The Scope 3 jargon barrier in 2026 SB 253 and CBAM audit engagements

The Scope 3 jargon barrier in 2026 SB 253 and CBAM audit engagements

Here's the issue: Your 2026 SB 253 audit engagement letter arrived in January, scoped at 180 hours for Scope 1 and Scope 2 limited assurance. The partner mentioned that Scope 3 Category 1 would add "another 120-150 hours, depending on supplier-evidence completeness and primary-data lineage." You nodded, signed, and moved on. By May, the fieldwork bill had reached 340 hours, with a supplementary memo requesting "tier-2 data reconciliation" and "activity-data verification procedures" you had never heard of.

However, a Scope 3 audit engagement consists of two things: the emissions total you are disclosing, and the supplier-evidence vocabulary the auditor uses to scope the work. Your finance team negotiated the first. The auditor priced the second.

The emissions total on its own has no value in an assurance context. The supplier-evidence vocabulary is what the auditor is actually pricing—because every undefined term in the scoping call becomes a billable clarification procedure during fieldwork. If your CFO cannot distinguish "primary data" from "activity data," or "population completeness" from "sampling coverage," the auditor will define those terms at $450 per hour while reviewing your supplier invoices.

While emissions calculation has become cheaper—most platforms now automate Scope 1 and Scope 2 lineage—supplier-evidence scoping has become more expensive. A Big Four partner told us in December 2024 that firms without evidence-lineage vocabulary are paying 20 to 40 percent premiums on Scope 3 assurance engagements, because the scoping conversation alone requires three rounds of revision. If your team cannot articulate what "tier-2 visibility" means in the context of purchased-goods emissions, the auditor will assume zero supplier coverage and price accordingly.

How do you solve this? I think you start by learning the vocabulary before the engagement letter arrives. The operators we work with treat Scope 3 audit preparation as a translation exercise: procurement teams speak in supplier names and purchase orders, auditors speak in population frames and sampling strata. The CFO's job is to bridge that gap—not by becoming an auditor, but by knowing enough jargon to negotiate scope intelligently. For now, that means defining 12 terms that will appear in every 2026 SB 253 and CBAM audit engagement.

