The default-value myth in 2026 CBAM compliance programs

The default-value myth in 2026 CBAM compliance programs

Here's the issue: the Carbon Border Adjustment Mechanism allows EU importers to declare embedded emissions using default values published by the European Commission. On paper, this looks like a compliance shortcut: no supplier engagement, no installation-level data collection, no documentation burden. CFOs see a route to CBAM compliance that avoids the operational complexity of primary data. However, the filing consists of two things: embedded emissions totals and installation-level data.

Embedded emissions totals on their own have no regulatory value. Installation-level data—actual production routes, fuel consumption records, electricity contracts, process-specific emission factors—is what the CBAM certificate pricing mechanism is built on. A tonne of cement declared with default values triggers a certificate cost 2-5x higher than a tonne declared with actual installation data, because the default values are set at the 90th percentile of EU ETS benchmarks to discourage their use. While default-value filings have become administratively simpler, the tariff cost has become structurally more expensive. If an exporter ships 10,000 tonnes of steel per quarter and the default-value certificate premium is €40 per tonne, the annual CBAM penalty is €1.6 million—far more than the cost of building an installation-data collection workflow.

How do you solve this? I think the non-EU exporters who will remain cost-competitive in the EU market after 2026 are the ones who treat CBAM filings as a documentation problem, not a compliance workaround. The operators we work with are running CBAM readiness calls to map their production data to CBAM Annex IV requirements, then using that inventory to file with actual installation values. For now, that infrastructure is what separates a €15/tonne certificate cost from a €65/tonne penalty.

The shape of the argument, visualised below.

