The assurance-fee escalation problem in California SB 253 compliance for mid-market manufacturers

The assurance-fee escalation problem in California SB 253 compliance for mid-market manufacturers

Here's the issue: a mid-market industrial manufacturer with operations in California now faces SB 253 compliance—Scope 1 and Scope 2 emissions due August 10, 2026, Scope 3 emissions starting 2027, and limited assurance beginning in 2027. The CFO budgeted for carbon accounting software and a one-time audit engagement. The first-year filing came in under budget. By year two, the assurance fee had tripled, and the auditor requested evidence lineage for 180 line items the software had aggregated into summary totals. The filing deadline was six weeks away.

However, an SB 253 filing consists of two things: emissions totals and evidence lineage. Emissions totals are what the software calculates—aggregated tonnes of carbon dioxide equivalent across Scope 1, Scope 2, and eventually Scope 3. Evidence lineage is the reproducible path from each invoice, bill of lading, utility bill, and supplier questionnaire to the final number in the filing—the audit trail that demonstrates every tonne is grounded in a source document, not an assumption.

Emissions totals on their own have no value. Evidence lineage is what the auditor is actually asking for, what the California Air Resources Board will verify, and what determines whether your assurance engagement stays in the 40-hour band or escalates to 200 hours. While carbon accounting software has become cheaper, evidence-gathering has become more expensive. If your software produces summary totals without line-item traceability, the cost of post-hoc evidence collection might outpace the savings of the software itself. For a manufacturer with 1.2 billion USD in revenue, the delta between a clean evidence package and a scrambled reconstruction is 60,000 to 150,000 USD in assurance fees—per year.

How do you solve this? I think the operators we work with focus on deterministic ingestion before they focus on dashboards. For now, that means document-first workflows: invoices, bills of lading, and utility bills are parsed on arrival, emissions are calculated line-by-line with full lineage to the source file, and the evidence package is generated as a by-product of the calculation, not an afterthought. The assurance engagement becomes a review of the lineage artifact, not a four-week evidence hunt.

The shape of the argument, visualised below.

The anonymised case: a California manufacturer's assurance journey

In November 2025, a U.S.-based manufacturer of precision metal components—annual revenue 1.3 billion USD, three facilities in California, supply chain spanning 14 countries—engaged Emission3 to prepare for SB 253 compliance. The company's CFO had already purchased carbon accounting software in early 2025, anticipating the August 2026 Scope 1 and Scope 2 reporting deadline. The software produced emissions totals, but when the CFO shared the outputs with the company's auditor in January 2026, the auditor requested line-item evidence for every material input: utility bills, freight invoices, supplier-specific emission factors, and process-level activity data. The software had no mechanism to export this lineage. The CFO faced a choice: reconstruct the evidence manually, or re-platform before the filing deadline.

The company chose re-platforming. Emission3's implementation began in February 2026. The scope included:

- Document ingestion for 18 months of utility bills (electricity, natural gas, diesel) across three facilities.

- Freight invoice parsing for 2,400 inbound shipments (raw material deliveries from suppliers in the U.S., Mexico, South Korea, and Germany).

- Process emissions calculation for on-site welding, heat treatment, and surface finishing operations.

- Refrigerant leak tracking for 12 HVAC units and industrial cooling systems.

- Evidence package generation with line-item traceability from each source document to the final Scope 1 and Scope 2 totals.

