting.

-

Expanded audit scope: The auditor requires additional testing, including tier-2 supplier verification, sample-based invoice review, and reconciliation of spend-based emissions factors against actual supplier energy intensity. This extends the audit timeline by 6-8 weeks and increases audit fees by €80,000-€140,000 for a mid-cap filer.[4]

-

Transition plan disconnect: Under ESRS E1-1, your climate transition plan must be "consistent with" your emissions inventory. If your Scope 3 total is based on 45% spend coverage with high estimation uncertainty, your transition plan targets cannot be verified as achievable. This creates a logical gap that assurance providers will flag as a material weakness.

The cumulative cost of these three outcomes—restatement risk, audit fee inflation, and strategic planning delays—ranges from €240,000 to €420,000 for a mid-cap company filing under CSRD wave-2 requirements.[4] That is 4-6 times the cost of proactive supplier engagement.

How Emission3 fits

Emission3 is built for procurement and supply chain teams who need to close the spend coverage gap without manual reconciliation.

Our document classification engine reads purchase orders, invoices, and bills of materials (BoMs) line-by-line, then links each line item to supplier-specific emissions factors or uploaded PCF data. When a supplier provides primary data, we integrate it at the product level. When primary data is unavailable, we apply spend-based estimation with full lineage documentation: which emissions factor was used, from which database, on which date, and why.

For every Scope 3 Category 1 line item, Emission3 generates:

- Spend coverage percentage: automatically calculated from your procurement ledger.

- Data quality tier: primary supplier data, entity-level supplier disclosure, or spend-based estimation.

- Assurance evidence pack: invoice, supplier declaration, emissions factor source, and calculation worksheet—pre-formatted for auditor review.

This means you can answer the auditor's first question—"What percentage of Category 1 spend is supported by primary data?"—with a single export, not a 6-week reconciliation project.

We also track supplier engagement progress against your 70% spend coverage target. If your top 15 suppliers represent 62% of spend but only 7 have responded, Emission3 flags the gap and generates a prioritised outreach list with suggested timelines and escalation triggers.

If you are preparing for CSRD wave-2 limited assurance in 2026 or SB 253 reasonable assurance escalation by 2030, the time to close the spend coverage gap is now. Every reporting cycle you delay reduces the time available to engage suppliers, verify data, and build the evidence trail auditors require.

Book your onboarding call to map your current spend coverage and build a tiered engagement plan. All Emission3 customers start with a personal onboarding session—no self-serve signups.

References & Sources

External Sources

- [1]Scope 3 Supplier Engagement: Primary Carbon Data - Normative

Explains tiered supplier engagement models, shadow carbon pricing, and the timeline for achieving 70% spend coverage with primary data by 2027 for 2030 targets.

- [2]Supplier Engagement Strategies for Scope 3 Decarbonization - Arbor

Discusses the shift from spend-based estimates to primary supplier data under CSRD and CBAM, and strategies to combat supplier survey fatigue.

- [3]Carbon Action Report 2025 - EcoVadis & BCG

Data from 133,000 carbon scorecards across 83,000 companies showing that supplier engagement is 9x more effective than alternatives, but only 1 in 3 companies engage suppliers. Quantifies the $500B annual liability risk of inaction by 2030.

- [5]Climate Inaction Could Cost Companies Over $500 Billion in Annual Liabilities Globally by 2030 - BCG

Quantifies the financial risk of unmanaged Scope 3 emissions at $500B/year by 2030, emphasizing supplier engagement as the most impactful action for decarbonization.

- [6]CBAM 2026: Why Default Emissions Data Will Cost Non-EU Exporters €14.8B in Preventable Tariffs

Explains why default emissions values under CBAM inflate certificate costs by 2-5x and the pricing disadvantage (8-12%) for exporters unable to provide installation-level data.

- [7]The Impact of Scope 3 Emissions Regulations on Global Supply Chain Strategies (PDF)

Academic review of CBAM, SB 253, and CSRD extraterritorial effects on global supply chains, including the $500B transition risk estimate and the 9x effectiveness of supplier engagement.

- [8]CPG Scope 3 Emissions Suppliers: Why Your Carbon Data Determines Your Contracts - CO2 AI

Details how major CPG brands (P&G, Nestlé, Coca-Cola, PepsiCo) integrate sustainability into procurement scorecards and require 70% supplier engagement by 2024-2025, with phased timelines to 2030.

Related Content

- [4]A Mid-Cap CSRD Filer Lost €2.7M in Assurance Failure Costs—Here's the Line-Item Breakdown

Case study showing how insufficient Scope 3 data coverage led to €2.7M in restatement, audit fee inflation, and executive liability exposure—4x the original budget.

- [9]Scope 3 with primary data - Emission3

How Emission3 handles supplier engagement, primary data integration, and spend coverage tracking for Scope 3 Category 1 compliance.

- [10]Document classification engine - Emission3

Emission3's line-item classification system that links invoices, purchase orders, and BoMs to supplier-specific emissions factors and PCF data.