The default-value penalty for non-EU steel exporters in CBAM filings

The default-value penalty for non-EU steel exporters in CBAM filings

Here's the issue: non-EU steel exporters shipping to the European Union in 2026 face a carbon cost for every tonne of product entering the single market. At the Q1 2026 certificate price of €75.36 per tonne CO₂, a single shipment of 500 tonnes of hot-rolled coil carrying 2.1 tonnes of embedded emissions per tonne of steel triggers a CBAM certificate cost of €79,128. Most exporters assume the calculation is straightforward: measure emissions, multiply by the carbon price, and pay. But the CBAM filing workflow splits into two distinct compliance paths, and choosing the wrong one inflates the declared carbon intensity by 200 to 500 percent.

However, a CBAM filing consists of two things: embedded emissions totals and installation-level data. The emissions total is what the EU importer declares in the CBAM Registry. The installation-level data is the auditable evidence that supports the total—monitoring plans, production records, utility bills, and third-party verification reports that prove the declared emissions reflect actual operations at the manufacturing site.

Embedded emissions totals on their own have no value. Installation-level data is what the CBAM declarant and the verification body are actually asking for. When an exporter cannot provide third-party verified emissions data from the production installation, the EU importer must fall back on country-specific default values published by the European Commission in Implementing Regulation 2025/2621. These default values are set conservatively to reflect the worst-case emissions for each country and product type, with a markup. For Indian steel producers using direct reduced iron technology with natural gas, actual emissions may be 40 to 60 percent below the country default. But without accredited verification of actual values, the importer pays CBAM certificates on the inflated default figure—and the exporter bears the commercial consequence.