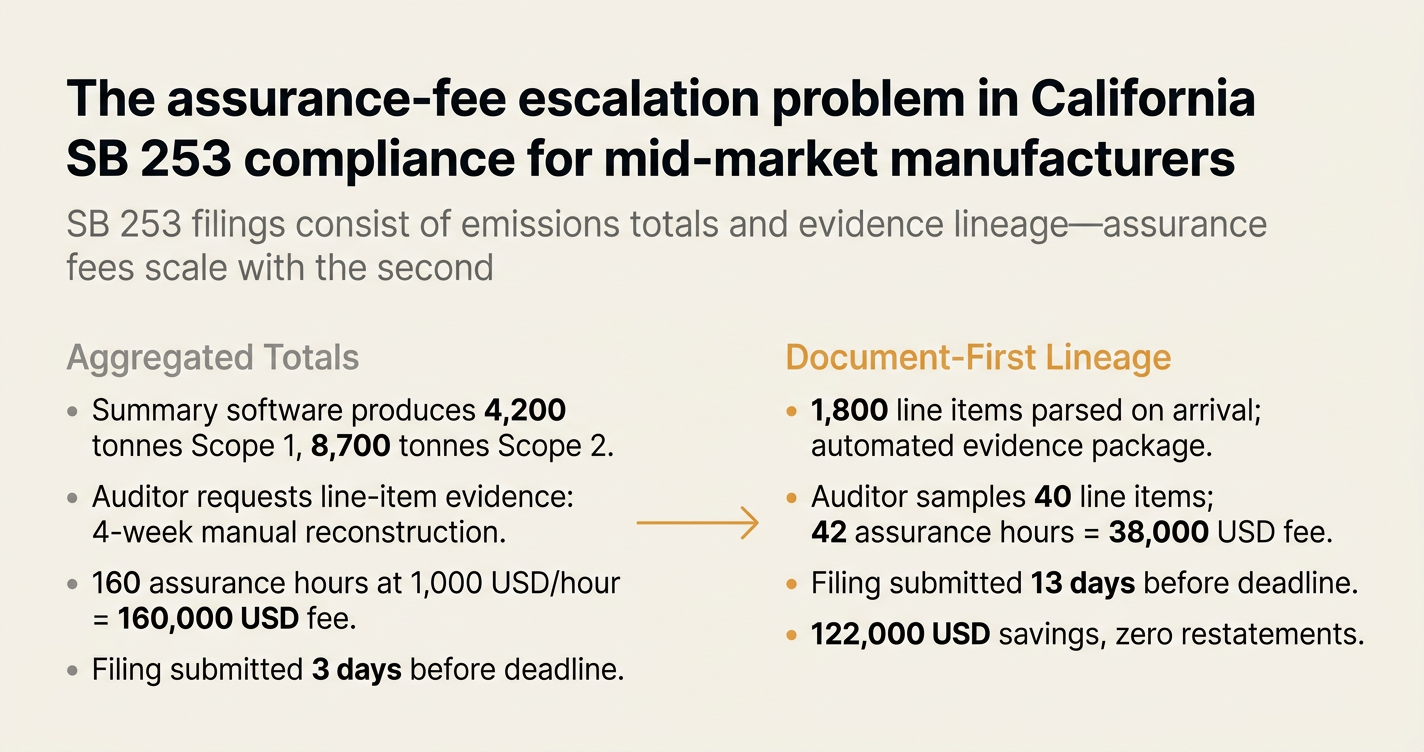

The engagement took nine weeks. The assurance review, conducted in June 2026 by a Big Four firm, took 42 hours—within the original 40-hour estimate. The auditor's report noted zero material misstatements. The filing was submitted July 28, 2026, 13 days before the deadline. The total cost of assurance: 38,000 USD, compared to the 120,000 USD quoted for the original software's outputs.

Why the assurance fee escalated in the first attempt

The original carbon accounting software calculated emissions correctly. The issue was not mathematical accuracy—it was evidence structure. The software aggregated utility consumption into monthly totals, applied standard emission factors from the U.S. Environmental Protection Agency eGRID database, and produced a summary table: Scope 1 emissions = 4,200 tonnes CO₂e, Scope 2 emissions (location-based) = 8,700 tonnes CO₂e. The CFO assumed this summary would satisfy the auditor.

It did not. Under SB 253, limited assurance engagements follow standards including International Standard on Sustainability Assurance 5000, ISAE 3410, or AT-C Section 210. [1] All of these standards require the auditor to verify that reported emissions are free from material misstatement, which means tracing each tonne back to a source document. The auditor requested:

- Individual utility bills for each facility, with meter readings and billing periods matched to the reported consumption.

- Freight invoices with shipment weights, distances, and transport modes (truck, rail, ocean container) matched to the freight emission calculations.

- Refrigerant purchase receipts and leak logs matched to the fugitive emissions totals.

- Process-level activity data (hours of operation, fuel consumption per batch) matched to the on-site combustion totals.

The software had none of this. The CFO's team spent four weeks reconstructing the evidence: scanning paper utility bills, matching invoice line items to shipment records in the ERP system, and cross-referencing refrigerant logs with facility maintenance records. The auditor's review stretched from 40 hours to 160 hours. The assurance fee escalated from 35,000 USD to 140,000 USD. The filing was submitted three days before the deadline, with the auditor noting "significant evidence-gathering challenges" in the management representation letter.

The architectural difference: document-first ingestion vs. summary aggregation

Emission3's approach begins with document ingestion, not data entry. Every source document—utility bill, freight invoice, supplier questionnaire, process log—is parsed on arrival using a deterministic large language model layer. The LLM extracts structured fields (meter reading, billing period, shipment weight, transport mode) and stores them alongside the original PDF. Emissions are calculated line-by-line, with each calculation linked to the source document and the emission factor applied. The evidence package is generated automatically: a zip file containing the source documents, the calculation lineage, and the final totals, structured for auditor review.