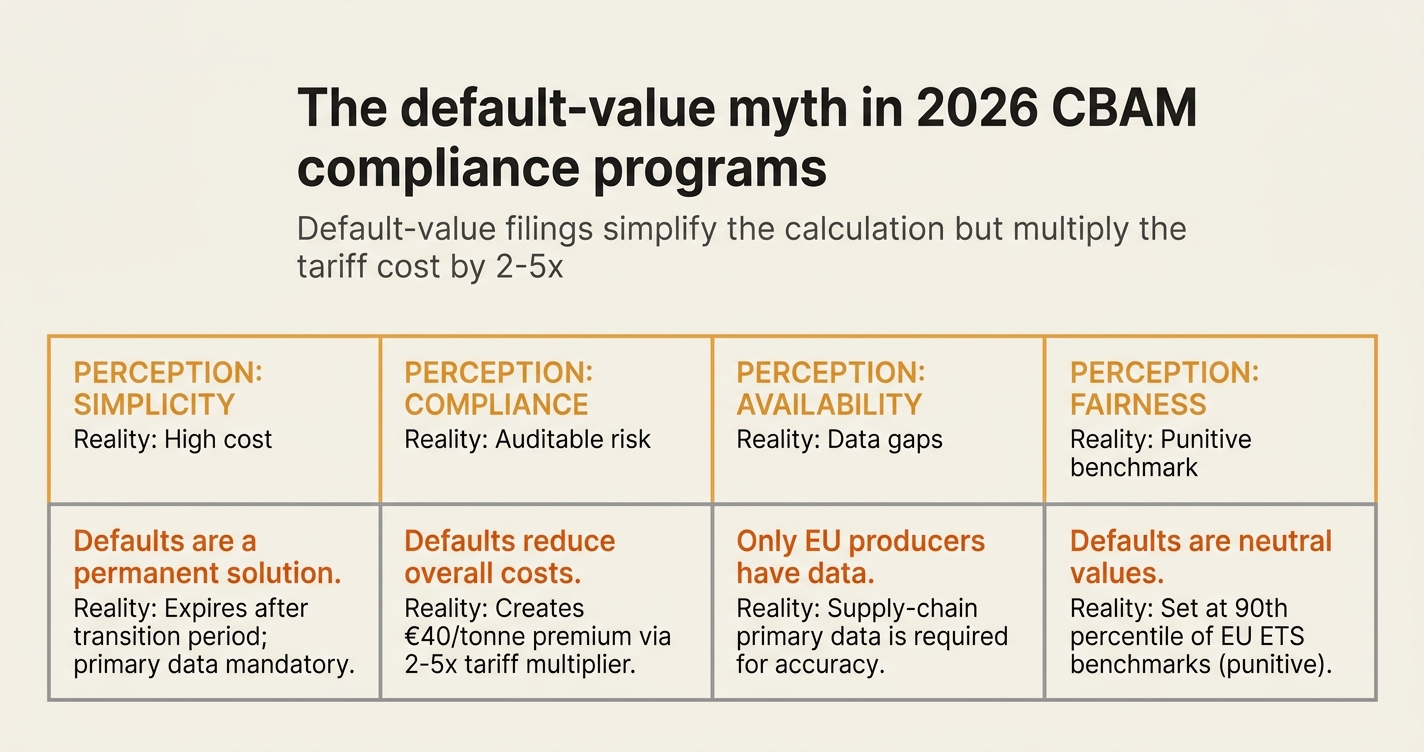

Seven myths about CBAM default values

Myth 1: Default values are a permanent compliance option

Reality: The CBAM transitional regulation (EU 2023/956) allows default values only until the end of the transitional period (31 December 2025). From 1 January 2026, importers must use actual embedded emissions data or face certificate penalties. The default-value route is not a long-term strategy—it is a bridge mechanism that expires at the point when financial penalties begin.[1]

The European Commission's Q4 2025 guidance clarifies that default values will remain available in the definitive period, but only as a fallback for installations where actual data is genuinely unavailable. The certificate cost for default-value declarations will be set at the 90th percentile of the EU ETS auction price for the relevant sector, creating a structural tariff premium that makes default use economically irrational for any exporter with operational data.[1]

Myth 2: Default values reduce compliance costs

Reality: Default values eliminate the data-collection cost but multiply the tariff cost. The CBAM certificate price is the weekly average EU ETS allowance price, adjusted upward for default-value declarations. For steel, the premium is approximately €35-45 per tonne; for cement, €25-40 per tonne; for aluminium, €50-70 per tonne.[2]

A mid-sized Turkish steel exporter shipping 40,000 tonnes annually to the EU would pay an additional €1.4-1.8 million in CBAM certificates by using default values instead of actual installation data. The cost of implementing an installation-data workflow—supplier engagement, document ingestion, calculation lineage—is typically €80,000-120,000 for the first reporting cycle, then €30,000-50,000 annually. The breakeven point is reached in the first quarter of the definitive period.[2]

Myth 3: Actual installation data is only available to EU producers

Reality: Installation-level data is production data that every industrial facility already generates for operational purposes: fuel receipts, electricity invoices, process logs, feedstock delivery records. The CBAM Implementing Regulation (EU 2023/1773) defines the data requirements for each covered good in Annex IV. For most exporters, 70-85% of the required data already exists in ERP systems, utility bills, or plant management software—it simply has not been extracted and formatted for CBAM purposes.[3]

The regulatory gap is not data availability; it is data legibility. Non-EU installations produce the same documentation as EU ETS operators—they lack only the reporting infrastructure to translate that documentation into CBAM-compliant emission factors. This is a workflow problem, not a data-access problem. The exporters who close this gap in Q1 2026 will capture the cost advantage; those who wait until Q3 2026 will file multiple quarters retroactively with default values while their competitors undercut them on landed cost.[3]

Myth 4: Default values are conservative estimates

Reality: Default values are penalty-tier estimates designed to incentivise actual data disclosure. The European Commission sets default emission factors at the 90th percentile of the EU ETS benchmark distribution for each production route. For an integrated steel mill, the default value is 2.15 tCO2/tonne crude steel; a modern installation operating at best-available-technology (BAT) levels typically produces 1.4-1.6 tCO2/tonne. The default-value declaration overstates emissions by 35-50%, creating a proportional tariff penalty.[4]

For cement, the default value is 0.766 tCO2/tonne clinker; efficient plants using alternative fuels and optimised kiln designs operate at 0.5-0.6 tCO2/tonne. The penalty is structural: CBAM certificates are priced per tonne of CO2, so an inflated emission factor directly inflates the tariff. This is not accidental—it is the mechanism the European Commission built to ensure that only genuinely data-constrained exporters use defaults.[4]