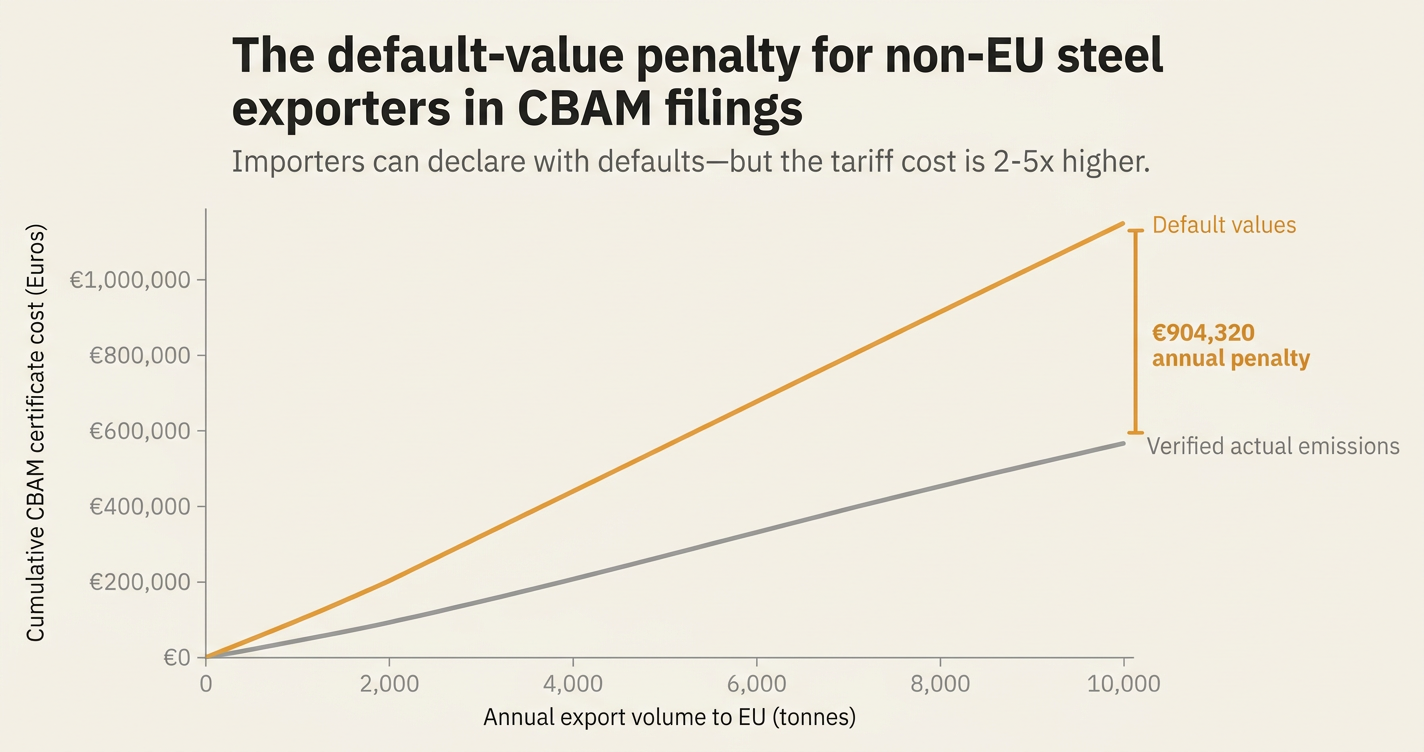

While embedded emissions reporting has become cheaper—monitoring software, carbon accounting SaaS, and procurement-side Scope 3 platforms have proliferated since 2023—installation-level data collection has become more expensive. If an exporter ships 10,000 tonnes of steel per year to the EU, and the difference between actual emissions and default values is 1.2 tonnes CO₂ per tonne of steel, the annual penalty is €904,320 at Q1 2026 certificate prices. That penalty recurs every compliance year. The cost of third-party verification for a single steel installation in 2026 ranges from €15,000 to €40,000, depending on the complexity of the production process and the verifier's travel requirements. The payback period is six weeks.

How do you solve this? I think the answer depends on whether the exporter treats CBAM as a reporting obligation or as a commercial negotiation with the EU importer. For now, the exporters we work with who avoid the default-value penalty share three characteristics: they mapped every production installation to the CBAM goods produced at that site before January 2026; they collected twelve months of utility bills, process emissions data, and purchased goods invoices before the first verification cycle in Q1 2026; and they contracted an accredited verifier early enough to secure a site visit slot in the first half of 2026, when verification capacity was still available. The operators who treated CBAM as a January 2026 problem are now negotiating contract amendments with EU buyers who cannot absorb the default-value markup.

The shape of the argument, visualised below.

The arithmetic of the default-value penalty

The penalty is not a compliance fine. It is the difference between what the EU importer pays in CBAM certificates when declaring actual emissions versus default values. The table below compares the certificate cost for a single shipment of 500 tonnes of hot-rolled steel coil from three countries, using actual emissions data versus EU default values.

| Country | Actual emissions (tCO₂/t steel) | Default value (tCO₂/t steel) | Certificate cost (actual) | Certificate cost (default) | Penalty per shipment |

|---|---|---|---|---|---|

| India | 1.8 | 2.9 | €67,824 | €109,272 | €41,448 |

| Turkey | 1.6 | 2.4 | €60,288 | €90,432 | €30,144 |

| Vietnam | 2.1 | 3.2 | €79,128 | €120,576 | €41,448 |

Table assumptions: Q1 2026 CBAM certificate price of €75.36 per tonne CO₂, 500-tonne shipment, CBAM factor of 2.5% (reflecting the transitional free allocation phase-out schedule).

The penalty scales linearly with volume. An exporter shipping 10,000 tonnes per year to the EU pays an additional €828,960 annually if relying on default values for Indian steel, or €602,880 for Turkish steel. The European Commission designed the default value system to discourage its use. As the Clean Carbon AI compliance guide notes, "using default values will always mean paying more carbon tax than applicable on actual emissions. This is a deliberate design to prevent carbon leakage and discourage use of default values." [1]

The penalty is not hypothetical. EU importers began purchasing CBAM certificates in April 2026 for Q1 2026 imports. Importers who could not provide verified actual emissions data from their non-EU suppliers paid certificate costs based on default values. Those importers are now renegotiating supply contracts to push the penalty back onto the exporter, either through direct price reductions or through contractual requirements to provide verified emissions data in future quarters. The carbon cost has become a line item in the commercial negotiation.

What installation-level data actually means

The CBAM Regulation defines installation-level data as the emissions monitoring, reporting, and verification framework required to calculate embedded emissions using actual values. The monitoring must follow a top-down approach: emissions are monitored at the installation level, attributed to specific production processes, and converted to specific embedded emissions per tonne of goods produced. The methodology is set out in Implementing Regulation 2025/2547. [2]

Installation-level monitoring requires three categories of data:

-

Direct emissions from production processes. For steel, this includes emissions from blast furnaces, basic oxygen furnaces, electric arc furnaces, and direct reduced iron units. Monitoring must be based on either continuous emissions measurement systems or calculation-based methodologies using fuel consumption and emission factors. The calculation must account for process-specific inputs: coal, coke, natural gas, electricity, and purchased ferroalloys.