This is not post-hoc documentation. The evidence package is a by-product of the calculation workflow. When the auditor requests line-item traceability, the system exports a table with these columns:

| Line Item | Source Document | Activity Data | Emission Factor | Calculation | CO₂e (tonnes) |

|---|---|---|---|---|---|

| Facility 1, electricity, Jan 2025 | Utility_Bill_Jan2025.pdf | 120,000 kWh | 0.385 kg CO₂e/kWh (California grid, 2025) | 120,000 × 0.385 / 1,000 | 46.2 |

| Inbound freight, shipment #4472 | Invoice_4472.pdf | 18 tonnes, 320 km, truck | 0.062 kg CO₂e/tonne-km (EPA freight factors) | 18 × 320 × 0.062 / 1,000 | 0.357 |

| Refrigerant leak, Unit 7 | Leak_Log_Mar2025.pdf | 2.4 kg R-410A | 2,088 kg CO₂e/kg (IPCC AR6) | 2.4 × 2,088 / 1,000 | 5.01 |

Every number is reproducible. The auditor can open the source PDF, verify the extracted fields, and trace the calculation to the final total. The review becomes a sampling exercise, not a reconstruction project. For this manufacturer, the auditor sampled 40 line items (out of 1,800 total), verified the calculations, and issued a clean opinion. The engagement took 42 hours.

The quantified consequence: assurance fees vs. evidence structure

The cost of assurance under SB 253 is not fixed. It scales with evidence quality. The California Air Resources Board does not specify assurance standards in detail for the first reporting year, but the board has indicated that limited assurance will be required starting in 2027, with reasonable assurance beginning in 2030. [2] Auditors are already pricing engagements based on the evidence structure they expect to review.

For mid-market manufacturers (revenue between 1 billion and 5 billion USD), the baseline assurance engagement is 40 to 60 hours. If the evidence is clean—line-item traceability, reproducible calculations, source documents attached—the engagement stays in this range. If the evidence is aggregated or reconstructed, the engagement expands to 120 to 200 hours. The hourly rate for sustainability assurance at a Big Four firm is typically 800 to 1,200 USD. The delta is:

- Clean evidence: 40 hours × 1,000 USD = 40,000 USD.

- Reconstructed evidence: 160 hours × 1,000 USD = 160,000 USD.

- Delta: 120,000 USD, per year.

Over a three-year compliance cycle (2026 to 2028, covering Scope 1, Scope 2, and the first year of Scope 3), the cumulative delta is 360,000 USD. For a manufacturer with 5,000 line items per year (typical for a multi-facility operation with complex freight and utility structures), the cost per line item for post-hoc evidence reconstruction is 24 USD. The cost per line item for deterministic ingestion is effectively zero—it is absorbed into the calculation workflow.

How Emission3 fits: deterministic lineage for SB 253 assurance

Emission3 is positioned as document-first compliance infrastructure, not generic carbon accounting software. The platform ingests source documents (utility bills, freight invoices, supplier questionnaires, process logs), extracts structured fields using a deterministic LLM layer, calculates emissions line-by-line with full traceability, and generates auditor-ready evidence packages as a by-product of the workflow. Every calculation is reproducible. Every number links to a source PDF. The evidence package is generated automatically, structured for limited assurance review under ISSA 5000, ISAE 3410, or AT-C 210. [3]

For SB 253 compliance, Emission3 supports:

- Scope 1 and Scope 2 emissions for the August 2026 deadline, with evidence packages ready for limited assurance review in 2027.

- Scope 3 Category 1 (purchased goods and services) and Category 4 (upstream transportation) for the 2027 reporting cycle, using supplier invoices and freight bills as the ingestion layer.

- Cross-year comparability: the same document-first workflow applies to 2026, 2027, and 2028 filings, so the evidence structure is consistent across reporting cycles.

- Audit-ready exports: evidence packages include source documents, calculation lineage, emission factor references, and a summary table formatted for auditor sampling.

The architectural difference is deterministic ingestion. Most carbon accounting platforms ask users to enter summary data (total electricity consumption, total freight spend) and apply emission factors to aggregated totals. Emission3 starts with the invoice, parses the line items, and calculates emissions at the transaction level. The evidence package is not an afterthought—it is the native output of the system.