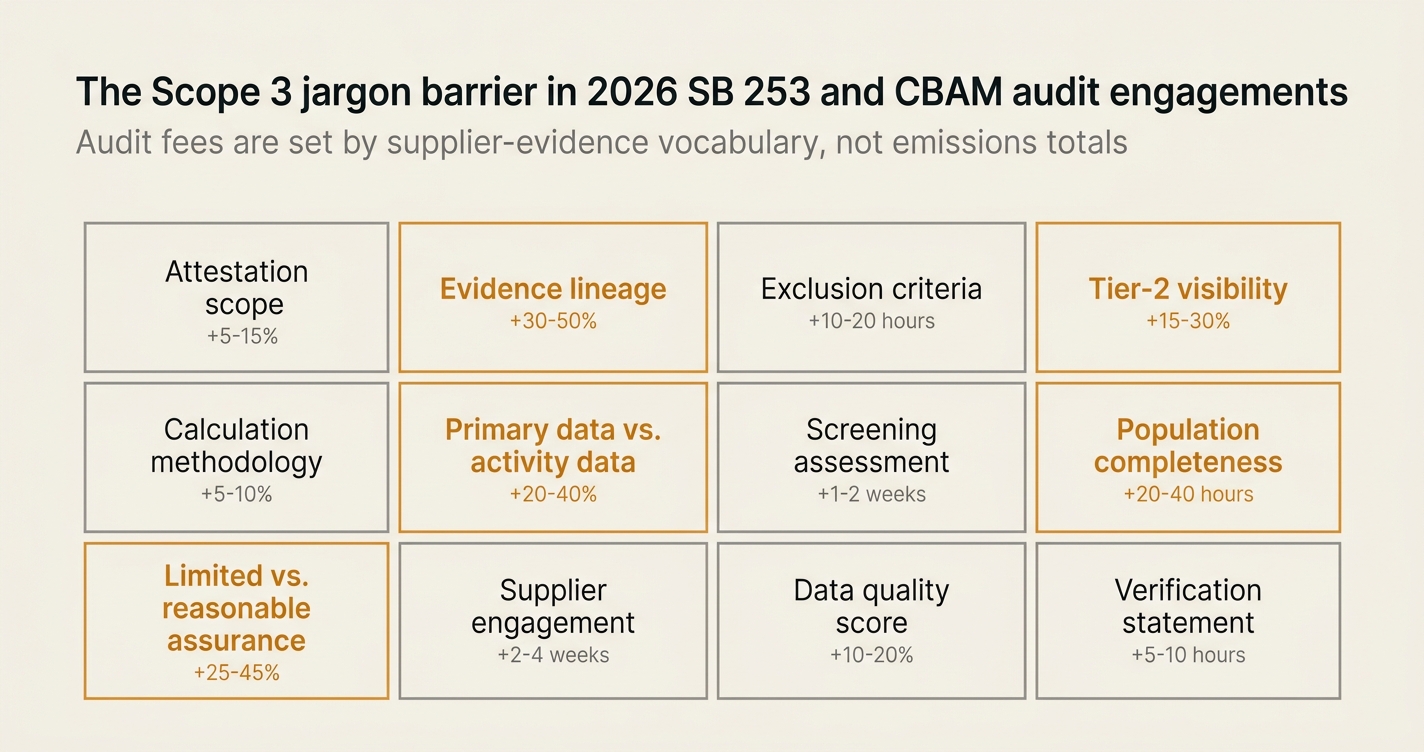

The shape of the argument, visualised below.

Why This Vocabulary Matters Now

"The assurance market is re-pricing. Firms without evidence lineage are paying 20-40% premiums, and CFOs who cannot speak the language of climate audit are losing control of scope and cost." — Big Four Assurance Partner, 2025 [1]

The 2026 SB 253 deadline is 382 days away for calendar-year reporters. Audit engagement letters are being negotiated in Q1 2025. California Air Resources Board (CARB) has confirmed that the first Scope 1 and Scope 2 reports are due August 10, 2026, with Scope 3 reporting beginning in 2027 [2]. If your procurement, facilities, and financial planning and analysis teams do not understand "population completeness" or "evidence lineage," you will pay for the auditor to define it—at $450 per hour—during fieldwork.

The table below maps 12 terms to the cost drivers in a typical climate assurance engagement:

| Term | Cost Impact | Typical Scoping Consequence |

|---|---|---|

| Limited assurance vs. reasonable assurance | 40-60% fee differential | Scope 1+2 engagements start at limited (2026-2029), scale to reasonable (2030+) [3] |

| Primary data vs. activity data | 25-35% uplift if undefined | Auditors assume zero primary data unless procurement can document supplier-specific values |

| Population completeness | 15-20% sampling expansion | Missing suppliers trigger expanded procedures to estimate unaudited emissions |

| Evidence lineage | 30-50% documentation premium | Firms without SOX-grade trails pay for auditor-led reconstruction |

| Tier-2 visibility | 20-30% Category 1 uplift | 40% of purchased-goods emissions hide in tier-2; auditors price for blind spots [4] |

| Materiality threshold | 10-15% scoping revision | Auditors define materiality differently than CFOs; misalignment triggers re-scoping |

This glossary defines 12 terms that will appear in your 2026 SB 253 and CBAM audit engagement letters, scoping calls, and assurance reports. Each entry includes a plain-English definition, a worked example, and the source regulation or standard. Bookmark this page—your audit committee will ask what "limited assurance" means, and you need an answer that connects to SOX-grade evidence expectations.

1. Limited Assurance vs. Reasonable Assurance

Plain-English Definition: Limited assurance means the auditor performs a review to determine whether anything appears materially misstated—a negative opinion ("nothing came to our attention"). Reasonable assurance means the auditor performs an audit with extensive testing and provides a positive opinion ("the data is free from material misstatement") [5].

Worked Example: A limited assurance engagement for Scope 1 and Scope 2 emissions might involve reviewing utility bills, checking calculation methods, and interviewing the facilities manager. A reasonable assurance engagement for the same scope would require testing internal controls, verifying meter readings, reconciling fuel invoices to consumption logs, and sampling facility-level data across multiple quarters.