-

Indirect emissions from electricity consumption. CBAM requires that electricity used in the production process be attributed to the goods produced. For installations connected to a national grid, the emissions intensity of electricity is calculated using either supplier-specific data or grid-average emission factors. For installations with on-site power generation, emissions are monitored at the installation level and attributed to production.

-

Emissions from precursor materials. For steel products made from purchased semi-finished goods (such as hot-rolled coil converted into cold-rolled coil), the embedded emissions of the precursor material must be included in the total. This requires supply-chain coordination: the exporter must obtain emissions data from the precursor supplier and ensure that data is verified to CBAM standards.

The data must be collected continuously throughout the reporting period. For imports in 2026, the reporting period is the full calendar year of 2026. As the CO2-IQ guide explains, "For imports in 2026, the full calendar year of 2026 needs to be covered. These producers must collect data according to a monitoring plan, report this data to accredited verifiers and obtain a compliant verification report." [3]

The monitoring plan is the foundational document. It specifies which emissions sources are included, which monitoring methodology is used, and how emissions are attributed to production processes. The plan must be documented before the reporting period begins. Installations that did not have a monitoring plan in place by January 1, 2026, are now collecting data retroactively, which creates gaps in the audit trail and increases the risk of verification failure.

The verification bottleneck in 2026

The CBAM Regulation requires that embedded emissions calculated using actual values be verified by an accredited verifier. Verification must follow the principles set out in Annex VI of the CBAM Regulation and the detailed requirements in Implementing Regulation 2025/2546. The verification standard is reasonable assurance, the same level of assurance required for EU Emissions Trading System installations. [4]

Reasonable assurance means the verifier must determine, with a high but not absolute level of confidence, that the emissions data is free from material misstatements and material non-conformities. The materiality threshold for CBAM verification is set at 5 percent of total specific embedded emissions per tonne of goods. If the verifier identifies misstatements or non-conformities exceeding this threshold, the verification report cannot be issued until the operator corrects the data.

Physical site visits are mandatory in 2026. As the CarbonGlance compliance alert explains, "Physical installation visits by verifiers are mandatory unless specific criteria for waiving this requirement are met. This ensures verifiers can assess operations firsthand rather than relying solely on documentation." [5] The site visit requirement creates a capacity constraint. Accredited verifiers must travel to production installations in India, Turkey, Vietnam, and China to conduct on-site audits. The number of accredited verifiers with experience in steel production and availability to travel to non-EU installations in Q1 and Q2 2026 is limited. Exporters who did not contract a verifier before January 2026 are now competing for the remaining verification slots in Q3 and Q4 2026.

The verification cycle takes 8 to 12 weeks from the initial site visit to the issuance of the verification report. The timeline includes: site visit and document review (1 to 2 weeks), draft verification report and operator review (2 to 3 weeks), resolution of findings and non-conformities (2 to 4 weeks), and final report issuance (1 week). If the verifier identifies material misstatements during the site visit, the timeline extends by an additional 4 to 6 weeks while the operator recalculates emissions and provides corrected data.

Verification reports issued in 2026 can be transmitted to the EU importer via the CBAM Registry or by other means. The electronic EU template for verification reports became available in the CBAM Registry in January 2027, so reports issued in 2026 are submitted as PDF documents. The importer uploads the verification report to the CBAM Registry as part of the annual CBAM declaration, which is due by May 31, 2027, for calendar year 2026 imports.

The commercial consequence for non-EU exporters

The default-value penalty is not borne by the exporter directly. The EU importer is the CBAM declarant, the entity legally responsible for purchasing CBAM certificates and submitting the annual declaration. But the commercial consequence flows upstream. EU importers who pay inflated certificate costs based on default values will push that cost back onto the exporter through one of three mechanisms:

-

Direct price reductions. The importer deducts the CBAM certificate cost from the purchase price paid to the exporter. If the certificate cost using default values is €109,272 per 500-tonne shipment, but the certificate cost using actual emissions is €67,824, the importer reduces the purchase price by €41,448 per shipment to offset the penalty.

-

Contractual requirements for verified data. The importer includes a clause in the supply contract requiring the exporter to provide third-party verified emissions data for all shipments. If the exporter cannot provide verified data by a specified deadline, the contract includes a price adjustment clause or a right of termination.

-

Supplier substitution. The importer sources from an alternative supplier who can provide verified actual emissions data. This is the most severe outcome. The exporter loses the EU market entirely, not because of product quality or price, but because of CBAM compliance capability.