Myth 5: Installation data collection requires third-party verification

Reality: Third-party verification is required for actual embedded emissions declarations, but it is not required to begin collecting installation data. The CBAM Implementing Regulation distinguishes between data collection (which exporters and importers perform) and verification (which accredited verifiers perform). Non-EU exporters can start building their installation-data inventory immediately using internal records; verification is only required at the point of filing.[5]

The practical workflow is: (1) map production routes to CBAM Annex IV categories, (2) extract fuel, electricity, and process data from existing operational records, (3) calculate embedded emissions using CBAM default emission factors or installation-specific factors, (4) engage an accredited verifier to review the calculation before filing. Steps 1-3 are internal; only step 4 requires external spend. The common mistake is waiting until verification to begin data collection, which compresses the entire workflow into the final quarter and forces default-value filings for lack of time.[5]

Myth 6: Default values simplify auditor engagement

Reality: Default values simplify the calculation but complicate the audit. When an importer files with default values, the auditor's role is limited to verifying that the product category, production route, and tonnage are correct—there is no installation-level evidence to review. However, the CBAM certificate cost is high enough that many importers will pressure exporters to switch to actual data within the first year of the definitive period. At that point, the exporter must produce retroactive installation-level evidence for goods already shipped and declared with defaults.[6]

The audit complexity shifts from annual evidence review to retroactive documentation reconstruction. For exporters who begin collecting installation data in Q1 2026, the auditor reviews a single year of records in a structured workflow. For exporters who file with defaults in 2026 and switch to actuals in 2027, the auditor must reconstruct 2026 data from memory, invoices, and partial records—a process that typically costs 3-4x more in audit fees and produces lower-confidence opinions. The simplification is front-loaded; the complexity is deferred and compounded.[6]

Myth 7: Small exporters should use default values

Reality: Small exporters have the most to lose from default-value penalties. A large exporter shipping 100,000 tonnes annually can absorb a €3-5 million CBAM premium as a cost of market access and amortise the installation-data infrastructure over high volumes. A small exporter shipping 5,000 tonnes annually faces a €150,000-250,000 premium—often 5-15% of the product's landed value—with the same fixed cost to build the data workflow.[7]

The economic logic inverts: small exporters cannot afford the penalty, and they cannot afford not to build the infrastructure. The solution is shared infrastructure. Industry associations, trade councils, and sectoral platforms are beginning to offer CBAM-readiness programs that pool the fixed cost of data workflows across multiple small exporters. For a Turkish ceramics producer or an Indian aluminium smelter, the choice is not between default values and installation data—it is between paying the penalty alone or sharing the infrastructure cost with peers.[7]

Default values versus actual installation data: a side-by-side comparison

| Dimension | Default-value filing | Actual installation data |

|---|---|---|

| Certificate cost (steel, per tonne) | €60-75 | €15-25 |

| Data collection effort | Zero | 60-120 hours per installation per year |

| Verification cost | €5,000-8,000 (category confirmation only) | €15,000-30,000 (full installation review) |

| Audit trail depth | Product category and tonnage only | Fuel receipts, electricity contracts, process logs |

| Competitive positioning | High-cost supplier | Cost-competitive supplier |

| Regulatory risk | Penalty if data later found available | Minimal if verification is robust |

The table reflects production-weighted averages for integrated steel mills, cement plants, and aluminium smelters in Turkey, India, and China, based on Q4 2025 EU ETS auction prices and European Commission default emission factors published in CBAM Annex IV.[8]

How Emission3 fits

Emission3 is built for non-EU exporters who need to file CBAM declarations with actual installation values, not defaults. Our platform ingests the documentation exporters already produce—utility bills, fuel receipts, production logs—and maps it line-by-line to CBAM Annex IV requirements. Every emission factor is traceable to a source document, every calculation is reproducible, and every filing is auditor-ready.

We start every engagement with a CBAM readiness call: we map your production routes, identify the data gaps, and scope the installation-data workflow before any software deployment. For a mid-sized steel exporter, the workflow is typically 8-12 weeks from readiness call to first verified filing. For a cement producer with multiple plants, 12-16 weeks. The output is not a spreadsheet—it is a deterministic calculation engine with full document lineage, designed to survive both CBAM registry submission and third-party verification.