Source Regulation: SB 253 requires limited assurance for Scope 1 and Scope 2 emissions beginning in 2026, scaling to reasonable assurance starting in 2030. There is currently no assurance requirement for Scope 3 emissions, but CARB has indicated this may change in future rulemaking [2].

Cost Implication: Reasonable assurance engagements typically cost 40 to 60 percent more than limited assurance for the same scope, because testing depth and documentation requirements increase substantially [3].

2. Primary Data vs. Activity Data

Plain-English Definition: Primary data is supplier-specific emissions data provided directly by the supplier (e.g., a steel mill reports 1.89 tonnes CO₂e per tonne of hot-rolled coil). Activity data is your procurement record of how much you purchased (e.g., 500 tonnes of steel) [6].

Worked Example: If your supplier sends you a carbon intensity certificate showing 1.89 tonnes CO₂e per tonne of product, that is primary data. If you multiply your purchase volume (500 tonnes) by that intensity, you are using activity data (the 500 tonnes) combined with primary data (the 1.89 factor). If you instead use a generic industry average (e.g., 2.1 tonnes CO₂e per tonne from a database), you have activity data but no primary data.

Source Regulation: CARB's SB 253 reporting template encourages alignment with the Greenhouse Gas Protocol Corporate Standard, which distinguishes primary data (supplier-specific) from secondary data (industry averages or spend-based estimates) [2]. CBAM requires actual embedded emissions from installations, not default values, which is functionally a primary-data requirement [7].

Cost Implication: Auditors cannot verify supplier-specific emissions claims without supplier-provided documentation. If your procurement system classifies spend-based estimates as "primary data," the auditor will re-scope the engagement to reflect zero primary-data coverage, adding 25 to 35 percent to Category 1 assurance costs [4].

3. Population Completeness

Plain-English Definition: Population completeness means your supplier list and procurement records account for all material purchased-goods emissions in Scope 3 Category 1. If 15 percent of your spend is unclassified or missing supplier identifiers, your population is incomplete.

Worked Example: Your enterprise resource planning system shows $450 million in Scope 3 Category 1 spend. However, $68 million is coded to "miscellaneous suppliers" with no supplier name or address. The auditor will treat that $68 million as an incomplete population and either (a) request additional procedures to identify those suppliers, or (b) assume higher uncertainty and flag it as a limitation in the assurance opinion.

Source Regulation: ISO 14064-3, the international standard for GHG assurance, requires verifiers to assess "completeness" of the emissions inventory—meaning all material sources are identified and quantified. CARB has not specified a completeness threshold, but auditors default to ISO standards [5].

Cost Implication: Missing suppliers trigger expanded sampling procedures. If 10 percent of your spend is unclassified, the auditor may expand the sample by 15 to 20 percent to estimate the emissions gap, adding 15 to 20 hours to the engagement.

4. Evidence Lineage

Plain-English Definition: Evidence lineage is the documented chain from source document (invoice, bill of materials, utility bill) to emission factor to calculated emissions to disclosure line item. Every number in your report must trace back to a specific document.

Worked Example: Your Scope 3 report states 12,450 tonnes CO₂e from purchased steel. The evidence lineage would show: (1) supplier invoice #78234 for 500 tonnes of steel, (2) supplier carbon intensity certificate showing 1.89 tonnes CO₂e per tonne, (3) calculation: 500 × 1.89 = 945 tonnes CO₂e, (4) aggregation of 15 such invoices totaling 12,450 tonnes CO₂e, (5) export to disclosure template.

Source Regulation: SB 253 does not explicitly mandate evidence lineage, but CARB's enforcement discretion notice for 2026 states that companies should use "the data companies already have or were collecting" when the enforcement notice was issued, which auditors interpret as requiring documentary support for all reported figures [2].

Cost Implication: Firms without SOX-grade evidence trails pay 30 to 50 percent premiums, because the auditor must reconstruct the lineage during fieldwork. One Big Four partner estimated that evidence-lineage retrofitting adds 80 to 120 hours to a typical Scope 1 and Scope 2 limited assurance engagement [1].

5. Tier-2 Visibility

Plain-English Definition: Tier-2 visibility means you can identify the suppliers of your suppliers—the upstream sources of emissions embedded in the goods you purchase. Most procurement systems track only tier-1 suppliers (the companies you pay directly).