The iFactory CBAM compliance guide for steel exporters notes that "Steel exporters shipping to the EU must now provide installation-level embedded emissions data calculated using EU-prescribed methodologies. EU importers must obtain Authorized CBAM Declarant status, submit verified annual declarations, and purchase CBAM certificates at EU ETS carbon prices—currently averaging €65–80 per tonne of CO₂. Non-compliance triggers penalties of €100 per undeclared tonne with no cap." [6]

The penalty for undeclared emissions is separate from the default-value penalty. If the EU importer fails to declare embedded emissions at all, or declares emissions below the actual quantity imported, the importer faces a penalty of €100 per tonne of undeclared CO₂. This penalty applies whether the importer used actual emissions or default values. But the penalty is in addition to the cost of purchasing CBAM certificates for the undeclared emissions. The total financial exposure for non-compliance is the sum of the certificate cost, the undeclared-emissions penalty, and any additional administrative fines imposed by the CBAM authority.

For non-EU exporters, the strategic question is whether to invest in installation-level monitoring and verification infrastructure, or accept the commercial consequence of default values. The Climate Leadership Council's CBAM guide observes that "Producers seeking to avoid the use of default values must monitor emissions at each installation, allocate emissions to specific production processes, and attribute emissions to individual goods. Actual emissions data must be verified by accredited third parties to ensure compliance with EU standards." [7]

The investment in monitoring and verification is not trivial, but the payback is immediate. At Q1 2026 certificate prices, the annual penalty for a 10,000-tonne-per-year exporter relying on default values is €828,960. The cost of implementing installation-level monitoring and securing third-party verification is €50,000 to €80,000 in the first year, including verifier fees, monitoring equipment, and internal labor. The payback period is four to six weeks. In subsequent years, the cost drops to €20,000 to €40,000 annually for ongoing monitoring and verification.

How Emission3 fits

Emission3 is built for non-EU exporters who need to move from default values to verified actual emissions in a single compliance cycle. The platform starts with document-first ingestion: we pull production records, utility bills, fuel purchase invoices, and process emissions data directly from your existing systems. The deterministic LLM layer maps those documents to CBAM-compliant monitoring categories, attributes emissions to specific production processes, and calculates embedded emissions per tonne of goods using the methodology in Implementing Regulation 2025/2547.

The output is not a carbon accounting dashboard. It is an auditor-ready evidence pack: a monitoring plan, a calculation lineage that traces every tonne of CO₂ back to the source document, and a pre-verification report that follows the structure of the EU verification template. When your accredited verifier conducts the site visit, they review the evidence pack, not your internal spreadsheets. The verification cycle compresses from 12 weeks to 6 weeks, because the verifier spends less time reconstructing your calculation methodology and more time testing the accuracy of your source data.

For steel exporters, Emission3 handles the three categories of installation-level data: direct emissions from production processes, indirect emissions from electricity, and emissions from precursor materials. The platform integrates with your ERP system to pull production quantities and fuel consumption in real time, with your utility provider to pull electricity consumption and grid emission factors, and with your procurement system to pull invoices for purchased semi-finished goods. The monitoring is continuous, not retroactive. Every tonne of steel produced in January 2026 is monitored according to a CBAM-compliant methodology, so the data is verification-ready when your verifier arrives in Q2 2026.

The platform also forecasts the financial impact of switching from default values to actual emissions. For every shipment to the EU, Emission3 calculates the CBAM certificate cost using both actual emissions and default values, and surfaces the penalty per tonne. That calculation becomes the commercial justification for investing in verification: the penalty avoided exceeds the verification cost by 10x to 20x in the first year.

Most exporters we work with achieve operational CBAM compliance in 8 to 12 weeks. Phase 1 covers installation mapping, emissions data collection, and methodology configuration. Phase 2 deploys supplier data management for precursor materials, certificate cost forecasting, and CBAM Registry integration. Phase 3 focuses on verification preparation: producing the monitoring plan, the calculation lineage, and the evidence pack the verifier needs to issue a reasonable assurance opinion. The platform integrates with your existing ERP and sustainability reporting systems, so you are not replacing infrastructure—you are adding a compliance layer on top of it. See how we handle CBAM compliance for non-EU exporters. [8]

What to do in Q3 2026

If you are a non-EU steel exporter shipping to the EU, and your EU importers are currently declaring your shipments using default values, you have until Q4 2026 to implement installation-level monitoring and secure third-party verification for calendar year 2026. The verification report must be submitted to the EU importer by May 31, 2027, as part of the annual CBAM declaration. If you miss that deadline, your importers pay the default-value penalty for the full year, and you negotiate the commercial consequence in Q3 2027 during the next contract renewal cycle.