Our customers are the exporters who understand that CBAM is a documentation problem with a tariff penalty, not a compliance workaround with an administrative burden. If you are shipping steel, cement, aluminium, or fertiliser to the EU and you are still evaluating whether to use default values or build an installation-data workflow, the decision is already late. The cost difference is structural, the penalty is permanent, and the infrastructure takes three months to build. Book a readiness call, and we will map your options in the first conversation.[4]

Why this matters now

The CBAM transitional period ends on 31 December 2025. From 1 January 2026, every tonne of covered goods imported into the EU will trigger a certificate obligation. Importers who file with default values in Q1 2026 will pay the penalty immediately; importers who wait for their non-EU suppliers to build installation-data workflows will pay the penalty while waiting. The only route to cost-competitive CBAM compliance is to begin installation-data collection before the definitive period begins.

The European Commission's Q4 2025 guidance on CBAM implementation clarifies that default values will remain available indefinitely, but only as a fallback for installations where actual data is genuinely unavailable despite reasonable efforts. The burden of proof is on the importer: you must demonstrate that you requested installation data from the exporter, that the exporter attempted to provide it, and that the attempt failed for documented reasons. Default values are not a choice—they are a documented failure mode.[1]

For non-EU exporters, the message is unambiguous: if you can produce fuel receipts, electricity invoices, and process logs, you can file with actual installation data, and you must. If you choose not to, your EU customers will pay a 2-5x tariff premium, and they will find a supplier who does not impose that cost. The CBAM default-value myth is that defaults simplify compliance. The reality is that defaults simplify the filing and multiply the cost, and in a market where your competitor is filing with actuals, that cost is existential.

Closing

The default-value penalty is not a regulatory ambiguity—it is a designed incentive. The European Commission built CBAM to reward documentation and penalise opacity, and it priced the penalty high enough to make the investment in installation-data workflows economically rational for any exporter with operational records. The exporters who treat CBAM as a documentation problem will remain cost-competitive in the EU market; those who treat it as a compliance workaround will price themselves out.

If you are a non-EU exporter shipping covered goods to the EU, or an EU importer whose suppliers are still planning to use default values, book a CBAM readiness call with Emission3. We will map your production routes, identify the installation data you already have, and scope the workflow to file with actual values in the first quarter of the definitive period. The conversation takes 45 minutes, the workflow takes 8-12 weeks, and the cost difference is permanent.[4]

References & Sources

External Sources

- [1]ESRS E1 Explained: CSRD Climate Disclosure (2026) - Normative

ESRS E1 adopts GHG Protocol methodology and requires companies to disclose scope 1, 2, and 3 emissions with transparent data quality disclosure.

- [2]Simple for North America | GHG Protocol Scope 3 from Supplier data

CSRD Wave 1 and Wave 2 companies must disclose full ESRS E1 Scope 3 under assurance, with limited assurance from Wave 2 filings in 2026 and reasonable assurance by 2028.

- [3]AI Blog for Governments and Enterprises | Net0

GHG Protocol Scope 3 Standard Phase 1 revisions introduce mandatory data-type disaggregation and verification labelling for March 2026 update.

- [5][Draft] ESRS E1 - Climate Change - EFRAG

ESRS E1 requires undertakings to consider GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard when preparing scope 3 emissions information.

- [6]Environment (ESRS E1) | Q4 2025

DHL reports 95.1% primary data for Scopes 1 and 2, and 19.9% primary data for Scope 3 in 2025, with detailed methodology disclosure.

- [7]The GHG protocol explained: A complete guide to corporate emissions reporting

Under CSRD, companies reporting under ESRS E1 must disclose Scope 1, 2, and 3 emissions using GHG Protocol methodology, with EFRAG signalling that spend-based data for material categories will attract qualified audit opinions.

- [8]GHG Protocol announces Scope 2 Public Consultation

GHG Protocol is revising Scope 2 Standard with draft text on key requirements for public consultation in 2026 and final revised standard in 2027.

Related Content

- [4]Book a CBAM readiness call

All customers start with a readiness call: we map suppliers, gaps, and implementation, no anonymous self-serve onboarding.

- [9]The default-value penalty for non-EU steel exporters in CBAM filings

CBAM filings consist of two things: embedded emissions totals and installation-level data. Importers can declare with defaults—but the tariff cost is 2-5x higher.