Worked Example: You purchase circuit boards from a tier-1 supplier in Taiwan. That supplier purchases copper foil from a tier-2 supplier in Japan. If you cannot name the tier-2 copper supplier, you have no tier-2 visibility. For CBAM-regulated goods, this matters because 40 percent of embedded emissions often hide in tier-2 production steps [4].

Source Regulation: CBAM requires actual embedded emissions from upstream installations, which in practice demands tier-2 visibility for complex goods like steel (scrap inputs), aluminum (anode production), and chemicals (feedstock sourcing). SB 253 does not explicitly require tier-2 data, but auditors will assess whether tier-1 data alone provides reasonable coverage of Category 1 emissions [7].

Cost Implication: If your Category 1 disclosure excludes tier-2 emissions, the auditor will either (a) qualify the opinion as incomplete, or (b) request expanded procedures to estimate the tier-2 gap. Either outcome adds 20 to 30 percent to the Category 1 assurance cost.

6. Spend-Based Estimation

Plain-English Definition: Spend-based estimation calculates emissions by multiplying procurement spend by an emission factor per dollar (e.g., $1 million of steel = 500 tonnes CO₂e). It is the lowest-quality method in the GHG Protocol hierarchy.

Worked Example: Your company spent $12 million on steel in 2025. You apply a spend-based emission factor of 0.42 tonnes CO₂e per $1,000, yielding 5,040 tonnes CO₂e. This estimate ignores the actual carbon intensity of your suppliers' mills, the product mix (hot-rolled vs. cold-rolled), and the energy source (coal vs. electric arc furnace).

Source Regulation: The GHG Protocol Corporate Value Chain (Scope 3) Standard ranks spend-based estimation as the least preferred method, below supplier-specific data and physical activity-based calculations. CARB's SB 253 guidance encourages companies to "use existing reporting standards such as the GHG Protocol" [2].

Cost Implication: Spend-based estimates cannot be verified at a supplier level, which limits the assurance opinion. If more than 30 percent of your Scope 3 Category 1 emissions rely on spend-based factors, the auditor may issue a qualified opinion or exclude those emissions from the assured total. This creates compliance risk under SB 253, where disclosure is mandatory even if assurance is limited [3].

7. Activity Data Verification

Plain-English Definition: Activity data verification means the auditor tests whether your procurement records (tonnes purchased, kilowatt-hours consumed, vehicle-kilometers traveled) are accurate and complete. This is distinct from verifying the emission factors you applied.

Worked Example: Your Scope 1 report states 45,000 tonnes CO₂e from natural gas combustion, calculated as 180,000 MMBtu × 0.25 tonnes CO₂e per MMBtu. Activity data verification checks the 180,000 MMBtu figure: the auditor reconciles utility invoices, meter readings, and facility logs to confirm you actually consumed 180,000 MMBtu.

Source Regulation: ISO 14064-3 requires verifiers to assess both activity data and emission factors. CARB has not specified verification procedures, but auditors default to ISO standards, which treat activity data verification as foundational [5].

Cost Implication: Activity data verification is less expensive than emission factor verification, because utility bills and purchase orders are standardized documents. However, if your enterprise resource planning system does not track physical units (only dollars), the auditor must reconstruct activity data from invoices, adding 10 to 15 hours per Scope 3 category.

8. Materiality Threshold

Plain-English Definition: A materiality threshold is the percentage or absolute value below which an emissions source is considered immaterial and may be excluded from detailed verification. Auditors and CFOs often define materiality differently.

Worked Example: Your total Scope 3 emissions are 500,000 tonnes CO₂e. You propose a 5 percent materiality threshold, meaning sources below 25,000 tonnes CO₂e (5 percent of 500,000) do not require supplier-specific data. The auditor counters with a 2 percent threshold (10,000 tonnes), arguing that California regulations treat climate disclosure as financial disclosure, where lower materiality thresholds apply.

Source Regulation: SB 253 does not define materiality, but it classifies climate disclosure as a financial filing with executive liability. Financial audits under Sarbanes-Oxley typically use 1 to 2 percent materiality thresholds for revenue-based metrics, which auditors may apply to emissions disclosure [3].