The first step is to map every production installation to the CBAM goods produced at that site. For integrated steel mills, this means identifying which blast furnaces, basic oxygen furnaces, and rolling mills produce the specific goods shipped to the EU. For electric arc furnace operators, this means documenting the electricity consumption and scrap inputs for each furnace, and attributing those inputs to the finished goods.

The second step is to collect twelve months of emissions data for calendar year 2026. This includes fuel consumption records, electricity invoices, process emissions calculations, and purchased goods invoices for any precursor materials. The data must be collected according to a monitoring plan that specifies the monitoring methodology and the attribution rules for each production process.

The third step is to contract an accredited verifier who can conduct a site visit in Q3 or Q4 2026. Verification capacity is constrained, and verifiers with availability in the second half of 2026 are prioritizing operators who have already implemented monitoring plans and collected baseline data. If you approach a verifier in Q4 2026 with no monitoring plan and incomplete data, the verification timeline extends into Q1 2027, which means the verification report will not be ready for the May 2027 CBAM declaration deadline.

The fourth step is to produce the evidence pack the verifier needs to issue a reasonable assurance opinion. This includes the monitoring plan, the calculation lineage, and the source documents that support every emissions calculation. The verifier will test a sample of production records and utility bills to confirm that your monitoring methodology is being applied consistently. If the verifier finds gaps or inconsistencies, they will issue findings, and you will need to correct the data and provide additional evidence before the verification report can be issued.

The Carra Globe CBAM trade analysis notes that "Exporters who invest in third-party verified emissions data pay only their actual carbon cost rather than conservative default values. The difference is significant. Default values are set to reflect the worst-case emissions for each country and product type with a markup. An Indian steel producer using direct reduced iron technology with natural gas may have actual emissions well below the country default. If that producer can provide accredited third-party verification of their actual embedded emissions, their EU buyers pay substantially less in CBAM certificates than competitors sourcing from producers who rely on defaults." [9]

The default-value penalty is not a compliance risk—it is a commercial risk. EU importers will continue to declare your shipments, whether you provide verified actual emissions or not. But the importers who pay the penalty will renegotiate the cost, and the exporters who cannot provide verified data will lose market access to competitors who can. The window to avoid that outcome is Q3 and Q4 2026. Book a CBAM readiness call to map your installations, gaps, and implementation timeline. [10]

References & Sources

External Sources

- [1]CBAM reporting requirements & Compliance Guide for 2026

Clean Carbon AI's guide to CBAM reporting requirements, explaining why default values always result in higher carbon tax than actual emissions and the deliberate design to discourage their use.

- [2]EU CBAM Emissions Data: Monitoring, Reporting & Verification

CO2-IQ's explanation of the top-down approach for calculating specific embedded emissions under CBAM, from installation-level monitoring to production process attribution to goods-level conversion.

- [3]EU CBAM Emissions Data: Monitoring, Reporting & Verification

CO2-IQ's documentation of the 2026 reporting period requirement for CBAM imports, specifying that producers must collect full calendar year data according to monitoring plans.

- [4]EU CBAM Verification: What Companies Need to Know Before 2026

CarbonGlance's overview of CBAM verification requirements, including reasonable assurance standards, materiality thresholds, and the end of unverified data in the definitive phase.

- [5]EU CBAM Verification: What Companies Need to Know Before 2026

CarbonGlance's explanation of mandatory physical installation visits by accredited verifiers in 2026 and the conditions under which visits may be waived in subsequent years.

- [6]EU CBAM Compliance Guide for Steel Exporters: 2026 Definitive Period

iFactory's compliance guide for steel exporters entering the CBAM definitive phase, covering installation-level data requirements, certificate costs at EU ETS prices, and non-compliance penalties.

- [7]A Guide to the EU CBAM

Climate Leadership Council's comprehensive CBAM guide, detailing the monitoring, reporting, and verification requirements for producers seeking to avoid default values.

- [9]EU CBAM 2026: How Carbon Border Rules Are Changing Export Costs and Trade Routes

Carra Globe's analysis of CBAM cost calculations and the competitive advantage for exporters who invest in third-party verified emissions data versus reliance on conservative default values.

Related Content

- [8]How Emission3 handles CBAM

Emission3's CBAM solution for non-EU exporters, showing the document-first ingestion flow, deterministic calculation lineage, and auditor-ready evidence pack that compresses verification cycles from 12 weeks to 6 weeks.

- [10]Book a CBAM readiness call

Schedule a CBAM readiness conversation with Emission3. We map your production installations, identify gaps in monitoring and verification infrastructure, and provide an implementation timeline to move from default values to verified actual emissions.