For the manufacturer in this case study, the implementation took nine weeks. The evidence package for the August 2026 filing included 1,800 line items, 240 source PDFs, and a calculation lineage table with 5,400 rows (three rows per line item: activity data extraction, emission factor application, final calculation). The auditor sampled 40 line items, verified the calculations against the source PDFs, and issued a clean opinion. The assurance fee was 38,000 USD, 73% below the quoted fee for the original software's outputs.

What this means for CFOs preparing for SB 253 in 2026 and 2027

If you are a CFO or finance leader at a U.S. company with over 1 billion USD in revenue doing business in California, you are in scope for SB 253. The first Scope 1 and Scope 2 filing is due August 10, 2026. [4] Limited assurance is not required for this first filing, but it will be required starting in 2027, and auditors are already pricing engagements based on the evidence structure they expect. If your current carbon accounting system produces summary totals without line-item traceability, you face a choice: reconstruct the evidence manually (typical cost: 120,000 to 200,000 USD in assurance fees), or re-platform to a document-first workflow before the 2027 cycle begins.

The cost of re-platforming is typically lower than the cost of post-hoc evidence reconstruction. For a mid-market manufacturer with three to five facilities and 1,500 to 3,000 line items per year, an Emission3 implementation takes eight to twelve weeks and costs 60,000 to 120,000 USD (depending on document volume and Scope 3 complexity). The assurance fee savings in year two alone typically exceed the implementation cost. Over a three-year compliance cycle, the cumulative savings are 250,000 to 400,000 USD.

The secondary benefit is zero restatements. When every calculation is reproducible and every number links to a source document, the risk of material misstatement drops to near-zero. For companies facing executive liability under SB 253 (penalties up to 500,000 USD per reporting year for non-compliance), [5] the cost of a clean assurance opinion is not just financial—it is reputational and legal.

If you are preparing for SB 253 and want to understand whether your current evidence structure will satisfy a limited assurance engagement in 2027, we recommend starting with a CBAM readiness call. The same document-first workflow that supports California SB 253 compliance also supports EU Carbon Border Adjustment Mechanism filings, which begin in 2026 for importers of steel, aluminium, cement, fertilisers, electricity, and hydrogen. [6] The architectural requirements are identical: line-item traceability, reproducible calculations, and auditor-ready evidence packages. A single implementation can support both regulatory programs.

Emission3's audit-ready exports include evidence packages formatted for limited assurance review, calculation lineage tables with full traceability, and submission-oriented outputs for CARB's SB 253 reporting portal. [7] The evidence structure is designed to minimise assurance fees, eliminate restatements, and position your organisation for reasonable assurance in 2030 without re-platforming. If that sounds relevant to your compliance planning, book a CBAM readiness call to map your current evidence gaps and implementation timeline. [8]

References & Sources

External Sources

- [1]California Climate Legislation Update — Status of CARB Rulemaking and Reporting Updates for 2026

CARB's guidance on assurance standards for SB 253, including ISSA 5000, ISAE 3410, and AT-C 210, and the phased implementation of limited and reasonable assurance requirements.

- [2]A guide to California's climate disclosure rules (SB 253, SB 261, SB 219)

Overview of SB 253 timelines, including Scope 1 and 2 reporting in 2026, Scope 3 in 2027, and the transition from limited assurance (2027-2029) to reasonable assurance (2030 onwards).

- [3]SB 253 Compliance Roadmap: How to Prepare for California's Climate Disclosure Law

Detailed compliance roadmap for SB 253, including reporting templates, assurance requirements, and CARB's enforcement discretion for first-year submissions.

- [4]California's climate disclosure laws: An overview of SB 253 & SB 261

Explanation of SB 253 phased rollout, including the August 10, 2026 deadline for Scope 1 and 2 emissions and the gradual scaling of assurance requirements.

- [5]California's New Climate Disclosure Laws for Large Businesses

Overview of SB 253 and SB 261 requirements, including revenue thresholds, reporting schedules, and enforcement mechanisms under CARB oversight.

Related Content

- [6]The verification-timing penalty for non-EU exporters in CBAM filings

Analysis of how verification scheduling determines CBAM tariff costs, using the same document-first evidence structure required for SB 253 limited assurance.

- [7]Audit-ready exports in Emission3

Emission3's evidence lineage artifact: line-item traceability, calculation reproducibility, and submission-oriented outputs for auditors and regulators.

- [8]Book a CBAM readiness call

Start with a readiness call to map your current evidence gaps, supplier data availability, and implementation timeline for SB 253 and CBAM compliance.