Cost Implication: Disagreement over materiality triggers scoping revisions. If the auditor uses a 2 percent threshold and you assumed 5 percent, the number of "material" suppliers requiring detailed verification could double, adding 10 to 15 percent to the engagement cost.

9. Sampling Coverage

Plain-English Definition: Sampling coverage is the percentage of total emissions (by mass or spend) included in the auditor's verification sample. Higher coverage reduces uncertainty but increases audit cost.

Worked Example: Your Scope 3 Category 1 emissions total 300,000 tonnes CO₂e from 1,200 suppliers. The auditor selects a sample of 80 suppliers representing 240,000 tonnes CO₂e (80 percent coverage by mass). The auditor verifies supplier data for those 80 suppliers and extrapolates the findings to the remaining 1,120 suppliers.

Source Regulation: ISO 14064-3 does not mandate a specific sampling percentage, but industry practice for limited assurance targets 60 to 80 percent coverage by emissions mass. Reasonable assurance typically requires 80 to 95 percent coverage [5].

Cost Implication: Each 10 percent increase in sampling coverage adds approximately 8 to 12 hours of fieldwork, because the auditor must verify additional supplier certificates, invoices, and calculations.

10. Emission Factor Provenance

Plain-English Definition: Emission factor provenance is the documented source and date of the emission factor you used in your calculation (e.g., "US EPA 2024 emission factors for natural gas combustion, published March 2024").

Worked Example: Your Scope 2 calculation uses an emission factor of 0.45 kg CO₂e per kWh for California grid electricity. The auditor asks: "Which source? Which year?" You provide the EPA eGRID 2023 dataset, published in January 2025. The auditor verifies that the factor matches the published value and that the dataset is appropriate for your reporting period (calendar year 2025).

Source Regulation: The GHG Protocol Corporate Standard requires companies to document the source and vintage of all emission factors. CARB's SB 253 reporting template includes fields for "emissions calculation methodology" and "data sources," which auditors interpret as requiring emission factor provenance [2].

Cost Implication: Missing or undocumented emission factors trigger verification delays. If your calculations reference "internal factors" or "consultant estimates" without source documentation, the auditor will request additional evidence or re-calculate using default factors, adding 5 to 8 hours per Scope.

11. Supplier Engagement Rate

Plain-English Definition: Supplier engagement rate is the percentage of material suppliers (by spend or emissions) that responded to your primary-data collection request. A 30 percent engagement rate means 70 percent of your suppliers did not provide data.

Worked Example: You sent carbon intensity questionnaires to 500 tier-1 suppliers representing $400 million in Scope 3 Category 1 spend. 150 suppliers responded with usable data, covering $180 million of spend. Your supplier engagement rate is 37.5 percent by supplier count, or 45 percent by spend coverage.

Source Regulation: Neither SB 253 nor CBAM specifies a minimum engagement rate, but low engagement rates limit the accuracy and assurance-readiness of Scope 3 disclosures. Industry benchmarks for mature programs range from 40 to 60 percent engagement by spend [4].

Cost Implication: Low engagement rates force reliance on spend-based estimates, which (as noted in Term 6) cannot be verified at a supplier level. If your engagement rate is below 40 percent, the auditor may qualify the Scope 3 assurance opinion or exclude unverified emissions from the assured total, creating compliance risk under mandatory disclosure regimes.

12. Assurance-Ready Documentation

Plain-English Definition: Assurance-ready documentation means every emissions figure in your report is supported by a source document, a calculation log, and a reconciliation to your disclosure template—before the auditor arrives.

Worked Example: Your Scope 1 report includes 8,500 tonnes CO₂e from diesel combustion in company vehicles. Assurance-ready documentation would include: (1) fuel purchase receipts for every diesel transaction, (2) a calculation log showing litres purchased × emission factor = tonnes CO₂e, (3) a reconciliation showing how the 8,500-tonne total maps to the "Mobile Combustion" line item in your SB 253 disclosure.

Source Regulation: CARB's enforcement discretion notice for 2026 states that companies should prepare reports "based on the data companies already have or were collecting" when the enforcement notice was issued, which auditors interpret as requiring pre-existing documentation systems, not retrofitted evidence [2].

Cost Implication: Firms without assurance-ready documentation pay for the auditor to build the documentation system during fieldwork. One UL Solutions case study estimated that pre-audit documentation preparation reduces total assurance costs by 25 to 35 percent, because the auditor spends less time reconstructing evidence trails [5].

The Vocabulary-to-Cost Translation Table

| If the auditor says… | They are pricing for… | Typical cost impact |

|---|---|---|

| "We'll need to assess population completeness" | Missing or unclassified suppliers | +15-20 hours |

| "What's your primary-data coverage?" | The percentage of emissions with supplier-specific factors | +25-35% if < 40% coverage |

| "Can you provide evidence lineage?" | Source documents for every emissions figure | +80-120 hours if absent |

| "We'll use a 2% materiality threshold" | Verification of suppliers you thought were immaterial | +10-15% scope expansion |

| "What's your tier-2 visibility?" | Upstream emissions your tier-1 data does not capture | +20-30% Category 1 uplift |

| "We'll need activity data verification" | Reconciliation of physical units to invoices | +10-15 hours per Scope 3 category |

How Emission3 Fits

Emission3 was built to eliminate the jargon barrier before the audit engagement letter arrives. Our platform generates:

- Evidence lineage by default: Every emissions figure traces to a source document (invoice, bill of materials, utility bill), with calculation logs and reconciliation to disclosure line items—before the auditor requests it.

- Primary-data coverage reports: Automated analysis of which suppliers provided supplier-specific data, which emissions rely on spend-based estimates, and where the audit risk concentrates.

- Assurance-ready exports: Pre-formatted evidence packs for auditors, including population completeness summaries, emission factor provenance tables, and activity data verification trails.

We work primarily with CFOs preparing for SB 253 Scope 1 and Scope 2 assurance (due August 10, 2026) and non-EU exporters facing CBAM quarterly reporting (due April 30, 2027). Our engagements start with a CBAM or SB 253 readiness call: we map your supplier data, identify evidence gaps, and translate procurement records into auditor vocabulary—so you can negotiate scope intelligently, not reactively.

If your 2026 audit engagement letter included terms you had to look up, that is a pricing signal. The vocabulary gap is the cost driver.

Start with the Readiness Call

Emission3 customers do not onboard anonymously. Every engagement begins with a CBAM or SB 253 readiness conversation: we review your supplier list, assess primary-data coverage, and map the evidence lineage your auditor will request. You leave the call with a scoped implementation plan and a vocabulary checklist—so the audit engagement becomes a verification exercise, not a vocabulary lesson.

Book a CBAM readiness call to identify your jargon gaps before the auditor does [8].

References & Sources

External Sources

- [1]The US Climate Disclosure Stack: 12 Terms Every CFO Must Know Before 2026 SB 253 Audits

Big Four partner quoted on assurance market re-pricing and evidence lineage premiums for firms without SOX-grade climate documentation.

- [2]SB 253/261 Public Workshop — California Air Resources Board

CARB workshop slides confirming August 10, 2026 deadline for Scope 1 and Scope 2 reporting, enforcement discretion, and alignment with GHG Protocol standards.

- [3]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law Now That CARB Has Finalized the Rules

Terrascope overview of limited versus reasonable assurance requirements, timeline transitions, and cost implications for audit-ready data systems.

- [5]The assurance gap: Are you ready for third-party verification under SB 253?

UL Solutions guide to understanding limited versus reasonable assurance, ISO 14064-3 verification requirements, and building assurance-ready systems.

- [7]Navigating California's Climate Disclosure Laws: Your Complete Guide to SB 253 and SB 261

Nelson Mullins legal analysis of CARB's final rulemaking, fee structures, and the relationship between SB 253 and CBAM primary-data requirements.

Related Content

- [4]The tier-2 data gap in CBAM-ready supplier engagement programs

Analysis of why 40% of embedded emissions hide in tier-2 suppliers and how procurement teams are pricing the visibility gap.

- [6]The primary-data illusion in 2026 Scope 3 assurance engagements

Emission3 analysis of how procurement teams misclassify activity data as primary data and the resulting audit-scope expansion.

- [8]Book a CBAM readiness call

All Emission3 customers start with a readiness call: we map suppliers, gaps, and implementation. No anonymous self-serve onboarding.